CHAPTER 22

SOLUTIONS TO EXERCISES—SET B

EXERCISE 22-1B

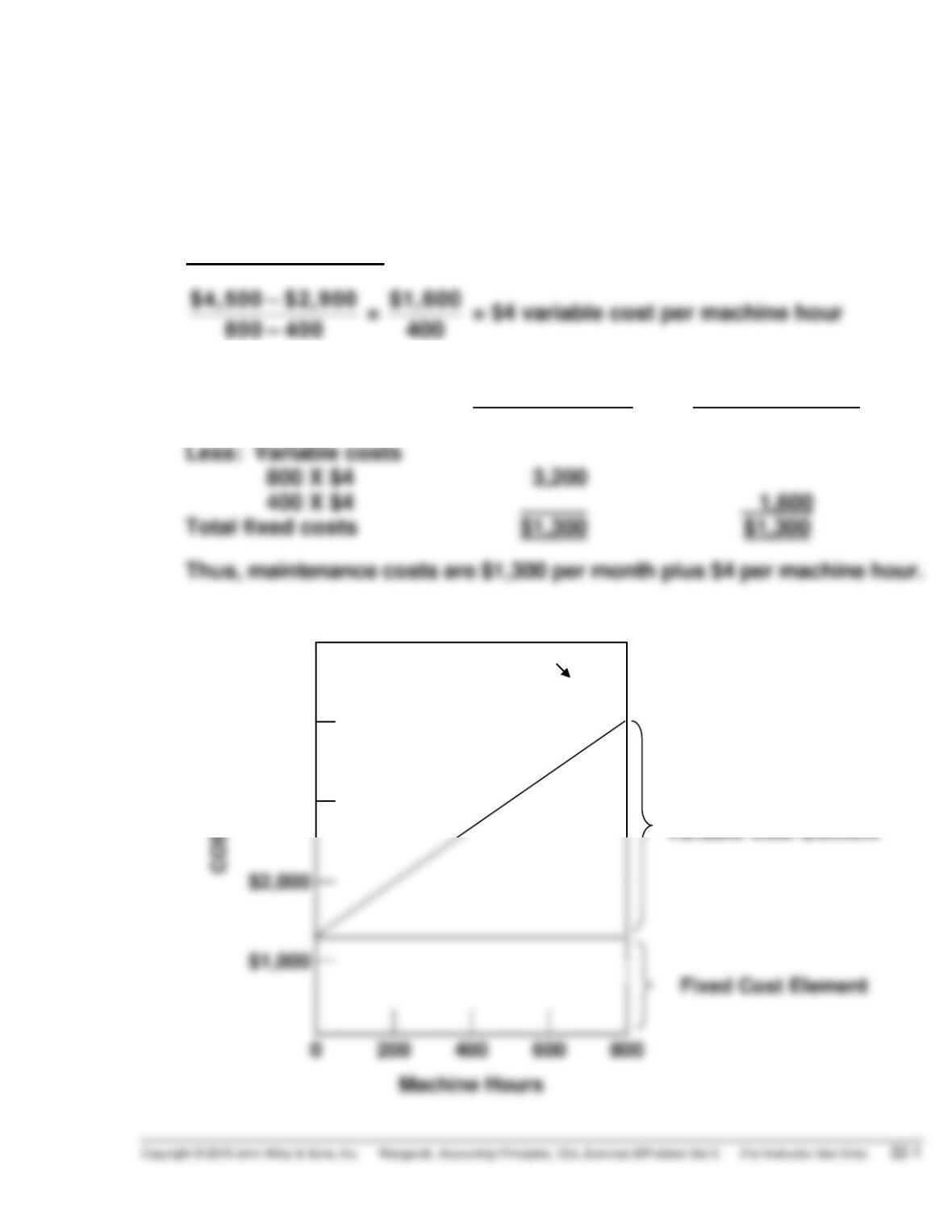

(a) Maintenance Costs:

$4,500 – $2,900

800 – 400

=

$1,600

400

= $4 variable cost per machine hour

800

Machine Hours

400

Machine Hours

Total costs

$4,500

$2,900

(b)

$5,000

Total Cost Line

$4,000

$4,000

$3,000

EXERCISE 22-2B

(a)

Contribution margin per lawn

Contribution margin per lawn

=

=

$70 – ($15 + $7 + $6)

$42

(b) Break-even point in dollars = 120 lawns X $70 per lawn

= $8,400 per month

EXERCISE 22-3B

(1)

Contribution margin per room

Contribution margin per room

=

=

$120 – ($32 + $40)

$48

(2) Break-even point in dollars = 375 rooms X $120 per room

EXERCISE 22-4B

(a) Contribution margin in dollars: Sales = 600 X $90 = $54,000

Variable costs = $54,000 X .60 = 32,400

Contribution margin $21,600

EXERCISE 22-5B

(a)

(1) Contribution margin ratio is:

$43,200

= 75%

$57,600

Break-even point in dollars =

(2) Round-trip fare =

(b) At the break-even point fixed costs and contribution margin are equal.

Therefore, the contribution margin at the break-even point would be

$18,000.

$18,000

$18,000

EXERCISE 22-6B

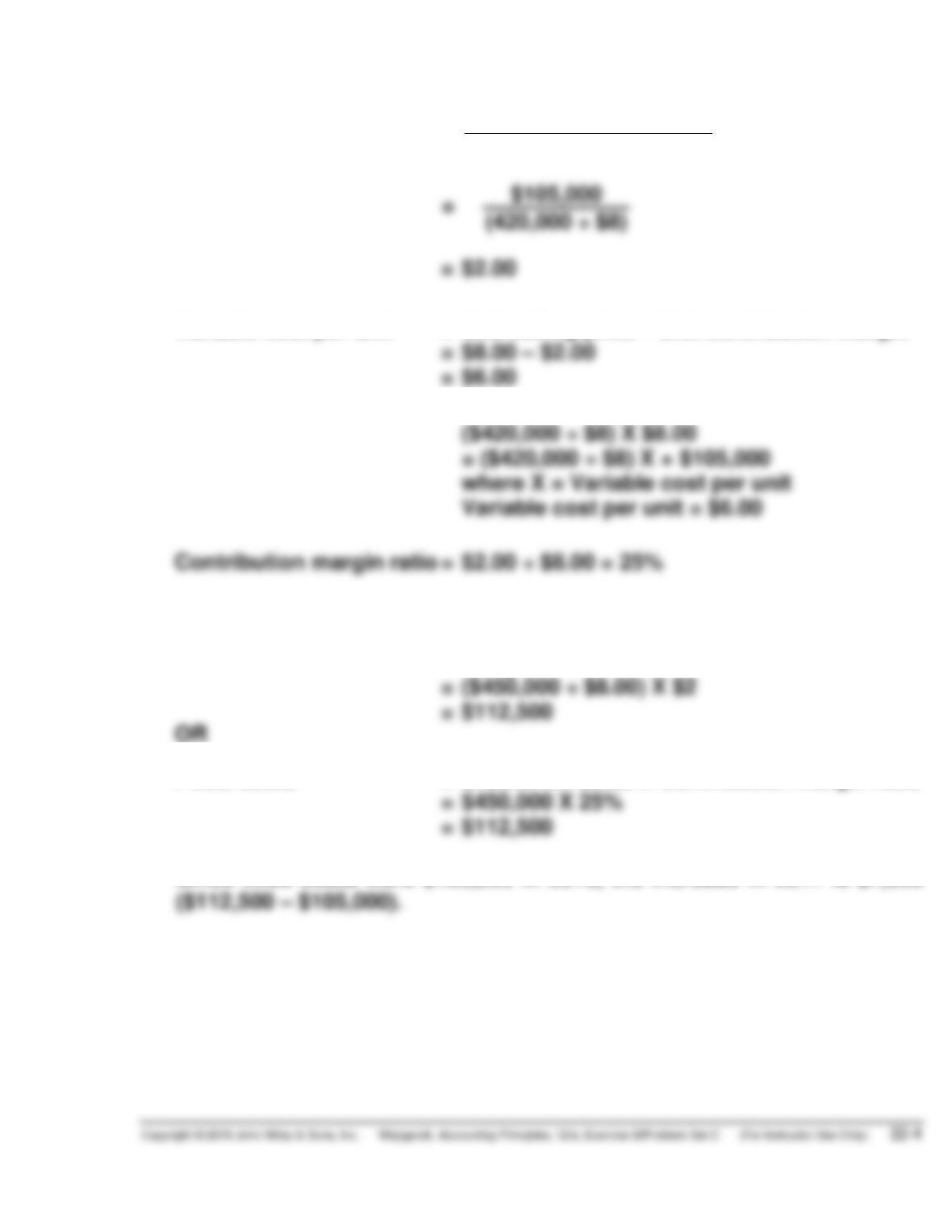

(a) Unit contribution margin =

units in sales Breakeven

costs Fixed

Variable cost per unit = Unit selling price – Unit contribution margin

OR

= ($420,000 ÷ $8) X $8.00

Contribution margin ratio = $2.00 ÷ $8.00 = 25%

(b) Fixed costs = Breakeven sales in units X Unit contribution

margin

Fixed costs = Breakeven sales X Contribution margin ratio

Since fixed costs were $105,000 in 2016, the increase in 2017 is $7,500

EXERCISE 22-7B

(a) AMBER COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

Total

Per Unit

Sales (720 video game consoles) ……………… $360,000 $500

Variable costs …………………………………………. 252,000 350

(b) Sales = Variable costs + Fixed costs

(c) AMBER COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

Total

Per Unit

Sales (480 video game consoles) ……………… $240,000 $500

EXERCISE 22-8B

(a) Sales = Variable cost + Fixed cost + Target net income

(b) Units needed in 2017 =

$540,000 + $162,000*

= 7,800 units

$180 − $90

(c)

$540,000 + $162,000

= 7,000 units, where X = new selling price

X − $90

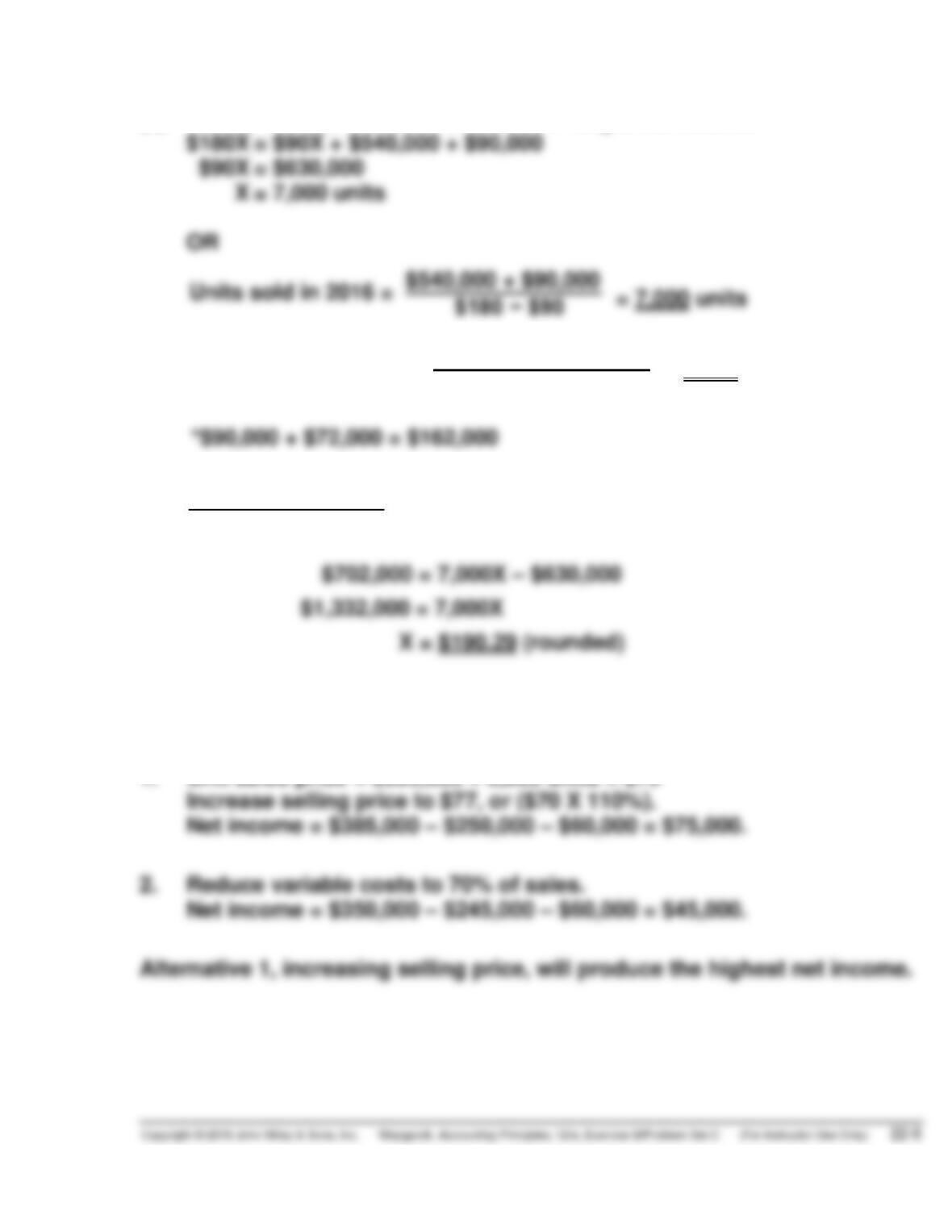

EXERCISE 22-9B

1. Unit sales price = $350,000 ÷ 5,000 units = $70

Increase selling price to $77, or ($70 X 110%).

Net income = $385,000 – $250,000 – $60,000 = $75,000.

EXERCISE 22-10B

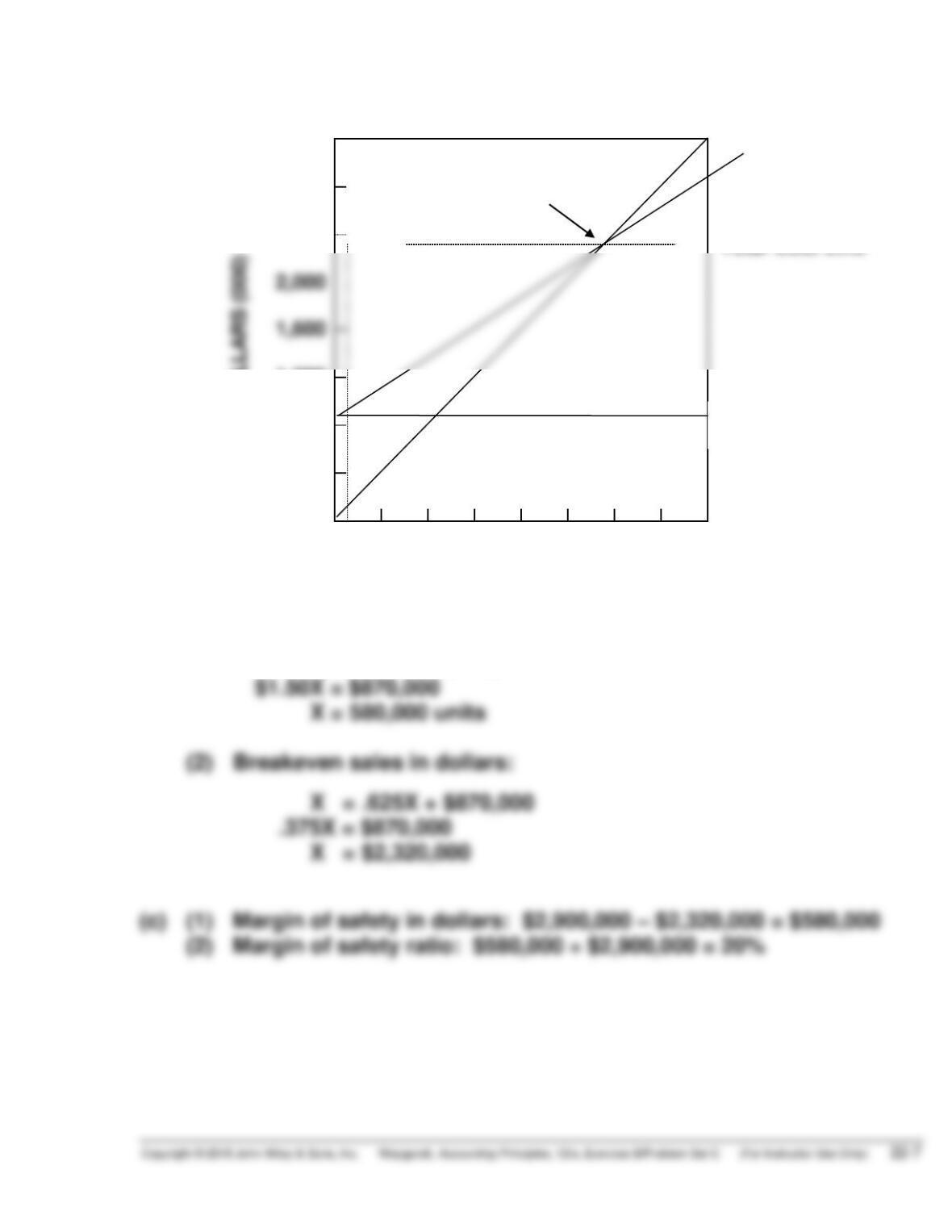

(a)

$3,200

Sales Line

DOLLARS (000)

2,800

Breakeven Point

2,400

Total Cost Line

1,600

1,200

800

Fixed Cost Line

400

100

200

300

400

500

600

700

800

Number of Units (in thousands)

(b) (1) Breakeven sales in units:

$4X = $2.50X + $870,000

EXERCISE 22-11B

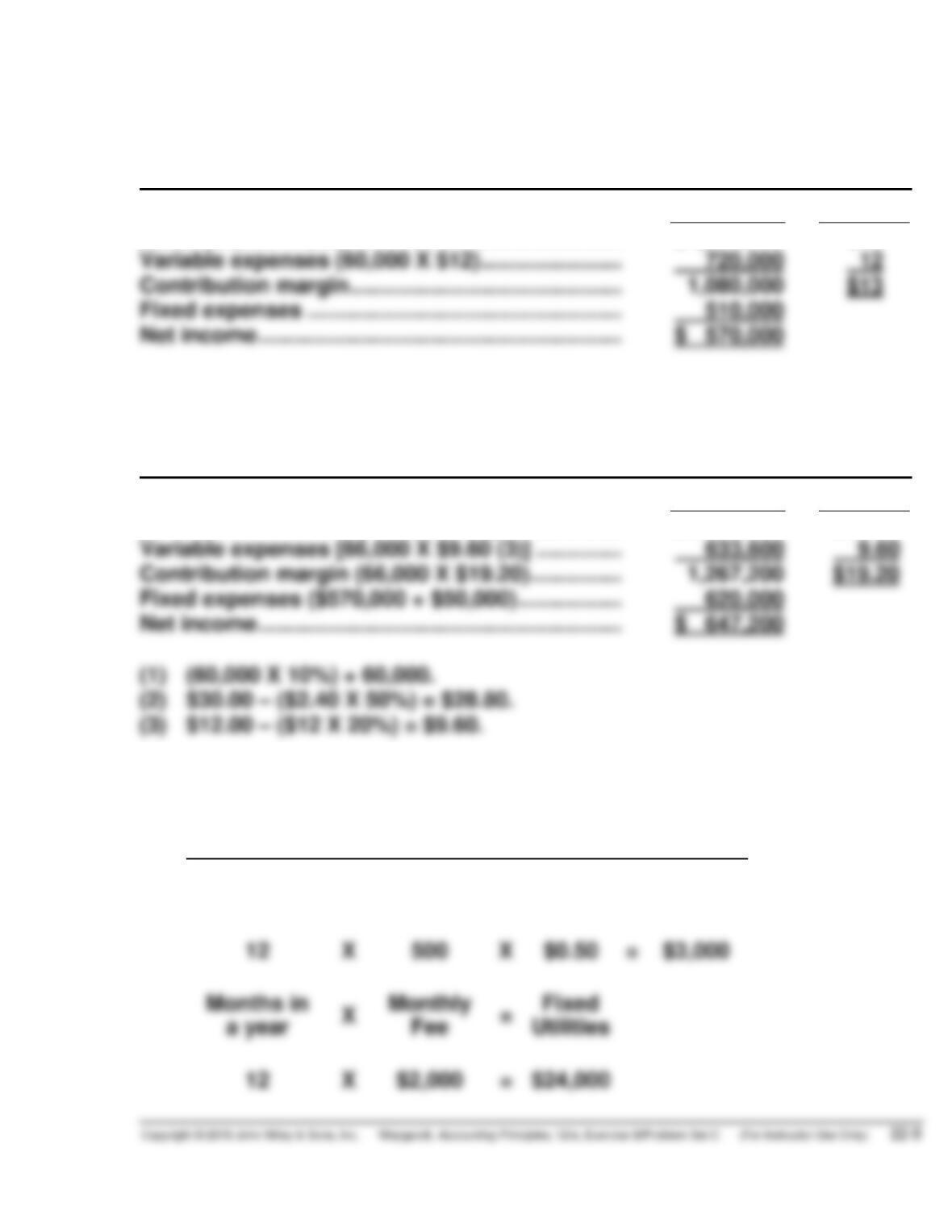

VALERO COMPANY

CVP Income Statement (Current)

For the Year Ended December 31, 2017

Total

Per Unit

Sales (60,000 X $30) …………………………………….. $1,800,000 $30

Variable expenses (60,000 X $12) ………………….. 720,000 12

VALERO COMPANY

CVP Income Statement (with Changes)

For the Year Ended December 31, 2017

Total

Per Unit

Sales [66,000 units (1) X $28.80 (2)] ………………. $1,900,800 $28.80

Variable expenses [66,000 X $9.60 (3)] ………….. 633,600 9.60

*EXERCISE 22-12B

(a)

Utility Expense

Months in

a year

X

Kilowatt

hours

X

Hourly

Charge

=

Variable

Utilities

*EXERCISE 22-12B (Continued)

Variable Costing

Labor:

Crate builders

$37,000

Material:

Wood

54,000

Variable Overhead:

Utilities

Nails

Total manufacturing costs

$94,350

(b)

Absorption Costing

Labor:

Crate builders

$ 37,000

Material:

Wood

54,000

Variable overhead:

Utilities

Nails

Fixed overhead:

Utilities

Rent

25,000

Total manufacturing costs

$143,350

(c) The entire difference in costs between the two methods is due to the

fact that fixed overhead is included as part of manufacturing costs

*EXERCISE 22-13B

(a) TALLY CORPORATION

Income Statement

For the Month Ended October 31, 2017

(Absorption Costing)

Sales (22,000 X $45) ……………………………………………. $990,000

Cost of goods sold (22,000 X $37*) ………………………. 814,000

(b) TALLY CORPORATION

Income Statement

For the Month Ended October 31, 2017

(Variable Costing)

Sales (22,000 X $45) …………………………………………… $990,000

Variable cost of goods sold (22,000 X $29)………….. 638,000

(c) Under variable costing, all fixed manufacturing costs ($200,000) are

expensed. Under absorption costing, some of the fixed manufacturing

SOLUTIONS TO PROBLEMS—SET C

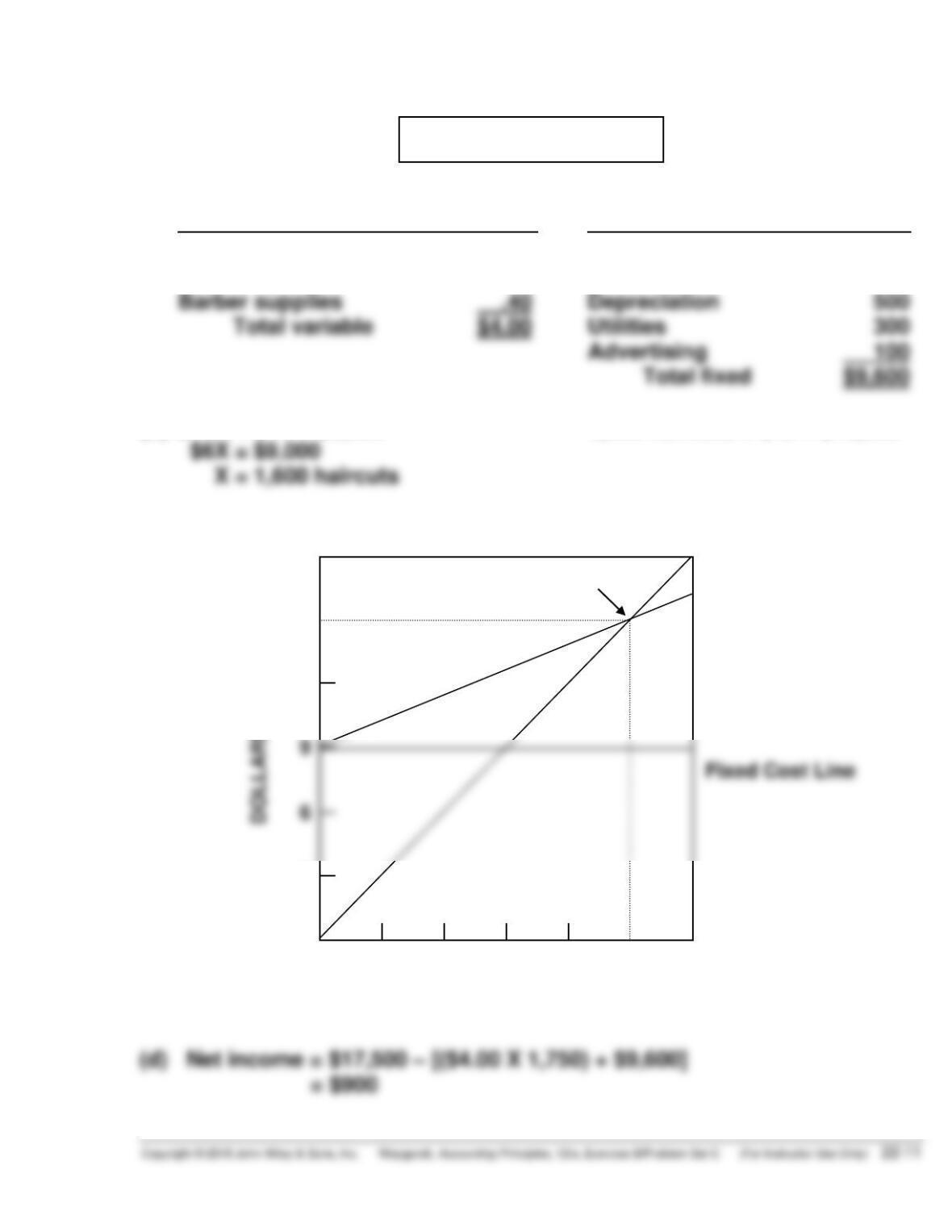

PROBLEM 22-1C

(a)

Variable costs (per haircut)

Fixed costs (per month)

Total variable $4.00

Utilities 300

Barbers’ commission $3.00

Rent .60

Barbers’ salaries $8,000

Rent 700

(b)

X = 1,600 haircuts

$10X = $4X + $9,600

1,500 haircuts X $10 = $15,000

(c)

18

Sales Line

Total Cost Line

6

Breakeven Point

15

12

3

300

600

900

1,200

1,500

1,800

Number of Haircuts

PROBLEM 22-2C

(a) FRUITY-ADE COMPANY

CVP Income Statement (Estimated)

For the Year Ending December 31, 2017

Net sales …………………………………………. $2,000,000

Variable expenses

Cost of goods sold ……………………. $1,220,000 (1)

Fixed expenses

Cost of goods sold ……………………. 236,000

Selling expenses ………………………. 150,000

(1) Direct materials $360,000 + direct labor $590,000 + variable manufac-

turing overhead $270,000.

(b) Variable costs = 68% of sales ($1,360,000 ÷ $2,000,000) or $.34 per

bottle ($.50 X 68%). Total fixed costs = $512,000.

(c) Contribution margin ratio = ($.50 – $.34) ÷ $.50

= 32%

(d) Required sales

PROBLEM 22-3C

(a) Sales were $1,500,000 and variable expenses were $900,000, which

means contribution margin was $600,000 and CM ratio was 40%. Fixed

expenses were $760,000. Therefore, the breakeven point in dollars is:

(b) 1. The effect of this alternative is to increase the selling price per unit

to $28 ($20 X 130%). Total sales become $1,950,000 (75,000 X $26).

Thus, the contribution margin ratio changes to 50% ($900,000 ÷

2. The effects of this alternative are to change total fixed costs to

$590,000 ($760,000 – $170,000) and to change the contribution margin

to .34 [($1,500,000 – $900,000 – $90,000) ÷ $1,500,000]. The new

breakeven point is:

3. The effects of this alternative are: (1) variable and fixed cost of

goods sold become $600,000 each, (2) total variable costs become

$720,000 ($600,000 + $65,000 + $55,000), and (3) total fixed costs

are $940,000 ($600,000 + $275,000 + $65,000). The new breakeven

point is:

X = ($720,000 ÷ $1,500,000)X + $940,000

PROBLEM 22-4C

(a) Current breakeven point: $30X = $13X + $221,000

(where X = pairs of shoes)

(b) Current margin of safety percentage =

(16,000 X $30) – (13,000 X $30)

(16,000 X $30)

(c) SASSY SHOE STORE

CVP Income Statement

Current

New

Sales (16,000 X $30)

Variable expenses (16,000 X $13)

$480,000

208,000

$644,000

299,000

(23,000 X $28)

(23,000 X $13)

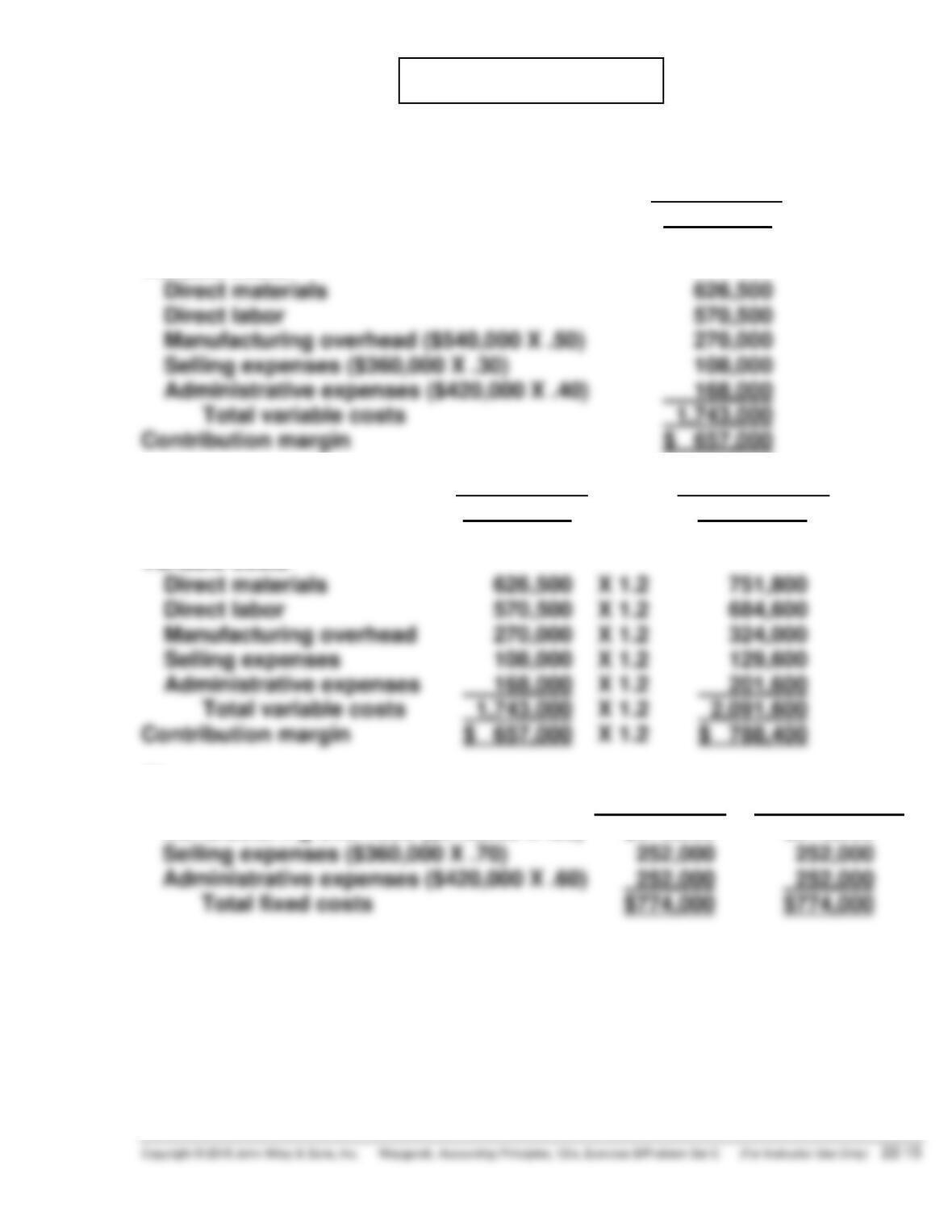

PROBLEM 22-5C

(a)

(1)

Current Year

Selling expenses ($360,000 X .30)

Contribution margin

Net sales

Variable costs

Direct materials

Direct labor

$2,400,000

626,500

570,500

Current Year

Projected Year

Contribution margin

Sales

Variable costs

Direct materials

$2,400,000

626,500

X 1.2

X 1.2

$2,880,000

751,800

(2)

Fixed Costs

Current Year

Projected year

Manufacturing overhead ($540,000 X .50)

Selling expenses ($360,000 X .70)

$270,000

252,000

$270,000

252,000

PROBLEM 22-5C (Continued)

(b) Unit selling price = $2,400,000 ÷ 200,000 = $12.00

Unit variable cost = $1,743,000 ÷ 200,000 = $8.72

Unit contribution margin = $12.00 – $8.72 = $3.28

(c) Sales dollars

required for

=

(Fixed costs

+

Target net income)

÷

Contribution margin ratio

target net income

=

+

Break-even point in units

=

Fixed costs

÷

Unit contribution margin

=

÷

Break-even point in dollars

Fixed costs

÷

Contribution margin ratio

=

÷

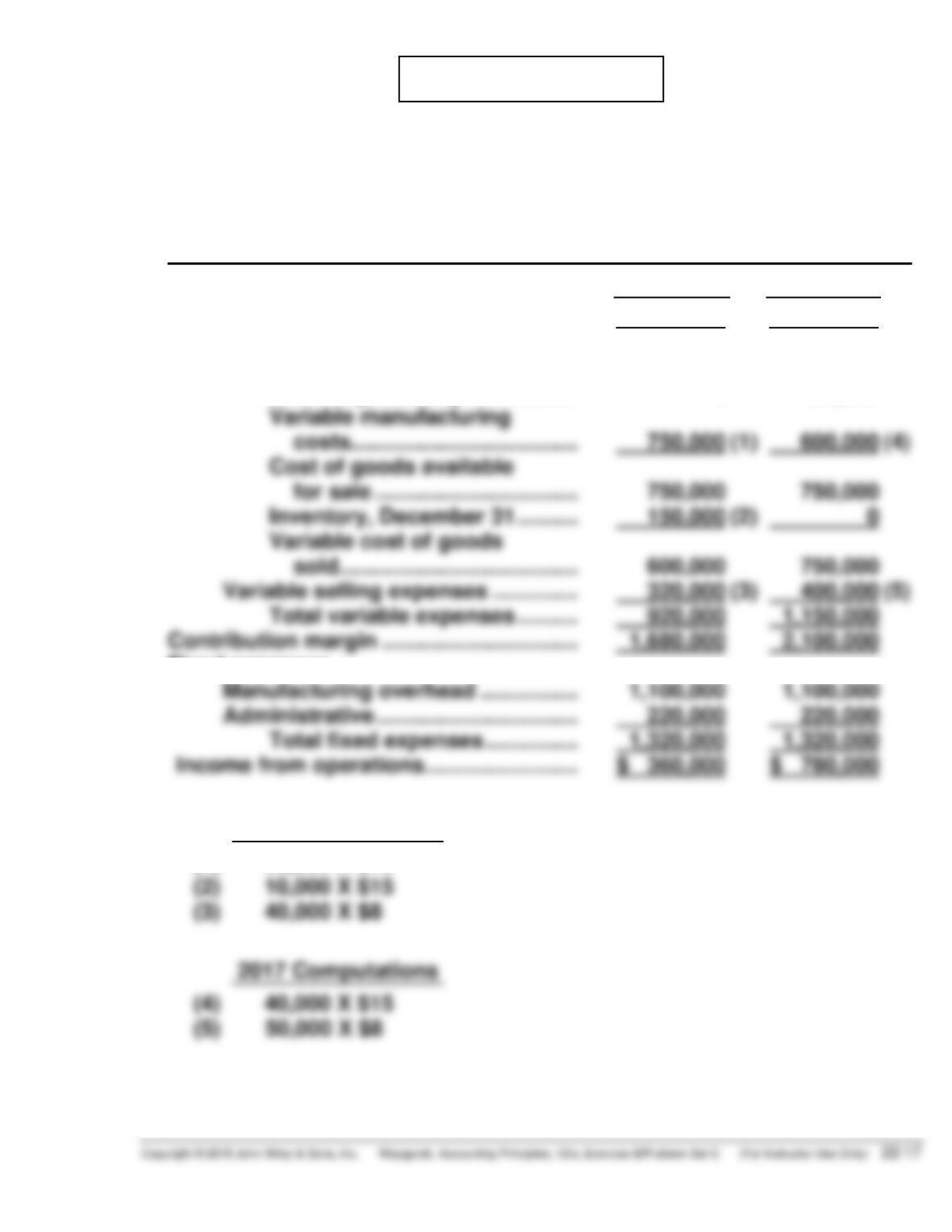

*PROBLEM 22-6C

(a) RAGGED METAL COMPANY

Income Statement

For the Year Ended December 31

(Variable Costing)

2016

2017

Income from operations …………………….

Sales …………………………………………………

Variable expenses

Variable cost of goods sold

Inventory, January 1 ……………

Variable manufacturing

sold…………………………………

Variable selling expenses …………..

Total variable expenses ……….

Contribution margin …………………………..

Fixed expenses

$2,600,000

0

600,000

320,000

920,000

1,680,000

(3)

$3,250,000

150,000

750,000

400,000

1,150,000

2,100,000

(5)

2016 Computations

(3)

(5)

*PROBLEM 22-6C (Continued)

(b) RAGGED METAL COMPANY

Income Statement

For the Year Ended December 31

(Absorption Costing)

2016

2017

Sales …………………………………………………………..

Cost of goods sold

Inventory, January 1 …………………………...

Cost of goods manufactured ……………….

Cost of goods available for sale …………..

Operating expenses

Selling expenses …………………………………

Administrative expenses ……………………..

$2,600,000

0

1,850,000

1,850,000

320,000

220,000

(1)

$3,250,000

370,000

1,700,000

2,070,000

400,000

220,000

(3)

2016 Computations

2017 Computations

(2)

(c) The variable costing and the absorption costing income from operations

can be reconciled as follows:

2016

2017

Variable costing income

Fixed manufacturing overhead

expensed with variable costing

$1,100,000

$360,000

$1,100,000

$780,000

Absorption costing income

*PROBLEM 22-6C (Continued)

(2)In 2017, with absorption costing $1,320,000 of fixed manufacturing overhead is expensed

(d) Income is more sensitive to changes in sales under variable costing as

seen in the increase in income from operations in 2017 when 10,000