CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-3B

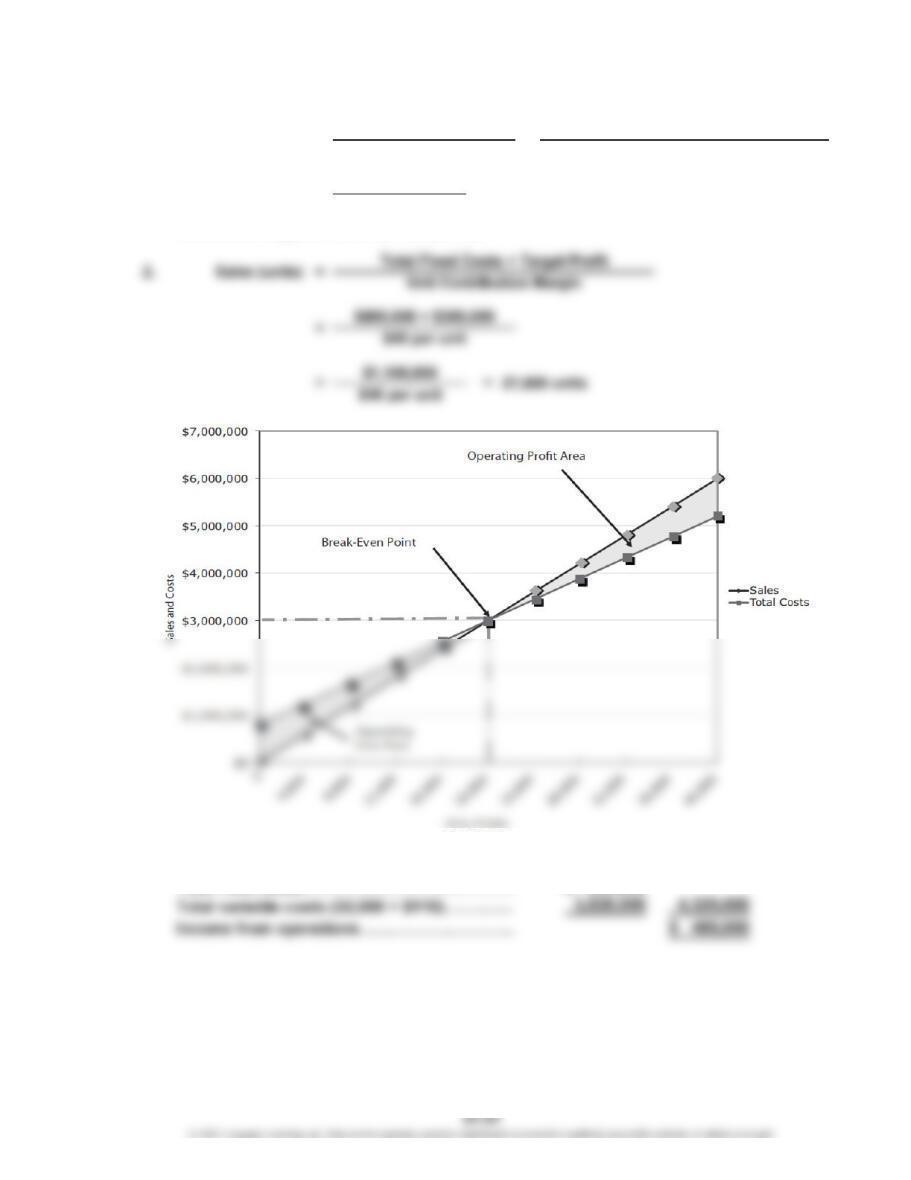

1. Break-Even

Sales (units)

$800,000

$40*

* $150 unit selling price – $110 unit variable cost

3.

4. Sales (32,000 × $150)…………………………… $4,800,000

20,000 units

==

Total Fixed Costs

Unit Selling Price – Unit Variable Cost

=Total Fixed Costs

Unit Contribution Margin =

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4B

1.

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4B (Continued)

1. Break-Even Units:

$225,000

37.5%

Total Fixed Costs

Unit Contribution Margin Unit Selling Price – Unit Variable Cost

$225,000 = 3,000 units

Break-Even Sales (units) = Total Fixed Costs =

=

=

Break-Even (dollars)

= $600,000

=Total Fixed Costs

Contribution Margin Ratio

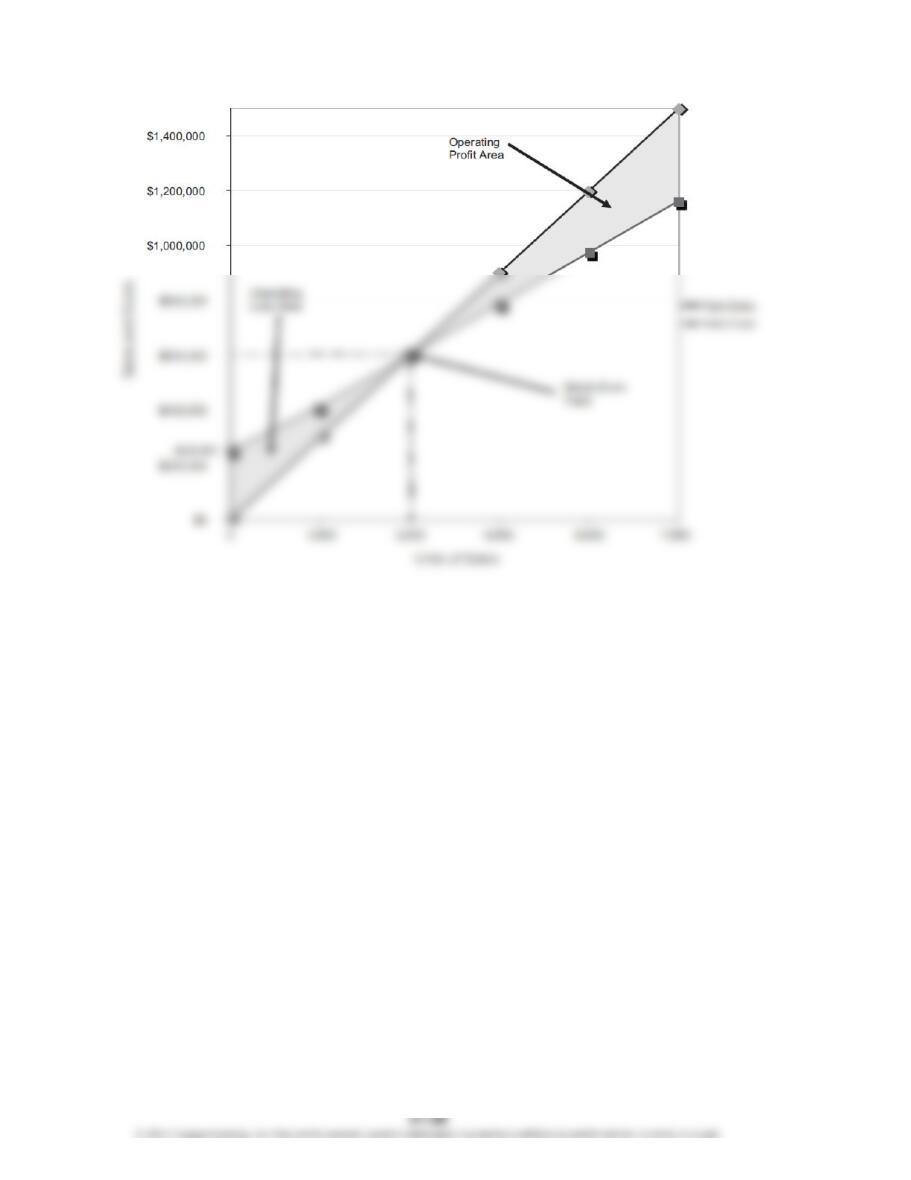

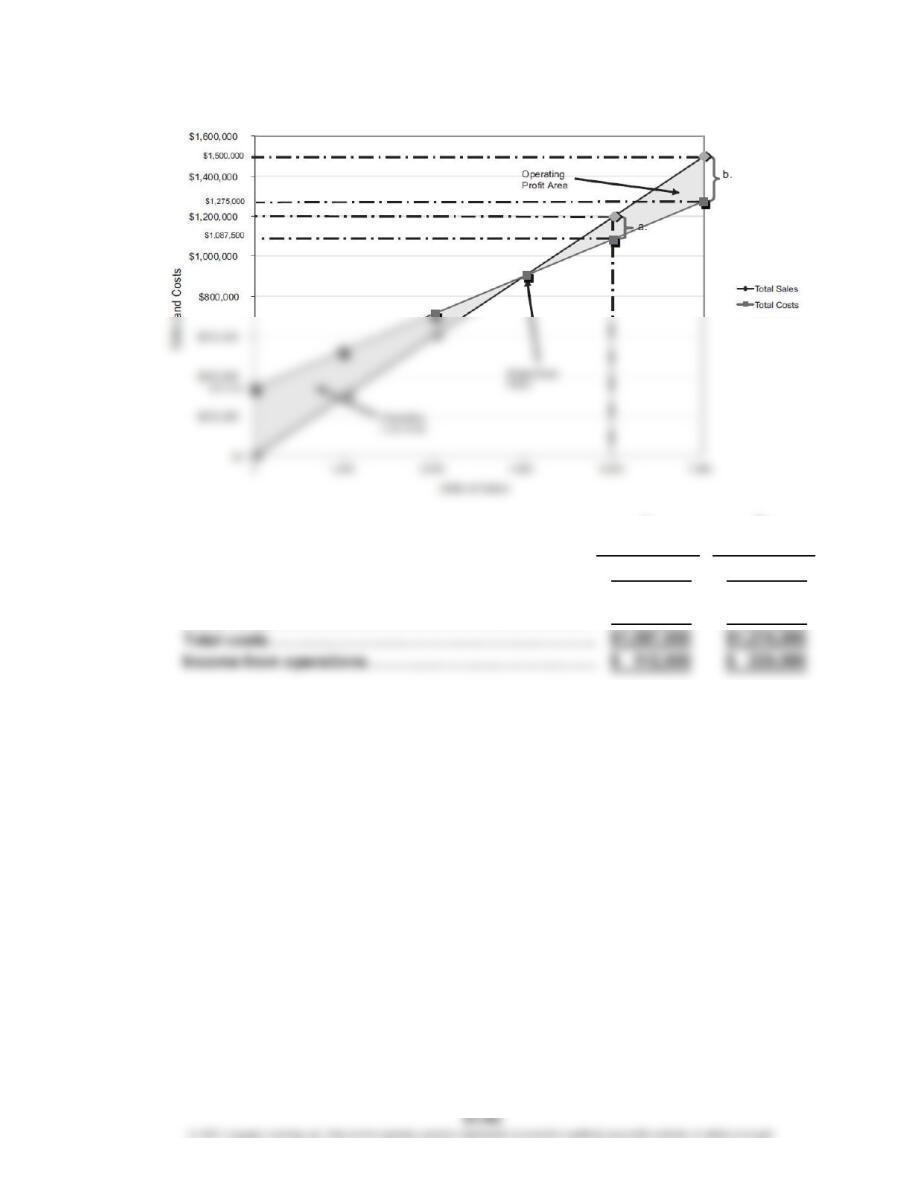

2.

a. b.

4,500 units 7,500 units

Sales…………………………………………………………

…

$900,000 $1,500,000

V

ariable costs………………………………………………

…

$562,500 $ 937,500

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4B (Continued)

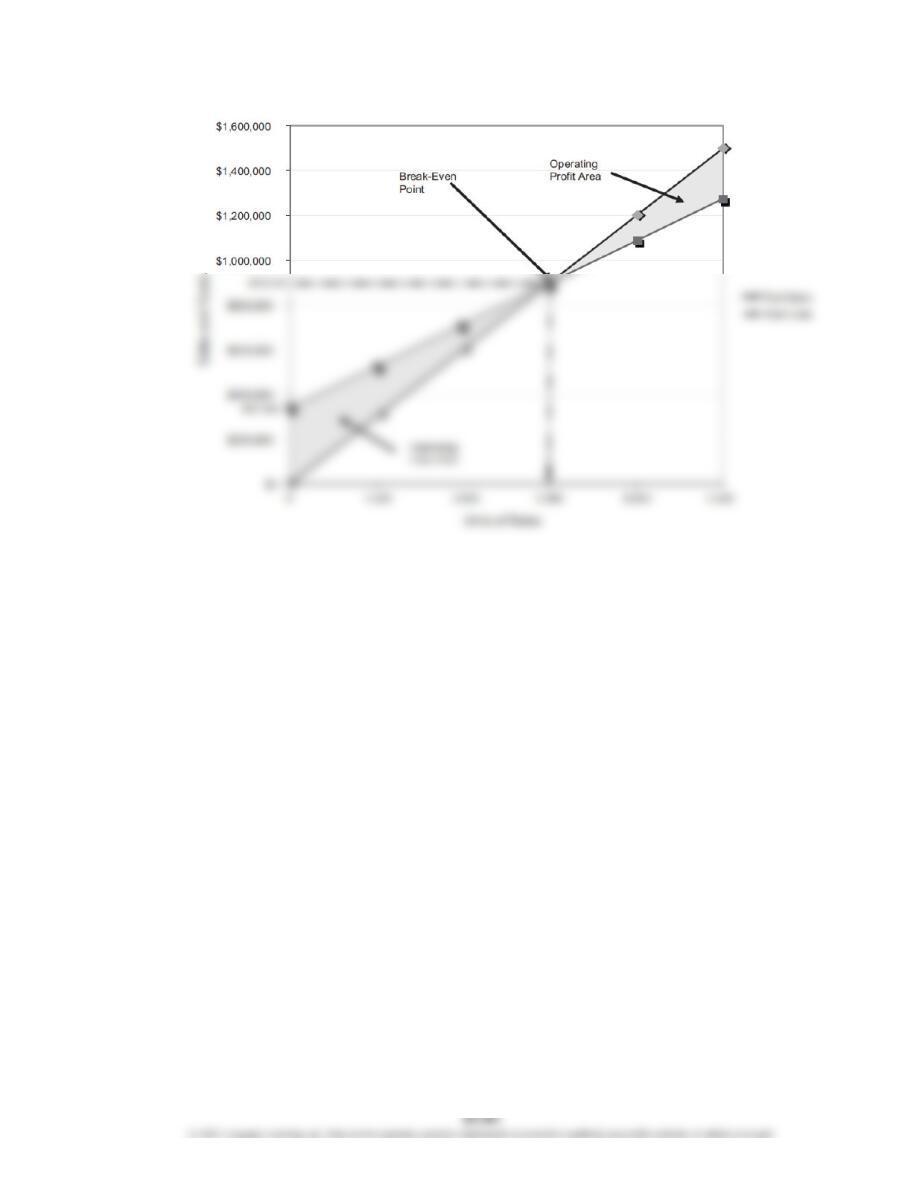

3.

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4B (Continued)

3. Break-Even Units:

Break-Even Dollars:

Break-Even Sales (units) = Total Fixed Costs =Total Fixed Costs

Unit Contribution Margin Unit Selling Price – Unit Variable Cost

37.5%

Contribution Margin Ratio = Unit Contribution Margin =Unit Selling Price – Unit Variable Cost

Unit Selling Price Unit Selling Price

=$200 Unit Selling Price – $125 Unit Variable Cost =

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4B (Concluded)

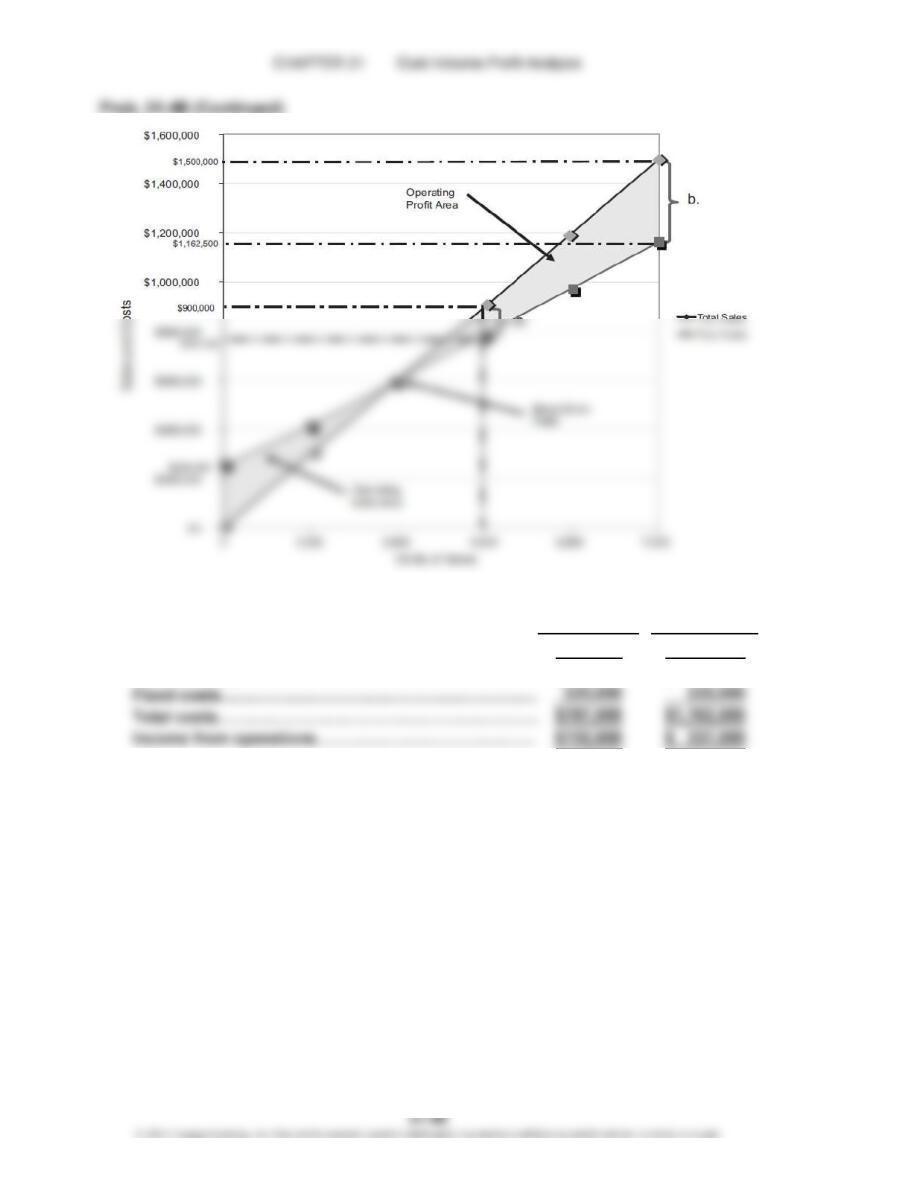

4.

a. b.

6,000 units 7,500 units

Sales…………………………………………………………… $1,200,000 $1,500,000

V

ariable costs………………………………………………

…

$ 750,000 $ 937,500

Fixed costs……………………………………………………

…

337,500 337,500

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-5B

(Overall product is labeled E.)

1. Unit selling price of E [($13 × 20%) + ($16 × 80%)]……………………………

…

$15.40

2. 5,200 units of E × 20% = 1,040 units of 12″ pizza

5,200 units of E × 80% = 4,160 units of 16″ pizza

3. Unit selling price of E [($13 × 50%) + ($16 × 50%)]……………………………

…

$14.50

Unit variable cost of E [($4 × 50%) + ($5 × 50%)]………………………………

…

4.50

Unit contribution margin of E……………………………………………………… $10.00

…

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-6B

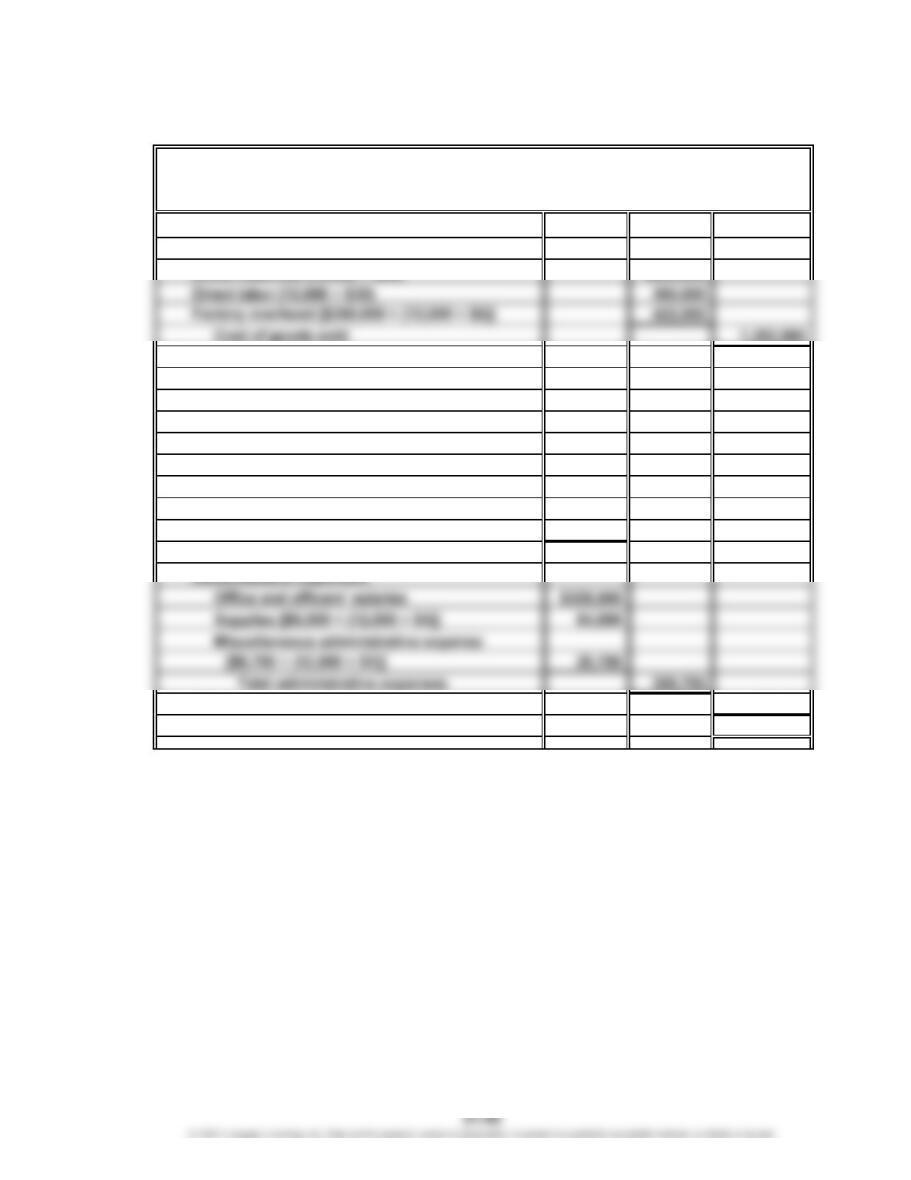

1.

Sales (12,000 × $240) $2,880,000

Cost of goods sold:

Gross profit $1,498,000

Expenses:

Selling expenses:

Sales salaries and commissions

[$340,000 + (12,000 × $4)] $388,000

Advertising 116,000

Travel 4,000

Miscellaneous selling expense

[$2,300 + (12,000 × $1)] 14,300

Total selling expenses $522,300

Total expenses 922,000

Income from operations $ 576,000

Belmain Co.

Estimated Income Statement

For the Year Ended December 31, 20Y7

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-6B (Continued)

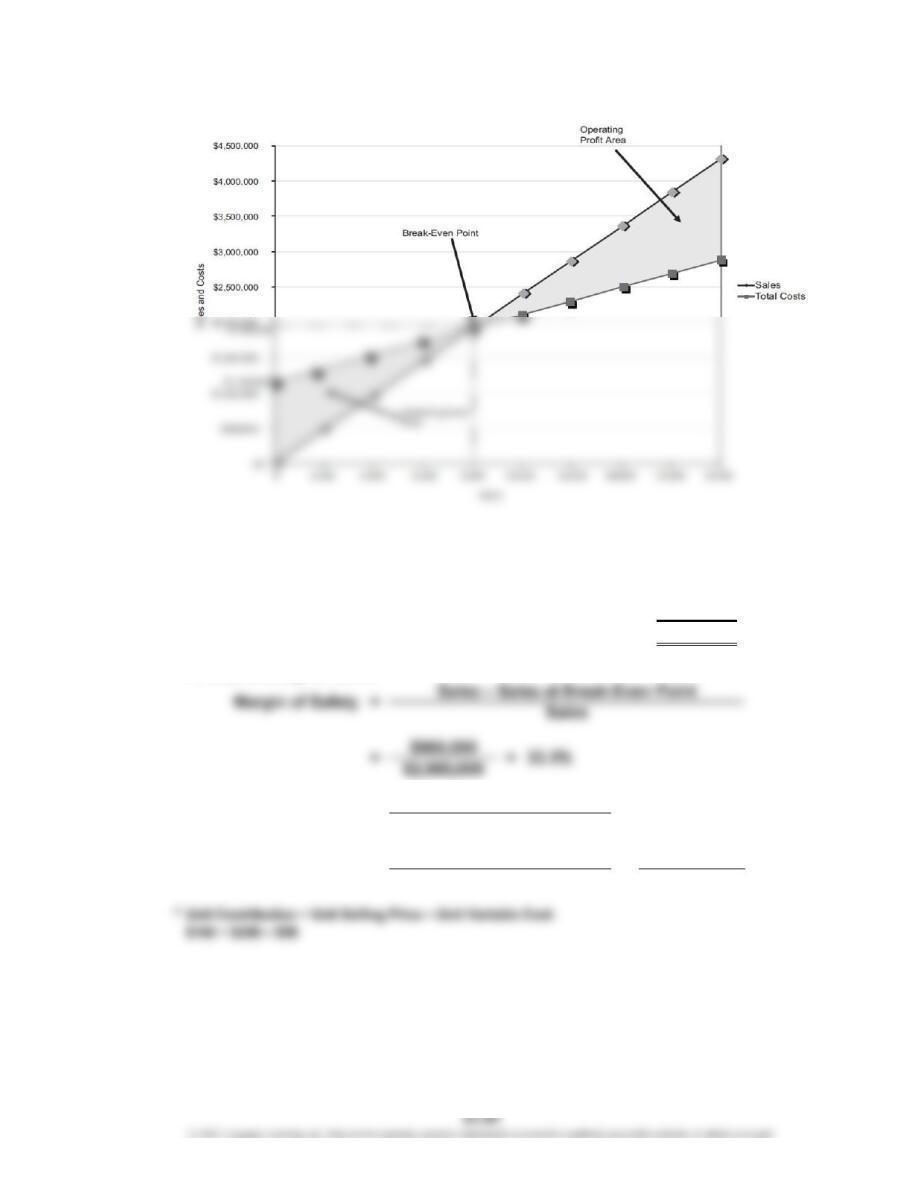

$1,152,000

$240 – $96

or

Break-Even Sales (dollars) = 8,000 units × $240 per unit = $1,920,000

==

8,000 units

2. Contribution Margin Ratio = Sales – Variable Costs

Sales

3. Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-6B (Concluded)

4.

5. Margin of safety:

In dollars:

Expected sales (12,000 units × $240)………………………

…

$2,880,000

Break-even point (8,000 units × $240)……………………… 1,920,000

Margin of safety………………………………………………… $ 960,000

As a percentage of sales:

$1,728,000

$576,000

Contribution Margin

Income from Operations

==3

$576,000

6.

=12,000 units × $144*

Operating Leverage =

CHAPTER 21 Cost-Volume-Profit Analysis

CP 21-1

In an absolute sense, Edward’s actions are devious. He is clearly attempting to

use the first four-year scenario, which is favorable, as a way to market the

partnerships. They are really longer-term investments. After the first four years,

the risk increases dramatically. The break-even occupancy becomes more

difficult to achieve at 95% than it does at 65%. Focusing on the 65% and remaining

silent about the increase to 95% is deceptive. One might argue “let the buyer

beware.” After all, the information is in the fine print. A little spadework would

CP 21-2

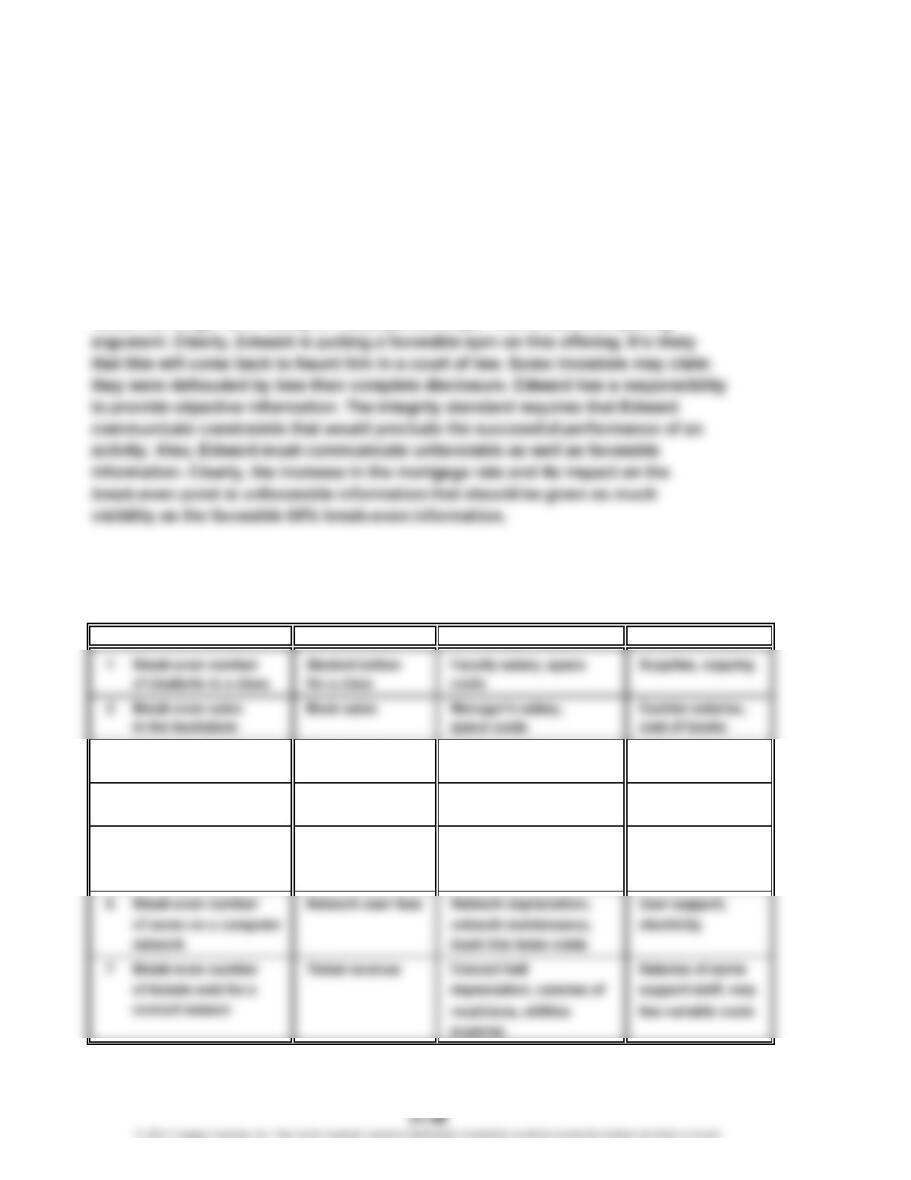

There are many possible applications of break-even analysis in a school

environment. Below are just a few possible ideas.

Revenues Fixed Costs Variable Costs

3 Break-even daily Meal revenue Salaries, space Food costs

meal revenues

4 Break-even students Room revenue Space, staff salaries, Janitorial costs

in a dorm utilities

5 Break-even number Ticket and Space, staff Clean-up costs,

of tickets sold for a concession salaries, utilities concession costs

basketball game revenue

Break-Even Analysis

CASES & PROJECTS

CHAPTER 21 Cost-Volume-Profit Analysis

CP 21-3

To: Neil Armstrong, CEO Sun Airlines

From: Ima Student

Re: Increasing Ticket Prices

In recent months, Sun Airlines has struggled to stay above break-even sales

volume, which has led to a string of monthly losses. Sun’s break-even volume is

75% of capacity, which is significantly higher than the industry average of 65% of

capacity.

and losses will increase.

For this strategy to succeed, the airline will have to minimize the impact of the

ticket price increase on sales volume. The airline might consider targeting

business travelers who need to fly regardless of ticket price. If successful, this

strategy can reduce the break-even point without significantly decreasing ticket

sales. Restrictions such as allowing reduced fares only on round-trip tickets that

include a Saturday night stay-over achieve this objective, because business

CHAPTER 21 Cost-Volume-Profit Analysis

CP 21-4

Do-Nothing Strategy:

Revenue – Variable Costs – Fixed Costs = Profit

($80 × 1,000,000) – ($35 × 1,000,000) – $35,000,000 = Profit

$80,000,000 – $35,000,000 – $35,000,000 =

James’s Strategy:

Revenue – Variable Costs – Fixed Costs = Profit

($80 × 1,400,000) – ($35 × 1,400,000) – $45,000,000 = Profit

$112,000,000 – $49,000,000 – $45,000,000 =

CP 21-5

The direct labor costs are not variable to the increase in unit volume. The unit

volume is the wrong activity base for direct labor costs. The “number of

impressions” is a more accurate reflection of the direct labor cost. An impression

is a separate printing color application on the banners. Thus, the analysis should

be done as follows:

One Three

$10,000,000

$18,000,000

Four

Two

CHAPTER 21 Cost-Volume-Profit Analysis

CP 21-6

The Shipping Department manager should respond by pointing out that the

activities performed by his department are not related to sales volume but to

sales orders. The orders require inventory pulling and sorting activities as well