Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

Chapter 22

Master Budgets and Planning

QUESTIONS

1. A written budget helps managers plan and control a business by 1) communicating

and 5) motivate employees.

2. Management controls operations by benchmarking against some norm. A

3. Continuous budgeting provides managers a full set of updated budgets each time a

5. Budgeting can be a strong positive motivating force if employees are involved or

consulted in the process. This participation promotes their commitment to reaching

6. Budgeting helps management coordinate and plan business activities by providing

7. The sales budget reflects the expected sales to be made over a period of time, stated

8. A selling expense budget is a plan of the expenses to be incurred to produce the

planned amount of sales. The capital expenditures budget lists dollar amounts of

9. In participatory budgeting, some employees might understate sales and/or overstate

10. A cash budget shows the planned cash receipts and cash payments for each budget

period, including any loans to be received or repaid. Since the operating budgets

11. A production budget shows the number of units to be produced each budget period.

12. A manager of an Apple store would have responsibility for and decision control over

13. With the exception of the decision to operate, the manager of a Samsung

distribution center is not likely to engage in a substantial amount of long-term

14.

Budget Participant

Description

Sales manager ………………..

Information on estimated sales (units and dollars).

Production manager ………..

Number of units to produce based on estimated sales.

of production.

Sales manager ………………..

Cost of selling the estimated sales level.

strative managers ……………

committee ………………………

to carry on business activities.

15. The bottle redesign will reduce the amount and total cost of glass used, thus

lowering direct materials costs on the direct materials budget. The lighter-weight bottle

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1205

QUICK STUDIES

Quick Study 22-1 (10 minutes)

Quick Study 22-2 (10 minutes)

Quick Study 22-3 (5 minutes)

Quick Study 22-4 (10 minutes)

Grace

Sales Budget

For Month Ended June 30

Prior month’s unit sales ………………………………………………………………

1,000

1,040

1206

Quick Study 22-5 (10 minutes)

Zilly Co.

Selling Expense Budget

For Month Ended June 30

Budgeted sales …………………………………………………………………………..

$400,000

Sales commission percent ………………………………………………………….

Sales commissions …………………………………………………………………….

Projected selling expense for June ……………………………………………..

Quick Study 22-6 (10 minutes)

Liza’s

Budgeted Cash Receipts

For Month Ended June 30

Budgeted sales …………………………………………………………………………..

$52,000

1207

Quick Study 22-7 (10 minutes)

ZORTEK CORP.

Direct Materials Budget

For Month Ended January 31

Budget production (units) ……………………………………………………………

400

Add budgeted ending inventory (200* units x 5 lbs. per unit x 40%) ….

Deduct beginning inventory (lbs.) ………………………………………………..

Quick Study 22-8 (5 minutes)

TORA CO.

Direct Labor Budget

For Month Ended July 31

Budget production (units) ……………………………………………………………

1,020

2,040

1208

Quick Study 22-9 (10 minutes)

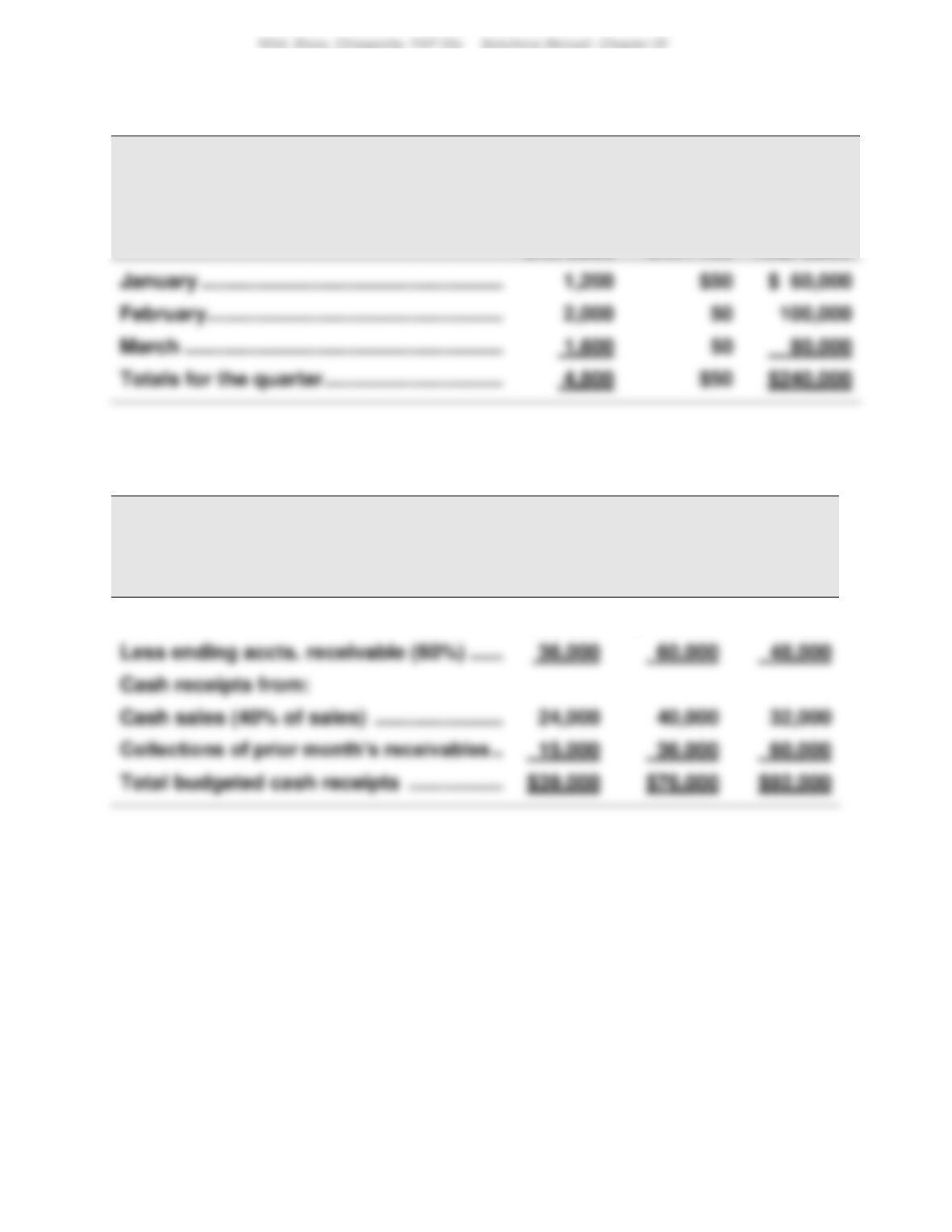

SCORA INC.

Sales Budget

For January, February, and March

Budgeted

Unit Sales

Budgeted

Unit Price

Budgeted

Total Sales

$ 60,000

Quick Study 22-10 (10 minutes)

X-TEL

Cash Receipts Budget

For April, May, and June

April

May

June

Sales ……………………………………………………..

$60,000

$100,000

$80,000

1209

Quick Study 22-11 (10 minutes)

X-TEL

Selling Expense Budget

For April, May, and June

April

May

June

Budgeted sales ……………………………………..

$60,000

$100,000

$80,000

Sales commission percent …………………….

Sales commissions ………………………………

Sales manager monthly salary ……………….

Quick Study 22-12 (10 minutes)

CHAMP, INC.

Production Budget

For Month Ended May 31

Next month’s budgeted sales (units) ……………………………………………

200

120

300

1210

Quick Study 22-13 (10 minutes)

MIAMI SOLAR

Direct Materials Budget

For Month Ended July 31

Budgeted production (units, given) ……………………………………………..

5,000

Quick Study 22-14 (10 minutes)

MIAMI SOLAR

Direct Labor Budget

For Month Ended July 31

Budgeted production…………………………………………………………………..

5,000

1211

Quick Study 22-15 (10 minutes)

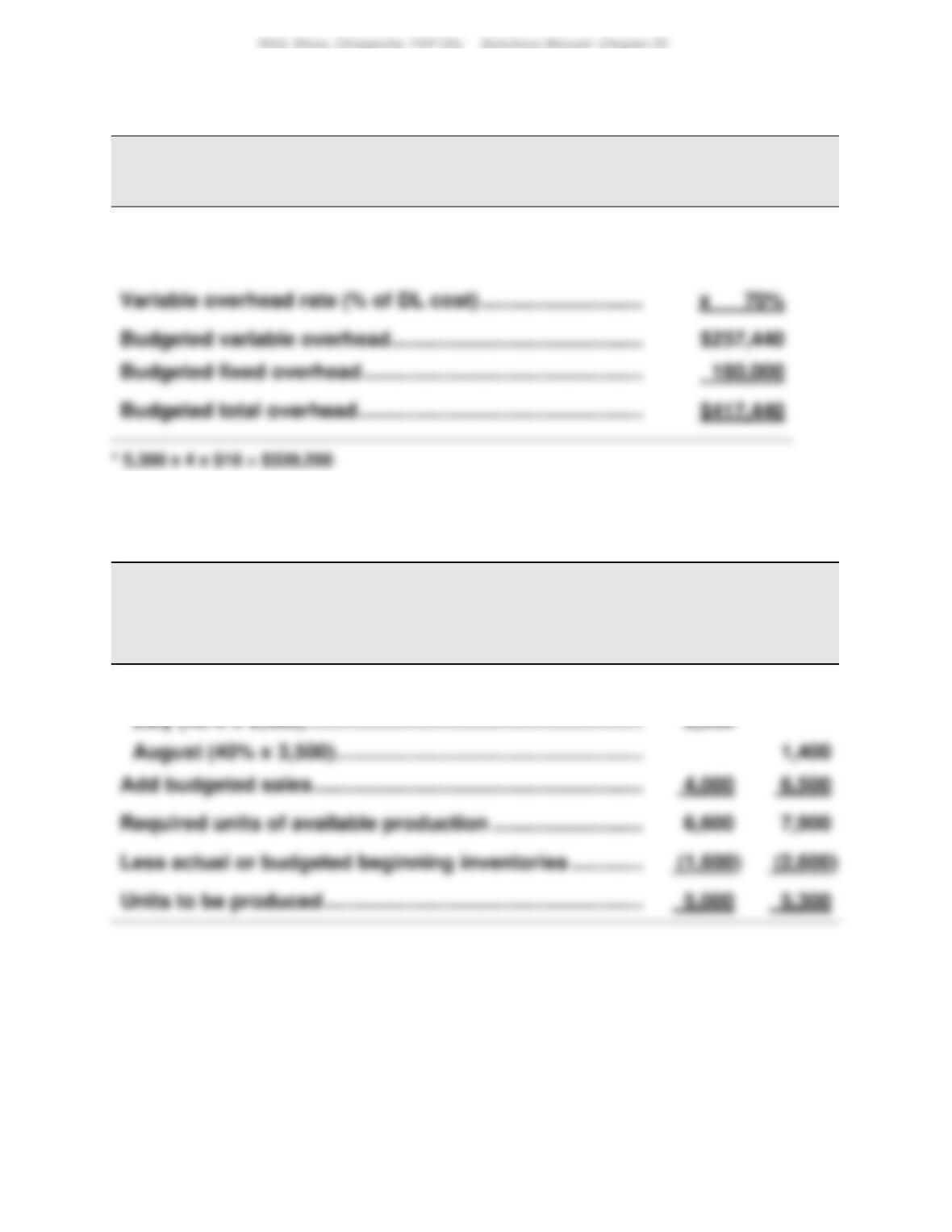

MIAMI SOLAR

Factory Overhead Budget

For Month Ended August 31

Total budgeted direct labor* ……………………………………………

$339,200

Budgeted variable overhead ……………………………………………

Quick Study 22-16 (15 minutes)

ATLANTIC SURF

Production Budget

July and August

July

August

Budgeted ending inventories

1212

Quick Study 22-17 (15 minutes)

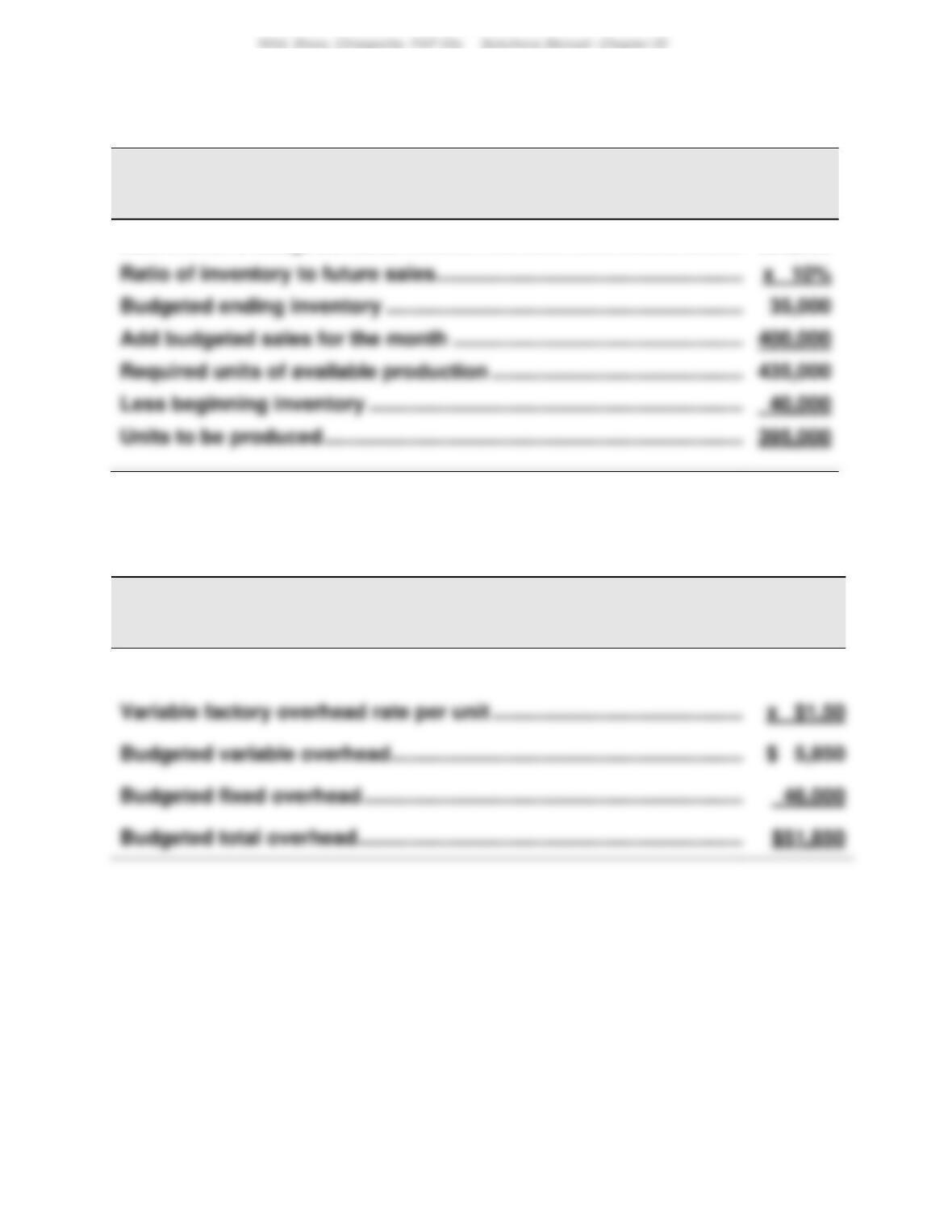

Forrest Company

Production Budget

For Month Ended November 30

Next month’s budgeted sales ………………………………………………………

350,000

400,000

435,000

Quick Study 22–18 (15 minutes)

Hockey Pro

Factory Overhead Budget

For Month Ended May 31

Units to be produced ………………………………………………………………….

3,900

1213

Quick Study 22-19 (10 minutes)

MUSIC WORLD

Cash Receipts Budget

For Month Ended September 30

Cash receipts from September cash sales (40% x $170,000) …………

Quick Study 22-20 (10 minutes)

THE GUITAR SHOPPE

Cash Receipts Budget

For Month Ended September 30

Cash receipts from August sales (55% x $150,000) ………………………

Total budgeted cash receipts ………………………………………………………

Quick Study 22-21 (10 minutes)

WELLS COMPANY

Budgeted Cash Receipts

For Month Ended November 30

Cash receipts from November cash sales (25% x $80,000) ……………

$ 20,000

Total budgeted cash receipts ………………………………………………………

$ 65,100

1214

Quick Study 22-22 (15 minutes)

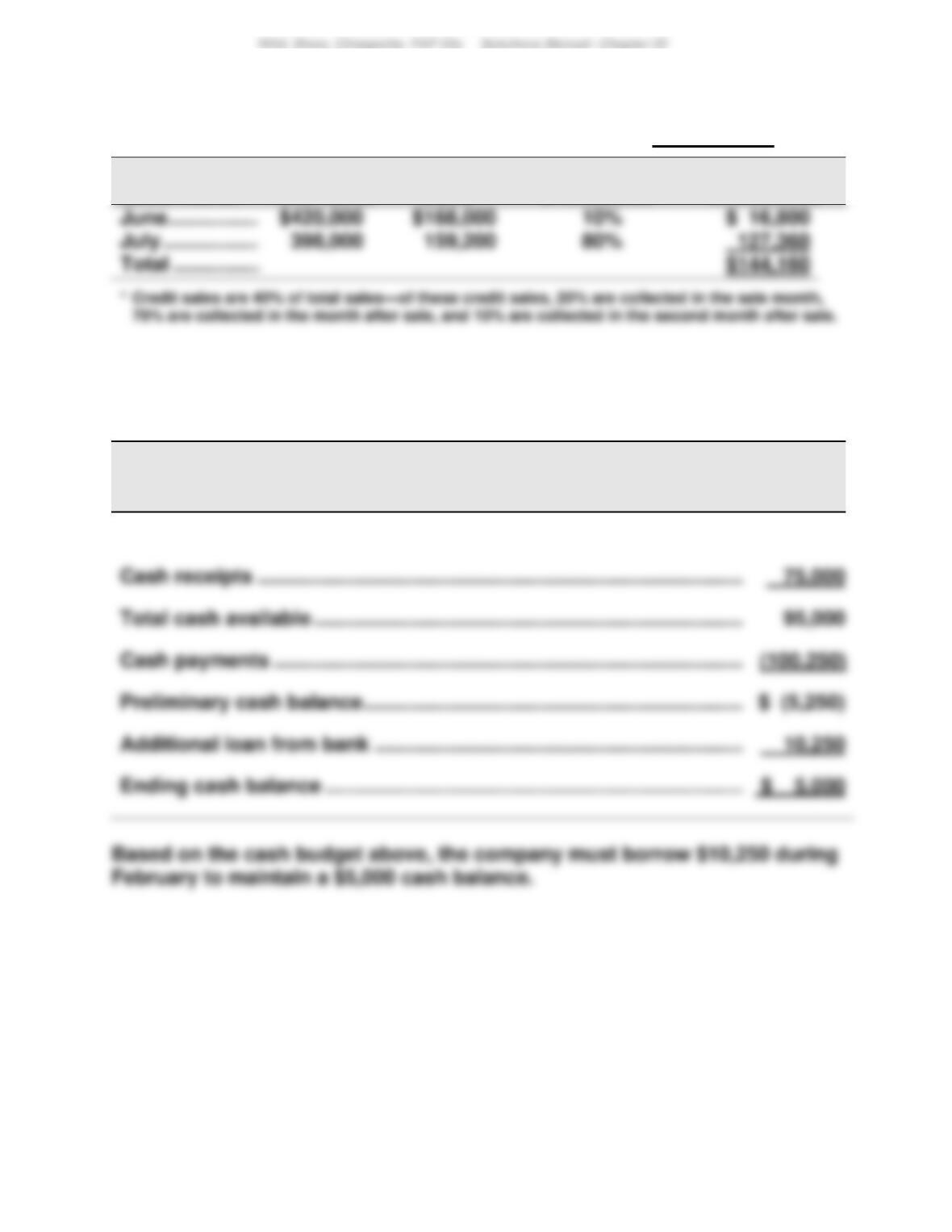

Computation of budgeted Accounts Receivable balance as of July 31

Sales month

Total Sales

Credit

Sales*

Percent Still

Uncollected*

Amount

Uncollected

Quick Study 22-23 (5 minutes)

SANTOS CO.

Cash Budget

For Month Ended February 28

Beginning cash balance ………………………………………………………………

$ 20,000

Cash payments …………………………………………………………………………..

Additional loan from bank …………………………………………………………..

1215

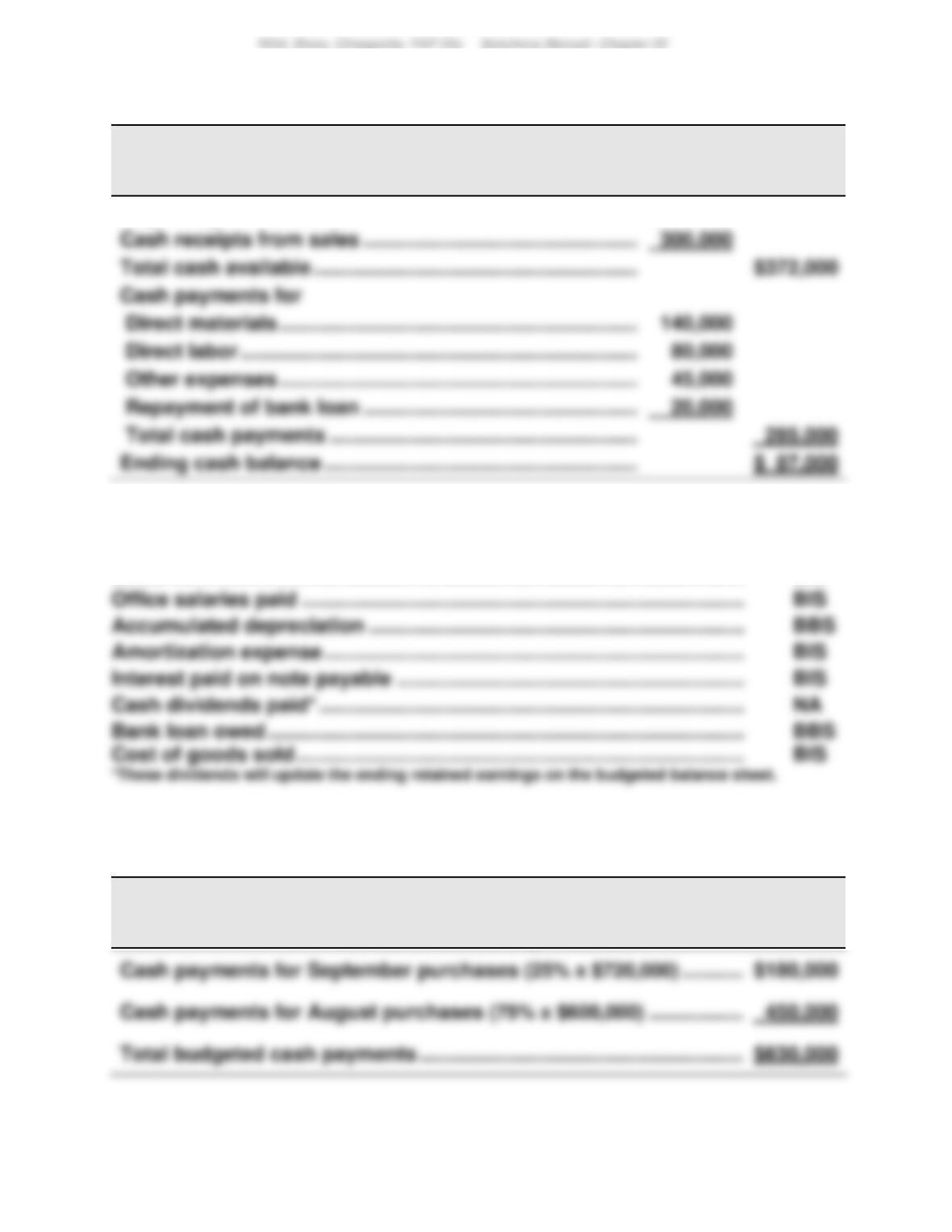

Quick Study 22-24 (15 minutes)

GADO COMPANY

Cash Budget

For Month Ended March 31

Beginning cash balance ………………………………………………….

$ 72,000

Quick Study 22-25 (10 minutes)

Sales ……………………………………………………….………………………………… BIS

Quick Study 22-26 (10 minutes)

GARDA

Cash Payments for Merchandise (Budgeted)

For Month Ended September 30

1216

Quick Study 22-27 (10 minutes)

TORRES CO.

Cash Payments for Merchandise (Budgeted)

For January, February, and March

January

February

March

Purchases ……………………………………………..

$15,800

$18,600

$20,200

Cash payments for

$ 6,320

$ 7,440

$ 8,080

Quick Study 22-28 (5 minutes)

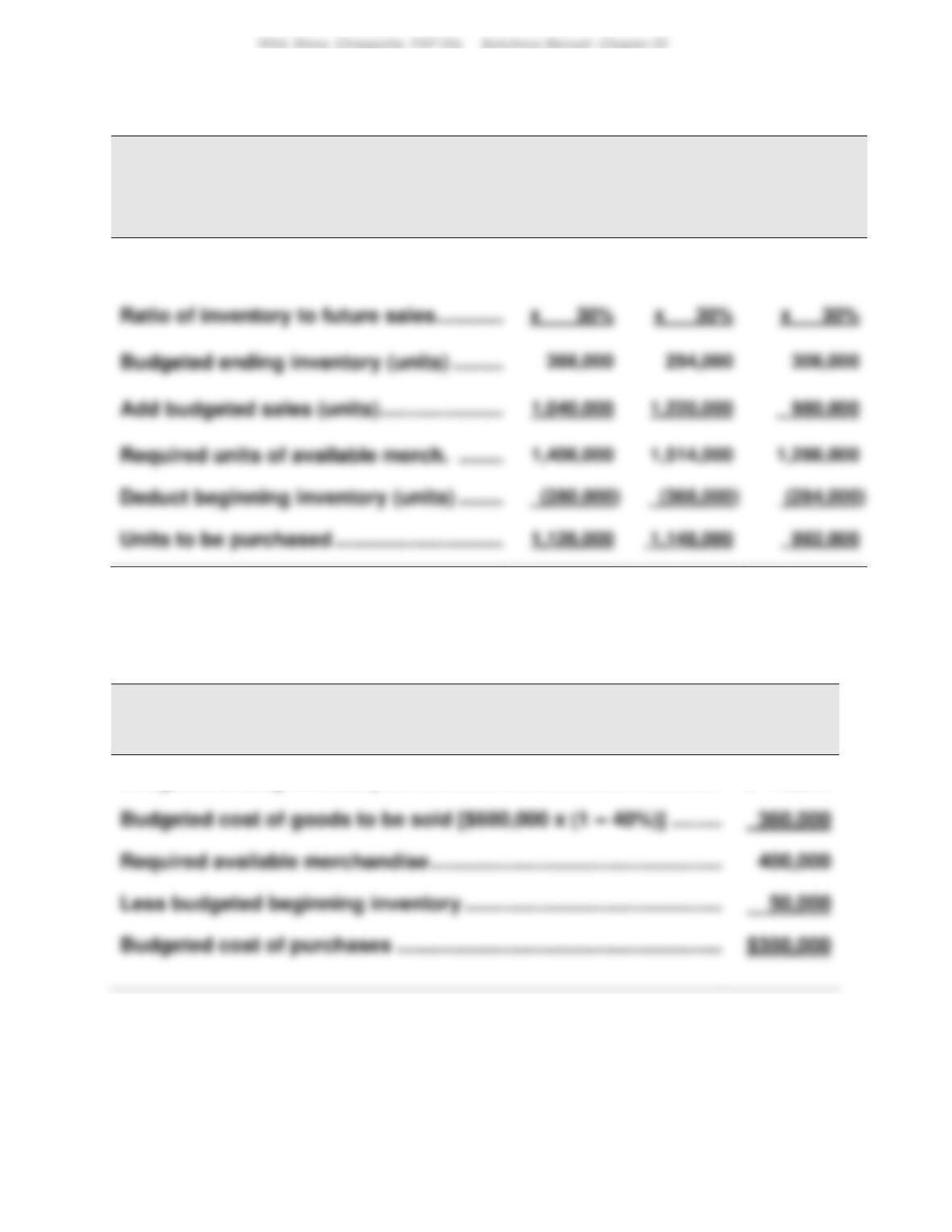

RAIDER-X COMPANY

Purchases Budget (in units)

For Month Ended April 30

Budgeted ending inventory (130% x 3,000) …………………………………..

3,900

1217

Quick Study 22-29 (15 minutes)

LEXI COMPANY

Merchandise Purchases Budget

For April, May, and June

April

May

June

Next month’s budgeted sales (units) ………

1,220,000

980,000

1,020,000

Quick Study 22-30 (15 minutes)

MONTEL COMPANY

Computation of Budgeted Cost of Purchases

For Month Ended July 31

Budgeted ending inventory ……………………………………………………….

$ 40,000

1218

Quick Study 22-31 (10 minutes)

1. Activity-based budgeting requires managers to focus on the activities of

2. Traditional budgeting consists of listing the amount of resources

Quick Study 22-32 (10 minutes)

1.

(in € millions)

2.

Note: Assume budgeted sales of €25,000 for this question.

1219

Quick Study 22-33 (10 minutes)

1.

2.

Shipping costs ($32,400 x 3%) ………………………………………..

$ 972

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1220

EXERCISES

Exercise 22-1 (5 minutes)

Exercise 22-2 (10 minutes)

Exercise 22-3 (15 minutes)

RUIZ CO.

Production Budget

For April, May, and June

April

May

June

Next month’s budgeted sales (units) ………

580

540

620

155

1221

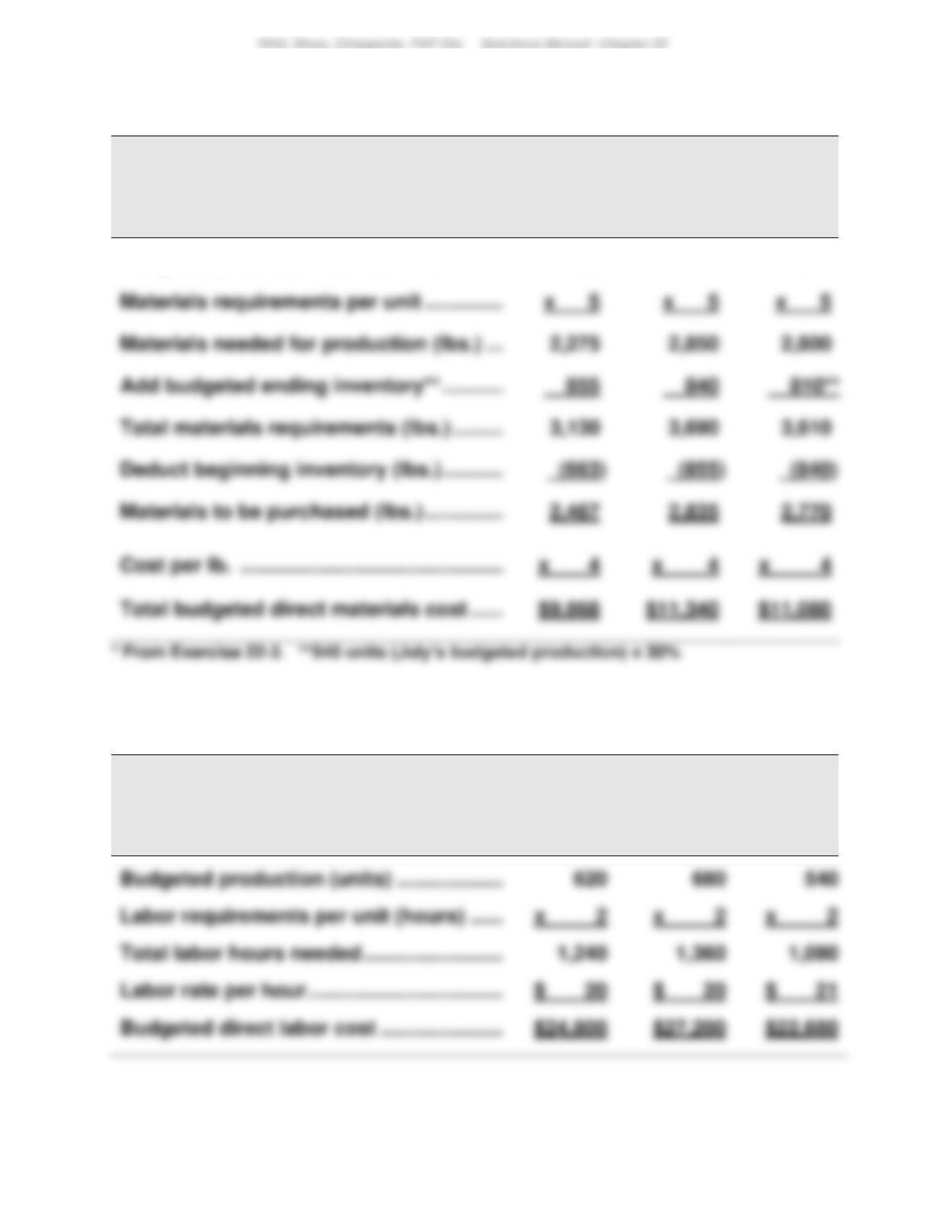

Exercise 22-4 (15 minutes)

RUIZ CO.

Direct Materials Budget

For April, May, and June

April

May

June

Budgeted production (units)* …………………

455

570

560

Materials needed for production (lbs.) ……

Exercise 22-5 (10 minutes)

MANNER COMPANY

Direct Labor Budget

For July, August, and September

July

August

Sept.

1222

Exercise 22-6 (15 minutes)

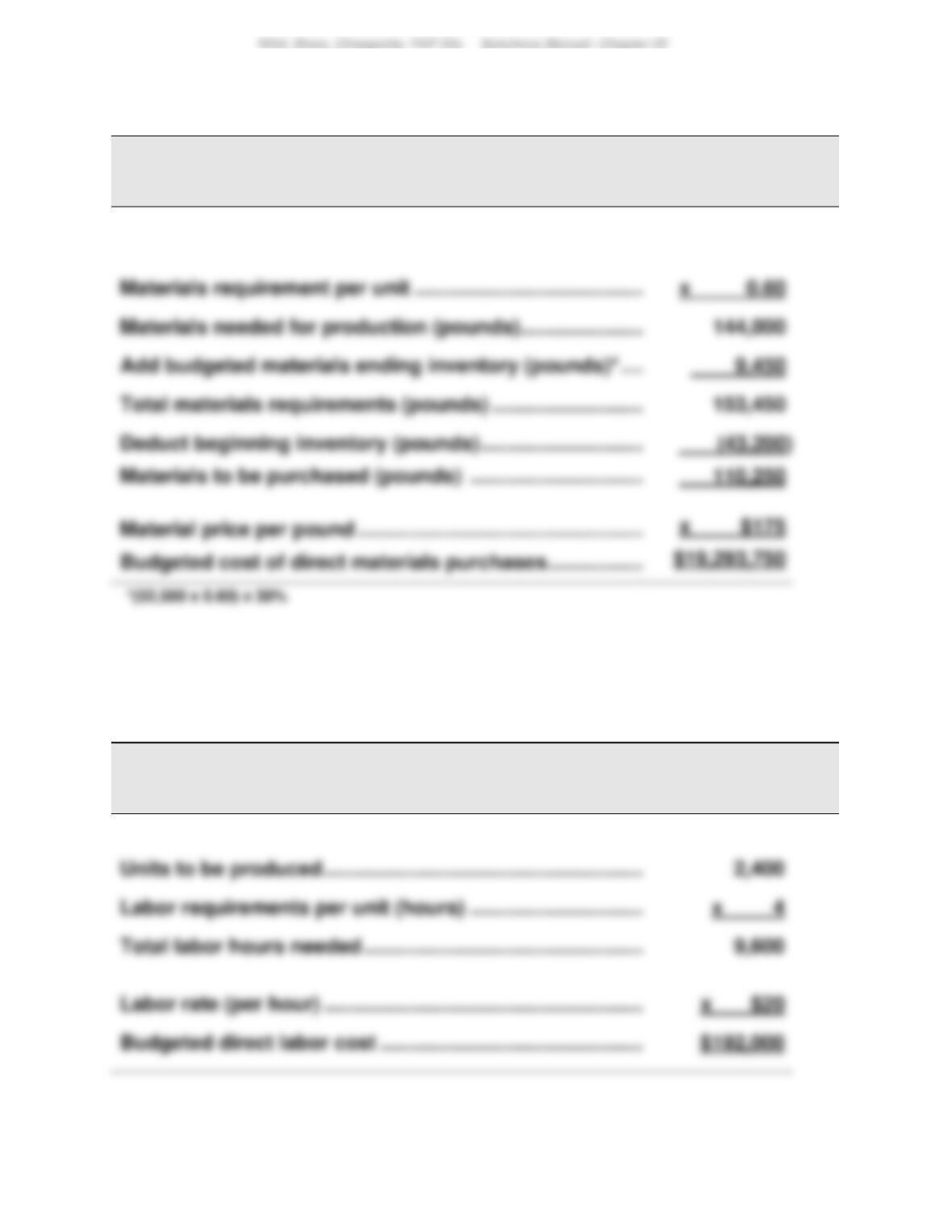

RIDA INC.

Direct Materials Budget

Second Quarter

Units to be produced ………………………………………………………

240,000

Exercise 22-7 (15 minutes)

1.

ADDISON CO.

Direct Labor Budget

Second Quarter

Exercise 22-7 (continued)