1. Total variable costs change in proportion to changes in the level of activity. Unit variable

2. a. Variable costs

b. Variable costs

3. Total fixed cost remains the same regardless of changes in the level of activity. Fixed cost per unit

4. Mixed costs are costs that have characteristics of both a variable and a fixed cost. The high-low

method uses the highest and lowest activity levels and their related costs to estimate the variable

5. a. No impact on the contribution margin.

6. A high contribution margin ratio, coupled with idle capacity, indicates a potential for increased

income from operations if additional sales can be made. A large percentage of each additional

8. Austin Company had lower fixed costs and a higher percentage of variable costs to sales than

9. The individual products are treated as components of one overall enterprise product. These

10. Operating leverage measures the relationship between a company’s contribution margin

and income from operations. The difference between contribution margin and income fro

m

operations is fixed costs. Thus, companies with high fixed costs will normally have a high

CHAPTER 21

COST BEHAVIOR AND COST-VOLUME-PROFIT ANALYSIS

DISCUSSION QUESTIONS

21-1

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

PE 21–1A

a. $20 per unit = ($900,000 – $350,000) ÷ (40,000 units – 12,500 units)

PE 21–1B

a. $50 per unit = ($440,000 – $300,000) ÷ (5,500 units – 2,700 units)

PE 21–2A

a. 25.0% = ($100 – $75) ÷ $100, or ($1,000,000 – $750,000) ÷ $1,000,000

PE 21–2B

a. 20% = ($30 – $24) ÷ $30, or ($660,000 – $528,000) ÷ $660,000

PRACTICE EXERCISES

21-2

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

PE 21–3A

a. 1,625 units = $65,000 ÷ ($115 – $75)

PE 21–3B

a. 1,600 units = $48,000 ÷ ($75 – $45)

PE 21–4A

a. 1,800 units = $45,000 ÷ ($100 – $75)

PE 21–4B

a. 5,000 units = $200,000 ÷ ($150 – $110)

PE 21–5A

Unit selling price of E: [($145 × 0.60) + ($110 × 0.40)] = $131.00

PE 21–5B

Unit selling price of E: [($50 × 0.40) + ($60 × 0.60)] = $56.00

21-3

PE 21–6A

PE 21–6B

PE 21–7A

PE 21–7B

21-4

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–1

1. Variable 9. Mixed

3. Fixed 11. Fixed

5. Variable 13. Variable

Ex. 21–2

a. Cost Graph Three d. Cost Graph Two

Ex. 21–3

1. e 4. f

Ex. 21–4

1. e

EXERCISES

21-5

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–5

a. Variable g. Fixed*

b. Variable h. Fixed

Ex. 21–6

Components produced…………

…

200,000 400,000 600,000

Total costs:

Total variable costs…………

…

$250,000 (d) $ 500,000 (j) $ 750,000

Supporting calculations:

a. $1.25 ($250,000 ÷ 200,000 units)

h. $1.50 ($600,000 ÷ 400,000 units)

i.

j. $750,000 ($1.25 × 600,000 units)

k. $600,000 (fixed costs do not change with volume)

o.

$2.75 ($1.25 + $1.50 units)

21-6

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–7

The fixed cost can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of production, as

follows:

Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Highest level:

b. Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Total cost for 12,000 units:

Variable cost:

Units……………………………………………

…

17,000

…

=Variable Cost per Unita.

Difference in Total Costs

Difference in Units Produced

21-7

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–8

The fixed costs can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of gross-ton mile,

as follows:

Total Cost = (Variable Cost per Gross-Ton Mile × Gross-Ton Miles) + Fixed Costs

Highest level:

Lowest level:

$1,440,000 = ($2.10 × 400,000 gross-ton miles) + Fixed Costs

Ex. 21–9

a. Sales………………………

…

$3,200,000

…

b. Sales…………………………………………………

…

Contribution margin ratio………………………………

…

…

Difference in Gross-Ton Miles

Difference in Total Costs

$2,700,000 – $1,440,000

=

Variable Cost per

Gross-Ton Mile

$2,100,000

35%

×

21-8

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–10

a. Sales (in millions)…………………………………………………………………

…

$18,602.5

Variable costs (in millions):

c. Same-store sales increase (in millions)……………………………………

Contribution margin ratio [from part (b)]…………………………………

…

Ex. 21–11

Sales – Variable Costs

Sales

b. =Contribution Margin Ratio

$900.0

35.5%

a. Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

×

21-9

…

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–12

Total Cost Variable Cost Variable Cost

(in millions) Percentage (in millions)

Cost of goods sold………………………

…

$16,447.0 × 70% = $11,512.9

Selling, general and administrative…

…

10,578.0 × 40% = 4,231.2

.

.

$11,280,900,000

$124.24 – $35.98 – $13.22

Break-Even Sales (units) =

a

.

Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

$11,280,900,000 + $400,000,000

$124.24 – $35.98 – $13.22

b

.

=

1

342

21-10

…

…

…

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–14

Ex. 21–15

The cost of the promotional campaign is the fixed cost in this analysis because

we’re trying to determine the break-even adoption rate of the campaign.

The contribution margin earned per new subscriber is essentially the revenue

earned less the variable cost over the 14-month subscription period.

Unit Contribution Margin

=Break-Even Sales (units)

Fixed Costs

21-11

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–16

1

Revenue per account (in millions):

$35,345 million ÷ 32.5 million = $1,087.5 (rounded)

2

Variable cost per account (in millions, except variable cost per account):

Cost of revenue………………………………………………

…

$20,841 × 70% = $14,588.7

3

Fixed costs (in millions):

Cost of revenue………………………………………………

…

$20,841 × 30% = $ 6,252.3

Note to Instructors: The rate charged per minute and the number of average

minutes of digital service influence the revenue per account. An interesting

=

$15,326.8 million

X – $539.0

Revenue per Account – Variable Cost per Account

Fixed Cost

Revenue per Account – Variable Cost per Account

=32.5 million accounts

b. Break-Even =

Fixed Costs

a.

Break-Even

21-12

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–17

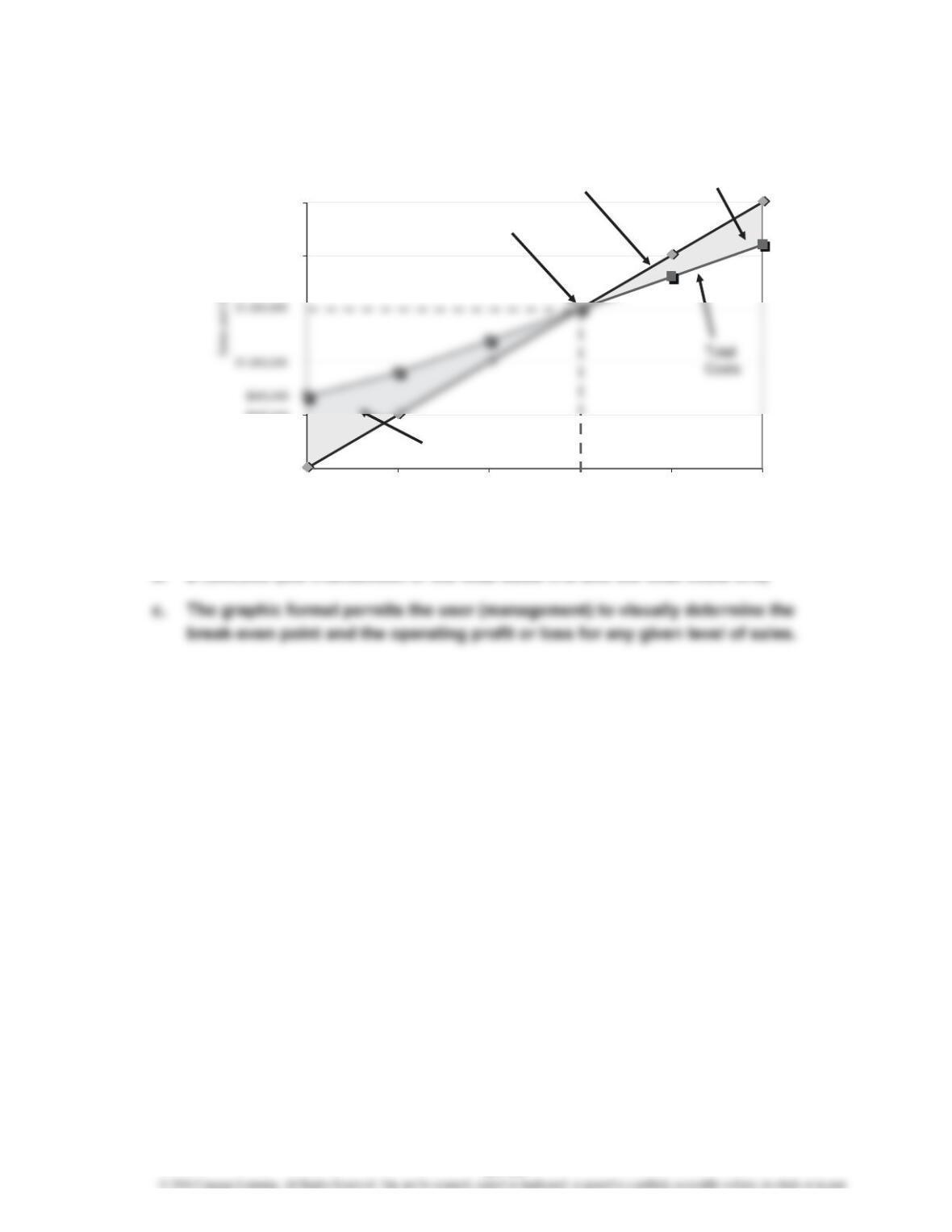

a.

b. $1,500,000 (the intersection of the total sales line and the total costs line)

$0

$500,000

$2,000,000

$2,500,000

0 4,000 8,000 12,000 16,000 20,000

Units of Sales

Break-

Even Point

Operating

Profit Area Total Sales Line

Operating

Loss Area

21-13

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–18

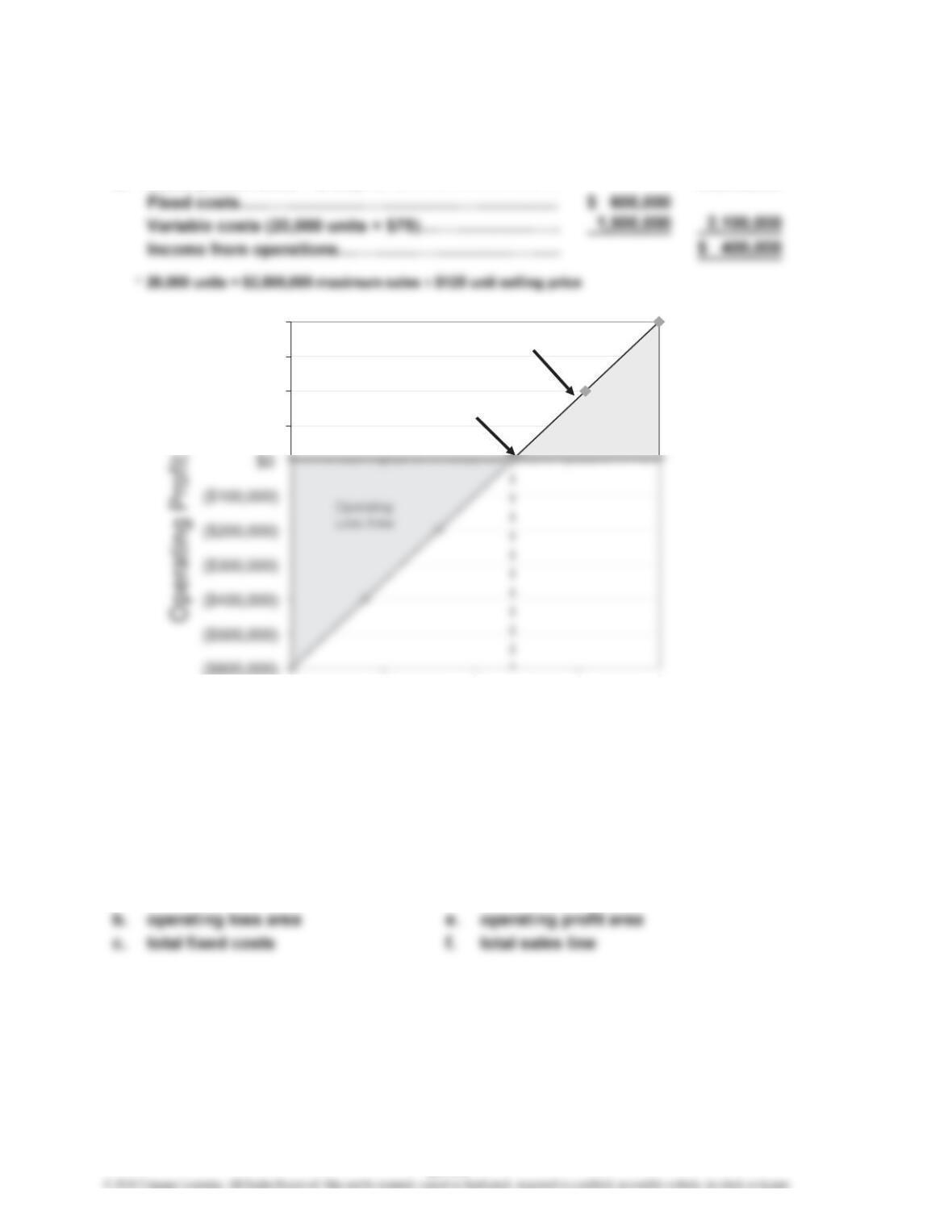

a. $600,000 (total fixed costs)

b. Sales (20,000 units × $125)……………………………… $2,500,000

c.

d. 12,000 units (the intersection of the profit line and the horizontal axis)

Ex. 21–19

Cost-volume-profit chart

a. break-even point d. total costs line

*

$100,000

$200,000

$300,000

$400,000

0 5,000 10,000 15,000 20,000

Units of Sales

Break-Even

Point

Operating

Profit Area

Profit Line

12,000

21-14

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–20

Profit-volume chart

a. break-even point

Ex. 21–21

a. Unit Selling Price of E = ($90 × 40%) + ($105 × 60%)

= $36 + $63 = $99

$40

b. 6,200 units of baseball bats (15,500 units × 40%)

21-15

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–22

a. Unit contribution margin of overall product (E):

Unit selling price of E [(10% × $800) + (90% × $300)]…………………………

…

$350

b. Business class break-even (60 seats × 10%)……………………………

…

6seats

Ex. 21–23

a. (1) Margin of Safety (dollars) = Sales – Sales at Break-Even Point

= $1,200,000 – $960,000 = $240,000

b. The break-even point (S) is determined as follows:

Break-Even Sales (dollars) = Total Fixed Costs + Total Variable Costs (at Break-Even)

Break-Even Sales (dollars) = Total Fixed Costs + 80% Break-Even Sales (dollars)

Break-Even Sales (dollars) = $1,875,000 + 80% Break-Even Sales (dollars)

21-16

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–24

If 420,000 units are sold and sales at the break-even point are 472,500 units,

Ex. 21–25

a. Beck Inc.:

Bryant Inc.:

b. Beck Inc.’s income from operations would increase by 100% (5.0 × 20%),

c. The difference in the increases of income from operations is due to the

Ex. 21–26

a. Variable cost of goods sold

Contribution Margin

Income from Operations

=

Contribution Margin

Income from Operations

Operating Leverage

Operating Leverage =

21-17

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–27

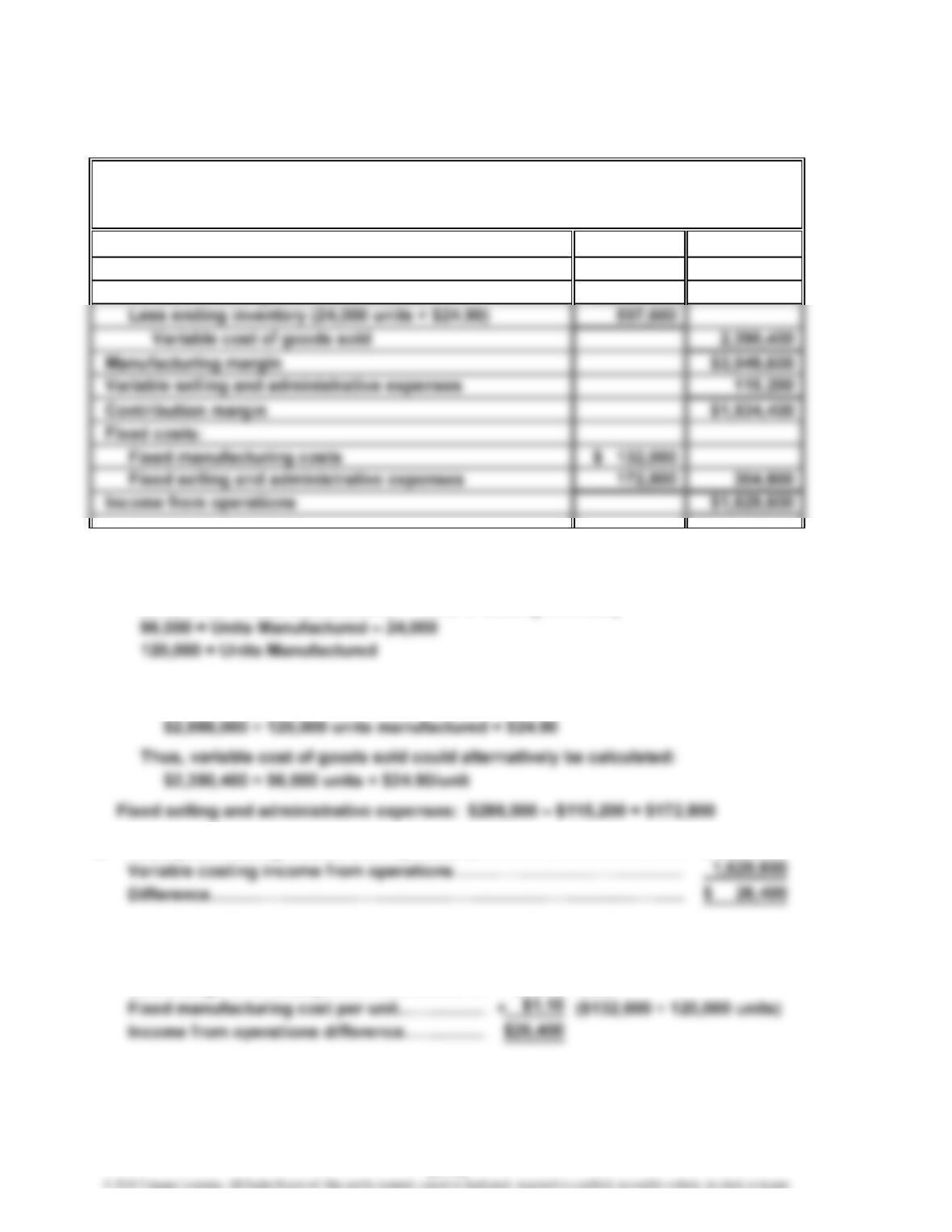

a.

Sales $4,440,000

Variable cost of goods sold:

Variable cost of goods manufactured $2,988,000

Computations:

Variable cost of goods manufactured: $3,120,000 – $132,000 = $2,988,000

Units Sold = Units Manufactured – Units in Ending Inventory

Unit cost of ending inventory:

Variable cost of goods manufactured per unit:

b. Absorption costing income from operations………………………………

…

$1,656,000

Note: The difference between the two income numbers can be reconciled

as follows:

Unit change in inventory………………………

…

24,000 units

RHYS COMPANY

Income Statement—Variable Costing

For the Month Ended July 31, 2016

21-18

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

Ex. 21–28

a.

Sales $7,450,000

Cost of goods sold:

Computations:

Cost of goods manufactured: $7,000,000 + $160,000 = $7,160,000

Unit cost of ending inventory:

Total cost of goods manufactured:

b. Note: The difference between the two income numbers can be reconciled

as follows:

Unit change in inventory………………………

…

80,000 units

TUDOR MANUFACTURING CO.

Income Statement—Absorption Costing

For the Month Ended June 30, 2016

21-19

CHAPTER 21 Cost Behavior and Cost-Volume-Profit Analysis

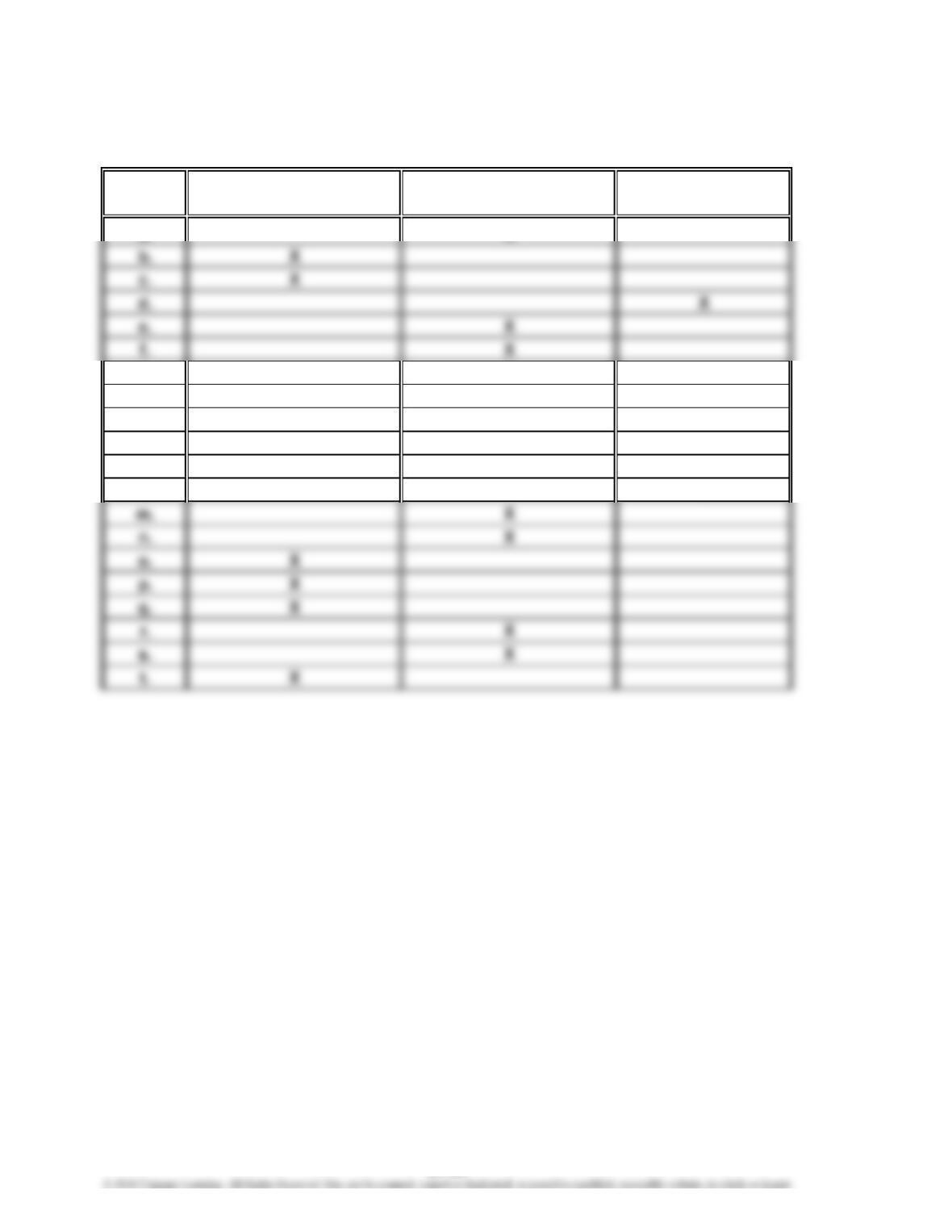

Prob. 21–1A

Fixed Variable Mixed

Cost Cost Cost Cost

a. X

g. X

h. X

i. X

j. X

k. X

l. X

PROBLEMS

21-20