CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-2A

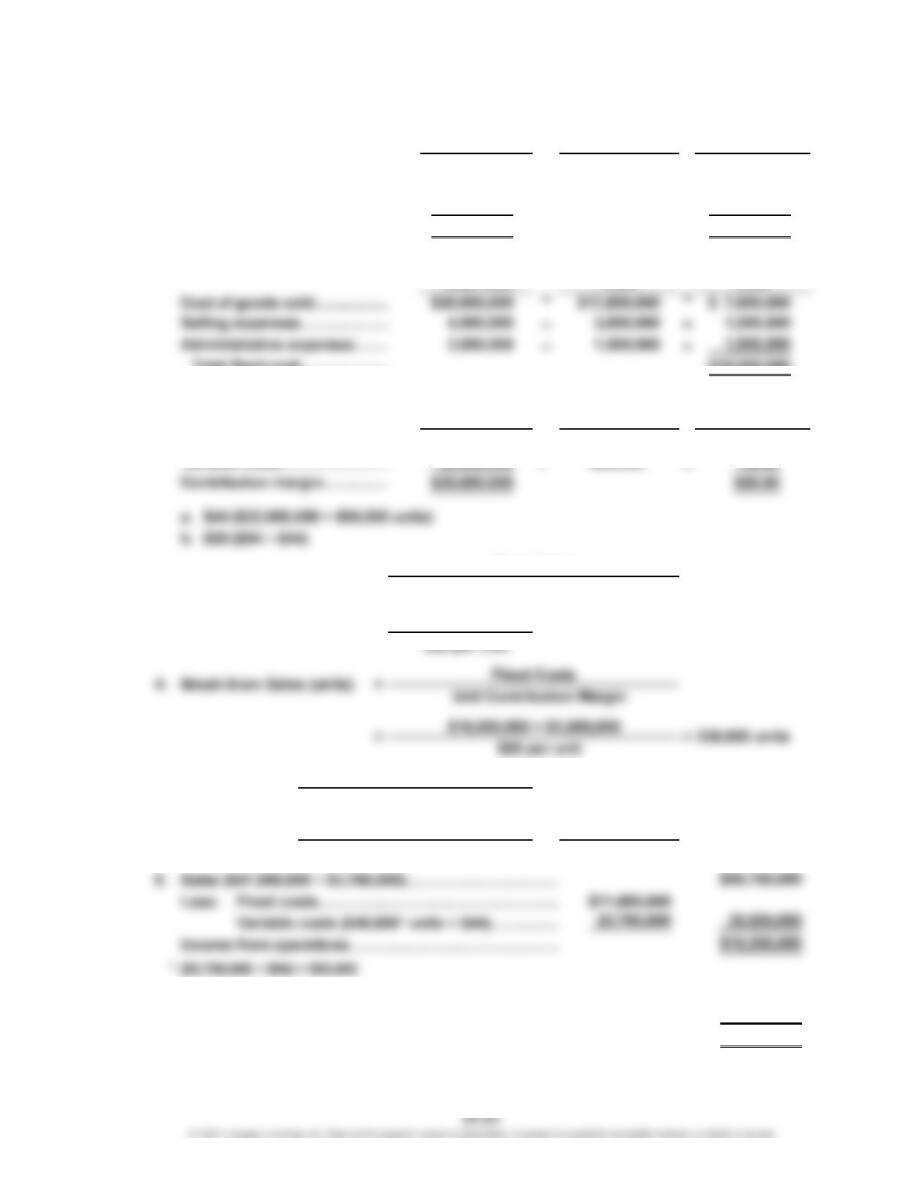

1. Variable Cost Variable

Total Cost Percentage Cost

Cost of goods sold…………… $25,000,000 × 70% = $17,500,000

Selling expenses……………… 4,000,000 × 75% = 3,000,000

Administrative expenses……

…

3,000,000 × 50% = 1,500,000

Total variable cost…………

…

$32,000,000 $22,000,000

Variable Fixed

Total fixed cost………………

$22,000,000 $10,000,000

2. Total Number

Amount of Units Per Unit

Sales……………………………

…

$47,000,000 ÷ 500,000 = $94.00

…

…

$26,800,000

$50 per unit

…

7. Present income from operations…………………………

…

Less additional fixed costs………………………………

…

Income from operations……………………………………

…

200,000 units=

=

5.

3.

=

=

Fixed Costs + Target Profit

Unit Contribution Margin

=

536,000 units==

Sales (units)

$11,800,000 + $15,000,000

$50 per unit

1,800,000

$13,200,000

$15,000,000

Break-Even Sales (units)

$10,000,000

Fixed Costs

Unit Contribution Margin

…

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-2A (Concluded)

8. In favor of the proposal is the possibility of increasing income from operations

from $15,000,000 to $15,200,000. However, there are many points against the

proposal, including:

a. The break-even point increases by 36,000 units (from 200,000 to 236,000).

b. The sales necessary to maintain the current income from operations of

$15,000,000 would be 536,000 units, or $3,384,000 (36,000 units × $94) in

CHAPTER 21 Cost-Volume-Profit Analysis

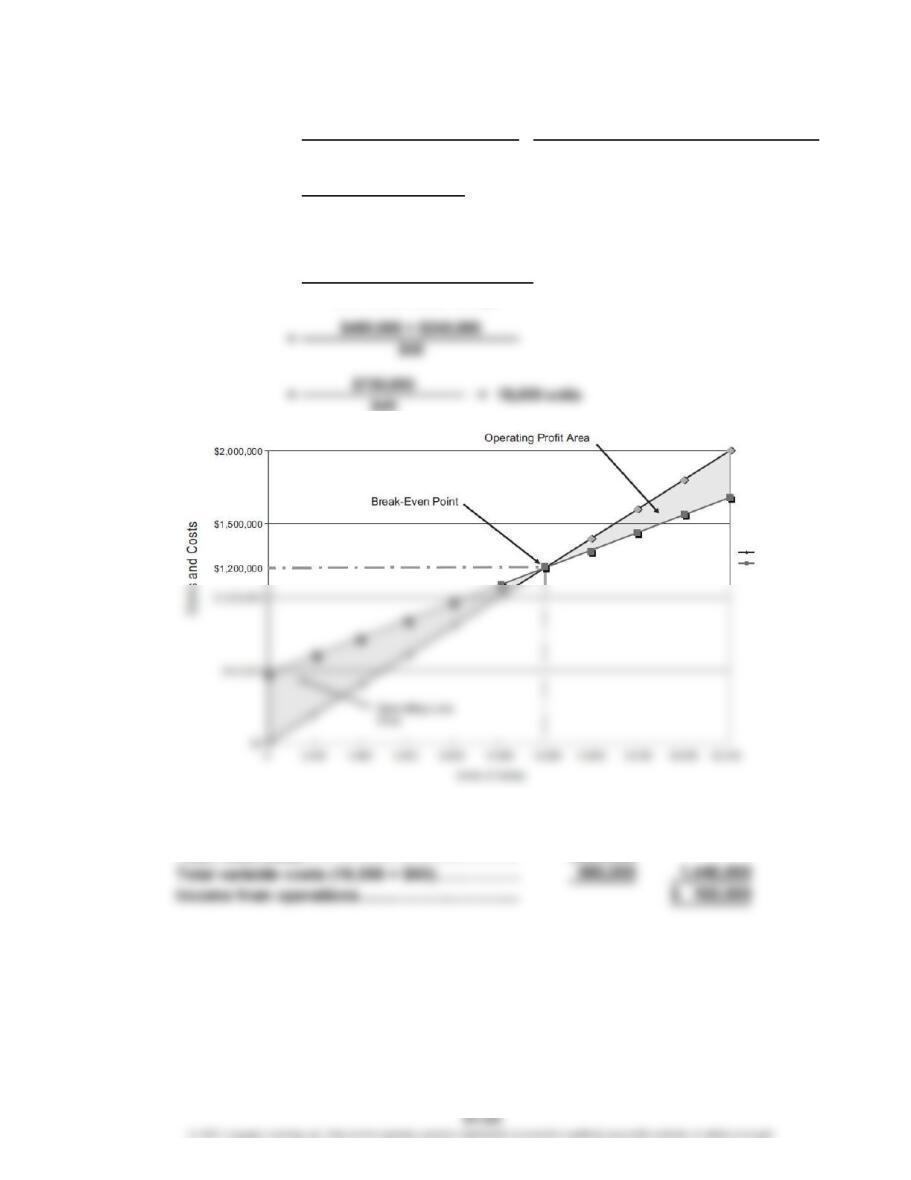

Prob. 21-3A

1. Break-Even

Sales (units)

$480,000

$40*

* $100 unit selling price – $60 unit variable cost

$40

3.

4. Sales (16,000 × $100)……………………………

…

$1,600,000

Total Fixed Costs

Unit Selling Price – Unit Variable Cost

= 12,000 units

Sales (units)

=Total Fixed Costs

Unit Contribution Margin

2. = Fixed Costs + Target Profit

Unit Contribution Margin

=

=

Total Sales

Total Costs

CHAPTER 21 Cost-Volume-Profit Analysis

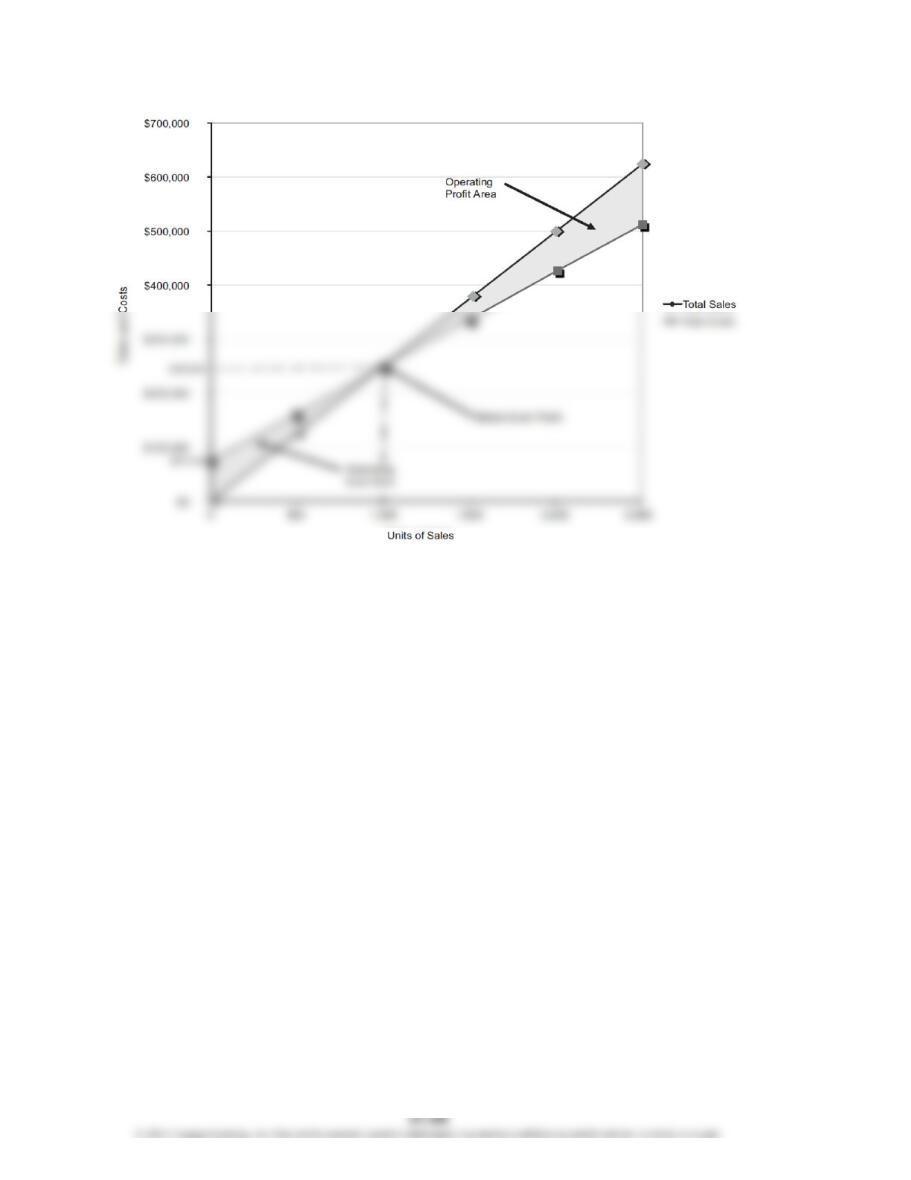

Prob. 21-4A

1.

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4A (Continued)

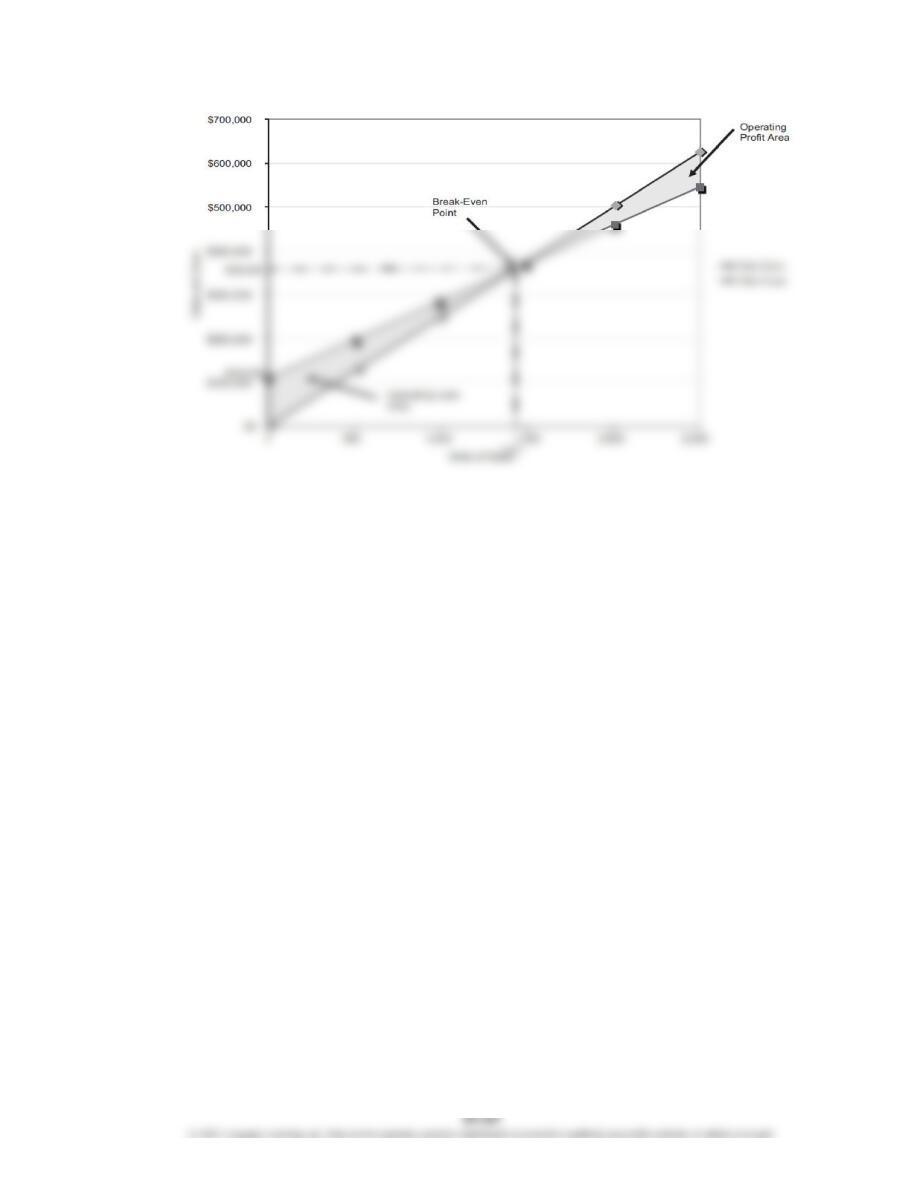

1. Break-Even Units:

Break-Even Dollars:

Break-Even Sales (units) = Total Fixed Costs =Total Fixed Costs

Unit Contribution Margin Unit Selling Price – Unit Variable Cost

$250 Unit Selling Price – $175 Unit Variable Cost

Contribution Margin Ratio = Unit Contribution Margin =Unit Selling Price – Unit Variable Cost

Unit Selling Price Unit Selling Price

=$75,000 = 1,000 units

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4A (Continued)

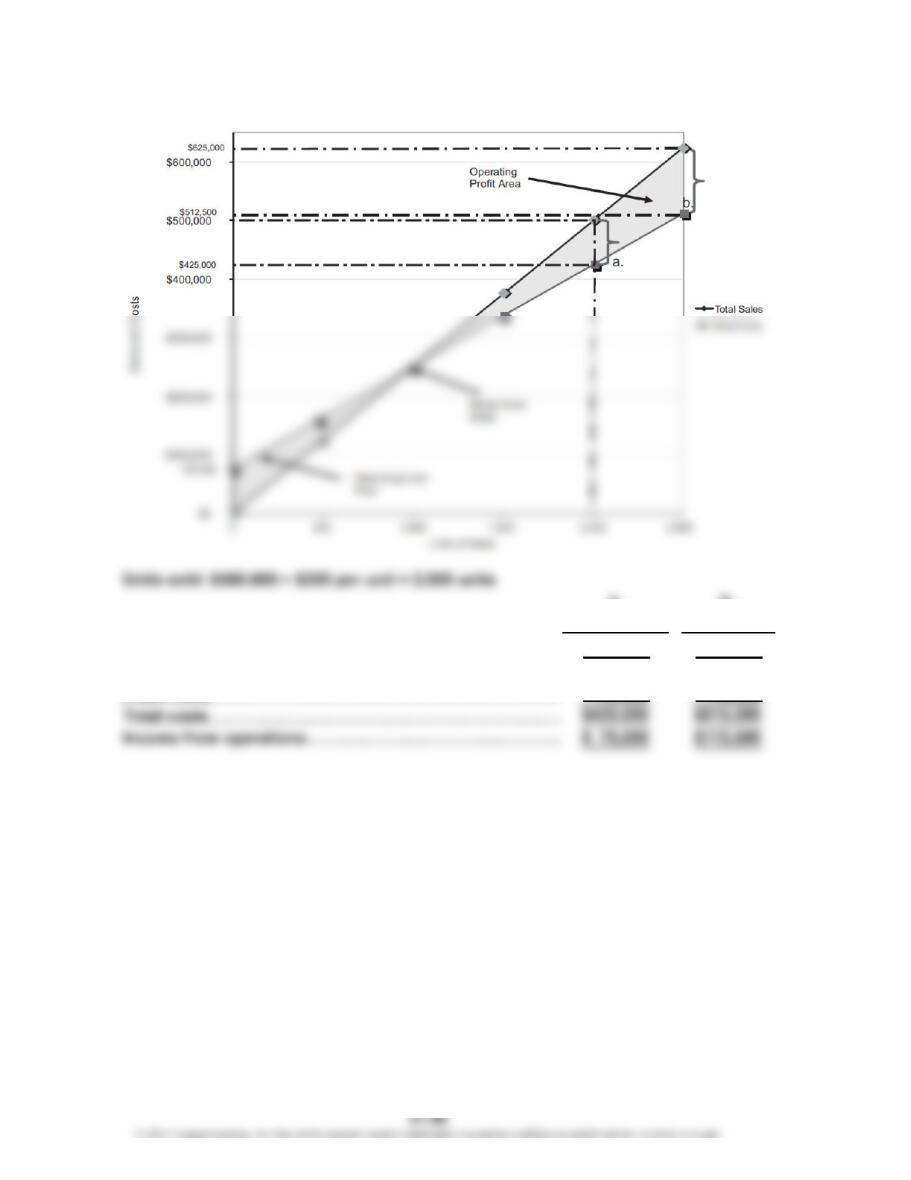

2.

a. b.

2,000 units 2,500 units

Sales………………………………………………………………

…

$500,000 $625,000

V

ariable costs……………………………………………………

…

$350,000 $437,500

CHAPTER 21 Cost-Volume-Profit Analysis

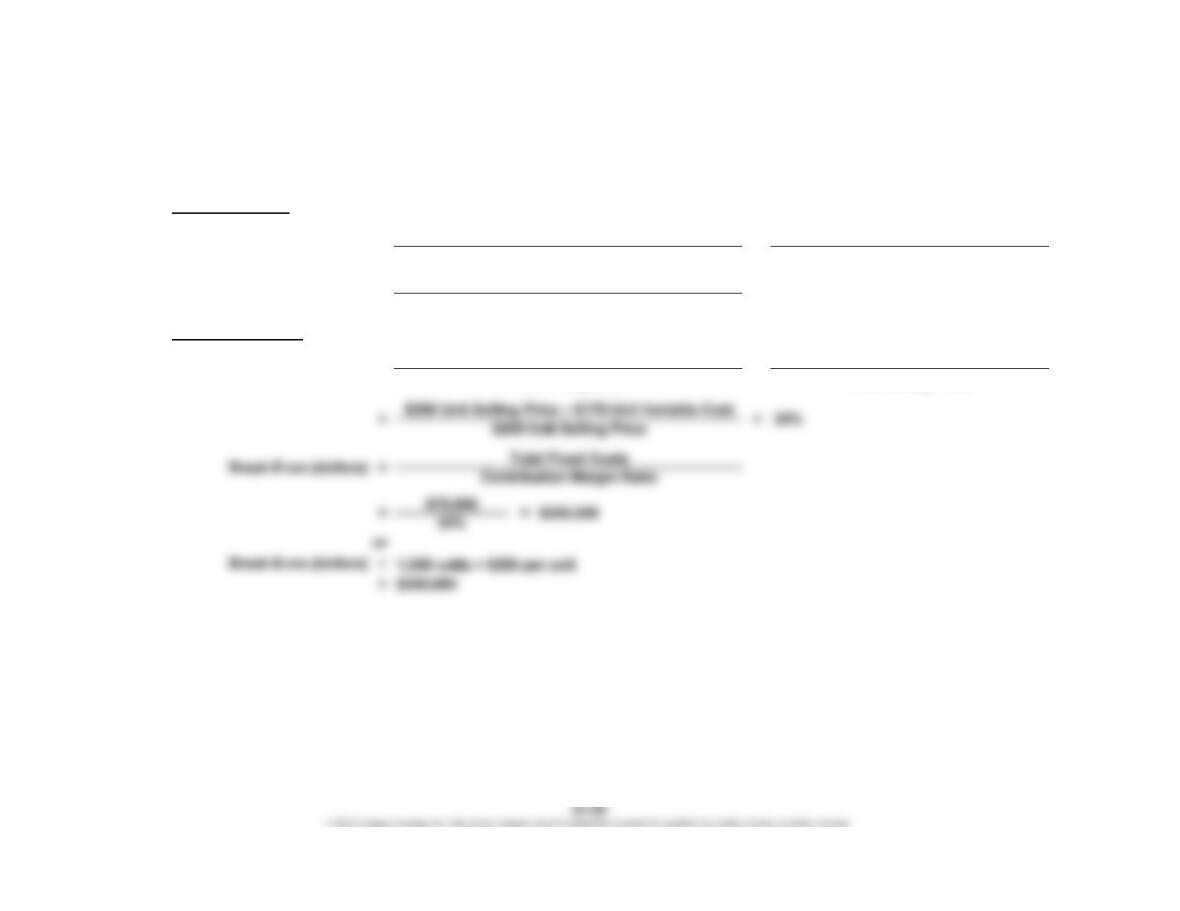

Prob. 21-4A (Continued)

3.

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4A (Continued)

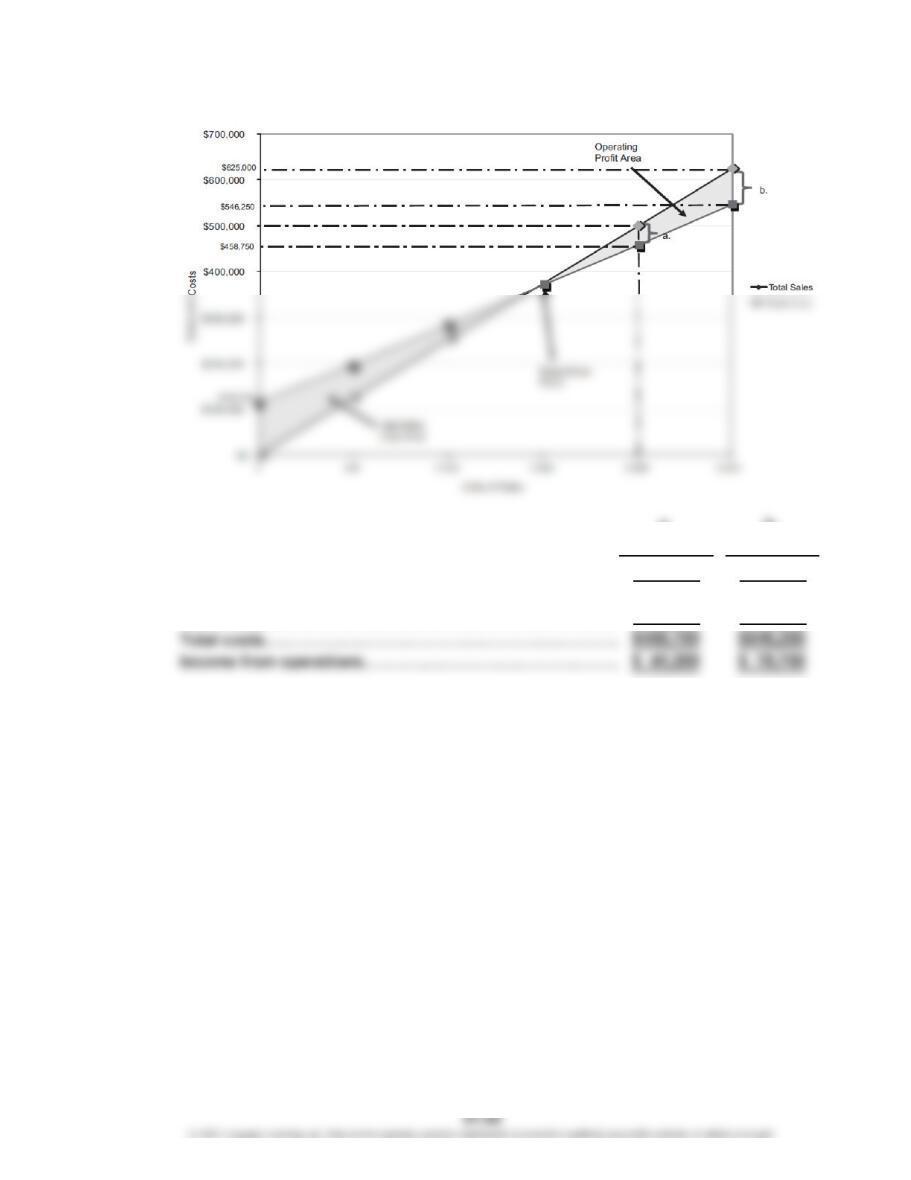

3. Break-Even Units:

Break-Even Dollars:

Break-Even Sales (units) = Total Fixed Costs =Total Fixed Costs

Unit Contribution Margin Unit Selling Price – Unit Variable Cost

=$75,000 + $33,750 = 1,450 units

$250 – $175

Contribution Margin Ratio = Unit Contribution Margin =Unit Selling Price – Unit Variable Cost

Unit Selling Price Unit Selling Price

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-4A (Concluded)

4.

a. b.

2,000 units 2,500 units

Sales………………………………………………………………

…

$500,000 $625,000

V

ariable costs……………………………………………………

…

$350,000 $437,500

Fixed costs………………………………………………………

…

108,750 108,750

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-5A

(Overall product is labeled E.)

1. Unit selling price of E [($1,600 × 40%) + ($850 × 60%)]…………………………

…

$1,150

Unit variable cost of E [($800 × 40%) + ($350 × 60%)]…………………………

…

530

Unit contribution margin of E………………………………………………………

…

$ 620

2. 4,030 units of E × 40% = 1,612 units of laptops

4,030 units of E × 60% = 2,418 units of tablets

3. Unit selling price of E [($1,600 × 50%) + ($850 × 50%)]…………………………

…

$1,225

Unit variable cost of E [($800 × 50%) + ($350 × 50%)]…………………………

…

575

Unit contribution margin of E………………………………………………………

…

$ 650

$2,498,600

3,844 units

==

Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

CHAPTER 21 Cost-Volume-Profit Analysis

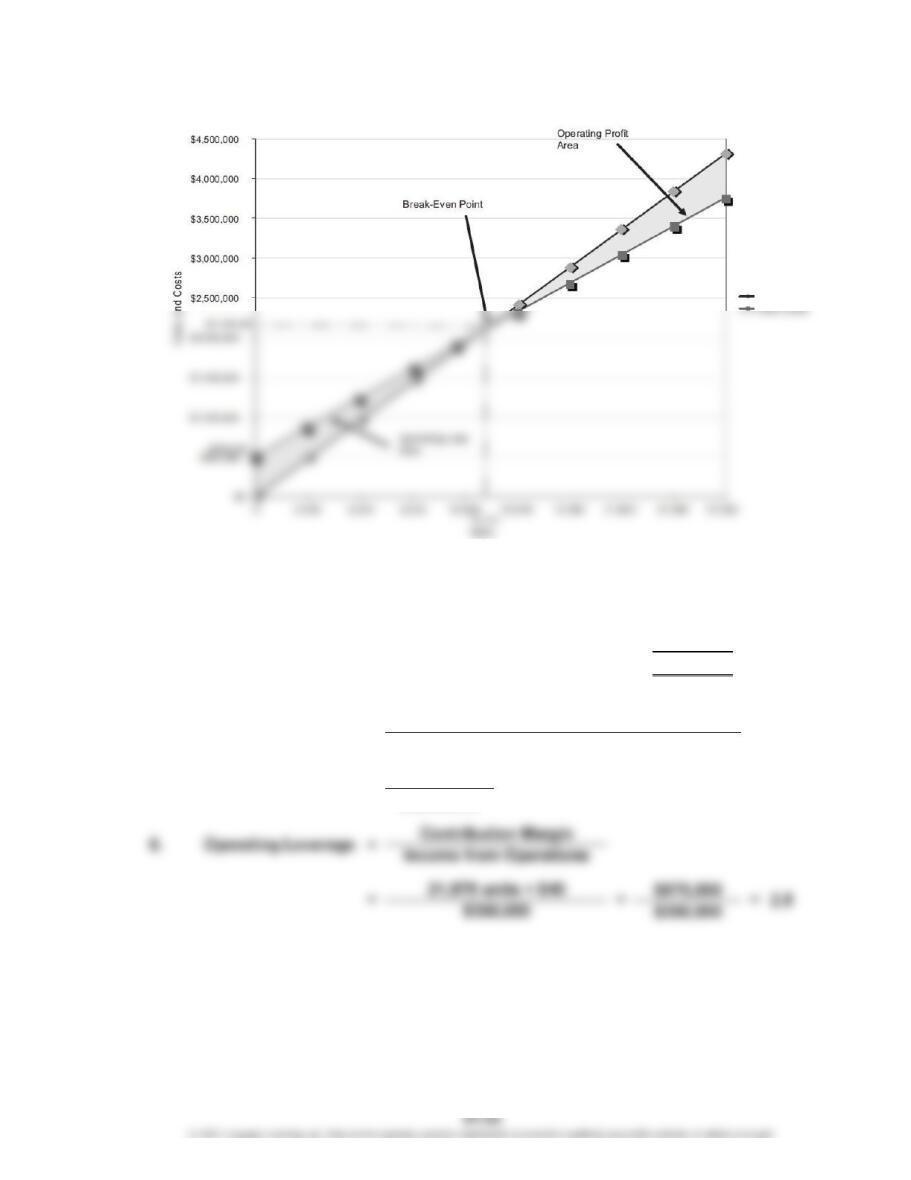

Prob. 21-6A

1.

Sales (21,875 × $160) $3,500,000

Cost of goods sold 2,518,750

Gross profit $ 981,250

Expenses:

Selling expenses:

Sales salaries and commissions

[$110,000 + (21,875 × $8)] $285,000

Advertising 40,000

Travel 12,000

Miscellaneous selling expense

[$7,600 + (21,875 × $1)] 29,475

Total selling expenses $ 366,475

Wolsey Industries Inc.

Estimated Income Statement

For the Year Ended December 31, 20Y8

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-6A (Continued)

$525,000

$160 – $120

13,125 units

3. Break-Even Sales (units)

==

=Fixed Costs

Unit Contribution Margin

2. Contribution Margin Ratio = Sales – Variable Costs

Sales

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-6A (Concluded)

4.

5. Margin of safety:

In dollars:

Expected sales (21,875 × $160)……………………………… $3,500,000

Break-even point (13,125 × $160)……………………………

…

2,100,000

Margin of safety………………………………………………… $1,400,000

As a percentage of sales:

$1,400,000

$3,500,000

=Margin of Safety Sales – Sales at Break-Even Point

Sales

40%==

Total Sales

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-1B

Fixed Variable Mixed

Cost Cost Cost Cost

g. X

h. X

i. X

j. X

k. X

l. X

m. X

n. X

o. X

p. X

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-2B

1. Total Variable Cost Variable

Cost Percentage Cost

Cost of goods sold………………

…

$1,280,000 × 75% = $ 960,000

Selling expenses…………………

…

320,000 × 60% = 192,000

Administrative expenses………

…

620,000 × 40% = 248,000

Total variable cost……………

…

$1,400,000

Total Variable Fixed

Cost Cost Cost

2. Number

Total Amount of Units Per Unit

Sales………………………………… $3,150,000 ÷ 35,000 =$90.00

V

…

$820,000

$50 per unit

6. Sales ($3,150,000 + $720,000)…………………………

…

Less: Fixed costs……………………………………

…

$1,090,000

V

ariable costs (43,000* units × $40)……… 1,720,000

Income from operations………………………………

…

$3,870,000

4. =

Fixed Costs

Break-Even Sales (units)

$820,000 + $270,000

Unit Contribution Margin

2,810,000

$1,060,000

3.

==

Break-Even Sales (units) Fixed Costs

Unit Contribution Margin

16,400 units

=

…

…

…

CHAPTER 21 Cost-Volume-Profit Analysis

Prob. 21-2B (Concluded)

8. In favor of the proposal is the possibility of increasing income from operations

from $930,000 to $1,060,000. However, there are many points against the

proposal, including:

a. The break-even point increases by 5,400 units (from 16,400 to 21,800).

c. If future sales remain at the current level, the income from operations of

$930,000 will decline to $660,000.