Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

21–136 Intermediate Accounting, 8/e

Case 21–5 (continued)

(f)

Retained Earnings

_______________________________________________________________

141 Beginning balance

DISTINCTIVE INDUSTRIES

Comparative Balance Sheets

At December 31

2016 2015

Assets:

Cash $ 360 $ 177

Liabilities and shareholders’ equity:

Accounts payable $ 120 $ 90

Case 21–5 (concluded)

Requirement 2

DISTINCTIVE INDUSTRIES

Statement of Cash Flows

For the Year Ended December 31, 2016

($ in millions)

Cash flows from operating activities:

Net income $ 84

Adjustments for noncash effects:

Depreciation expense 30

* $279 – 252 = $27

** $180 – 156 = $24

Real World Case 21–6

Requirement 1

Year to year during the three years, Staples’ largest investing activity was the

Requirement 2

Transactions that involve merely transfers from cash to “cash equivalents” such as the

purchase of a CD should not be reported in the statement of cash flows. A dollar

Requirement 3

The sale of debt and the sale of stock are reported as financing activities.

Requirement 4

The payment of cash dividends to shareholders is classified as a financing activity, but

Case 21–6 (concluded)

Requirement 5

A statement of cash flows reports transactions that cause an increase or a decrease in

cash. However, some transactions that don’t increase or decrease cash, but which

activities. Examples of noncash transactions that would be reported:

• Acquiring an asset by incurring a debt payable to the seller.

21–140 Intermediate Accounting, 8/e

Ethics Case 21–7

Discussion should include these elements.

The apparent situation:

There seems to be at least superficial evidence that income is being artificially

Ethical Dilemma:

Does Ben have an obligation to challenge the questionable practices? If his

Who is affected?:

Ben

Real World Case 21–8

Requirement 1

Cash flows from operating activities are both inflows and outflows of cash that

result from the same activities that are reported in the income statement. The income

Requirement 2

Depreciation and amortization are noncash expenses. They are merely an

Requirement 3

A sizable reduction in the amount PetSmart owes its suppliers is a contributor to

PetSmart’s cash flows from operating activities being different from net income in

21–142 Intermediate Accounting, 8/e

Case 21–8 (continued)

Requirement 4

Cash outflows from financing activities exceeded cash inflows from those activities

during each year reported. Even though financing activities are not providing positive

cash inflows, investing activities can also produce net cash outflows because operating

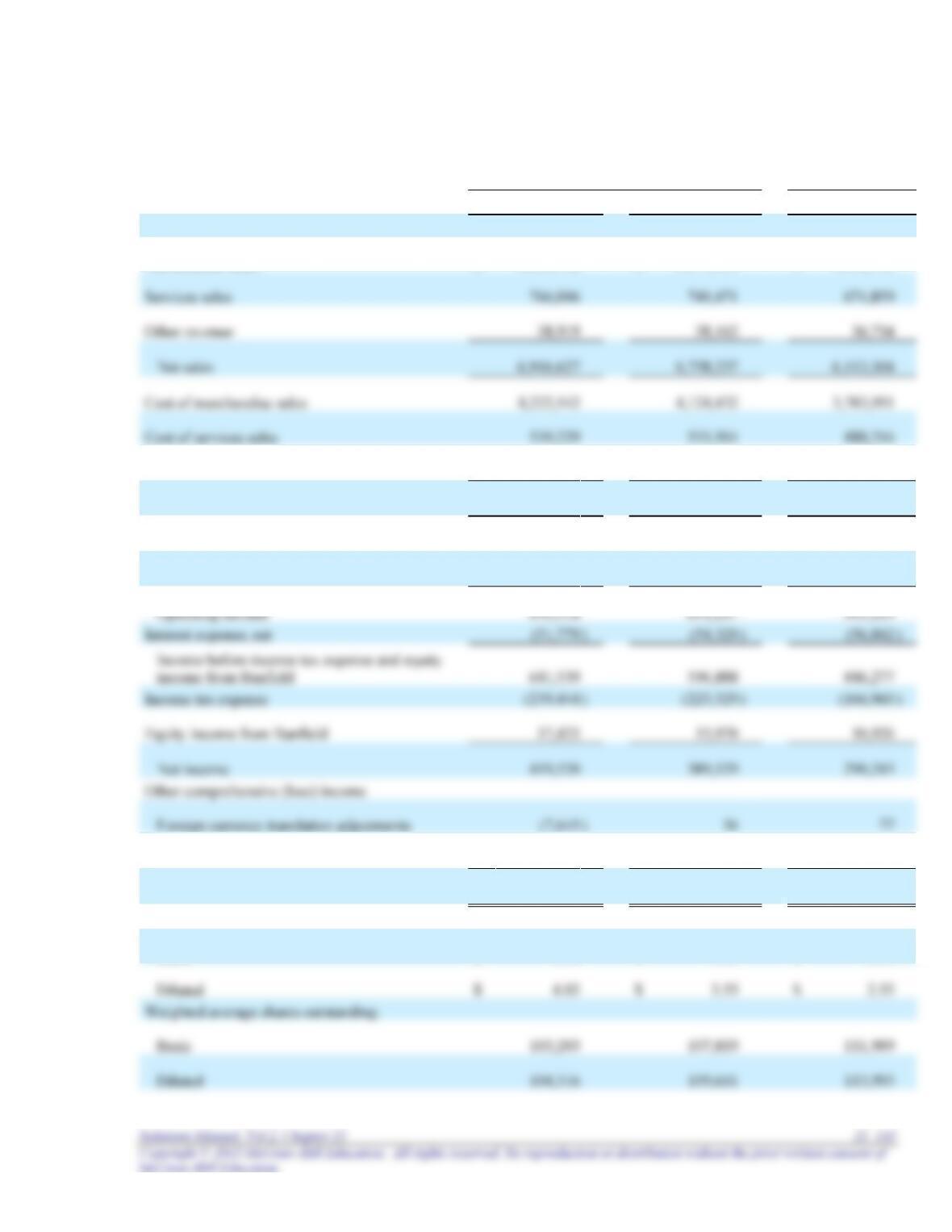

PETSMART INC.

CONSOLIDATED STATEMENTS OF INCOME

(in thousands, except per share amounts)

Fiscal Year Ended

February 2, 2014

February 3, 2013

January 29, 2012

(52 weeks)

(53 weeks)

(52 weeks)

Merchandise sales

$

6,111,702

$

5,979,604

$

5,401,731

Cost of other revenue

38,919

38,162

36,714

Total cost of sales

4,800,690

4,696,098

4,308,881

Gross profit

2,115,937

2,062,139

1,804,423

Operating, general, and administrative expenses

1,422,619

1,410,922

1,301,304

Other

(20

)

(20

)

33

Comprehensive income

$

411,855

$

389,545

$

290,353

Earnings per common share:

Basic

$

4.06

$

3.61

$

2.59

Case 21–8 (continued)

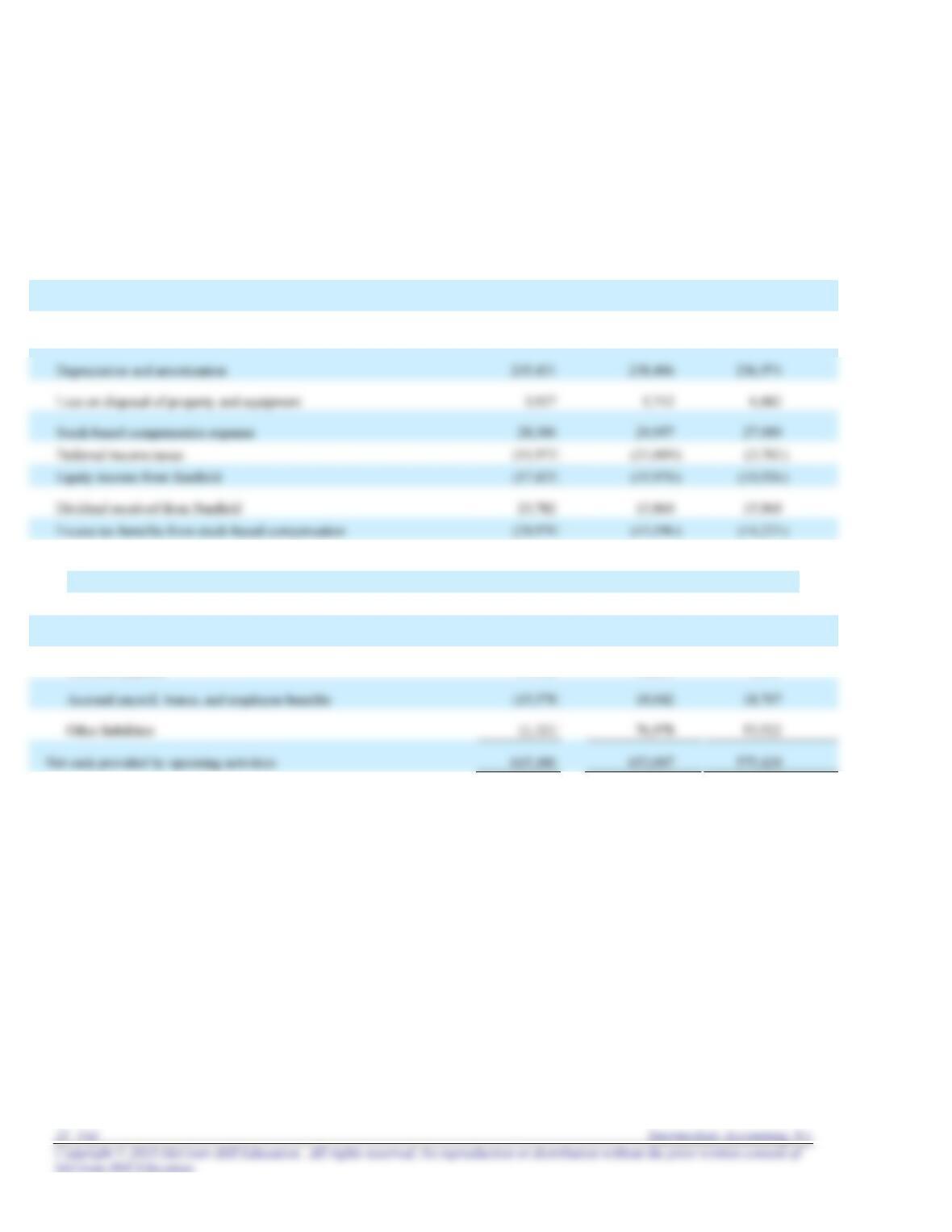

CONSOLIDATED STATEMENTS OF CASH FLOWS

Fiscal Year Ended

February 2, February 3, January 29,

2014 2013 2012

CASH FLOWS FROM OPERATING ACTIVITIES:

Net income

$

$419,520

$

389,529

$

290,243

Adjustments to reconcile net income to net cash provided by operating

activities:

Non-cash interest expense

608

962

782

Changes in assets and liabilities:

Merchandise inventories

(64,473

)

(34,015

)

(29,220

)

Other assets

2,234

(46,932

)

(26,703

)

Accounts payable

37,118

40,653

9,135

Case 21–8 (concluded)

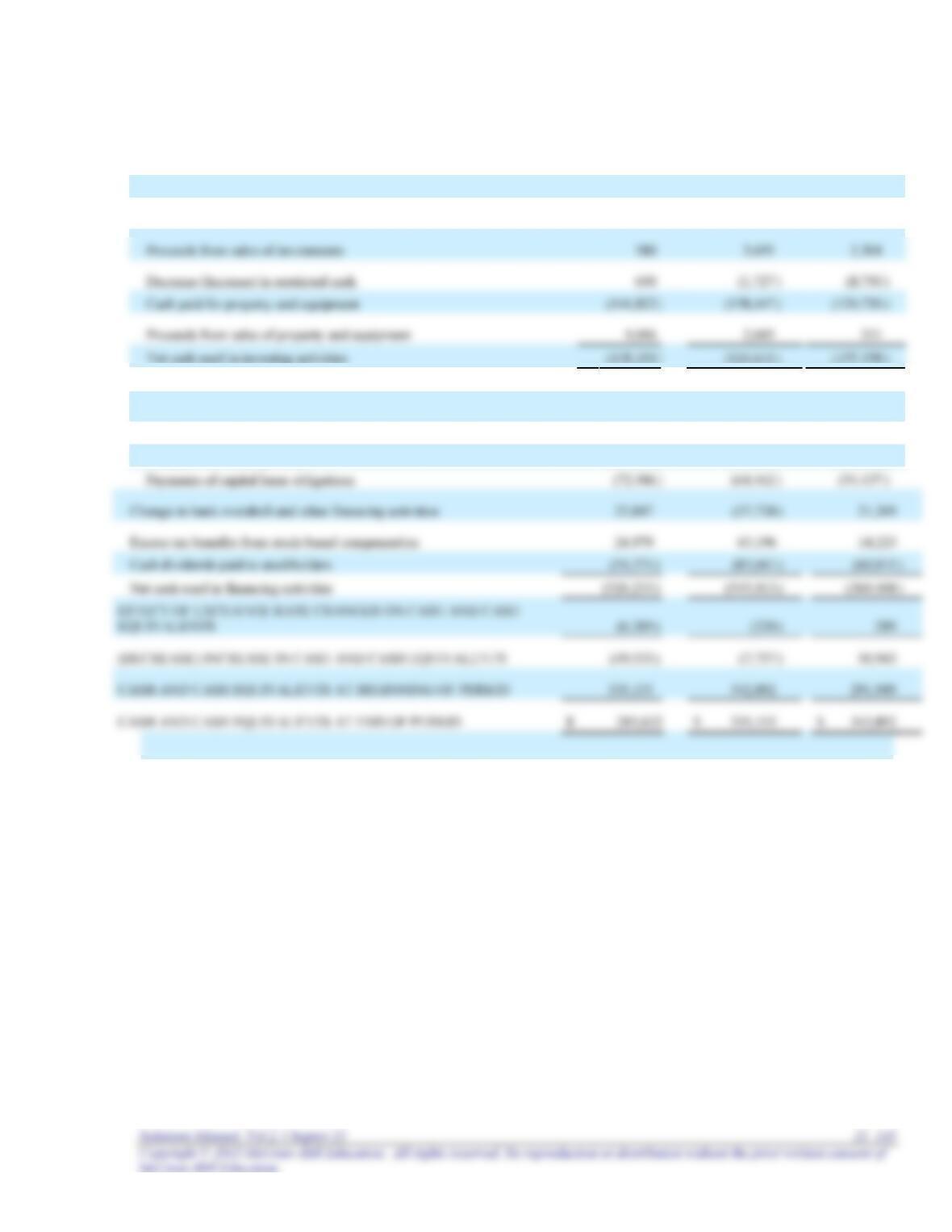

CASH FLOWS FROM INVESTING ACTIVITIES:

Purchases of investments

(14,446

)

(4,027

)

(38,738

)

Proceeds from maturities of investments

12,801

23,230

10,215

CASH FLOWS FROM FINANCING ACTIVITIES:

Net proceeds from common stock issued under stock incentive plans

49,506

55,197

53,439

Minimum statutory withholding requirements

(5,792

)

(23,172

)

(7,061

)

Cash paid for treasury stock

(485,404

)

(435,283

)

(336,830

)

21–146 Intermediate Accounting, 8/e

Research Case 21–9

The results students report will vary depending on the companies chosen. It can

be interesting to have students compare in class their findings with those of their

classmates.

Most companies use the indirect method to report operating activities.

Adjustments to net income in reconciling net income and cash flows from operations

are reported on the face of the statement of cash flows when the indirect method is

Analysis Case 21–10

Structural free cash flow (what Warren Buffett calls "owner's earnings") is net income

from operations plus depreciation and amortization minus capital expenditures:

2014 2013 2012

Net income $420 $390 $290

Increase from previous year 8% 34%

Net income $420 $390 $290

Increase from previous year 4% 21%

In 2013, net income shows a sizeable increase of 34% from 2012. Structural free cash

21–148 Intermediate Accounting, 8/e

Research Case 21–11

Requirement 1

The specific citation that specifies the classification of notes payable to suppliers is

Requirement 2

Specifically, paragraph 45–17a states that cash outflows for operating activities

Requirement 3

Analysis Case 21–12

Requirement 1

BT’s statement of cash flows, prepared in accordance with IFRS, classifies cash flows

Requirement 2

BT reports interest received and dividends received as investing activities and

dividends paid and interest paid as financing activities. IAS No. 7 allows flexibility,

21–150 Intermediate Accounting, 8/e

Air France–KLM Case

Requirement 1

AF’s statement of cash flows, prepared in accordance with IFRS, classifies cash

Requirement 2

AF reports dividends received as investing activities. It reports dividends paid as

a financing activity. Interest received and interest paid are reported as operating