CHAPTER 21

UNDERSTANDING THE ISSUES

1. Given a restructuring that is not under

bankruptcy law, the gain on restructuring is

measured as the amount by which the book

value of the debt, including accrued inter-

est, exceeds the total of all restructured

principal and interest payments. If the total

the restructured consideration received.

The value of the consideration received is

the net present value of the restructured

payments.

2. A corporate reorganization is a legal remedy

designed to restructure the debt and/or eq-

uity of a troubled company so that the

company may continue to operate and

3. If a creditor is fully secured, by definition no

portion of their claim will become unse-

cured. However, if the value of the assets

securing their claim exceeds the amount of

the claim, such excess amounts will

become available to unsecured creditors.

of priority.

4. The statement of realization and liquidation

serves several purposes. First, it provides a

reporting of the activities of the trustee in

liquidation and helps discharge the fidu-

ciary responsibility. The statement also

documents that available assets are being

distributed properly among the various

Ch. 21—Exercises 21–2

EXERCISES

Note: Some calculations may vary due to rounding or method of calculation. Answers presented

have been determined using Excel.

EXERCISE 21-1

Alternative A—Income Statement Impact

First Month:

Gain on land:

Fair market value ………………………………………………………………. $ 380,000.00

the net present value of the restructured loan is $183,306 determined as follows:

Where: The number of payments is …………………………………… 40

The periodic payment is ……………………………………….. $5,067.60

The future value is ………………………………………………. $ —

Periodic interest rate is ………………………………………… 0.50%

21–3 Ch. 21—Exercises

Exercise 21-1, Continued

Second Month:

Interest expense:

Current carrying value ……………………………………………………….. $ 182,654.73

where n = 39, interest rate = 0.40%,

Using the original loan’s effective of interest rate of 0.5% (6% divided by 12 months),

the net present value of the restructured loan is $155,177 determined as follows:

Where: The number of payments is …………………………………… 60

The periodic payment is ……………………………………….. $3,000.00

The future value is ………………………………………………. $ —

Interest expense:

The implicit interest rate on the new debt is 0.39% per month determined as follows:

Where: The number of payments is …………………………………… 60

The periodic payment is ……………………………………….. $ 3,000.00

The future value is ………………………………………………. $ —

Exercise 21-1, Concluded

Second Month:

EXERCISE 21-2

Interest Bearing Debt ……………………………………………………………. 300,000

Preferred Stock (at par) …………………………………………………… 50,000

Paid-In Capital in Excess of Par ……………………………………….. 200,000

Gain on Restructuring ……………………………………………………… 50,000

To record extinguishment of debt.

EXERCISE 21-3

(1) The impact on the ratios is directly related to how each of the actions taken by manage-

ment impacts the financial statements. The recognition of impairment losses will decrease

long-lived assets and decrease net income and corresponding shareholders’ equity. Future

periods will base depreciation/amortization on the long-lived assets on the lower impaired

value, which will increase future income. The restructuring of the long-term debt will result

in a restructuring gain. However, since the future cash payments are less than the carrying

basis of the original debt, no interest expense will be recognized in future periods. The

adjustment of the par value of common stock in order to eliminate the deficit in retained

earnings will have no impact on net income nor will it change the total amount of share-

(2) Net income in future periods would be affected by lower depreciation/amortization expense

EXERCISE 21-4

Outstanding Debt

A B C D

Total amount due ………………………… $ 84,000 $ 520,000 $328,000 $350,000

Less amounts applied against debt:

Value of assets transferred ……… (80,000) (120,000) — (48,339)

Value of stock transferred ……….. (380,000) —

Remaining debt …………………………… $ 4,000 $ 20,000 $328,000 $301,661

Regarding Debt C: Because the total of the periodic payments is less than the remaining debt,

there would be a gain of restructuring in the amount of $28,000. Furthermore, because the pe-

riodic payments are less than the remaining debt, no interest expense would be recognized. All

periodic payments are considered to be a reduction of the revised principal amount due of

$300,000.

EXERCISE 21-5

July 1 Quarter 3 Quarter 4 Total

Debt A (see note 1):

Gain on transfer of land……..……

…

$175,000

$

175,000

Gain on restructuring………………

…

64,000 64,000

$

$

$

Gain on restructuring …………………………………………………………. $ 64,000

Because the sum of the restructured payments equal the restructured carry value of

the debt, there is no recognized interest expense.

Note 2 Original carrying value of debt …………………………………………….. $2,152,500.00

Less: Fair value of stock …………………………………………………….. (500,000.00)

Remaining carry value ……………………………………………………….. $1,652,500.00

Sum of restructured payments (7 × $193,553.02 plus $400,000) $1,754,871.14

Payment Interest Principal Balance

Beginning balance $1,652,500.00

Payment 1 $193,553.02 $21,482.50 $172,070.52 1,480,429.48

Payment 2 193,553.02 19,245.59 174,307.43 1,306,122.05

Payment 3 193,553.02 16,979.59 176,573.43 1,129,548.62

Payment 4 193,553.02 14,684.14 178,868.88 950,679.74

EXERCISE 21-6

(1) Quarterly

Item Cash Outflows

Loan A restructuring:

$3,580,000 restructured at 10%, 8 years, and monthly

installments. The monthly payment is $50,000 ………………………………. $150,000

Loan B restructuring:

(2) Effect on Net Income If

Part of a Not Part of a

Item Formal Filing Formal Filing

Loan A restructuring:

Gain on forgiveness of debt ………………………………………… … $500,000 $500,000

Gain on restructuring of remaining debt:

Total payments = $4,800,000 (96 × $50,000). Net present

value of payments at 10% is $3,295,074 vs. carrying basis of

$3,580,000 ……………………………………………………………… 284,926 —

The effective interest rate on the restructured note (0.64% per month) is less than the ef-

fective interest rate of the original note (1% per month). Therefore, the lender has made a

concession.

EXERCISE 21-7

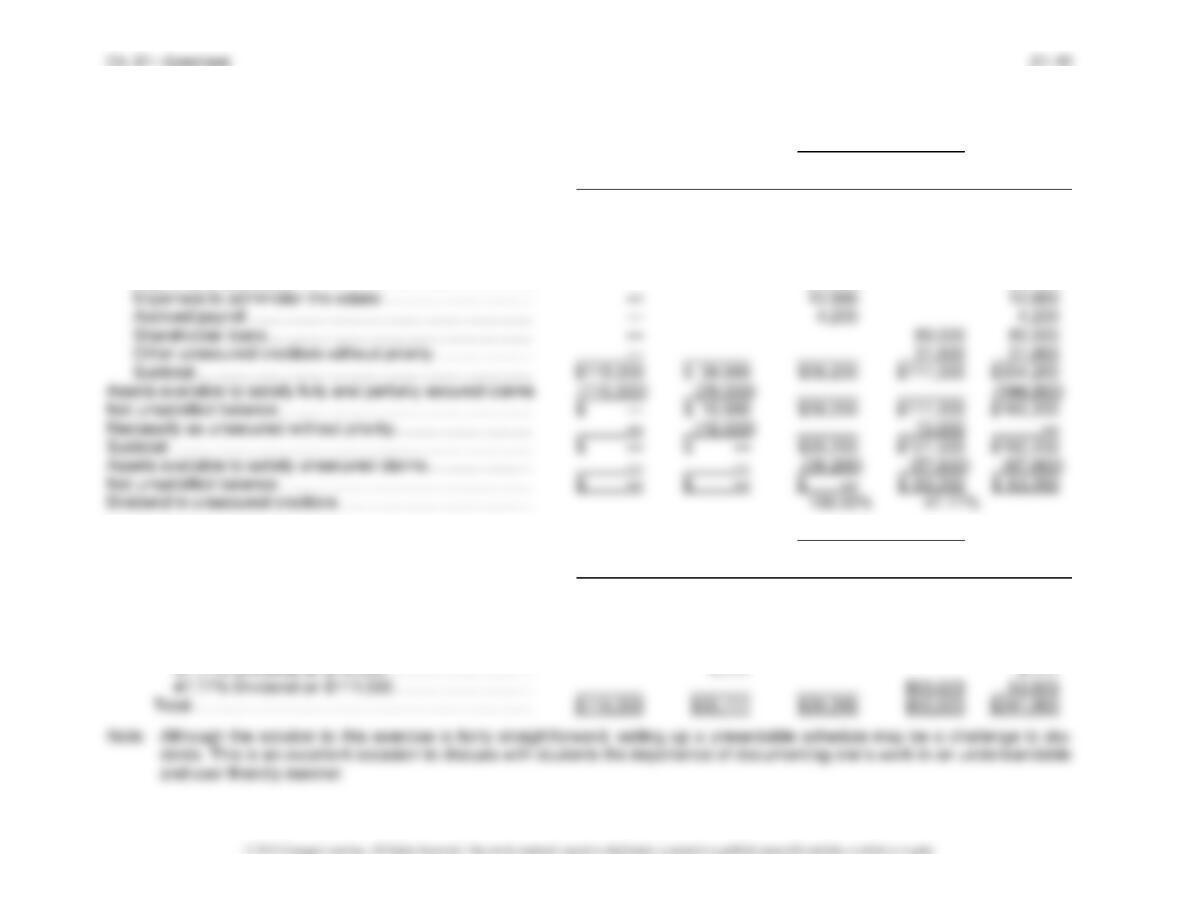

Liabilities

Unsecured

Fully Partially With Without

Secured Secured Priority Priority Total

Accounts payable …………………….. $130,000 $150,000 $ 280,000

Note payable—A ……………………… $560,000 40,000 600,000

Realizable

Value

Assets to be applied against

the liabilities:

Inventory $ 150,000 $130,000 $ 20,000 $ 150,000

Inventory ……………………………… 200,000 $200,000 200,000

Receivables …………………………. 360,000 360,000 360,000

Equipment ……………………………. 300,000 300,000 300,000

Total consideration to be received by Note B:

Received toward partially secured portion ……………………….. $300,000

EXERCISE 21-8

Unsecured

Fully Partially With Without

Claims against the bankrupt estate: Secured Secured Priority Priority Total

Bank loan balance and accrued interest …………………… $ 85,000 $ — $ — $ — $ 85,000

Dealer-financed vehicle loan …………………………………… — 18,000 18,000

Accounts payable due vendors ……………………………….. — 21,000 21,000

Line of credit due…………………………………………………… 30,000 30,000

Payroll and taxes due …………………………………………….. — 23,000 23,000

Unsecured

Fully Partially With Without

Amounts received by each major class of creditor: Secured Secured Priority Priority Total

Amounts received:

Secured amount received …………………………………… $115,000 $29,000 $144,000

Unsecured amount received:

100% Dividend on $39,200 …………………………….. $39,200 39,200

EXERCISE 21-9

(1) The Rodak Corporation

Statement of Realization and Liquidation

For Period July 1, 2014, to August 12, 2014

Liabilities

Unsecured

Assets

Fully Partially With Without Owners’

Cash

Noncash Secured Secured Priority Priority Equity

Beginning balances, assigned

July 1, 2014 ……………………….. $ 12,000 $590,000 $200,000 $175,000 $54,000 $150,000 $ 23,000

Cash receipts:

Sale of inventory ………………… 30,000 (25,000) 5,000

Collection on receivables …….. 39,000 (54,000) (15,000)

(2) Estimated assets available:

Cash ……………………………………………………………………………………….. $ 66,500

Estimated value of noncash assets ……………………………………………… 410,000

Ch. 21—Problems 21–12

PROBLEMS

PROBLEM 21-1

Jan. 1, 2014 Cash …………………………………………………………………….. 4,915,562

Deferred Debt Issuance Costs ………………………………….. 84,438

June 30, 2014 Interest Expense …………………………………………………… 157,298

Deferred Debt Issuance Costs …………………………….. 7,298

Cash ………………………………………………………………… 150,000

To record semi-annual interest at the effective interest rate of 3.20% per six

months. Where, PV = $4,915,562, FV = $5,000,000, interest = $150,000, and

n = 10.

Effective interest rate per six months ……………………….. 3.20%

Interest Deferred Debt Interest NPV of

Payment Issuance Expense Debt

Jan. 1, 2014 84,438 4,915,562

June 30, 2014 (150,000) (7,298) 157,298 4,922,860

Dec. 31, 2014 Interest Expense ……………………………………………………. 157,532

Deferred Debt Issuance Costs …………………………….. 7,532

Cash ………………………………………………………………… 150,000

To record semi-annual interest at the effective rate of 3.2%.

June 30, 2015 Interest Expense …………………………………………………… 157,773

The effective interest rate on the original debt prior to restructuring was 3.11% semiannual

Where: Number of periods is……….… 7

Periodic payment is…………… $ 150,000

Future value is………………… $5,150,000 ($5,000,000 + $150,000 unpaid interest)

Net present value is…………… $5,088,164 ($4,938,164 + $150,000 unpaid interest)

The effective interest rate on the restructured debt is ………………………. 3.09% semiannual

Where: Number of periods is……….… 10