Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 21

Chapter 21

Cost-Volume-Profit Analysis

QUESTIONS

1. A variable cost is one that varies proportionately with the volume of activity. For

2. Variable costs per unit stay the same (remain constant) when output volume

3. Fixed costs per unit decrease when output volume increases. This is because the

4. Cost-volume-profit analysis is especially useful in the planning phase for a

5. A step-wise cost remains constant over a limited range of output activity, outside of

6. Contribution margin ratio means that for each sales dollar a specified percent is

7. Definition: Contribution margin ratio = Contribution margin / Sales price per unit.

8. Definition: Unit contribution margin = Sales price per unit – Variable costs per unit.

9. A CVP analysis for a manufacturing company is simplified by assuming that the

10. The first is that although individual costs classified as fixed or variable might not

behave precisely in those patterns, some variations of individual components in the

11. By assuming a relevant range for operating activity, management can more

justifiably assume either fixed or variable relations between costs and volume, and

12. Three common methods for measuring cost behavior are: the scatter diagram, the

high-low method, and least-squares regression.

13. A scatter diagram is used to display the relation between past costs and sales

15. This line represents total cost, which equals the sum of the fixed and variable costs

17. Company A has a contribution margin of 50% [($20,000 – $10,000) / ($20,000)] and

Company B has a contribution margin of 80% [($20,000 – $4,000) / ($20,000)]. This

19. Apple’s primary variable costs in making tablet computers are: labor, energy,

manufacturing and inventory-related costs. The costs of operating the plant and

20. Apple designs, manufactures, and markets mobile communication and media

devices, personal computers, and portable digital music players, and sells a variety

21. A 65% increase in sales of a popular smartphone model of Samsung is likely viewed

as a substantial increase. When this occurs, the sales and cost structures are likely

to change. Specifically, the selling price per unit, fixed costs, and variable costs are

1149

22. If units produced equals units sold, no conversion is necessary. If production

exceeds sales, absorption costing income can be determined by adding [increase in

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 21

1150

QUICK STUDIES

Quick Study 21-1 (10 minutes)

Quick Study 21-2 (10 minutes)

Quick Study 21-3 (10 minutes)

Quick Study 21-4 (15 minutes)

1. Estimated line of cost behavior

1151

Quick Study 21-4 (Concluded)

2. Estimated cost components

Fixed costs = $3,000

Quick Study 21-5 (10 minutes)

Quick Study 21-6 (10 minutes)

Quick Study 21-7 (10 minutes)

Quick Study 21-8 (10 minutes)

1152

Quick Study 21-9 (5 minutes)

Quick Study 21-10 (5 minutes)

Quick Study 21-11 (10 minutes)

Quick Study 21-12 (10 minutes)

ZHAO CO.

Contribution Margin Income Statement (at Expected Sales Level)

For Year Ended December 31, 2017

Sales (10,000 x $175) ………………………………………………………………..

$1,750,000

Quick Study 21-13 (5 minutes)

Quick Study 21-14 (10 minutes)

Quick Study 21-15 (10 minutes)

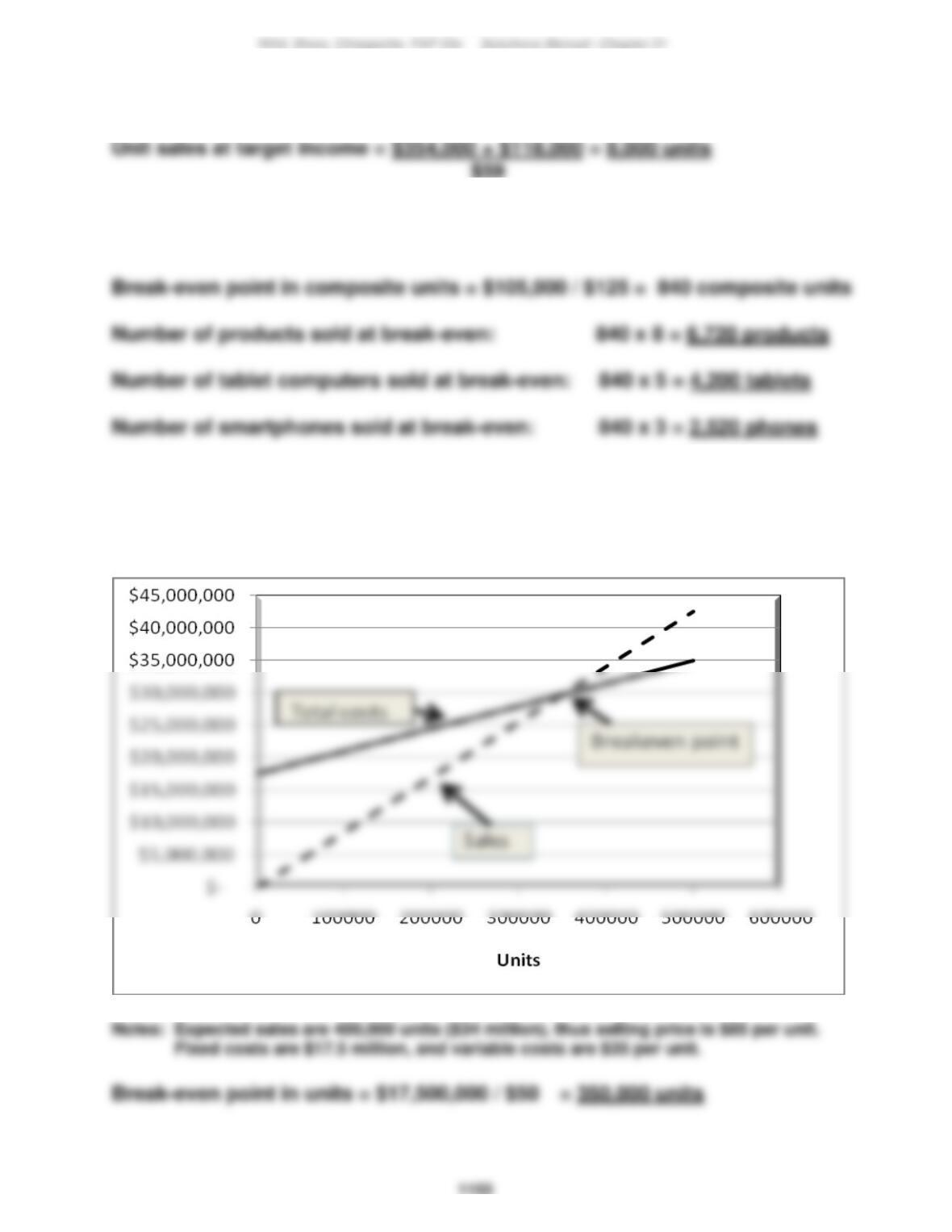

CVP Chart

1154

Quick Study 21-16 (10 minutes)

1.

Contribution margin ………………………………………………………………..

$960,000

2. If sales increase by 15%, income will increase by 4.0 x 15% = 60%, or,

Quick Study 21–17 (10 minutes)

Cost per unit using absorption costing

Per unit

Variable overhead………………………………………

Fixed overhead ($160,000/20,000 units)…………….

Total product cost per unit………………………..…..

Quick Study 21–18 (10 minutes)

Cost per unit using variable costing

Per unit

Direct labor………………………………………………

Variable overhead………………………………………

1155

Quick Study 21–19 (15 minutes)

ACES INC.

Variable Costing Income Statement

Sales (4,900 units x $90 per unit)………………..

$441,000

Variable expenses

Quick Study 21–20 (10 minutes)

ACES INC.

Absorption Costing Income Statement

Sales (4,900 units x $90 per unit)………………………

$441,000

1156

Quick Study 21-21 (10 minutes)

BMW Automotive Group

Contribution Margin Statement (in € millions)

Sales ……………………………………………………………………………………

€92,175.00

Variable costs:

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 21

EXERCISES

Exercise 21-1 (15 minutes)

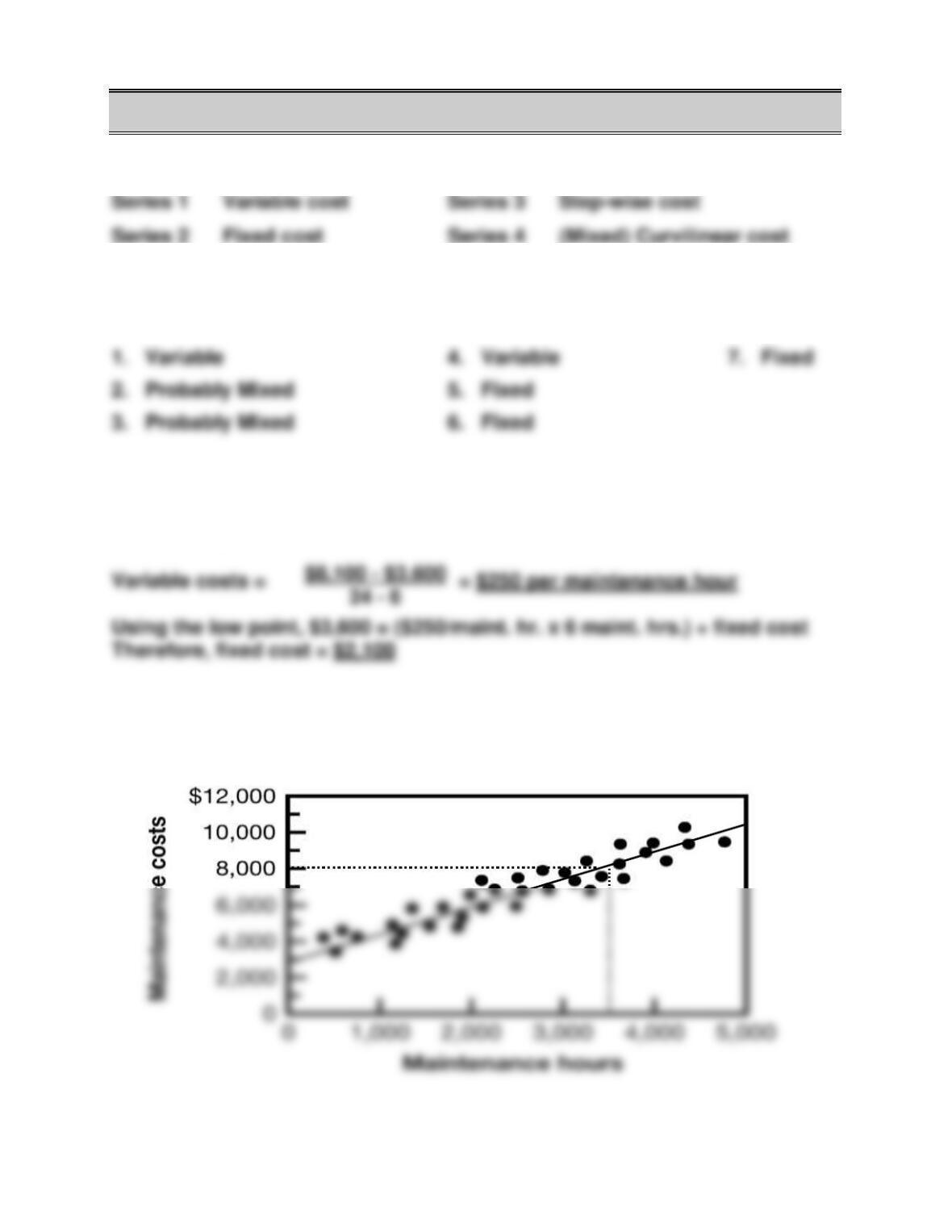

1. Graph #1 Variable cost

2. a. Graph #5

Exercise 21-2 (10 minutes)

1. A

Exercise 21-3 (15 minutes)

Series A Variable cost

1158

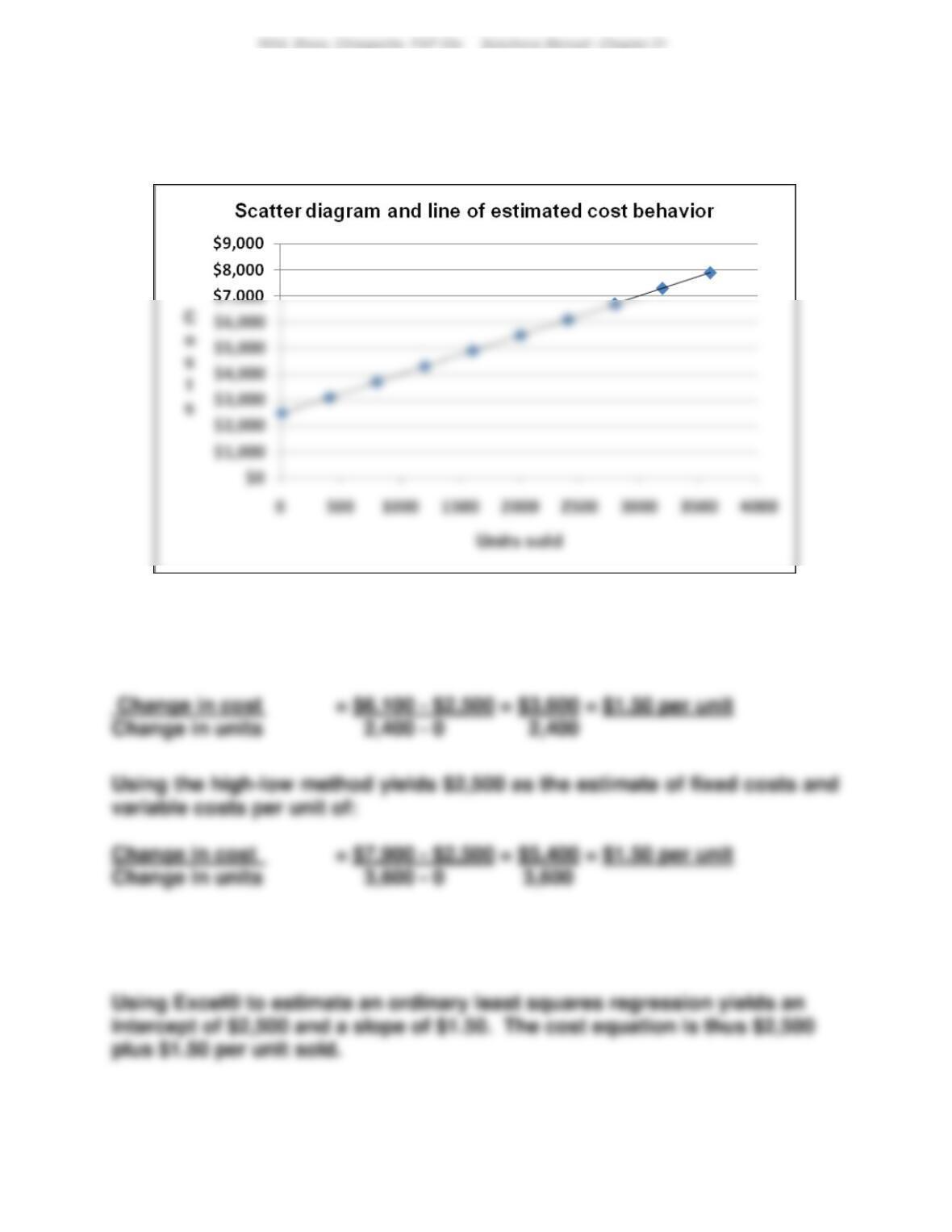

Exercise 21-4 (20 minutes)

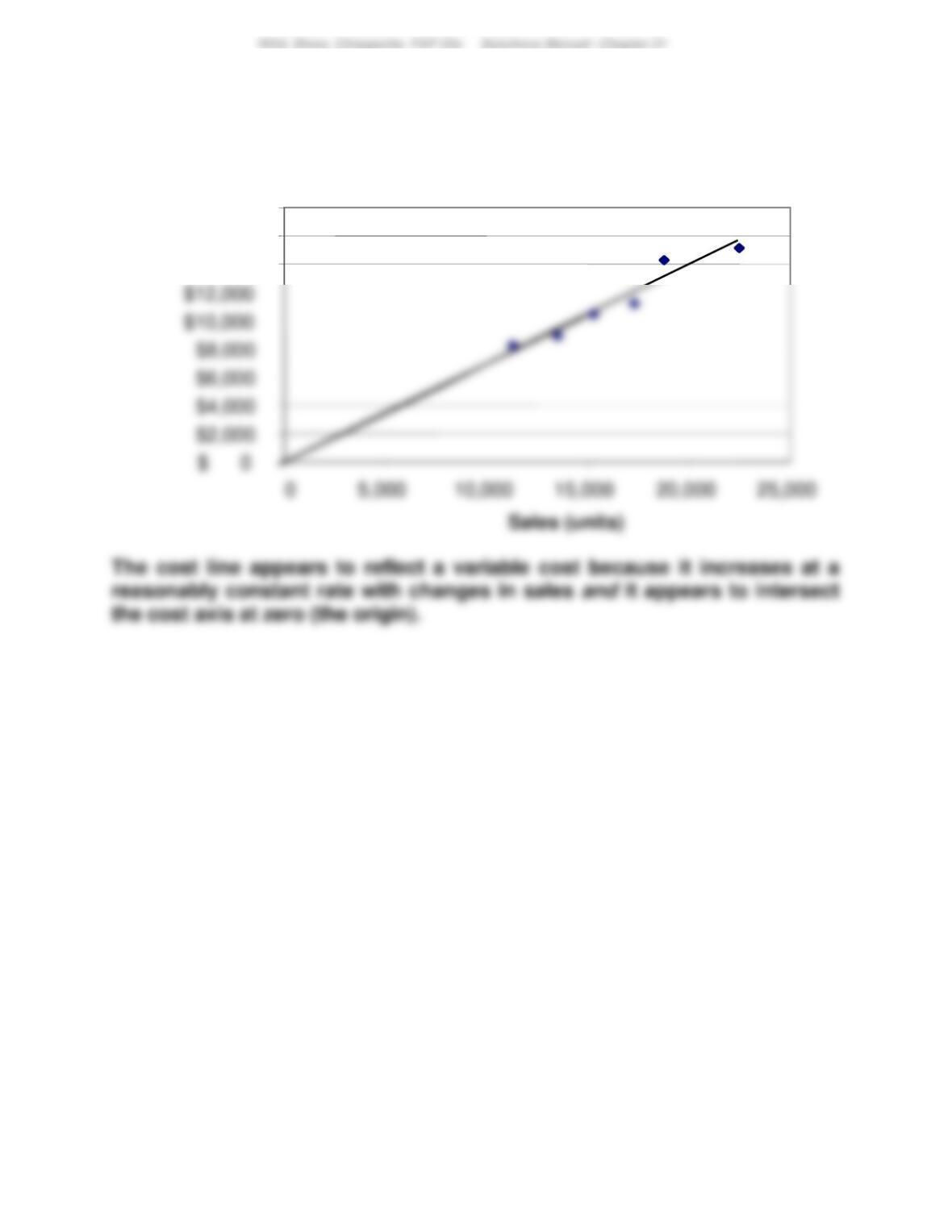

The scatter diagram and its estimated line of cost behavior appear below.

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

Cost of sales

1159

Exercise 21-5 (20 minutes)

The scatter diagram and its estimated line of cost behavior appear below.

$600

$700

1160

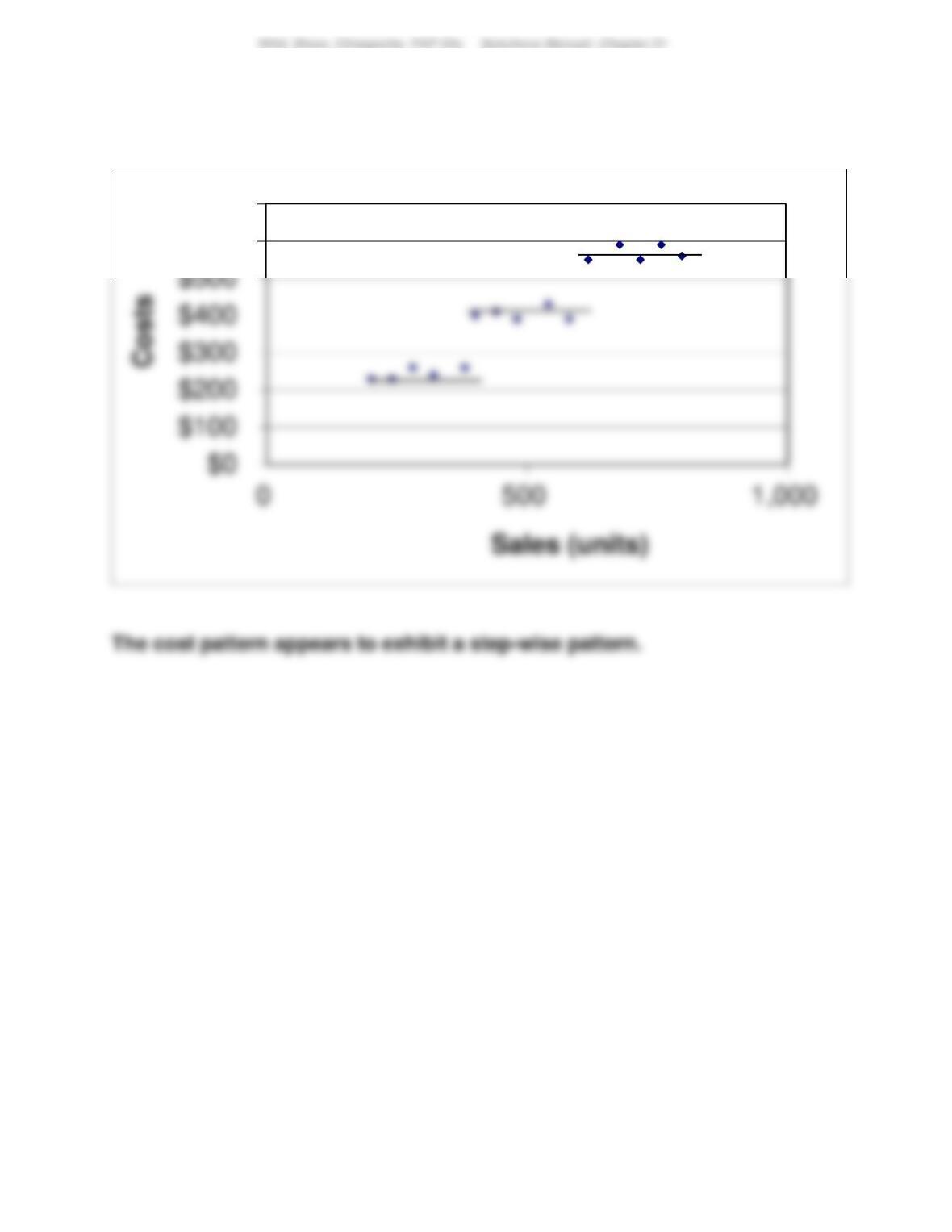

Exercise 21-6 (20 minutes)

The scatter diagram and line of estimated cost behavior appear below.

Selecting 0 and 2,400 units sold as the activity levels yields $2,500 as the

estimate of fixed costs and the following estimate of variable costs per

unit:

Exercise 21-7A (20 minutes)

$2,500,000

$3,000,000

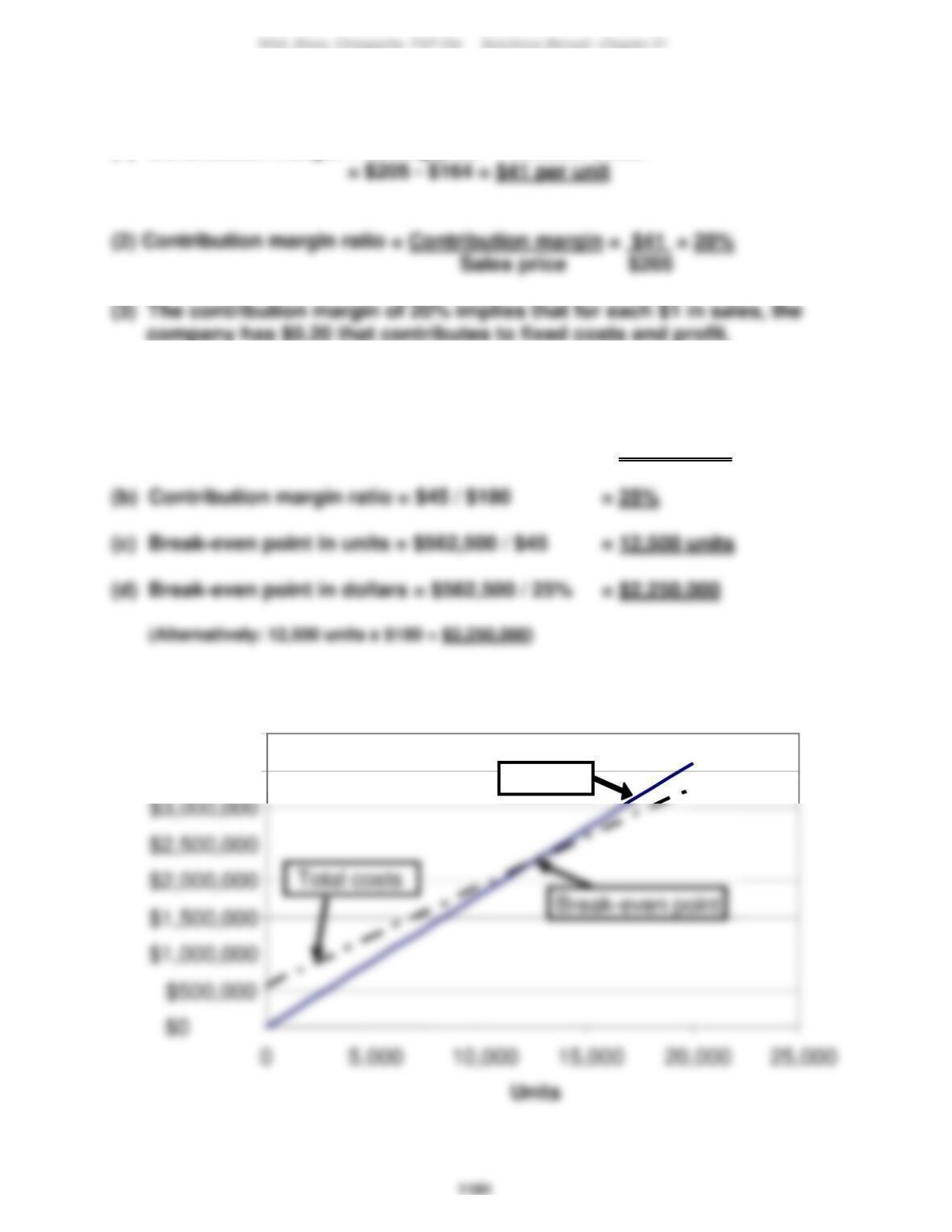

Exercise 21-8 (10 minutes)

(1) Contribution margin = Selling price – Variable costs

Exercise 21-9 (30 minutes)

(a) Contribution margin per unit = $180 – $135 = $45 per unit

Exercise 21-10 (15 minutes)

$3,500,000

$4,000,000

Sales

1162

Exercise 21-11 (20 minutes)

1.

BLANCHARD COMPANY

Contribution Margin Income Statement (at Break-Even)

2. Sales (in dollars) to break even with increased fixed costs

1163

Exercise 21-12 (25 minutes)

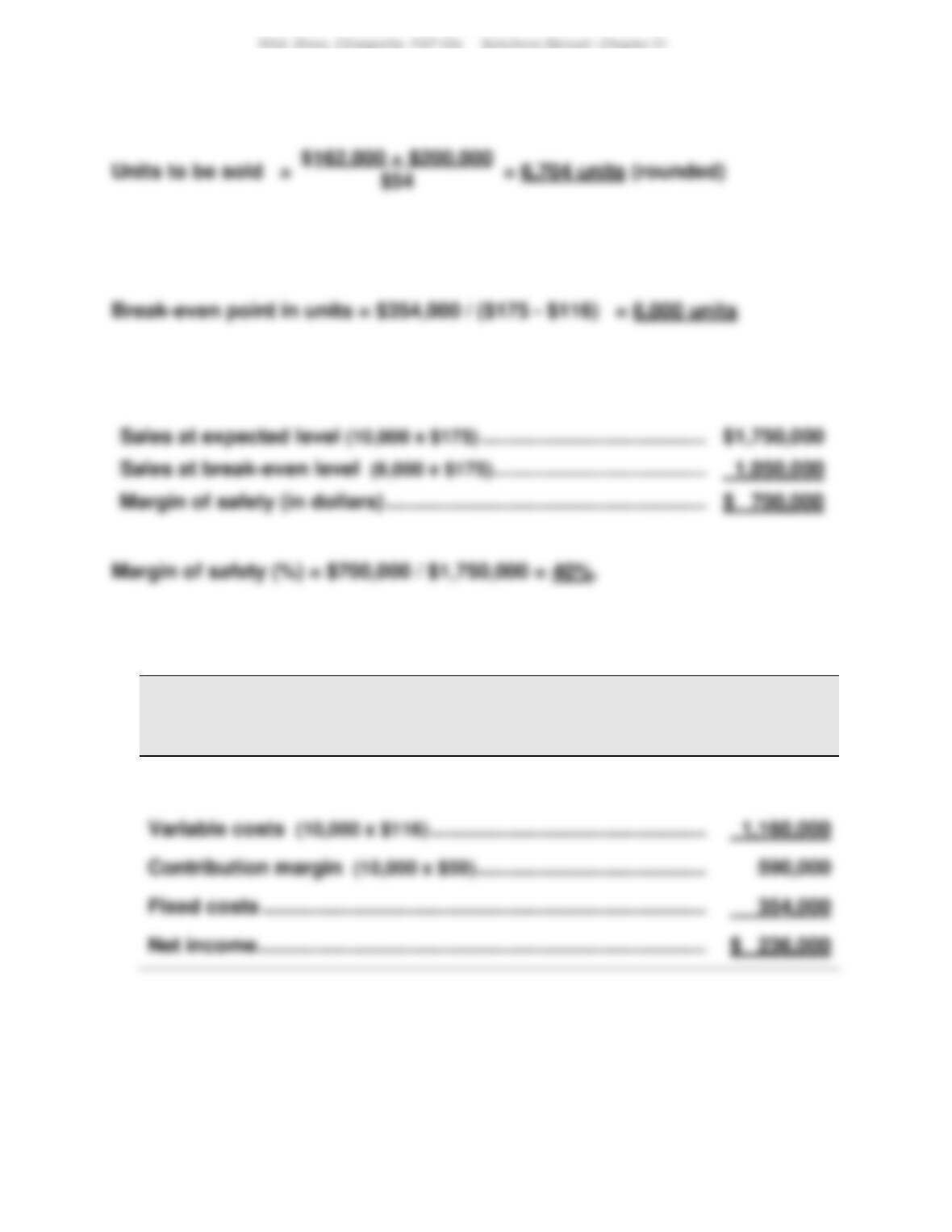

1. Unit sales at target income =

Fixed + Target

2. Dollar sales at target income = costs income

Contribution margin ratio

Exercise 21-13 (20 minutes)

BLANCHARD COMPANY

Forecasted Contribution Margin Income Statement

Sales (40,000 x $200) ………………………………………………………………..

$8,000,000

Fixed Target

costs income

Contribution margin/unit

+

1164

Exercise 21–14 (10 minutes)

1. Fixed costs + Target pretax income

Dollar sales = Contribution margin ratio

2.

Sales …………………………………………….

$1,296,000

Pretax income …………………………..

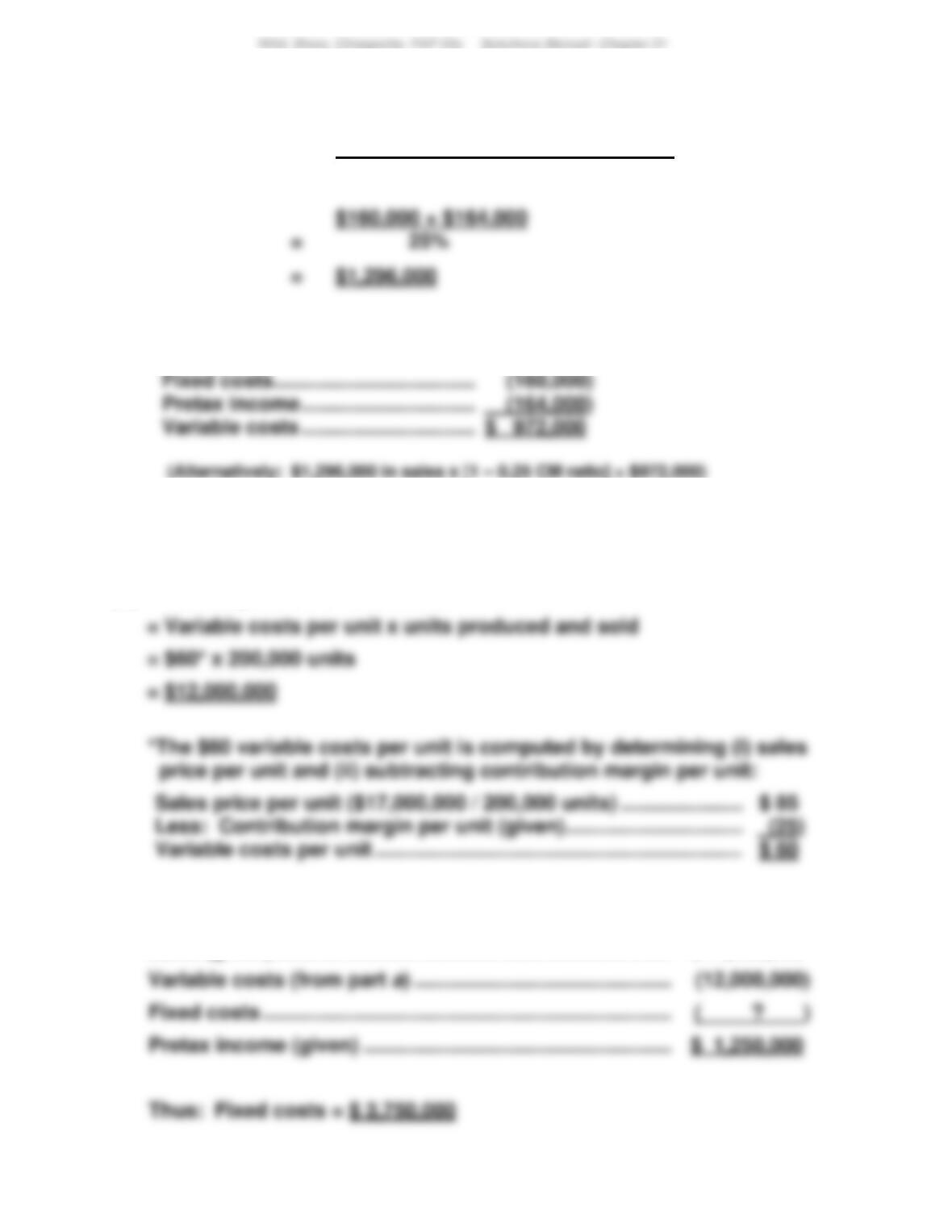

Exercise 21-15 (30 minutes)

(a) Total expected variable costs

(b) To solve, set up a brief contribution margin income statement

Sales (given) …………………………………………………………………..

$17,000,000

Pretax income (given) …………………………………………………….

$ 1,250,000

1165

Exercise 21-16 (10 minutes)

1. Break-even in units = Fixed costs / Contribution margin per unit

Exercise 21-17 (15 minutes)

1. Dollar sales for target income = Fixed costs + Target income

2. Margin of safety (%) = Expected sales – breakeven sales

Exercise 21-18 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2018

Sales (9,600 x $225) ……………………………………………………….………..

$2,160,000

1166

Exercise 21-19 (10 minutes)

1. Revised contribution margin per unit = $240 – $180 = $60

Exercise 21-20 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2018

Sales (11,000 x $225) ……………………………………………………………….

$2,475,000

Variable costs (11,000 x $180) ………………………………………………….

Fixed costs ($324,000 + $81,000) ……………………………………………..

Exercise 21-21 (20 minutes)

1. Pretax income = Sales – Variable costs – Fixed costs

2. Instructor note: Use equation in Exhibit 21.23;