Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

C

CH

HA

AP

PT

TE

ER

R

2

21

1

S

St

ta

at

te

em

me

en

nt

t

o

of

f

C

Ca

as

sh

h

F

Fl

lo

ow

ws

s

R

Re

ev

vi

is

si

it

te

ed

d

Overview

The objective of financial reporting is to provide investors and creditors with useful

information, primarily in the form of financial statements. The balance sheet and the income

statement – that have been the focus of your study in earlier chapters – do not provide all the

Learning Objectives

After studying this chapter, you should be able to:

LO20-1 Explain the usefulness of the statement of cash flows.

LO20-2 Define cash equivalents.

LO20-3 Determine cash flows from operating activities by the direct method.

LO20-4 Determine cash flows from operating activities by the indirect method.

L

Le

ec

ct

tu

ur

re

e

O

Ou

ut

tl

li

in

ne

e

I. Investors and creditors analyze the prospects of receiving a cash return from their dealings with

a firm.

A. Cash flows to investors and creditors depend on the corporation generating cash flows to

itself. (T21-1)

II. The statement of cash flows fills an information gap left by the balance sheet and the income

statement.

A. It presents information about cash flows that the other statements either (a) do not

provide or (b) provide only indirectly.

B. Cash continuously flows into and out of an active business.

21-2 Intermediate Accounting, 8/e

III. The requirement that companies present the statement of cash flows is relatively recent.

A. During the early 1900s and continuing into the mid-1930s, the cash basis was a widely

used means of financial reporting.

B. Early efforts to create the standard of accrual accounting intentionally suppressed the

IV. Cash includes “cash equivalents.” The statement of cash flows does not differentiate between

amounts held as cash and amounts held in cash equivalent investments. (T21-3)

A. These are short-term, highly liquid investments that can readily be converted to cash with

little risk of loss.

B. Examples are money market funds, treasury bills, and commercial paper.

V. Cash flows from operating activities are both inflows and outflows of cash that result from

activities reported on the income statement. (T21-4)

A. The classification includes the elements of net income, but reported on a cash basis, such

as: (T21-5)

1. Cash received from customers rather than sales and service revenue.

B. Noncash items reported on the income statement on not reported on the statement of cash

flows, such as:

1. Gain on sale of assets.

VI. Cash flows from investing activities are related to the acquisition and disposition of assets,

other than (a) inventory and (b) assets classified as cash equivalents. (T21-6)

A. The classification includes the acquisition of:

1. Property, plant and equipment and other productive assets [except inventories].

VII. Cash flows from financing activities result from the external financing of a business. (T21-7)

A. The classification includes:

1. The sale or repurchase of shares.

B. The classification also includes subsequent transactions related to these, such as:

1. The repurchase of common or preferred stock (to retire the stock or as treasury

VIII. Noncash investing and financing activities, such as acquiring equipment (an investing activity)

by issuing a long-term note payable (a financing activity) must be disclosed also.

A. Examples of transactions that do not increase or decrease cash, but which result in

significant investing and financing activities are:

1. Acquiring an asset by incurring a debt payable to the seller.

B. Noncash transactions that do not affect a company's assets or liabilities, such as the

distribution of stock dividends, are not considered investing or financing activities and

are not reported.

C. Noncash investing and financing activities are reported either on the same page as the

statement of cash flows or in a related schedule or note.

D. Both U.S. GAAP and IFRS require a statement of cash flows that classifies cash flows

21-4 Intermediate Accounting, 8/e

IX. A spreadsheet offers a systematic method of preparing a statement of cash flows.

A. It allows us to analyze available data to ensure that all operating, investing, and

financing activities are detected.

B. We use it to record spreadsheet entries that explain account balance changes and

D. Procedure:

1. Enter the beginning and ending balances of each account by transferring the

comparative balance sheets and income statement to a blank spreadsheet. (T21-10)

2. Following the balance sheets and income statement, we allocate space on the

spreadsheet for the statement of cash flows. (T21-11)

3. Enter spreadsheet entries that duplicate the actual journal entries used to record the

transactions as they occurred during the year. Example: sales revenue (T21-12)

[Also, T21-13 through T21-30 can be used to explain some or all of the other

entries to the spreadsheet.]

4. When a transaction being entered on the spreadsheet includes an operating,

investing, or financing activity, enter that portion of the entry under the

X. Either the direct or the indirect method can be used to calculate and present the net cash

increase or decrease from operating activities.

A. Unlike the direct method, which directly lists cash inflows and outflows, the indirect

Decision-Makers’ Perspective

A. Some analysts supplement their analysis with cash flow ratios. (T21-35)

1. Some cash flow ratios are derived by simply substituting “Cash flow from

21-6 Intermediate Accounting, 8/e

P

Po

ow

we

er

rP

Po

oi

in

nt

t

S

Sl

li

id

de

es

s

A PowerPoint presentation of the chapter is available at the textbook website.

T

Te

ea

ac

ch

hi

in

ng

g

T

Tr

ra

an

ns

sp

pa

ar

re

en

nc

cy

y

M

Ma

as

st

te

er

rs

s

The following can be reproduced on transparency film as they appear here, or

CASH INFLOWS

Operating Activities Investing Activities Financing Activities

Cash received Sale of operational assets Issuance of stock

⧫________________⧫________________ ⧫

Business

⧫________________⧫________________ ⧫

T21-1

21-8 Intermediate Accounting, 8/e

United Brands Corporation

Statement of Cash Flows

For Year Ended December 31, 2016 ($ in millions)

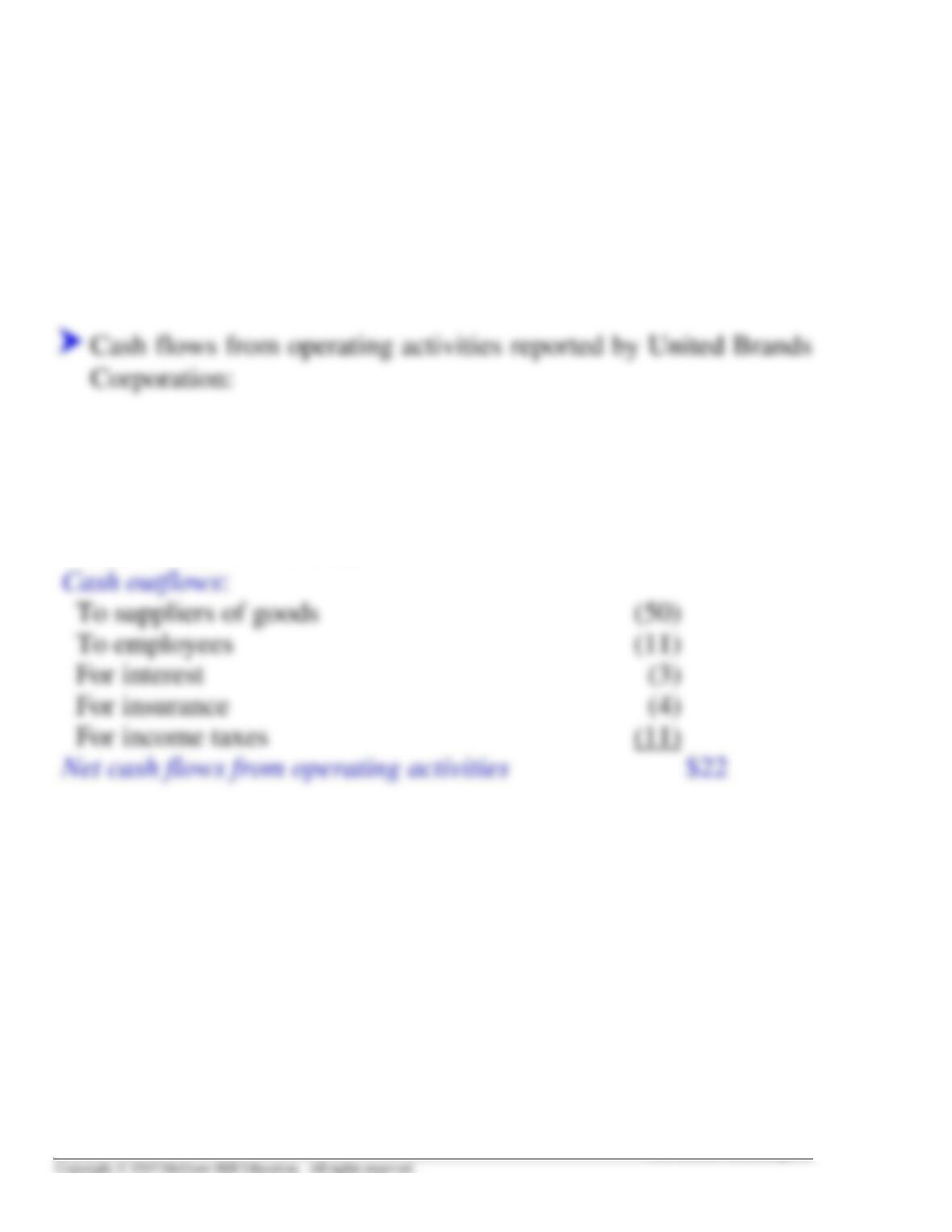

Cash flows from operating activities:

Cash inflows:

From customers $98

From investment revenue 3

Cash outflows:

To suppliers of goods (50)

Net cash flows from operating activities $22

Cash flows from investing activities:

Purchase of land ($30)

Net cash flows from financing activities 6

Net increase in cash $9

Cash balance, January 1 20

T21-2

Note X:

Noncash investing and financing activities:

Acquired $20 million of equipment

by issuing a 12%, 5-year note. $20

Reconciliation of Net Income to Cash Flows from Operating

Activities:

Net income $12

Adjustments for noncash effects:

Gain on sale of land (8)

Depreciation expense 3

T21-2 (continued)

21-10 Intermediate Accounting, 8/e

CASH EQUIVALENTS

The statement of cash flows does not differentiate between

amounts held as cash and amounts held in cash equivalent

investments.

Short-term, highly liquid investments that can readily

be converted to cash with little risk of loss.

Examples of cash equivalents:

of cash flows.

CASH FLOWS FROM OPERATING ACTIVITIES

Cash flows from operating activities are both inflows and

outflows of cash that result from activities reported on the

income statement.

Income Statement Cash Flows from Operating

Activities

Revenues: Cash inflows:

Sales and service revenue Cash received from customers

Less: Expenses: Less: Cash outflows:

Cost of goods sold Cash paid to suppliers of inventory

Salaries expense Cash paid to employees

T21-4

21-12 Intermediate Accounting, 8/e

CASH FLOWS FROM OPERATING ACTIVITIES

Direct Method

Cash flows from operating activities are the elements of net

income, but reported on a cash basis.

Cash flows from operating activities:

Cash inflows:

From customers $98

From investment revenue 3

T21-5

CASH FLOWS FROM OPERATING ACTIVITIES

Indirect Method

By the indirect method, the net cash increase or decrease from

operating activities ($22 million in our example) would be derived

indirectly by starting with reported net income and working

backwards to convert that amount to a cash basis.

Net income $12

Adjustments for noncash effects:

Gain on sale of land (8)

Depreciation expense 3

T21-5 (continued)

21-14 Intermediate Accounting, 8/e

CASH FLOWS FROM INVESTING ACTIVITIES

Cash flows from investing activities are related to the

acquisition and disposition of assets, other than (a) inventory

and (b) assets classified as cash equivalents.

Included in this classification are cash payments to acquire:

Property, plant and equipment and other productive assets

Cash flows from investing activities reported by United

Brands Corporation:

Cash Flows from Investing Activities:

Purchase of land $(30)

T21-6

CASH FLOWS FROM FINANCING ACTIVITIES

Cash flows from financing activities are both inflows and

outflows of cash resulting from the external financing of a

business.

Included in this classification are cash inflows from:

The sale of common and preferred stock

The issuance of bonds and other debt securities

Cash flows from financing activities reported by United

Brands Corporation:

Cash Flows from Financing Activities:

Sale of common stock $26

T21-7

21-16 Intermediate Accounting, 8/e

NONCASH INVESTING AND FINANCING ACTIVITIES

A statement of cash flows should report transactions that do not

increase or decrease cash, but still represent significant

investing and financing activities.

Examples are:

Acquiring an asset by incurring a debt payable to the

seller.

Transactions that do not affect a company's assets or liabilities,

such as the distribution of stock dividends, are not considered

investing or financing activities.

UBC acquired $20 million of new equipment by issuing a $20

million long-term note payable in a single transaction. UBC

reported this transaction in the following manner:

T21-8

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Classification of Cash Flows. Both U.S. GAAP and IFRS require

a statement of cash flows that classifies cash flows into operating,

investing, or financing activities. A difference, though, is that U.S.

T21-9

21-18 Intermediate Accounting, 8/e

United Brands Corporation

Comparative Balance Sheets

December 31, 2016 and 2015 ($ in millions)

Assets: 2016 2015

Cash $29 $20

Accounts receivable 32 30

$267 $221

Liabilities:

Accounts payable $ 26 $ 20

Salaries payable 3 1

Shareholders' Equity:

Common stock $130 $100

United Brands Corporation

Income Statement

For the Year Ended December 31, 2016 ($ in millions)

Revenues:

Sales revenue $100

Expenses:

Cost of goods sold $60

Net income $12

Additional information from the accounting records:

a. A portion of company land, purchased in a previous year for $10 million, was sold

for $18 million.

b. Equipment that originally cost $14 million, and which was one-half depreciated,

was sold for $5 million cash.

T21-10 (continued)

United Brands Corporation

Spreadsheet for the Statement of Cash Flows

Dec. 31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 20 29

Accounts receivable 30 32

Liabilities:

Accounts payable 20 26

Salaries payable 1 3

Shareholders' Equity:

Common stock 100

130

T21-11

(continued)