EXERCISE 21–12

To: David Skaros

From: Student

Re: Ending inventory

The reason for any confusion related to your department’s ending inventory

quantity stems from the fact that the quantity can be measured in two different

ways, depending on what the information is used for.

The ending inventory quantity can be measured in physical units or equivalent

units. Physical units are actual units present without regard to the stage of

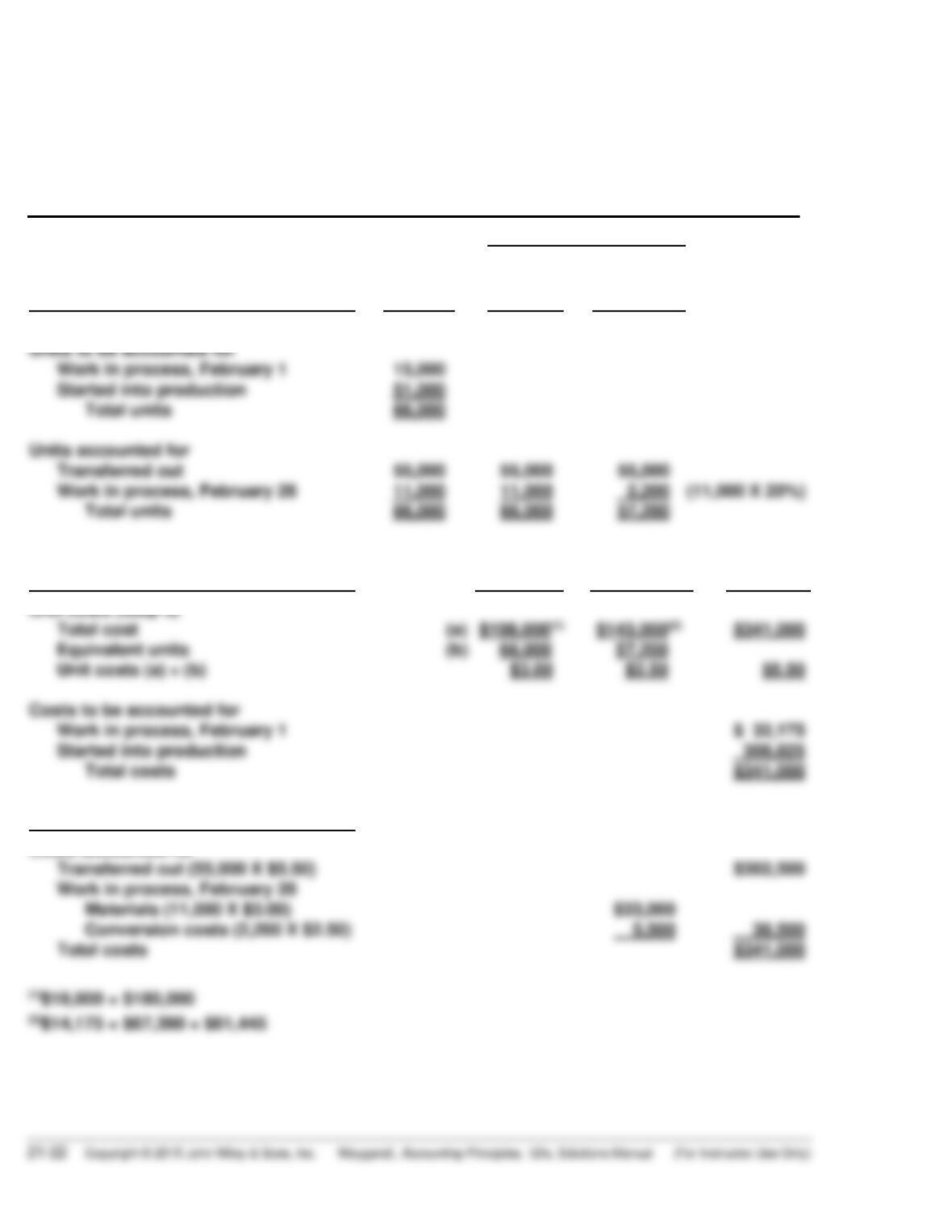

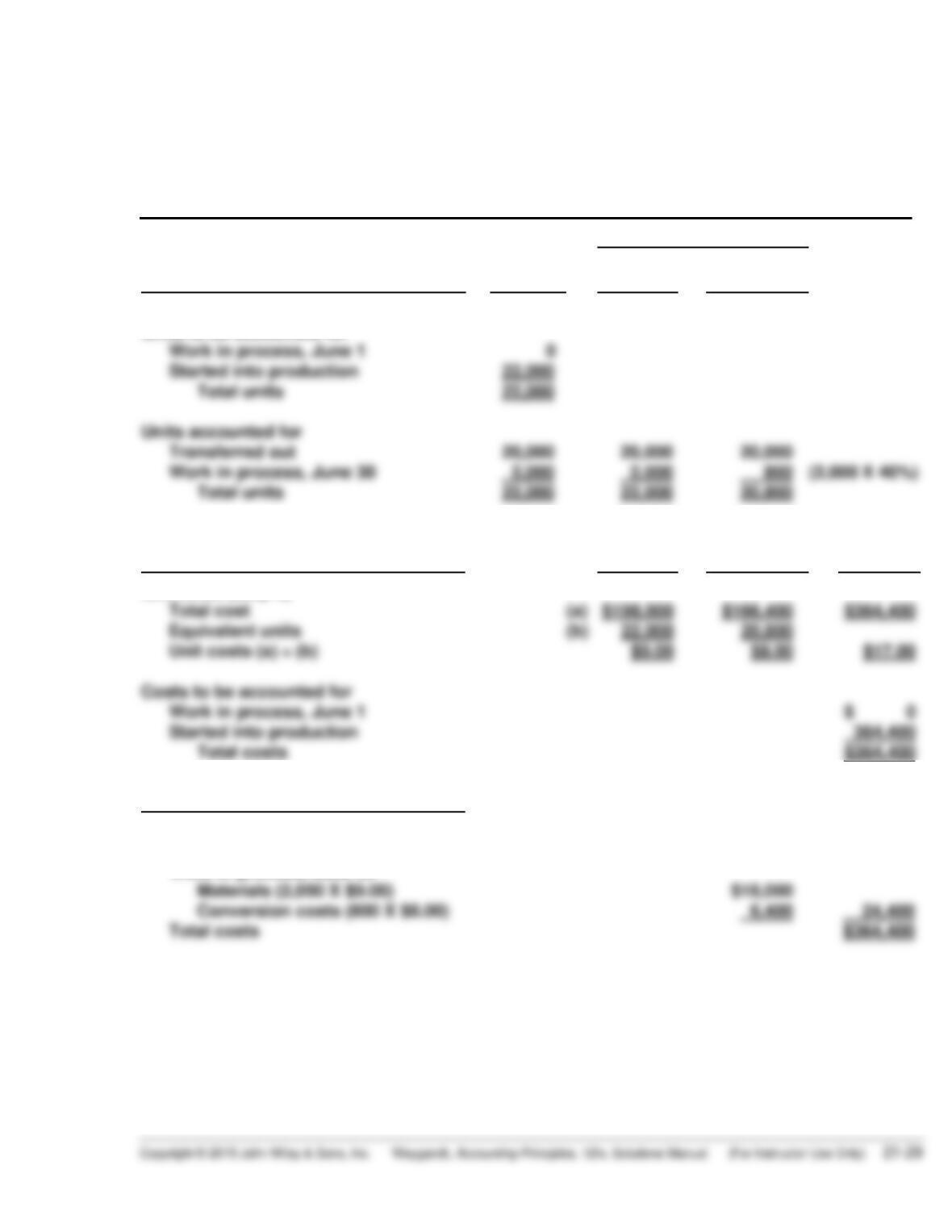

EXERCISE 21–13

HEALTHY COMPANY

Welding Department

Production Cost Report

For the Month Ended February 28, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversio

n

Costs

(Step 1)

(Step 2)

Work in process, February 28

(11,000 X 20%)

Total units

Units to be accounted for

Work in process, February 1

15,000

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Total cost

Equivalent units

(a)

(b)

$198,000(1)

66,000

$143,000(2)

57,200

$341,000

Cost Reconciliation Schedule (Step 4)

Conversion costs (2,200 X $2.50)

Total costs

Costs accounted for

Transferred out (55,000 X $5.50)

$302,500

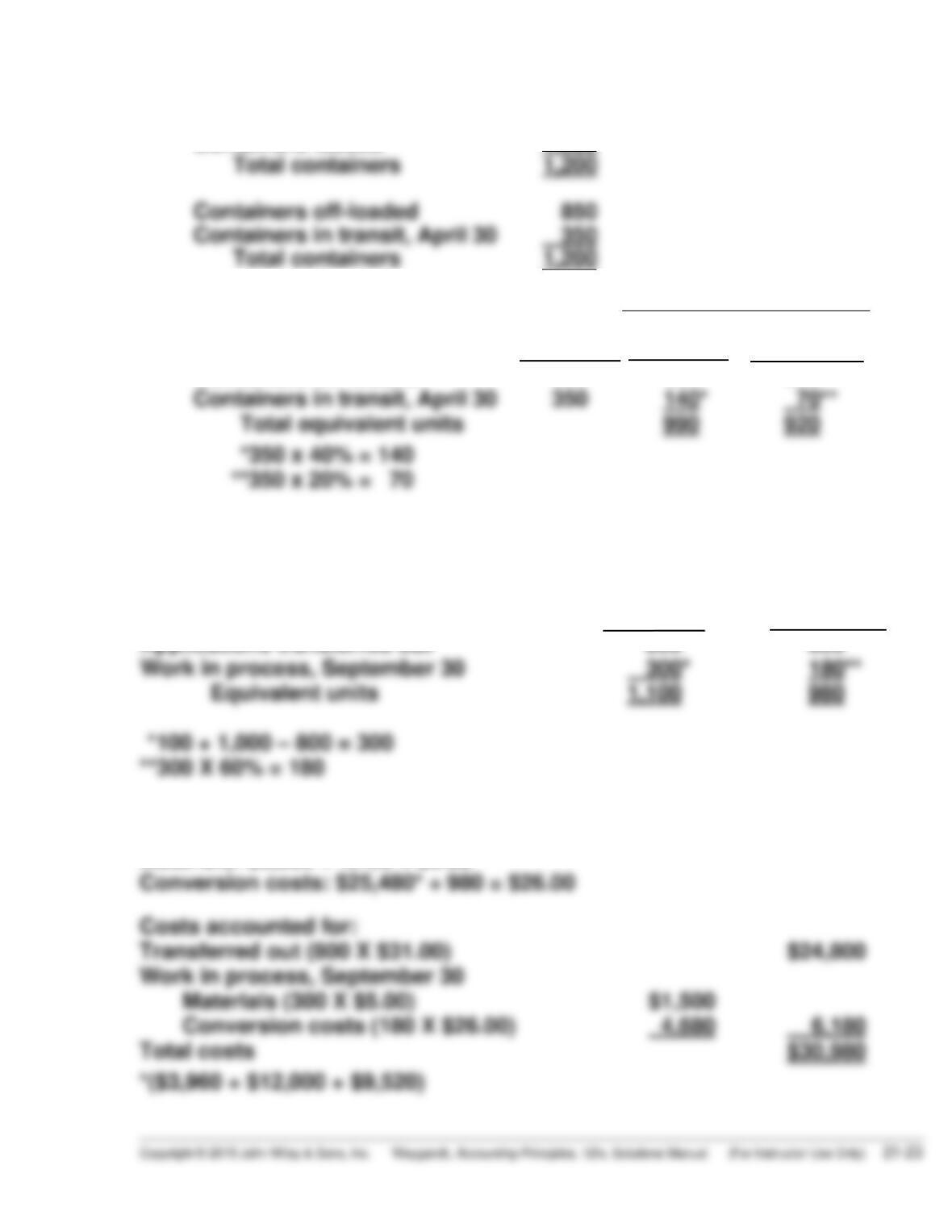

EXERCISE 21–14

(a)

Containers in transit, April 1

0

Containers loaded

1,200

Total containers

1,200

Containers off-loaded

850

Containers in transit, April 30

350

Total containers

1,200

Equivalent Units

(b)

Physical

Units

Direct

Materials

Conversion

Costs

Containers off-loaded

Containers in transit, April 30

Total equivalent units

*350 x 40% = 140

**350 x 20% = 70

EXERCISE 21–15

(a)

Materials

Conversion

Costs

Applications transferred out

800

800

Work in process, September 30

300*

180**

Equivalent units

1,100

980

(b)

Materials: $5,500 ÷ 1,100 = $5.00

Conversion costs: $25,480* ÷ 980 = $26.00

Costs accounted for:

Transferred out (800 X $31.00)

$24,800

Work in process, September 30

Materials (300 X $5.00)

Conversion costs (180 X $26.00)

Total costs

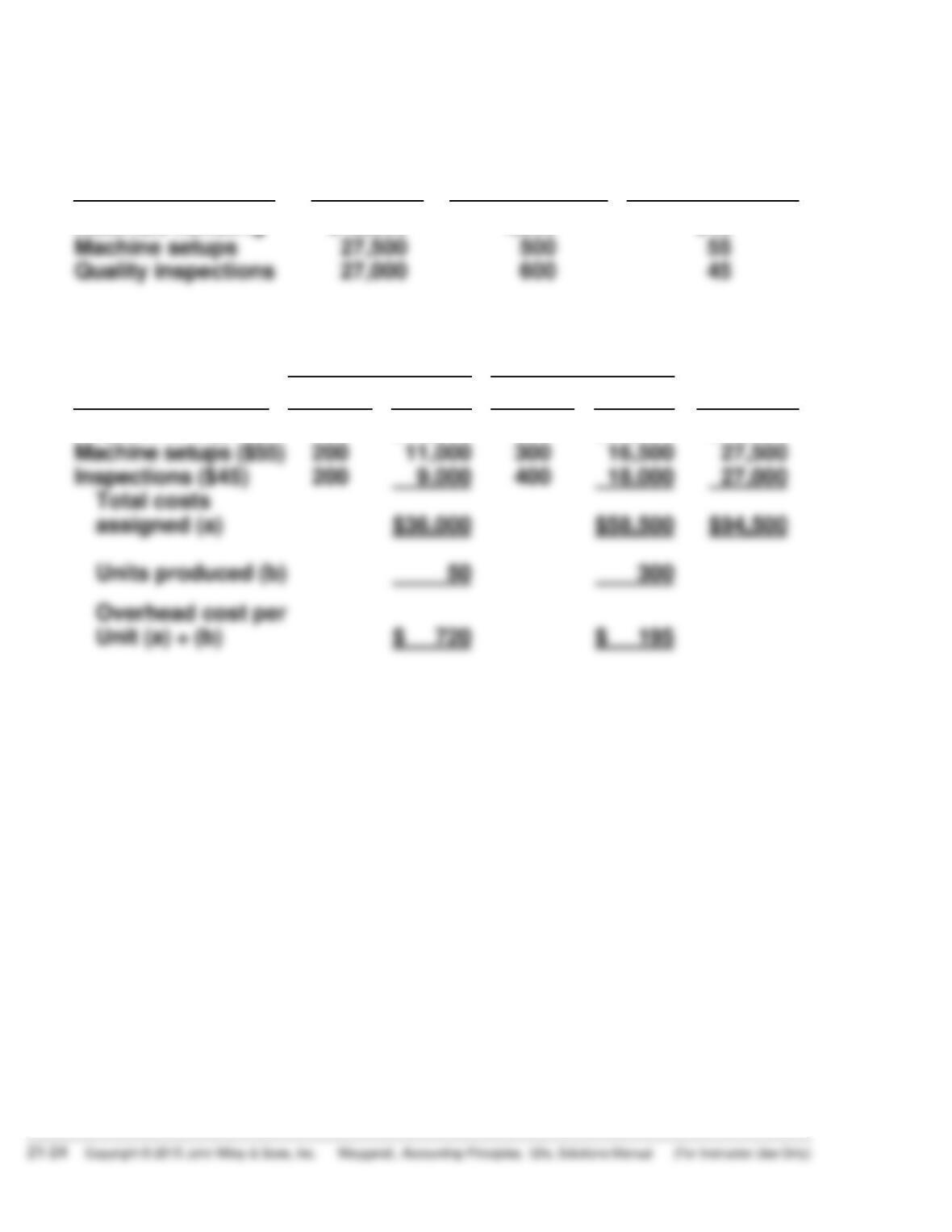

*EXERCISE 21-16

(a) The overhead rates are:

Activity Cost Pools

Estimated

Overhead

÷

Expected Use

of Cost Drivers

per Activity

=

Activity-Based

Overhead Rates

Machine setups

Materials handling

$40,000

1,000

$40

(b) The assignment of the overhead costs to products is as follows:

Instruments

Gauges

Cost

Assigned

Cost Driver

Number

Cost

Number

Cost

Requisitions ($40)

400

$16,000

600

$24,000

$40,000

*EXERCISE 21-16 (Continued)

(c) MEMO

To: President, Major Instrument, Inc.

From: Student

Re: Benefits of activity-based costing (ABC)

ABC focuses on the activities performed in producing a product.

Overhead costs are assigned to products based on cost drivers that

measure the activities performed on the product.

*EXERCISE 21-17

(a) Direct materials (1,000 X $35) …………………………. $35,000

Direct labor (1,000 X $15) ……………………………….. 15,000

SOLUTIONS TO PROBLEMS

PROBLEM 21–1A

1. Raw Materials Inventory ……………………………. 300,000

Accounts Payable ……………………………… 300,000

2. Work in Process—Mixing ………………………….. 210,000

Work in Process—Packaging ……………………. 45,000

Raw Materials Inventory …………………….. 255,000

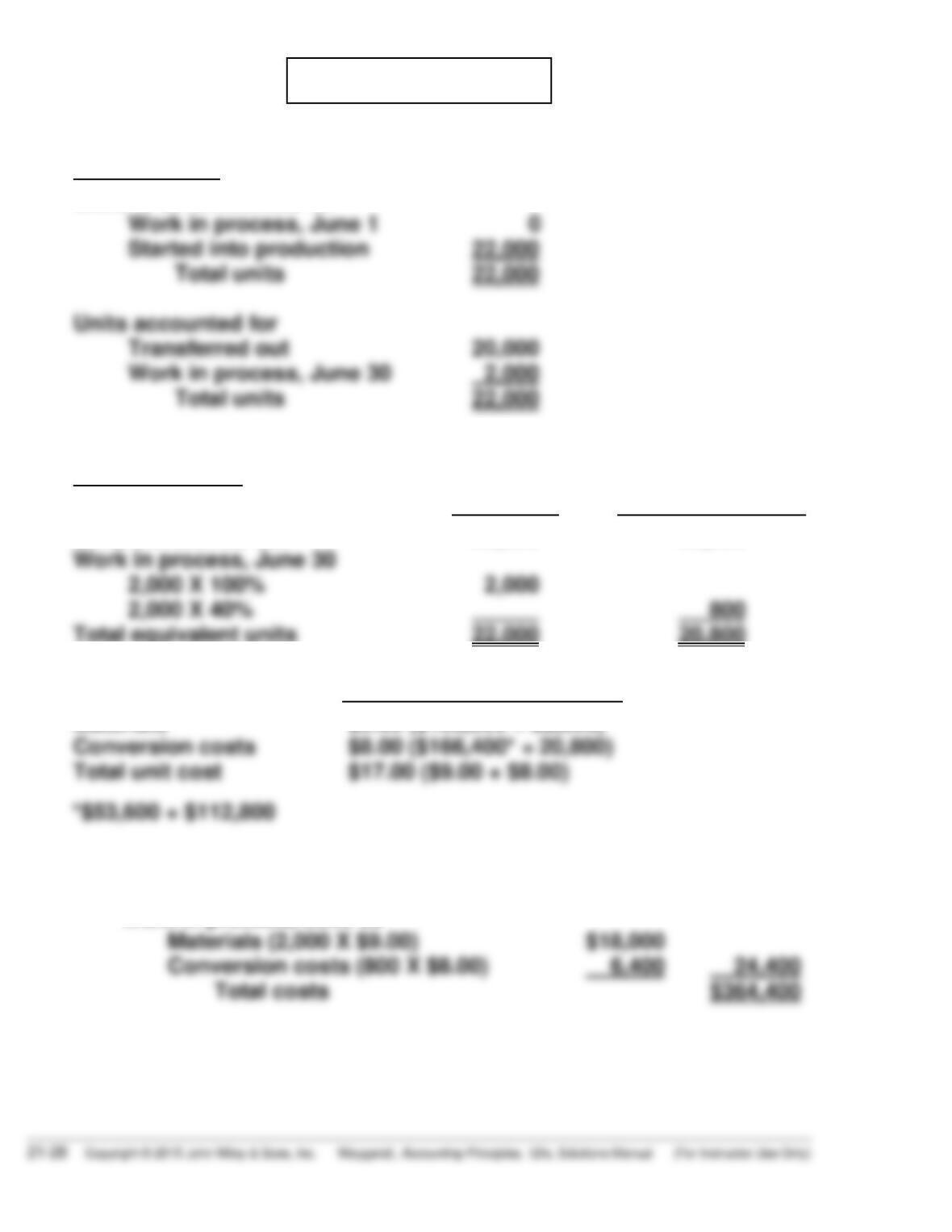

PROBLEM 21–2A

(a)

Physical units

Units to be accounted for

Work in process, June 1

Started into production

Total units

0

22,000

22,000

(b)

Equivalent units

Materials

Conversion Costs

Units transferred out

Total equivalent units

20,000

22,000

20,000

20,800

(c)

Unit Costs

Materials

$9.00 ($198,000 ÷ 22,000)

(d) Costs accounted for

Transferred out (20,000 X $17.00) $340,000

Work in process, June 30

PROBLEM 21-2A (Continued)

(e) ROSENTHAL COMPANY

Molding Department

Production Cost Report

For the Month Ended June 30, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Work in process, June 30

(2,000 X 40%)

Total units

Units to be accounted for

Work in process, June 1

Started into production

Total units

0

22,000

22,000

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Total cost

(a)

$198,000

$166,400

$364,400

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out (20,000 X $17.00)

Work in process, June 30

$340,000

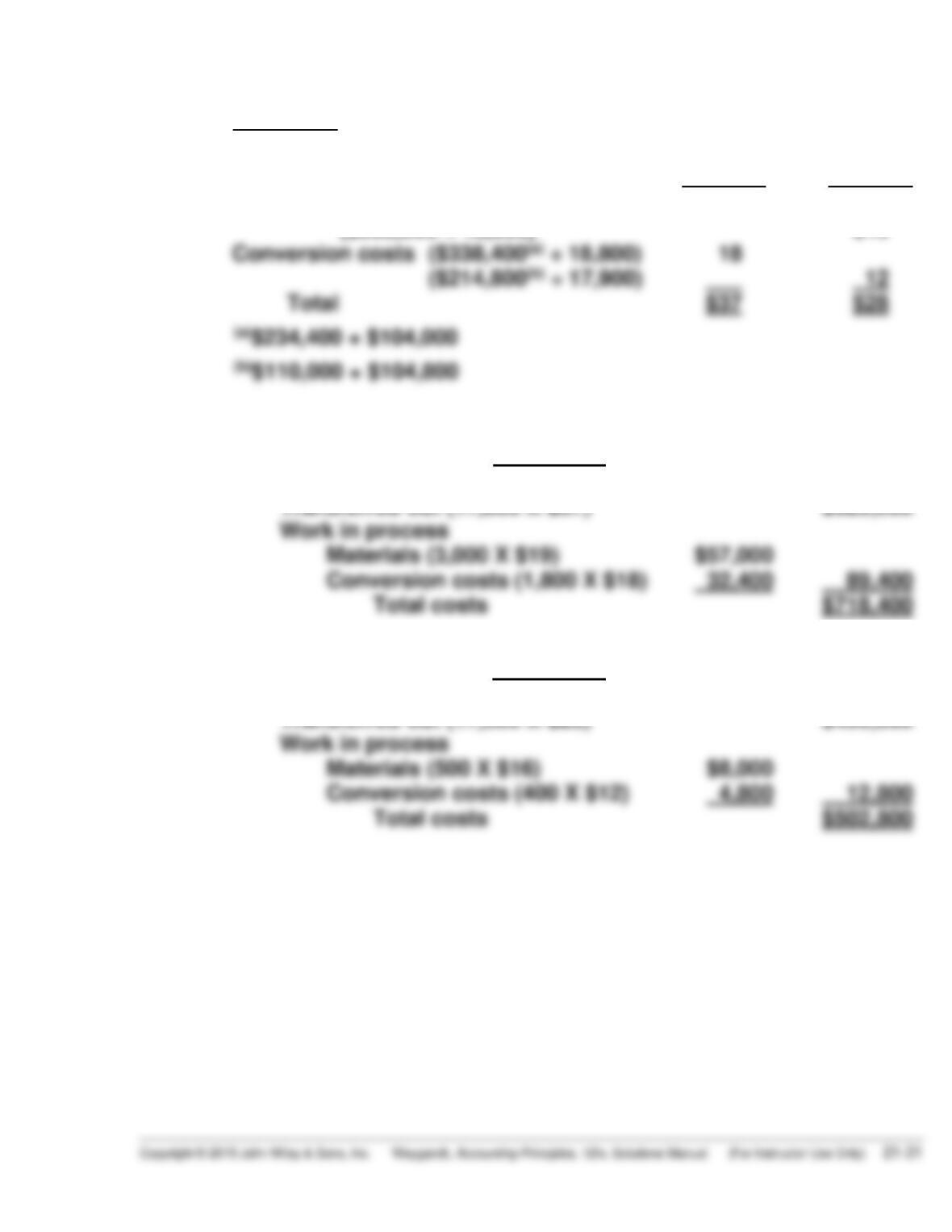

PROBLEM 21–3A

(a) (1) Physical units

T12

Tables

C10

Chairs

Units to be accounted for

Work in process, July 1

0

0

(2) Equivalent units

T12 Tables

Materials

Conversion

Costs

Units transferred out

Work in process, July 31

17,000

17,000

C10 Chairs

Materials

Conversion

Costs

Units transferred out

Work in process, July 31

17,500

17,500

PROBLEM 21-3A (Continued)

(3) Unit costs

T12

Tables

C10

Chairs

Materials ($380,000 ÷ 20,000)

($288,000 ÷ 18,000)

$19

$16

(4) T12 Tables

Costs accounted for

Transferred out (17,000 X $37) $629,000

Total costs $718,400

C10 Chairs

Costs accounted for

Transferred out (17,500 X $28) $490,000

PROBLEM 21-3A (Continued)

(b) THAKIN INDUSTRIES INC.

Cutting Department—Plant 1

Production Cost Report

For the Month Ended July 31, 2017

Equivalent Units

Quantities

Physical

Units

Materials

Conversion

Costs

(Step 1)

(Step 2)

Work in process, July 31

(3,000 X 60%)

Total units

Units to be accounted for

Work in process, July 1

0

Costs

Materials

Conversion

Costs

Total

Unit costs (Step 3)

Total cost

(a)

$380,000

$338,400

$718,400

Cost Reconciliation Schedule (Step 4)

Costs accounted for

Transferred out (17,000 X $37)

$629,000

PROBLEM 21–4A

(a)

Equivalent Units

Physical

Units

Materials

Conversion

Costs

695,000

Units to be accounted for

Work in process, November 1

Started into production

Total units

35,000

660,000

695,000

Beginning work in

process

Added during month

Materials cost

$ 79,000

1,589,000

Conversion costs

$ 48,150

563,850

($225,920 + $337,930)

(b)

Costs accounted for

Transferred out (670,000 X $3.30)

$2,211,000