Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

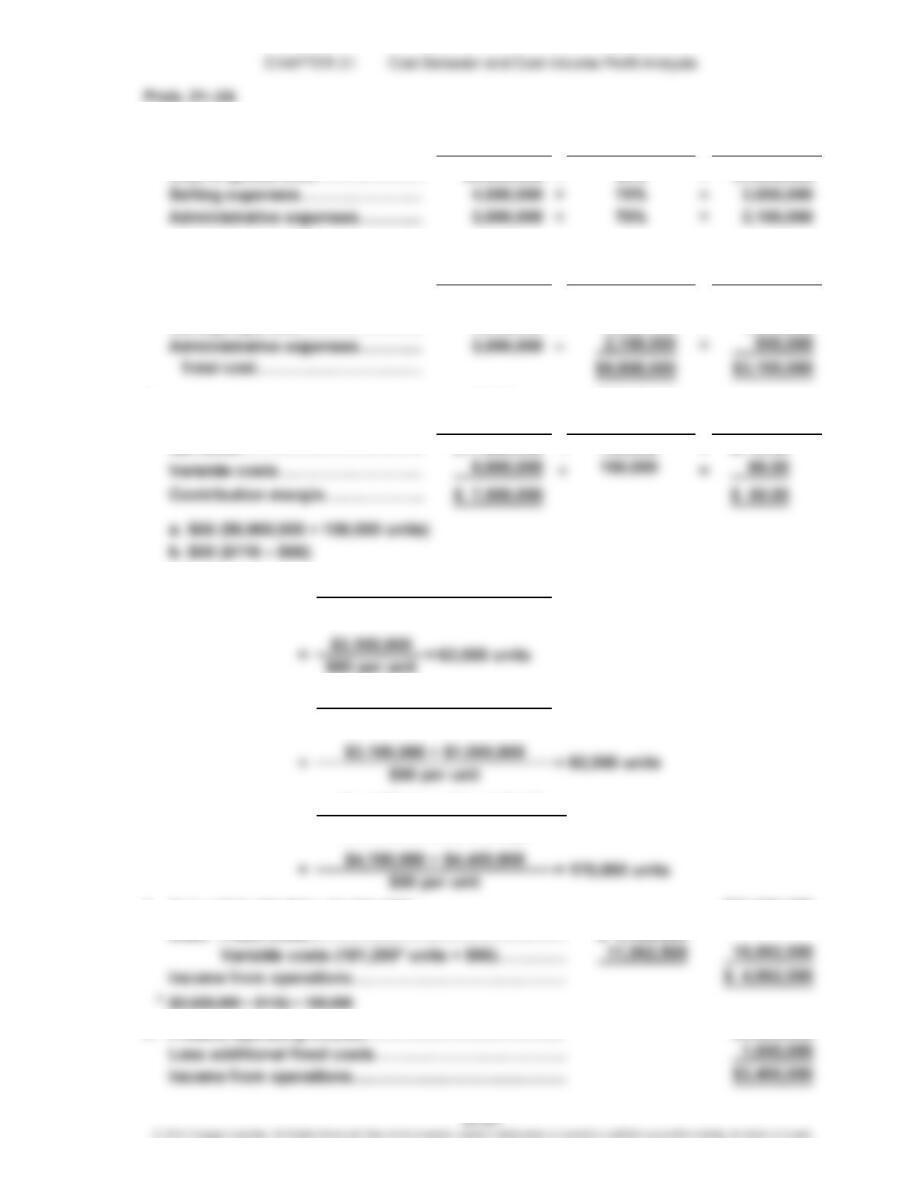

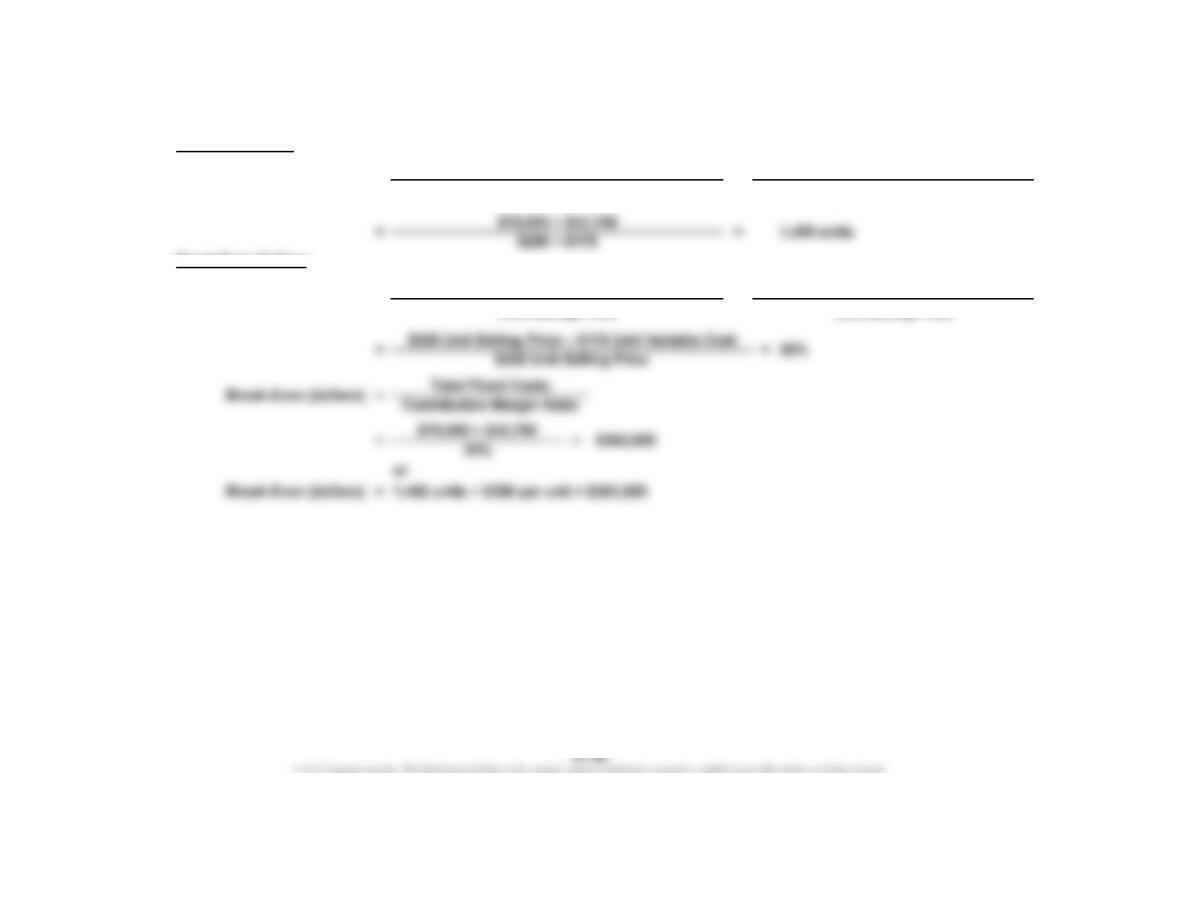

1. Variable Variable

Total Cost Cost Percentage Cost

Cost of goods sold………………

…

$6,000,000 × 80% = $4,800,000

Variable Fixed

Total Cost Cost Cost

Cost of goods sold………………

…

$6,000,000

–

$4,800,000 = $1,200,000

Selling expenses…………………

…

4,000,000 –3,000,000 = 1,000,000

2. Total Number

Amount of Units Per Unit

Net sales……………………………

…

$17,400,000

÷

150,000 = $116.00

$50 per unit

6. Sales ($17,400,000 + $3,625,000)………………………

…

Less: Fixed costs………………………………………… $ 4,100,000

7. Present operating income………………………………

…

Sales (units)

$4,400,000

5.

$21,025,000

4. Break-Even

Sales (units) =Fixed Costs

Unit Contribution Margin

3. Fixed Costs

Unit Contribution Margin

Break-Even

Sales (units) =

Fixed Costs + Target Profit

Unit Contribution Margin

=

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–2A (Concluded)

8. In favor of the proposal is the possibility of increasing income from operations

from $4,400,000 to $4,962,500. However, there are many points against the

proposal, including:

a. The break-even point increases by 20,000 units (from 62,000 to 82,000).

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

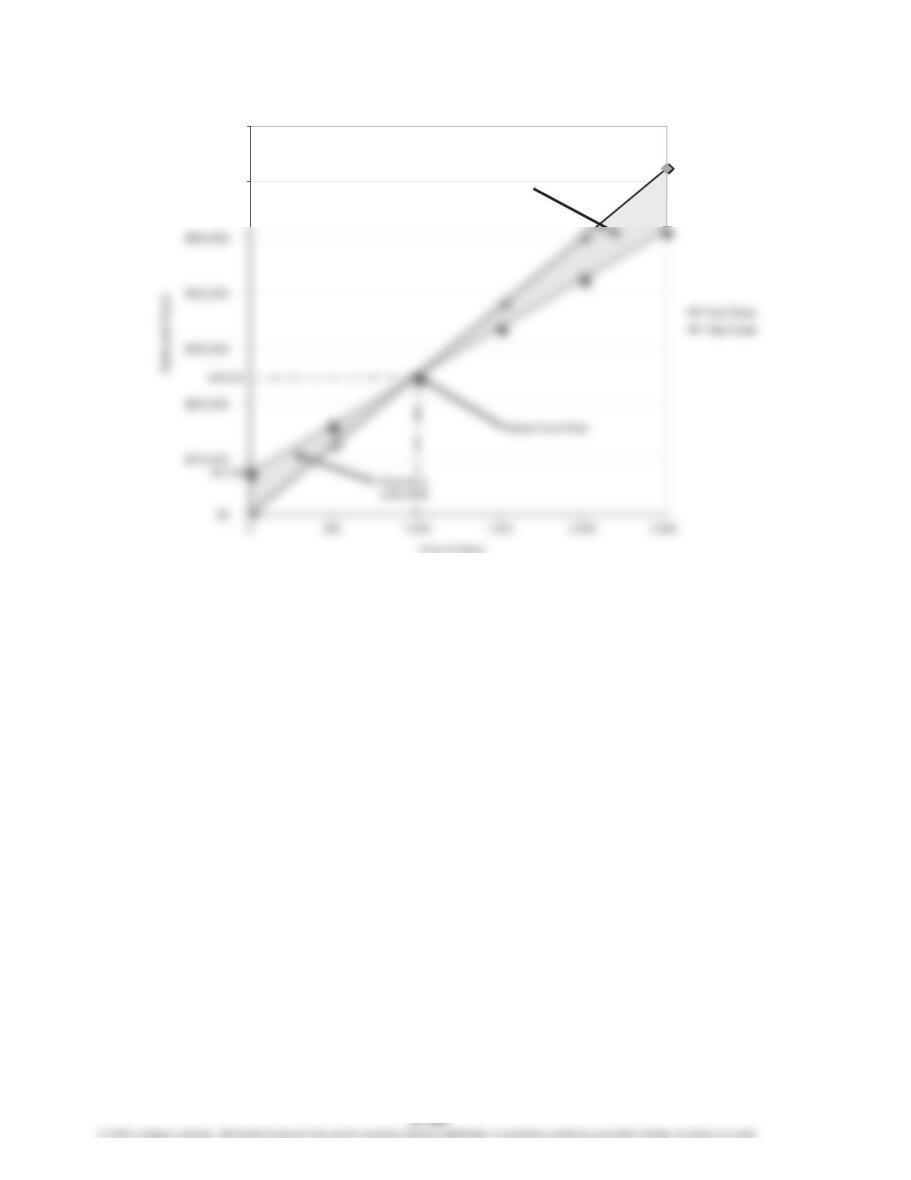

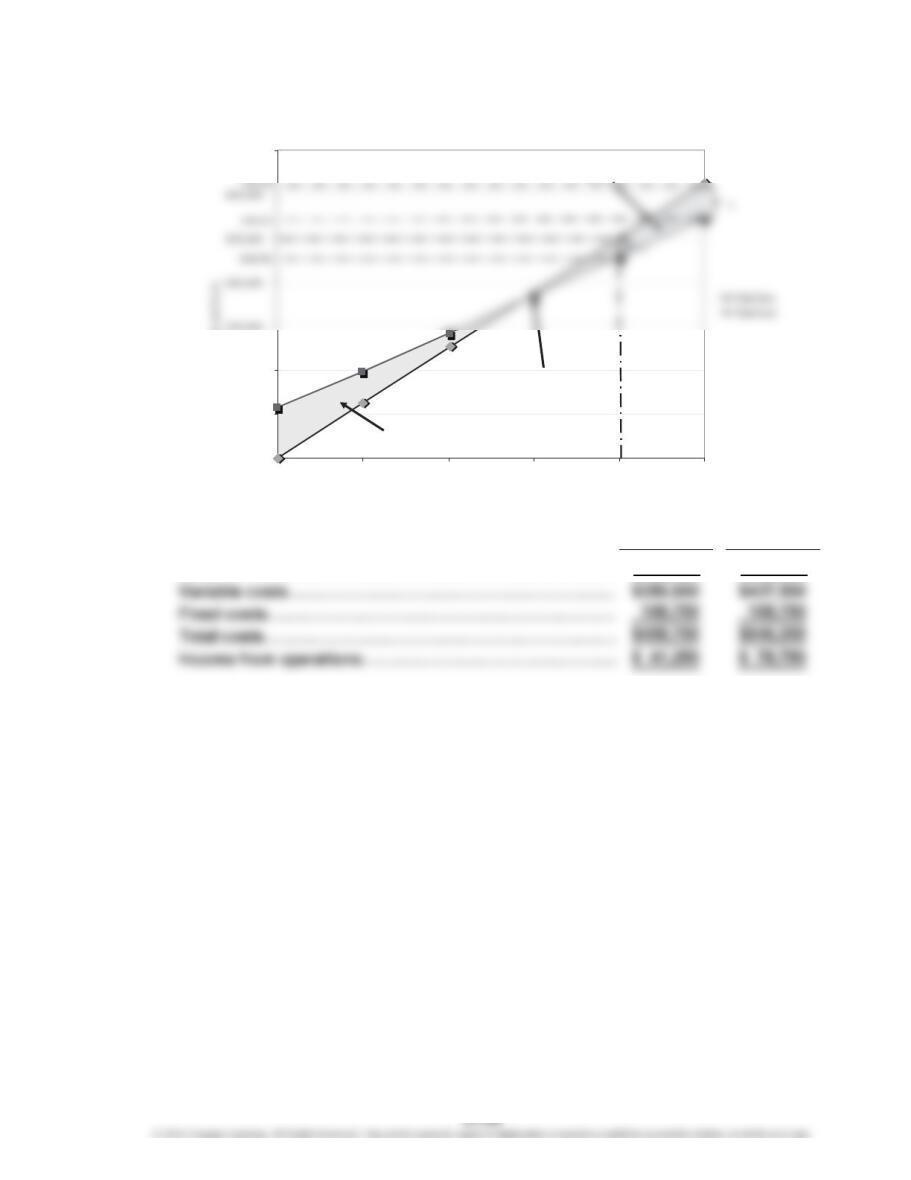

Prob. 21–3A

Break-Even

Sales (units)

3.

4. Sales (16,000 × $100)…………………… $1,600,000

1. = Total Fixed Costs

Unit Contribution Margin

2. = Fixed Costs + Target Profit

Unit Contribution Margin

Sales (units)

=Total Fixed Costs

Unit Selling Price – Unit Variable Cost

$2,000,000

Operating Profit Area

Break-Even Point

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

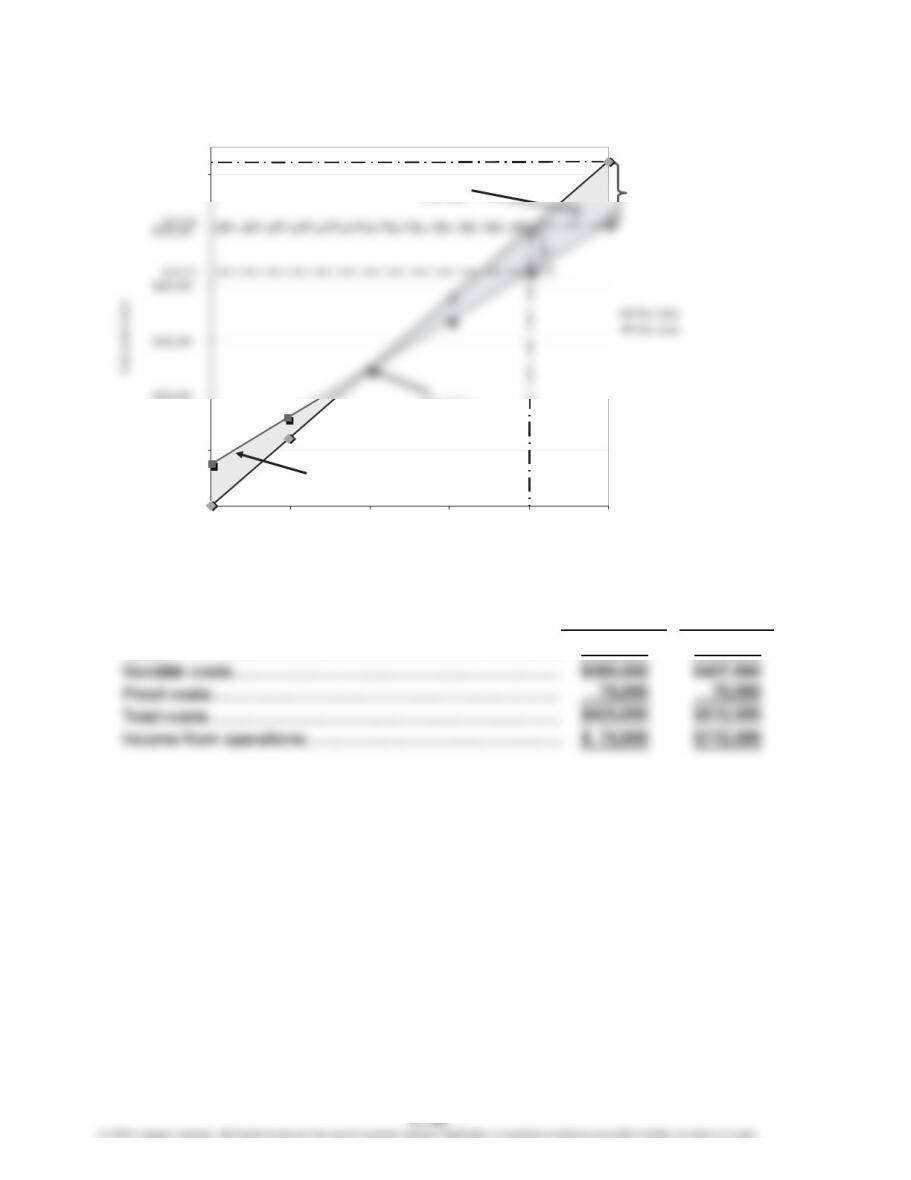

Prob. 21–4A

1.

$600,000

$700,000

Operating

Profit Area

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–4A (Continued)

1. Break-Even Units:

Break-Even Dollars:

Contribution Margin Ratio = Unit Contribution Margin =Unit Selling Price – Unit Variable Cost

Unit Selling Price Unit Selling Price

Break-Even Sales (units) = Total Fixed Costs =Total Fixed Costs

Unit Contribution Margin Unit Selling Price – Unit Variable Cost

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–4A (Continued)

2.

Units sold: $500,000 ÷ $250 per unit = 2,000 units

a. b.

2,000 units 2,500 units

Sales………………………………………………………………

…

$500,000 $625,000

$0

$100,000

$600,000

0 500 1,000 1,500 2,000 2,500

Units of Sales

Operating

Profit Area

Break-Even

Point

Operating Loss

Area

$625,000

$75,000

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–4A (Continued)

3.

$600,000

$700,000

Operating

Profit Area

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–4A (Continued)

3. Break-Even Units:

Break-Even Dollars:

Contribution Margin Ratio = Unit Contribution Margin =Unit Selling Price – Unit Variable Cost

Unit Selling Price Unit Selling Price

Break-Even Sales (units) = Total Fixed Costs =Total Fixed Costs

Unit Contribution Margin Unit Selling Price – Unit Variable Cost

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–4A (Concluded)

4.

a. b.

2,000 units 2,500 units

Sales………………………………………………………………

…

$500,000 $625,000

$0

$100,000

$200,000

$700,000

0 500 1,000 1,500 2,000 2,500

Sales and Costs

Units of Sales

Operating

Profit Area

Break-Even

Point

Operating

Loss Area

$108,750

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–5A

(Overall product is labeled E.)

1. Unit Selling Price of E [($1,600 × 40%) + ($850 × 60%)]…………………………

…

$1,150

530

2. 4,030 units of E × 40% = 1,612 units of laptops

3. Unit selling price of E [($1,600 × 50%) + ($850 × 50%)]…………………………

…

$1,225

Unit variable cost of E [($800 × 50%) + ($350 × 50%)]…………………………

…

575

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–6A

1.

Sales (21,875 × $160) $3,500,000

Cost of goods sold:

Direct materials (21,875 × $46) $1,006,250

Expenses:

Selling expenses:

Sales salaries and commissions

[$110,000 + (21,875 × $8)] $285,000

Advertising 40,000

WOLSEY INDUSTRIES INC.

Estimated Income Statement

For the Year Ended December 31, 2016

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

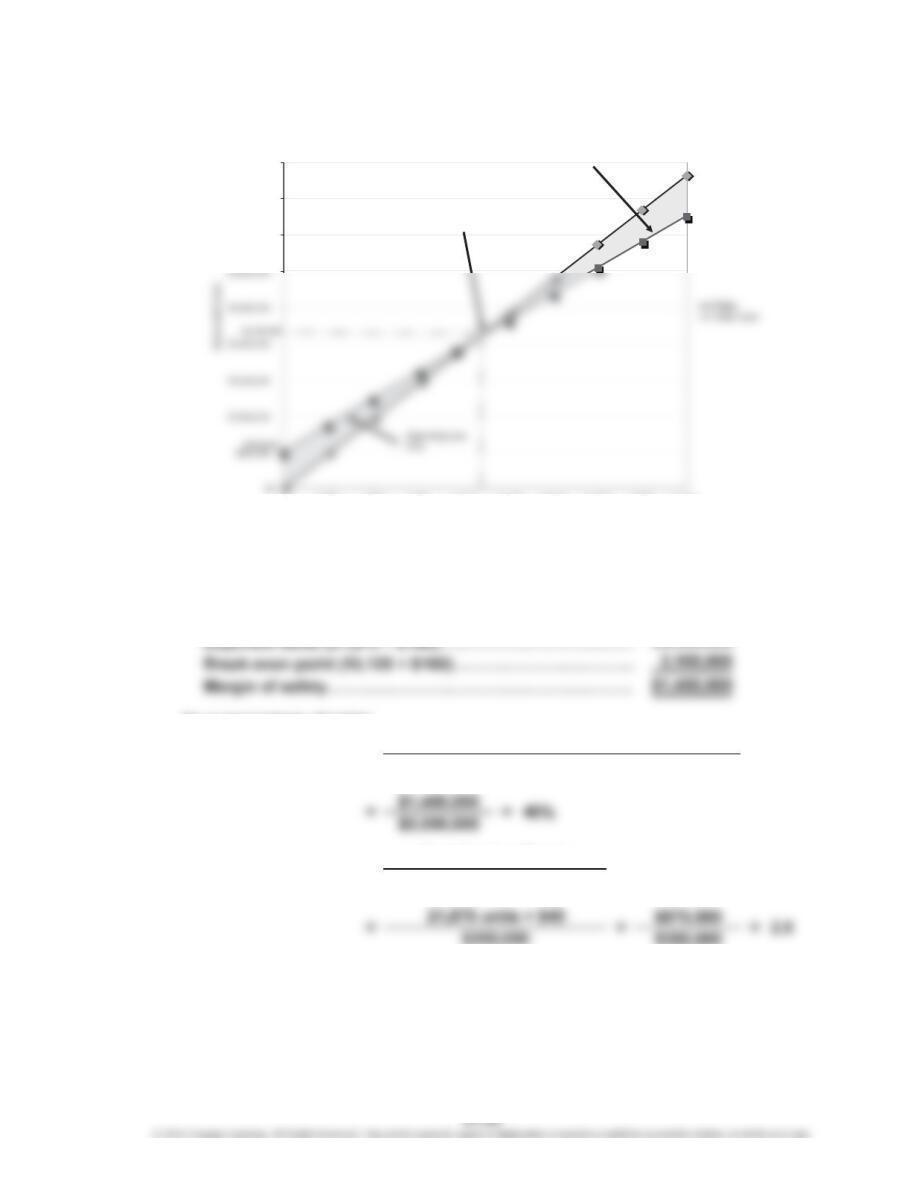

Prob. 21–6A (Continued)

$525,000

$160 – $120

=Fixed Costs

Unit Contribution Margin

2. Contribution Margin Ratio = Sales – Variable Costs

Sales

==

3. Break-Even Sales (units)

13,125 units

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–6A (Concluded)

4.

5. Margin of safety:

In dollars:

$3,500,000

As a percentage of sales:

=Margin of Safety Sales – Sales at Break-Even Point

Sales

Contribution Margin

Income from Operations

6. Operating Leverage =

$3,500,000

$4,000,000

$4,500,000

0 3,000 6,000 9,000 12,000 15,000 18,000 21,000 24,000 27,000

Units

Operating Profit

Area

Break-Even Point

13,125

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–1B

Fixed Variable Mixed

Cost Cost Cost Cost

a. X

b. X

j. X

k. X

l. X

m. X

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

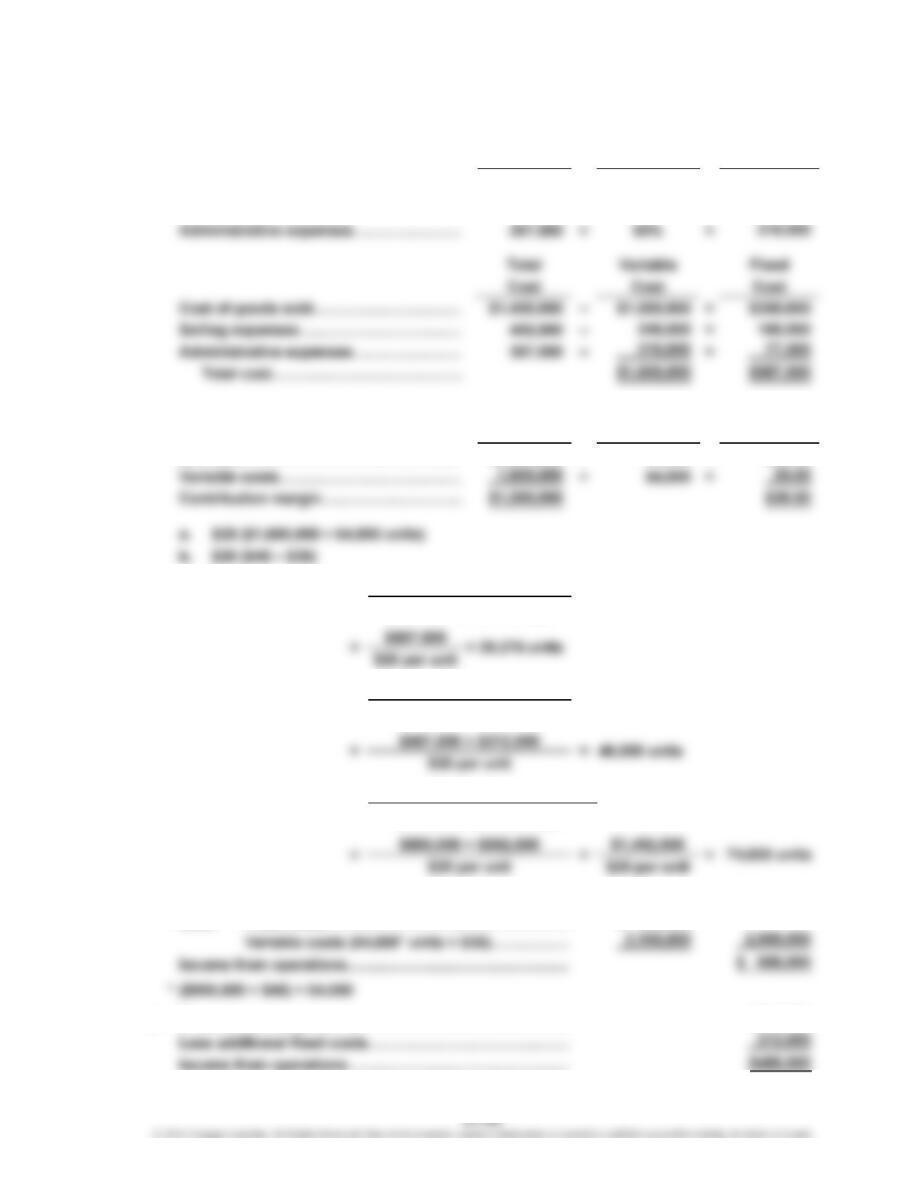

Prob. 21–2B

1. Total Variable Cost Variable

Cost Percentage Cost

Cost of goods sold…………………………

…

$1,400,000 × 75% = $1,050,000

Selling expenses…………………………… 400,000 × 60% = 240,000

2. Number

Total Amount of Units Per Unit

Net sales……………………………………

…

$2,880,000 ÷ 64,000 =$45.00

6. Sales ($2,880,000 + $900,000)………………………………

…

Less: Fixed costs…………………………………………

…

$ 800,000

7. Present operating income……………………………………

…

5. Unit Contribution Margin

Break-Even

Sales (units)

$692,500

Sales (units)

=

=

3. Fixed Costs

Unit Contribution Margin

4. Break-Even

Sales (units) =

Fixed Costs

Unit Contribution Margin

$3,780,000

Fixed Costs + Target Profit

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 21–2B (Concluded)

8. In favor of the proposal is the possibility of increasing income from operations

from $692,500 to $880,000. However, there are many points against the

proposal, including:

a. The break-even point increases by 10,625 units (from 29,375 to 40,000).