Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

PROBLEM 21-4A (Continued)

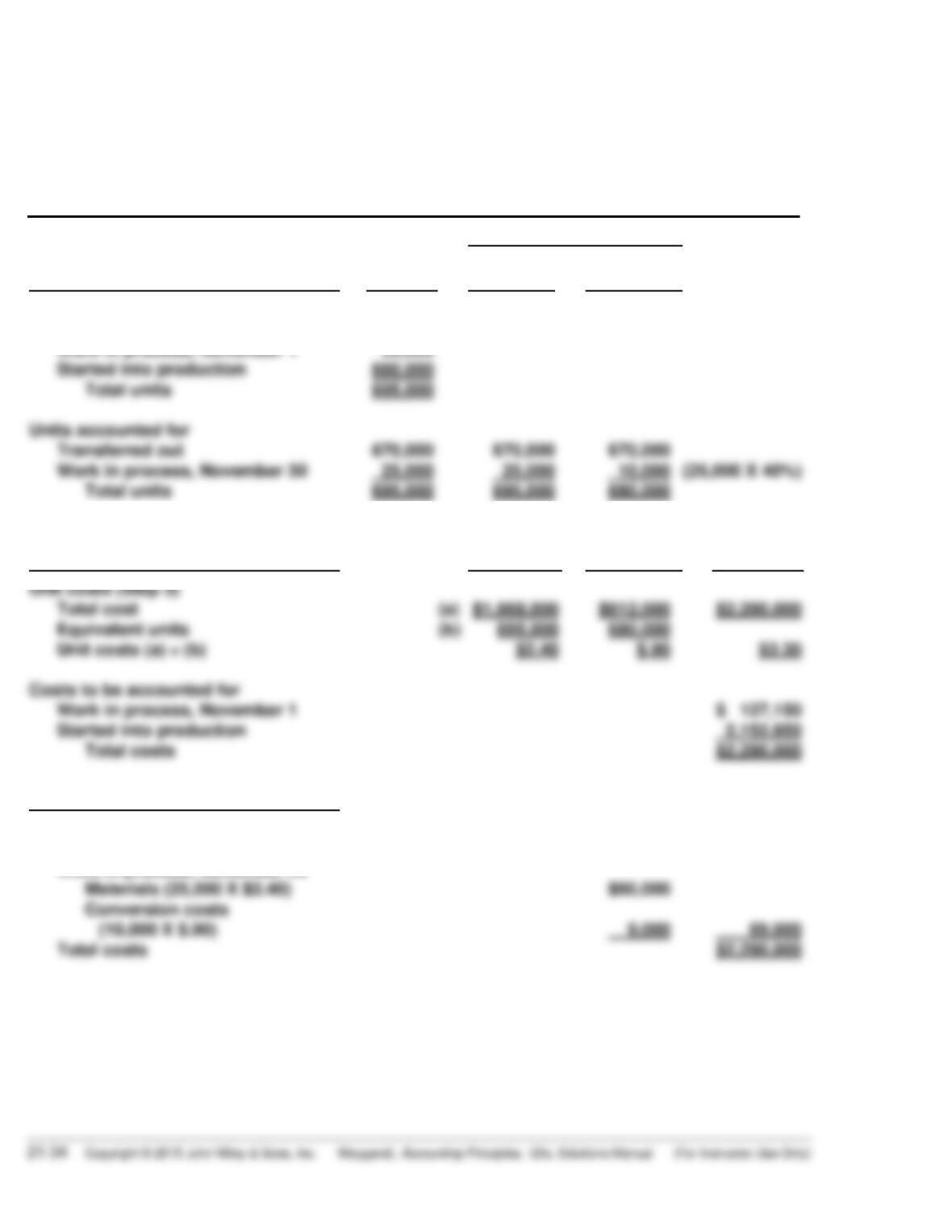

(c) RIVERA COMPANY

Assembly Department

Production Cost Report

For the Month Ended November 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, November 1

Started into production

35,000

660,000

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Total cost

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$1,668,000

695,000

$2.40

$612,000

680,000

$.90

$2,280,000

$3.30

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out (670,000 X $3.30)

Work in process, November 30

$2,211,000

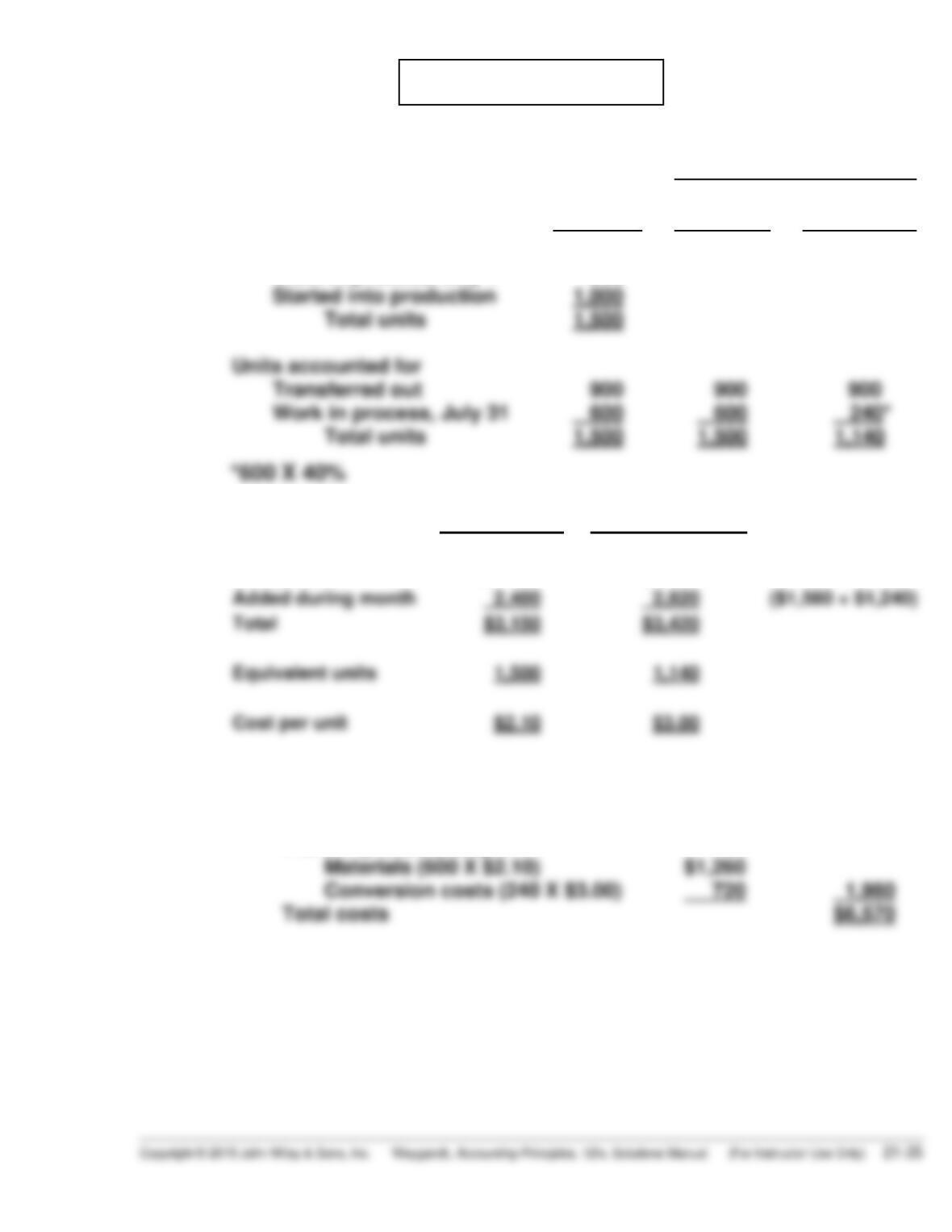

PROBLEM 21-5A

(a)

(1)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units to be accounted for

Work in process, July 1

Started into production

Total units

500

1,000

1,500

(2)

Beginning work

in process

Added during month

Materials cost

$ 750

2,400

Conversion costs

$ 600

2,820

($1,580 + $1,240)

(3)

Costs accounted for

Transferred out (900 X $5.10)

Work in process, July 31

$4,590

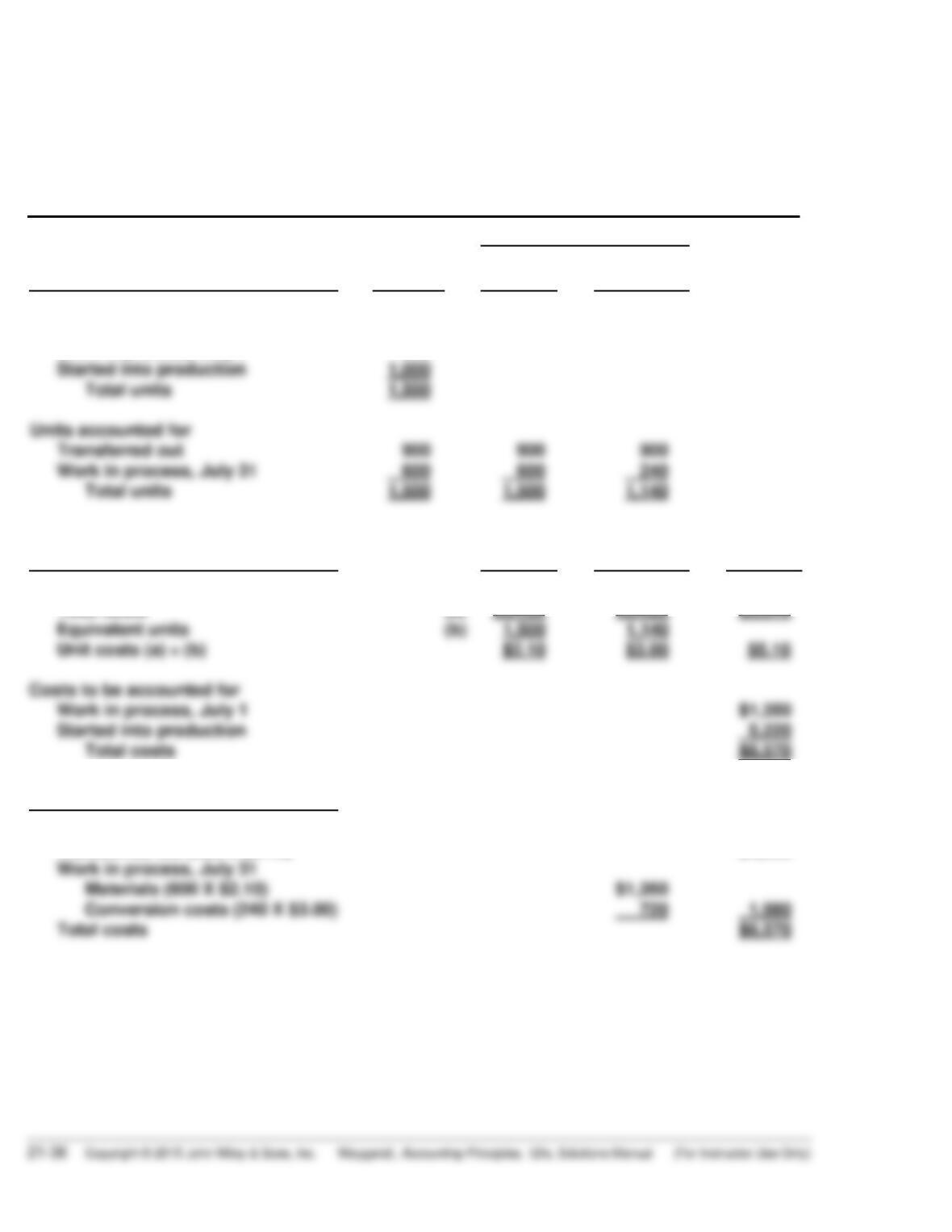

PROBLEM 21-5A (Continued)

(b) POLK COMPANY

Basketball Department

Production Cost Report

For the Month Ended July 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, July 1

500

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Total costs

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$3,150

1,500

$2.10

$3,420

1,140

$3.00

$6,570

$5.10

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out (900 X $5.10)

$4,590

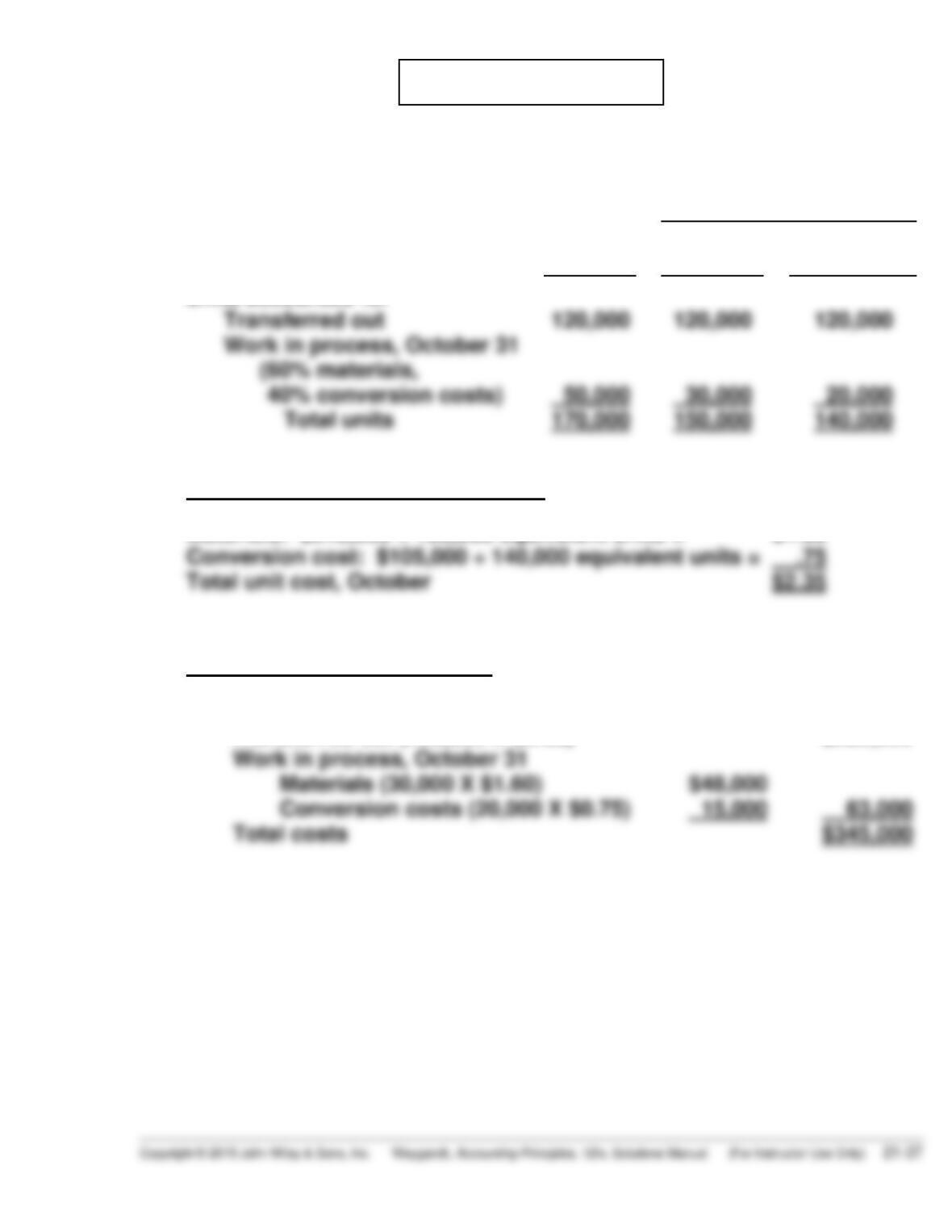

PROBLEM 21-6A

(a) Computation of equivalent units:

Equivalent Units

Physical

Units

Materials

Conversion

Costs

Units accounted for

Computation of October unit costs

Materials: $240,000 ÷ 150,000 equivalent units = $1.60

(b) Cost Reconciliation Schedule

Costs accounted for

Transferred out (120,000 X $2.35) $282,000

Work in process, October 31

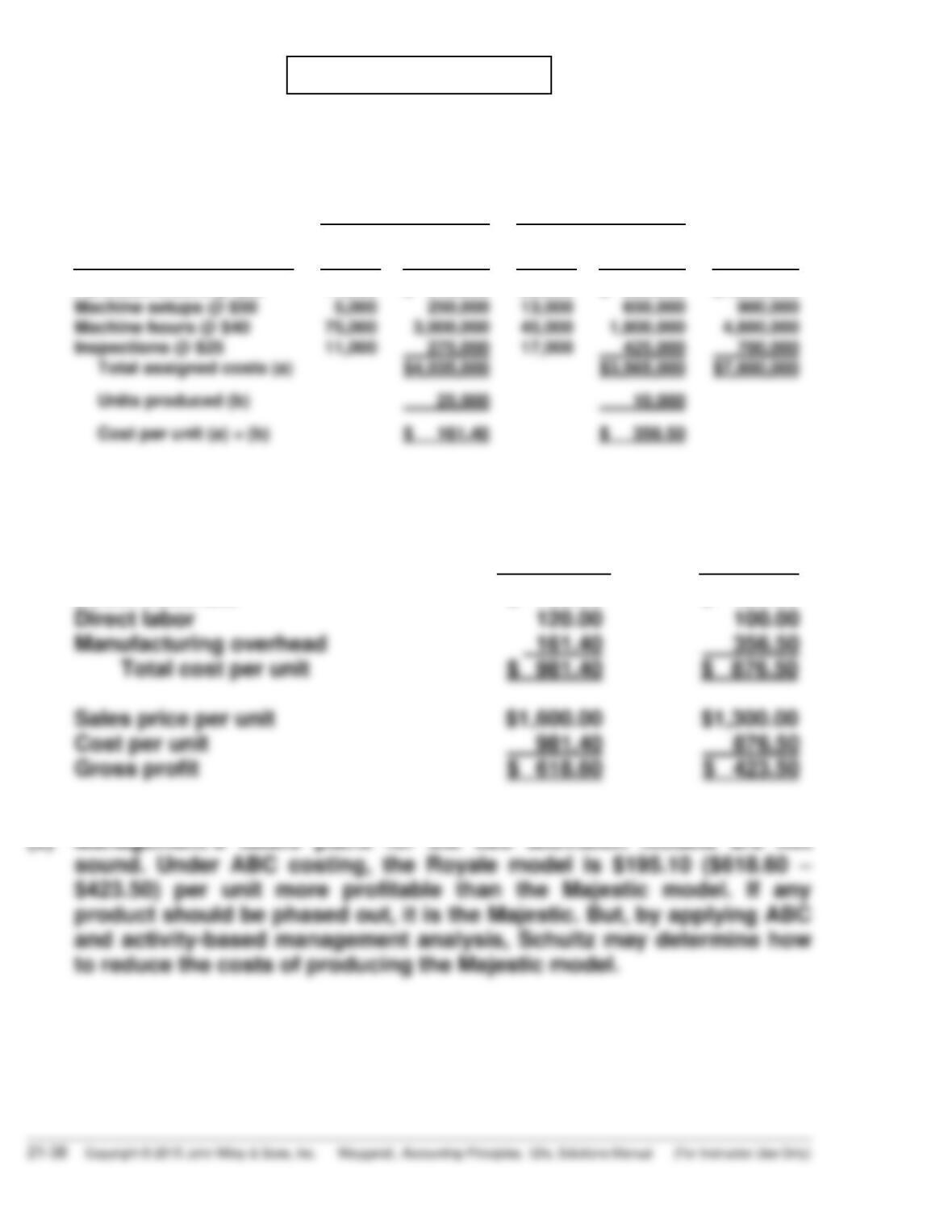

*PROBLEM 21-7A

(a) The allocation of total manufacturing overhead using activity-based

costing is as follows:

Royale

Majestic

Overhead Rate

Drivers

Used

Cost

Assigned

Drivers

Used

Cost

Assigned

Total

Overhead

Purchase orders @ $30

Machine setups @ $50

17,000

5,000

$ 510,000

250,000

23,000

13,000

$ 690,000

650,000

$1,200,000

900,000

(b) The cost per unit and gross profit of each model under ABC costing

were:

Royale

Majestic

Direct materials

Direct labor

$ 700.00

120.00

$ 420.00

100.00

(c) Management’s future plans for the two television models are not

sound. Under ABC costing, the Royale model is $195.10 ($618.60 –

$423.50) per unit more profitable than the Majestic model. If any

CD21 CURRENT DESIGNS

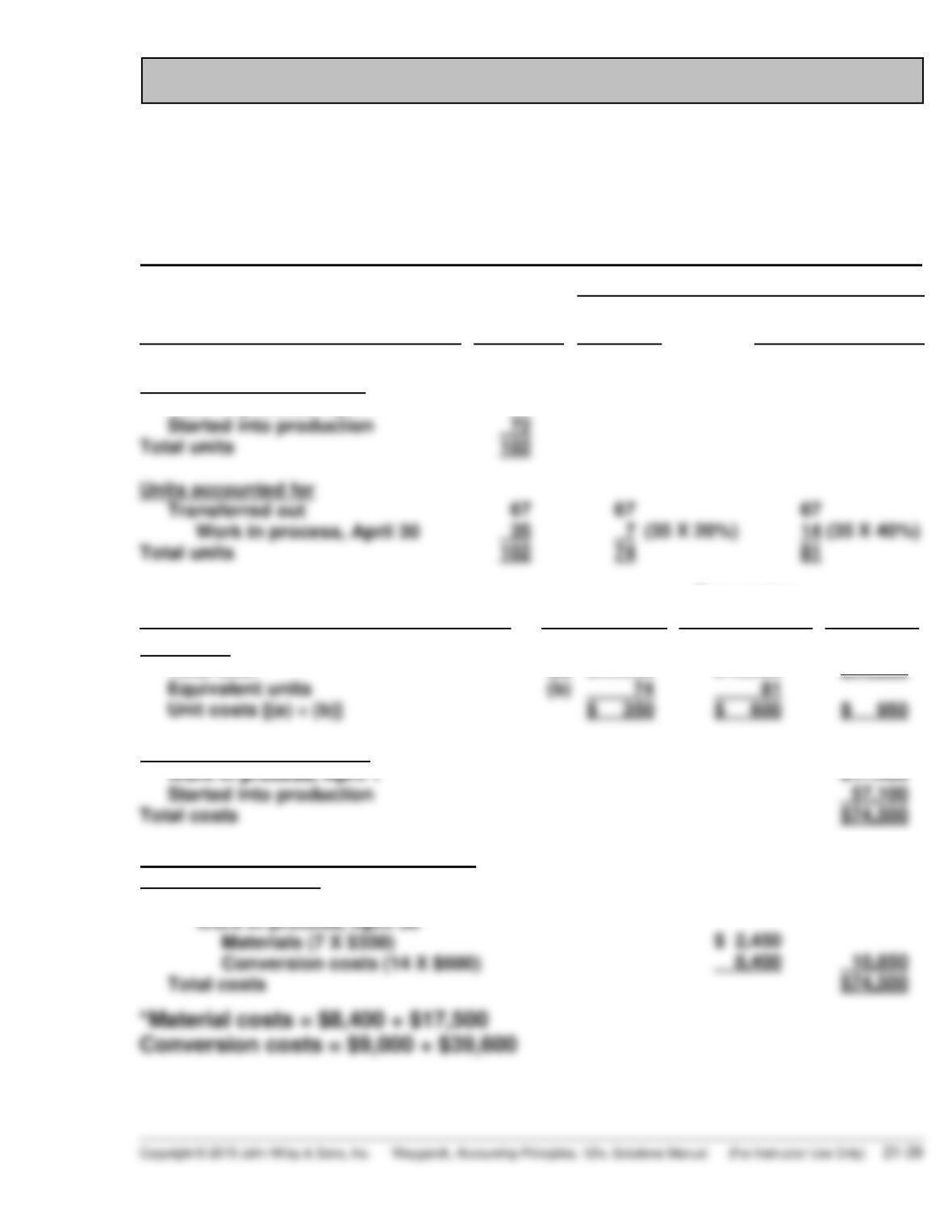

CURRENT DESIGNS

Fabrication Department

Production Cost Report

For the Month Ended April 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, April 1

Started into production

Total units

Units accounted for

30

72

102

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Total cost*

Costs to be accounted for

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out (67 X $950)

(a) $25,900

$48,600

$74,500

$63,650

BYP 21-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) The unit cost suggests that Joe took the highest total costs and divided

these costs by the units started into production. The highest total costs

(b) The principal errors made by Joe were: (1) he did not compute equivalent

BYP 21-1 (Continued)

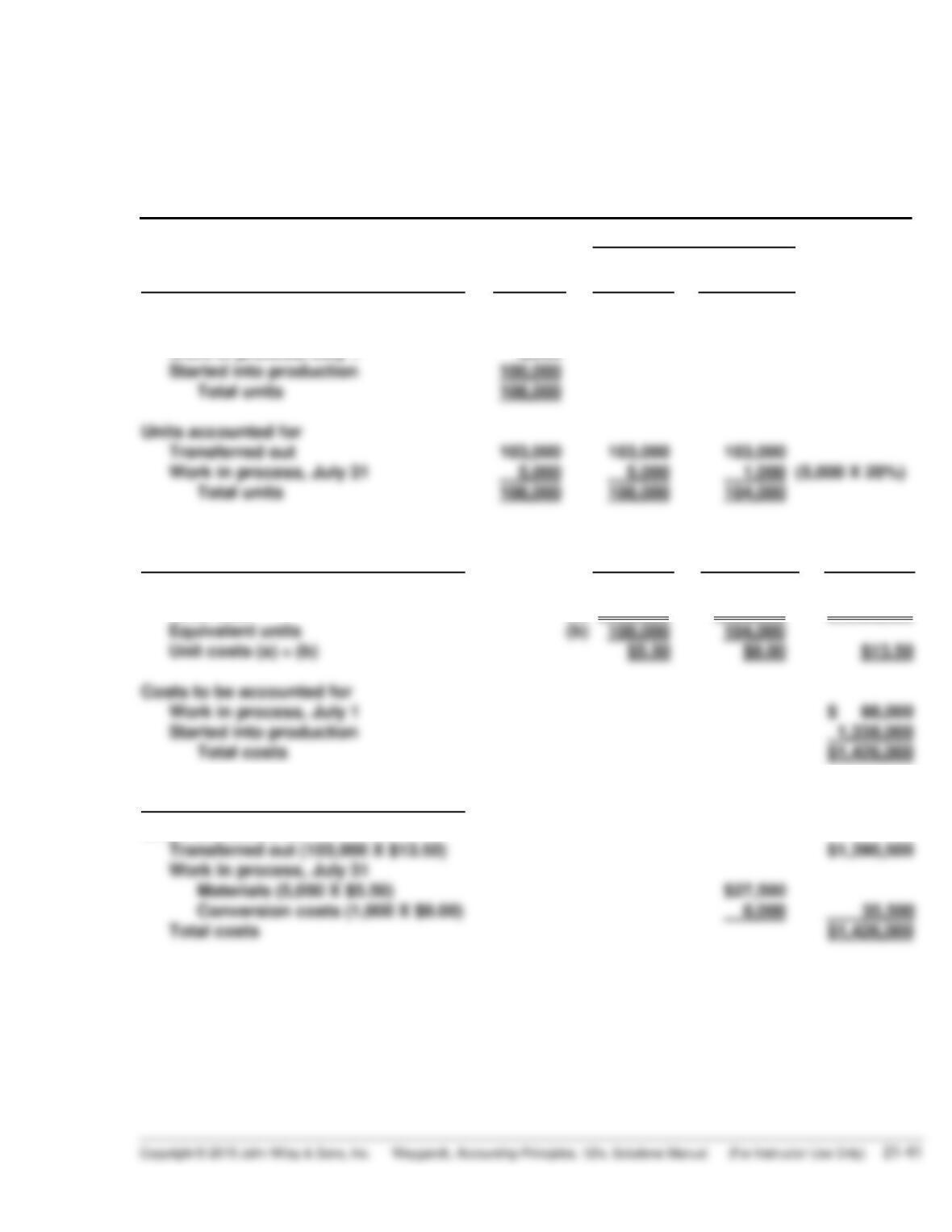

(c) FLORIDA BEACH COMPANY

Mixing Department

Production Cost Report

For the Month Ended July 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Units to be accounted for

Work in process, July 1

8,000

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Total cost

Equivalent units

Unit costs (a) ÷ (b)

(a)

(b)

$594,000

108,000

$5.50

$832,000

104,000

$8.00

$1,426,000

$13.50

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out (103,000 X $13.50)

$1,390,500

BYP 21-2 MANAGERIAL ANALYSIS

(a) The unit cost of materials is $150 ($450,000 ÷ 3,000).

(b) The materials cost of the goods transferred out is $375,000 (2,500 X

BYP 21-3 REAL-WORLD FOCUS

(a) The outer shell of the paintballs is made from a mixture that includes

water, sweeteners, food ingredients, and most importantly, gelatin. All

of the ingredients used to make paintballs are food grade, biodegradable

products. The “paint” filling inside a paintball is comprised of the same

inert ingredient used in cough syrup, as well as crayon wax.

After mixing the gelatin and other materials, the mixture is heated, and

then spread on rolling drums which create thin gelatin ribbons. Each of

the ribbons then passes over a rotating die. The dies are designed so

(b) Materials: water, sweeteners, food ingredients, gelatin, “cough syrup

material”, crayon wax, and food coloring.

Labor: People would be needed run the various machines.

Overhead: Depreciation and maintenance of the various machines.

(c) This would appear to be a perfect situation for the use of process

costing. Paintballs are a high volume product, and the paintballs are

very homogenous. While there may be some differences in various

types of paintballs that would merit keeping track of specific costs to

make the various types, the primary method of cost determination

would be process costing.

BYP 21-4 ETHICS CASE

(a) The stakeholders in this situation are:

Jan Wooten, molding department head.

Tony Ferneti quality control inspector.

(b) Tony is placed in an ethical dilemma. He can offend his department head

by disregarding Jan’s instructions and lose the support of his supervisor,

BYP 21-5 CONSIDERING PEOPLE, PLANET, AND PROFIT

(a) Some of the costs that the company now faces include:

• Monetary damages: The company paid $21.4 million in fines as a

result of an OSHA investigation; $1.6 billion to compensate those

affected by the accident; and $1 billion to repair and update its

refinery (plus an additional $250 million to install safety valves)

• Bad publicity

• Lost sales

(b) Some steps that the company could have taken to reduce the environ-

mental failure costs include:

• Install up to date safety equipment