1. Total variable costs change in proportion to changes in the level of activity. Unit variable

costs remain the same regardless of the level of activity.

2. a. Variable costs

b. Variable costs

3. Total fixed cost remains the same regardless of changes in the level of activity. Fixed cost per unit

decreases as the activity level increases and increases as the activity level decreases.

5. a. No impact on the contribution margin.

b

7. Decreases in unit variable costs, such as a decrease in the unit cost of direct materials, will

decrease the break-even point.

8. Austin Company had lower fixed costs and a higher percentage of variable costs to sales than

did Hill Company. Such a situation resulted in a lower break-even point for Austin Company.

9. The individual products are treated as components of one overall enterprise product. These

components are weighted by the sales mix percentages when determining the contribution

margin. Therefore, the sales mix affects the contribution margin and thus the break-even

p

oint.

CHAPTER 21

COST-VOLUME-PROFIT ANALYSIS

DISCUSSION QUESTIONS

CHAPTER 21 Cost-Volume-Profit Analysis

PE 21-1A

PE 21-1B

a. $16 per unit = ($551,000 – $495,000) ÷ (6,600 units – 3,100 units)

b. $445,400 = $551,000 – ($16 × 6,600 units), or $495,000 – ($16 × 3,100 units)

PE 21-2A

a. 30.0% = ($60 – $42) ÷ $60, or ($5,400,000 – $3,780,000) ÷ $5,400,000

b. $18 per unit = $60 – $42

c. Sales……………………………………… $5,400,000 (90,000 units × $60 per unit)

PE 21-2B

a. 25% = ($16 – $12) ÷ $16, or ($1,984,000 – $1,488,000) ÷ $1,984,000

b. $4 per unit = $16 – $12

c. Sales……………………………………… $1,984,000 (124,000 units × $16 per unit)

PRACTICE EXERCISES

CHAPTER 21 Cost-Volume-Profit Analysis

PE 21-3A

PE 21-3B

a. 2,600 units = $65,000 ÷ ($90 – $65)

b. 1,625 units = $65,000 ÷ ($105 – $65)

PE 21-4A

PE 21-4B

a. 3,600 units = $180,000 ÷ ($220 – $170)

b. 4,720 units = ($180,000 + $56,000) ÷ ($220 – $170)

PE 21-5A

Unit selling price of E: [($125 × 0.40) + ($90 × 0.60)] = $104

PE 21-5B

Unit selling price of E: [($40 × 0.70) + ($60 × 0.30)] = $46

Unit variable cost of E: [($15 × 0.70) + ($25 × 0.30)] = 18

Unit contribution margin of E $28

Break-Even Sales (units) = 16,400 units = $459,200 ÷ $28

Break-Even Sales (units) for QQ = 16,400 units of E × 70% = 11,480 units of Product QQ

Break-Even Sales (units) for ZZ = 16,400 units of E × 30% = 4,920 units of Product ZZ

CHAPTER 21 Cost-Volume-Profit Analysis

PE 21-6A

PE 21-6B

Contribution Margin $352,000

Income from Operations $220,000

PE 21-7A

PE 21-7B

= $740,000 – $547,600

$740,000 = 26%

Operating Leverage

Margin of Safety = Sales – Sales at Break-Even Point

Sales

= = = 1.6

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-1

1. Variable 9. Variable

2. Fixed 10. Variable

3. Variable 11. Mixed

4. Variable 12. Mixed

Ex. 21-2

a. Cost Graph Four d. Cost Graph One

Ex. 21-3

1. a 4. f

2. c 5. b

3. e 6. d

Ex. 21-4

1. e

2. f

EXERCISES

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-5

a. Variable f. Fixed

b. Variable g. Fixed*

c. Fixed h. Fixed

Ex. 21-6

Components produced……………

…

45,000 60,000 75,000

Total costs:

Total variable costs……………

…

$1,350,000 (d) $1,800,000 (j) $2,250,000

Total fixed costs………………… 810,000 (e) 810,000 (k) 810,000

Total costs………………………

…

$2,160,000 (f) $2,610,000 (l) $3,060,000

Cost per unit:

V

ariable cost per unit…………

…

(a) $30.00 (g) $30.00 (m) $30.00

Supporting calculations:

a. $30.00 ($1,350,000 ÷ 45,000 units)

b. $18.00 ($810,000 ÷ 45,000 units)

h. $13.50 ($810,000 ÷ 60,000 units)

i.

j. $2,250,000 ($30.00 × 75,000 units)

k. $810,000 (fixed costs do not change with volume)

l.

$43.50 ($30.00 + $13.50)

$3,060,000 ($2,250,000 + $810,000)

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-7

The fixed cost can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of production, as

follows:

Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Highest level:

$24,090,000 = ($163.00 × 90,000 units) + Fixed Costs

$24,090,000 = $14,670,000 + Fixed Costs

$9,420,000 = Fixed Costs

Lowest level:

b. Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Total cost for 86,000 units:

Variable cost:

Units………………………………………

…

86,000

V

ariable cost per unit……………………

…

$163.00

=Variable Cost per Unita.

Difference in Total Costs

Difference in Units Produced

×

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-8

The fixed costs can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of gross-ton mile,

as follows:

Total Cost = (Variable Cost per Gross-Ton Mile × Gross-Ton Miles) + Fixed Costs

Highest level:

= ($2.10 × 1,000,000 gross-ton miles) + Fixed Costs

= $2,100,000 + Fixed Costs

= Fixed Costs

Ex. 21-9

a. Sales…………………………………………………………………………….. $1,800,000

V

ariable costs…………………………………………………………………

…

1,116,000

Contribution margin…………………………………………………………

…

$ 684,000

b. Sales…………………………………………………………………………….. $2,500,000

…

…

Sales – Variable Costs

Sales

Difference in Gross-Ton Miles

=

=$684,000

$1,800,000 = 38%

Contribution

Margin Ratio

$2,700,000

$2,700,000

$600,000

Difference in Total Costs

=

Variable Cost per

Gross-Ton Mile

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-10

a. Sales (in millions)…………………………………………………………………

…

$12,718.9

Variable costs (in millions):

Food and packaging…………………………………………………………

…

$ 4,033.5

$4,264.4 million

$12,718.9 million

c. Same-store sales increase (in millions)………………………………………

…

$500.0

Contribution margin ratio [from part (b)]……………………………………

…

33.5

Increase in income from operations (in millions)…………………………

…

$167.5

Ex. 21-11

$12,600,000

$540 – $360

Sales – Variable Costs

Sales

b. =Contribution Margin Ratio

= = 33.5%

a. Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

= = 70,000 units

×%

×%

…

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-12

Total Cost Variable Cost Variable Cost

(in millions) Percentage (in millions)

Cost of goods sold………………………

…

$20,360 × 75% = $15,270

Selling, general, and administrative

expenses……………………….………

…

16,438 × 50% = 8,219

Total Cost Variable Cost Fixed Cost

(in millions) (in millions) (in millions)

Number of

Total Amount Barrels

(in millions) (in millions) Per-Unit Amount

Net sales…………………………………

…

$54,619 ÷ 400 = $136.55

V

ariable cost of goods sold……………

…

15,270 ÷ 400 = 38.18

Variable selling, general,

and administrative expenses………

…

8,219 ÷ 400 = 20.55

The variable costs per unit are determined by multiplying the total amount of each cost by the

variable cost percentage (75% for cost of goods sold and 50% for selling, general, and

administrative expenses), then dividing by the number of barrels.

1

($20,360,000,000 × 25%) + ($16,438,000,000 × 50%)

2

$54,619,000,000 ÷ 400,000,000

3

($20,360,000,000 × 75%) ÷ 400,000,000

4

($16,438,000,000 × 50%) ÷ 400,000,000

Ex. 21-13

=

Fixed Costs

Unit Contribution Margin

= 17,000 units

$750 – $600

$2,550,000

a.

=

Break-Even Sales (units)

…

…

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-14

$4,000

Ex. 21-15

The cost of the promotional campaign is the fixed cost in this analysis because

we’re trying to determine the break-even adoption rate of the campaign.

Note: The variable cost is for 14 months because the costs are incurred, even during

the free months.

The break-even number of subscribers necessary to cover the fixed cost of the

promotion is computed as follows:

=Break-Even Sales (units)

Fixed Costs

= 2,000 units

Unit Contribution Margin

=

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-16

=27.2 million (rounded) accounts

1

Revenue per account (in millions):

$33,600 million ÷ 32.6 million = $1,030.7 (rounded)

2

Variable cost per account (in millions, except variable cost per account):

Cost of revenue……………………………………………… $13,389 × 70% = $ 9,372.3

Selling, general, and administrative expenses………… 7,774 × 30% =2,332.2

3

Fixed costs (in millions):

Cost of revenue……………………………………………… $13,389 × 30% = $ 4,016.7

Selling, general, and administrative expenses………… 7,774 × 70% =5,441.8

Depreciation…………………………………………………

…

8,783 × 100% =8,783.0

Total fixed costs……………………………………………

…

$18,241.5

*

Difference between $11,704.5 in Part (a) and $11,703.4 is due to rounding.

Note to Instructors: The rate charged per minute and the number of average

minutes of digital service influence the revenue per account. An interesting

question is whether the costs are variable to the number of minutes or

number of accounts. If we assume that the costs are variable to the number

of minutes, then the break-even analysis revolves around the number of

b. Break-Even =

Fixed Cost

Revenue per Account – Variable Cost per Account

…

CHAPTER 21 Cost-Volume-Profit Analysis

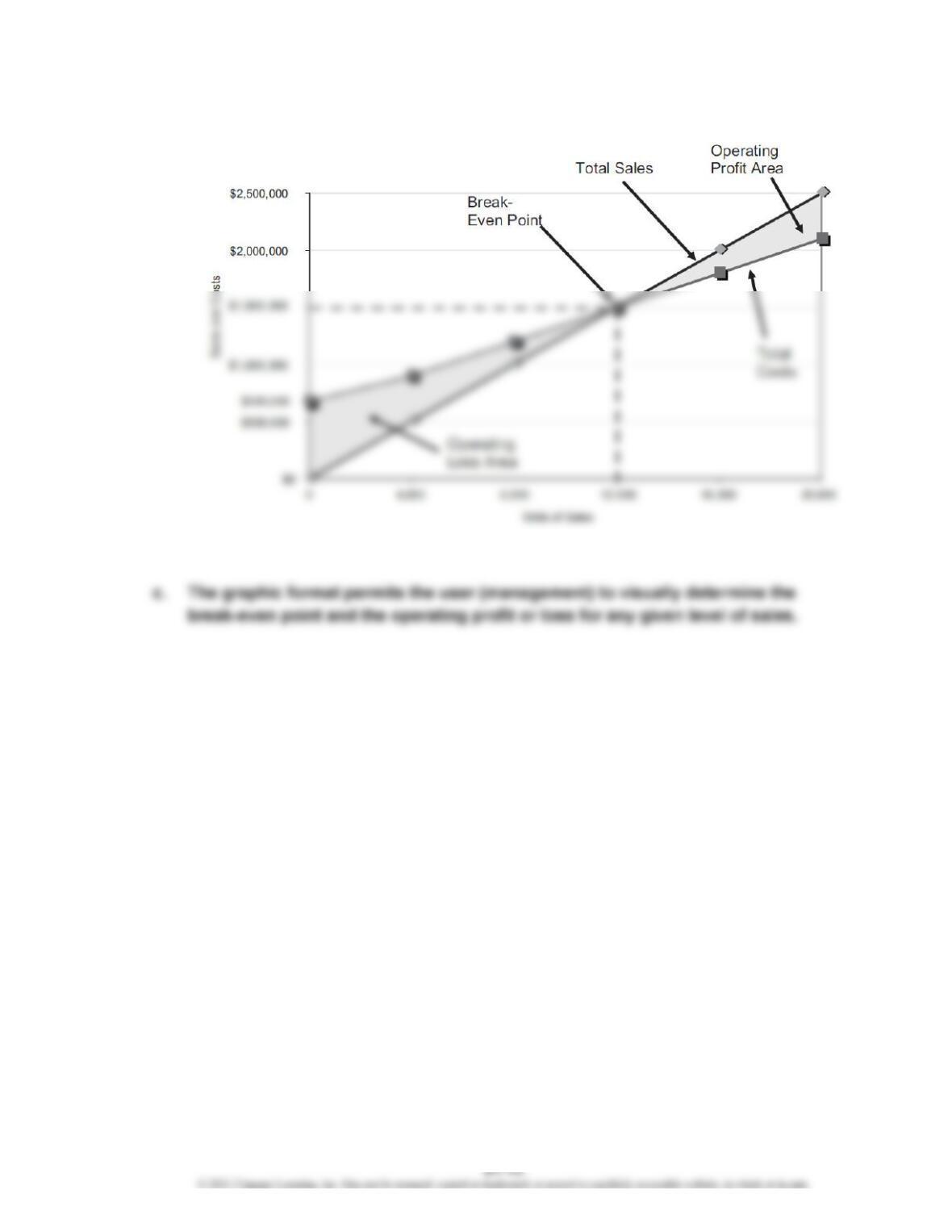

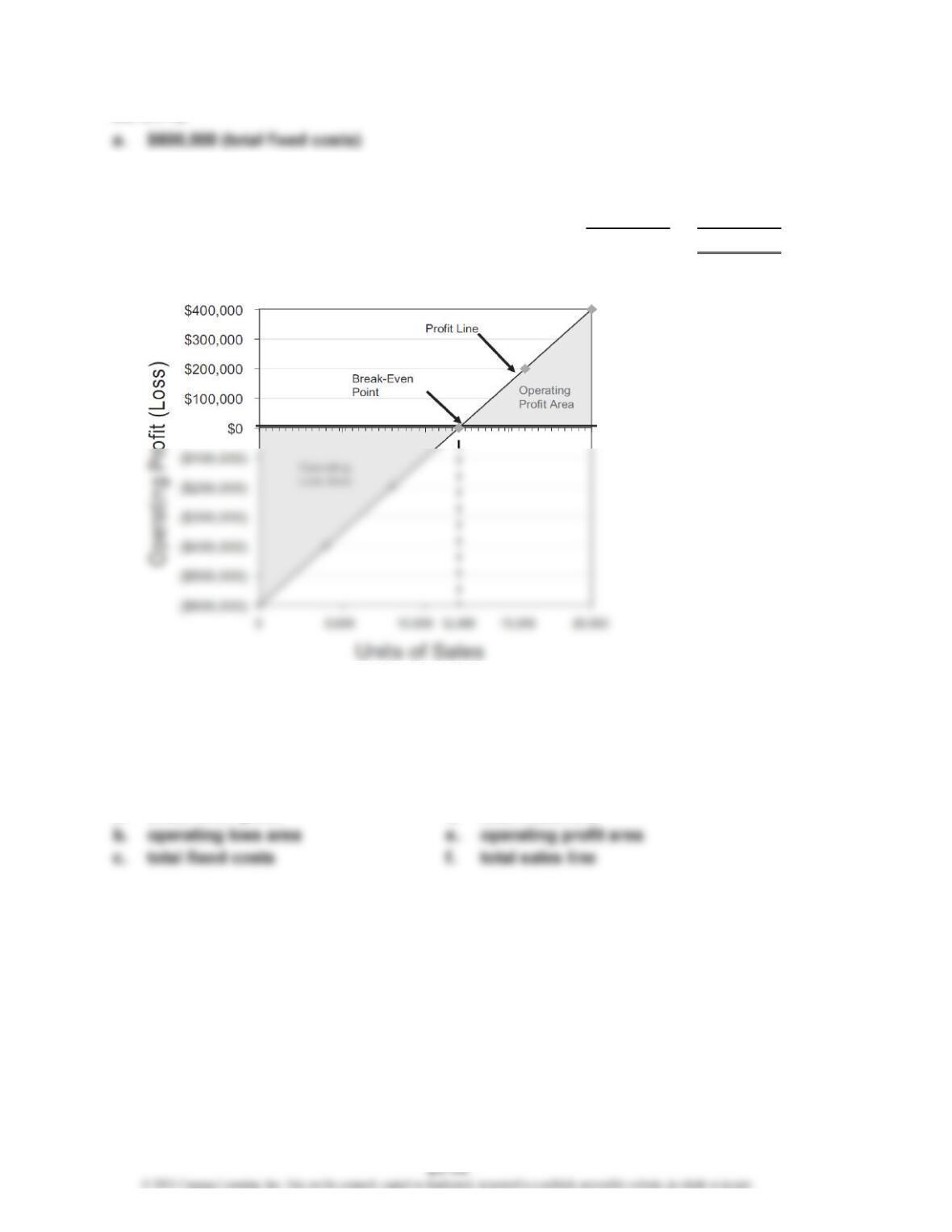

Ex. 21-17

a.

b. $1,500,000 (the intersection of the total sales line and the total costs line)

CHAPTER 21 Cost-Volume-Profit Analysis

b. Sales (20,000 units × $125)……………………………

…

$2,500,000

Fixed costs………………………………………………… $ 600,000

V

ariable costs (20,000 units × $75)……………………

…

1,500,000 2,100,000

Income from operations…………………………………

…

$ 400,000

*20,000 units = $2,500,000 maximum sales ÷

$125 unit selling price

c.

d. 12,000 units (the intersection of the profit line and the horizontal axis)

Ex. 21-19

Cost-volume-profit chart

a. break-even point d. total costs line

*

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-20

Profit-volume chart

a. break-even point

b. total fixed costs

Ex. 21-21

a. Unit Selling Price of E = ($95 × 60%) + ($115 × 40%)

= $57 + $46 = $103

Unit Variable Cost of E = ($55 × 60%) + ($75 × 40%)

= $33 + $30 = $63

b. 10,680 units of baseball bats (17,800 units × 60%)

7,120 units of baseball gloves (17,800 units × 40%)

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-22

a. Unit contribution margin of overall product (E):

Unit selling price of E [(10% × $800) + (90% × $300)]……………………

…

$350

Unit variable cost of E [(10% × $140) + (90% × $120)]…………………… 122

Unit contribution margin of E………………………………………………

…

$228

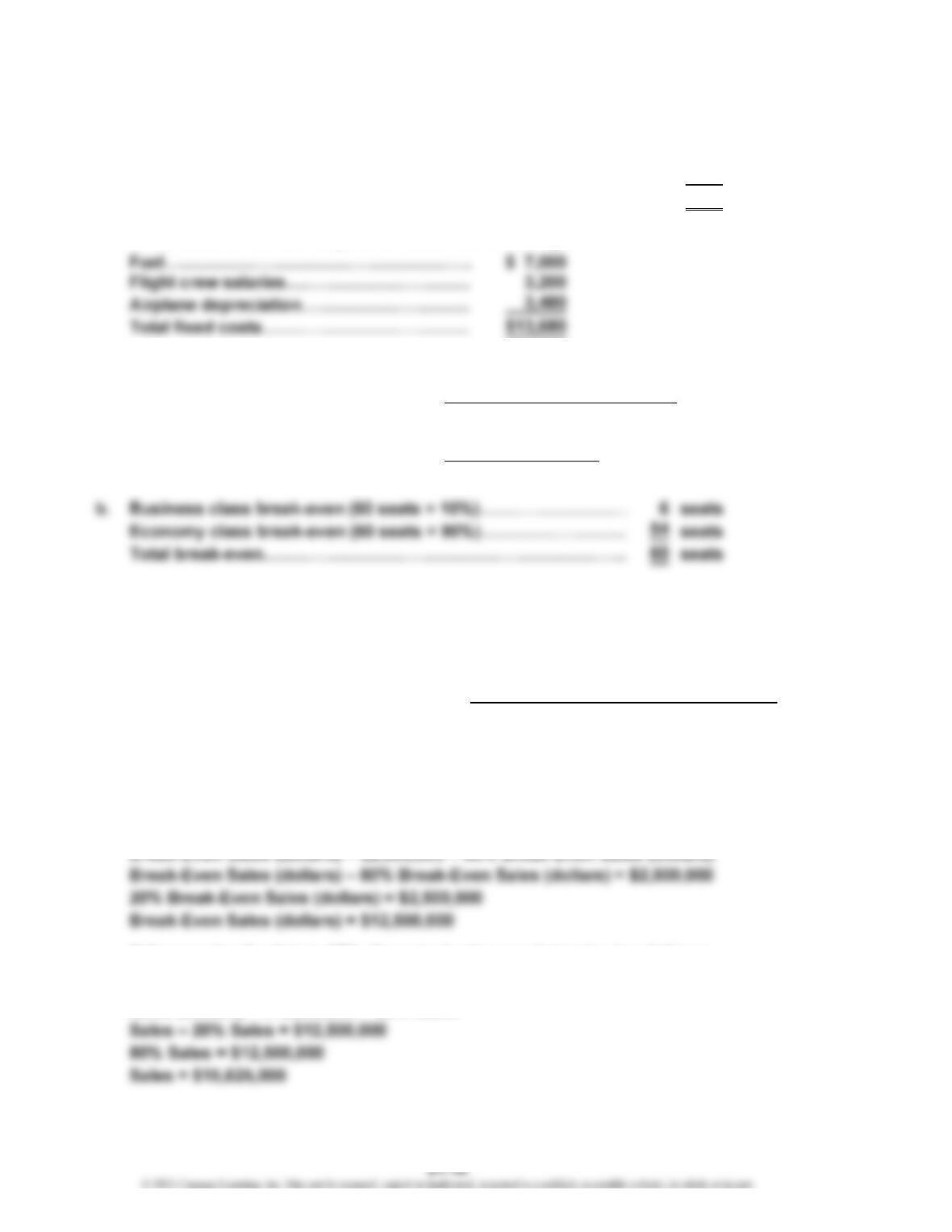

Fixed costs of the Los Angeles to Kona round-trip flight:

Break-even sales (units) of overall product:

Ex. 21-23

a. (1) = Sales – Sales at Break-Even Point

= $1,450,000 – $1,160,000 = $290,000

= $290,000 ÷ $1,450,000 = 20%

b. The break-even point (S) is determined as follows:

Break-Even Sales (dollars) = Total Fixed Costs + Total Variable Costs (at Break-Even)

Break-Even Sales (dollars) = Total Fixed Costs + 80% Break-Even Sales (dollars)

If the margin of safety is 20%, the actual sales are determined as follows:

Sales = Break-Even Sales (dollars) + (Sales × Margin of Safety)

Sales (dollars) = $12,500,000 + 20% Sales

=

=Break-Even Sales (units)

(2)

= = 60 seats (tickets)

Fixed Costs

$13,680

$228 per seat

Unit Contribution Margin

Margin of Safety (percentage)

Margin of Safety (dollars)

Sales – Sales at Break-Even Point

Sales

CHAPTER 21 Cost-Volume-Profit Analysis

Ex. 21-24

If 420,000 units are sold and sales at the break-even point are 472,500 units,

there is no margin of safety.

Ex. 21-25

a. Beck Inc.:

$500,000

$100,000

b. Beck Inc.’s income from operations would increase by 100% (5.0 × 20%),

or $100,000 (100% × $100,000), and Bryant Inc.’s income from operations

would increase by 50% (2.5 × 20%), or $150,000 (50% × $300,000).

c. The difference in the increases of income from operations is due to the

Appendix Ex. 21-26

a. Variable cost of goods sold

b. Variable selling and administrative expenses

Operating Leverage

= 5.0

=

=

Contribution Margin

Income from Operations

CHAPTER 21 Cost-Volume-Profit Analysis

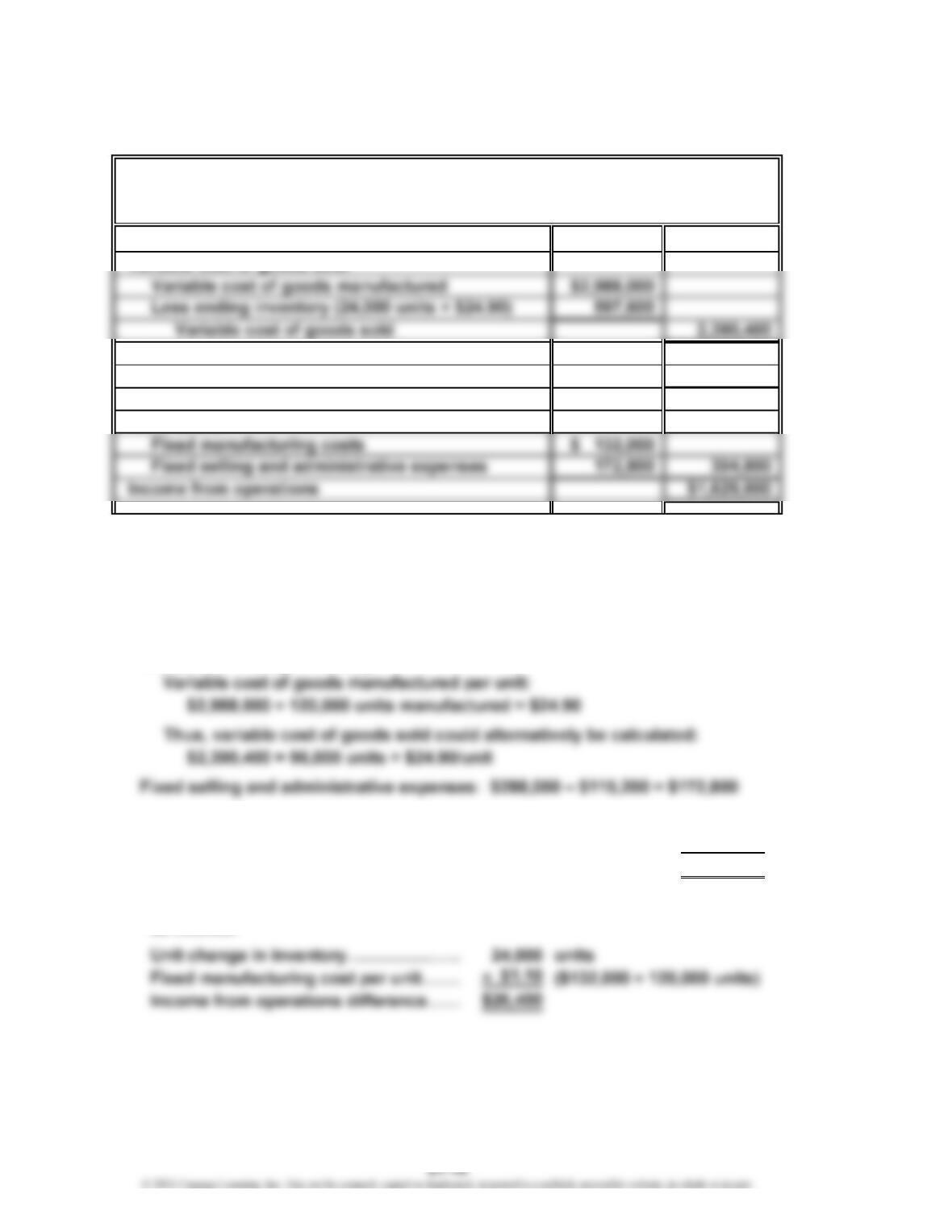

Appendix Ex. 21-27

a.

Sales $4,440,000

Manufacturing margin $2,049,600

V

ariable selling and administrative expenses 115,200

Contribution margin $1,934,400

Fixed costs:

Computations:

Variable cost of goods manufactured: $3,120,000 – $132,000 = $2,988,000

Units Sold = Units Manufactured – Units in Ending Inventory

96,000 = Units Manufactured – 24,000

120,000 = Units Manufactured

Unit cost of ending inventory:

b. Absorption costing income from operations………………………

…

$1,656,000

V

ariable costing income from operations…………………………… 1,629,600

Difference……………………………………………………………….…

…

$ 26,400

Note: The difference between the two income numbers can be reconciled

Rhys Company

Income Statement—Variable Costing

For the Month Ended July 31

V

CHAPTER 21 Cost-Volume-Profit Analysis

Appendix Ex. 21-28

a.

Sales $7,450,000

Cost of goods sold:

Cost of goods manufactured (500,000 units × $14.32) $7,160,000

Less ending inventory (80,000 units × $14.32) 1,145,600

Computations:

Cost of goods manufactured: $7,000,000 + $160,000 = $7,160,000

Unit cost of ending inventory:

Total cost of goods manufactured:

$7,160,000 ÷ 500,000 units manufactured = $14.32

b.

V

ariable costing income from operations…………………………………

…

$1,255,000

Absorption costing income from operations………………………………

…

1,280,600

Difference…………………………………………………………………………

…

$ 25,600

Tudor Manufacturing Co.

Income Statement—Absorption Costing

For the Month Ended June 30

CHAPTER 21 Cost-Volume-Profit Analysis

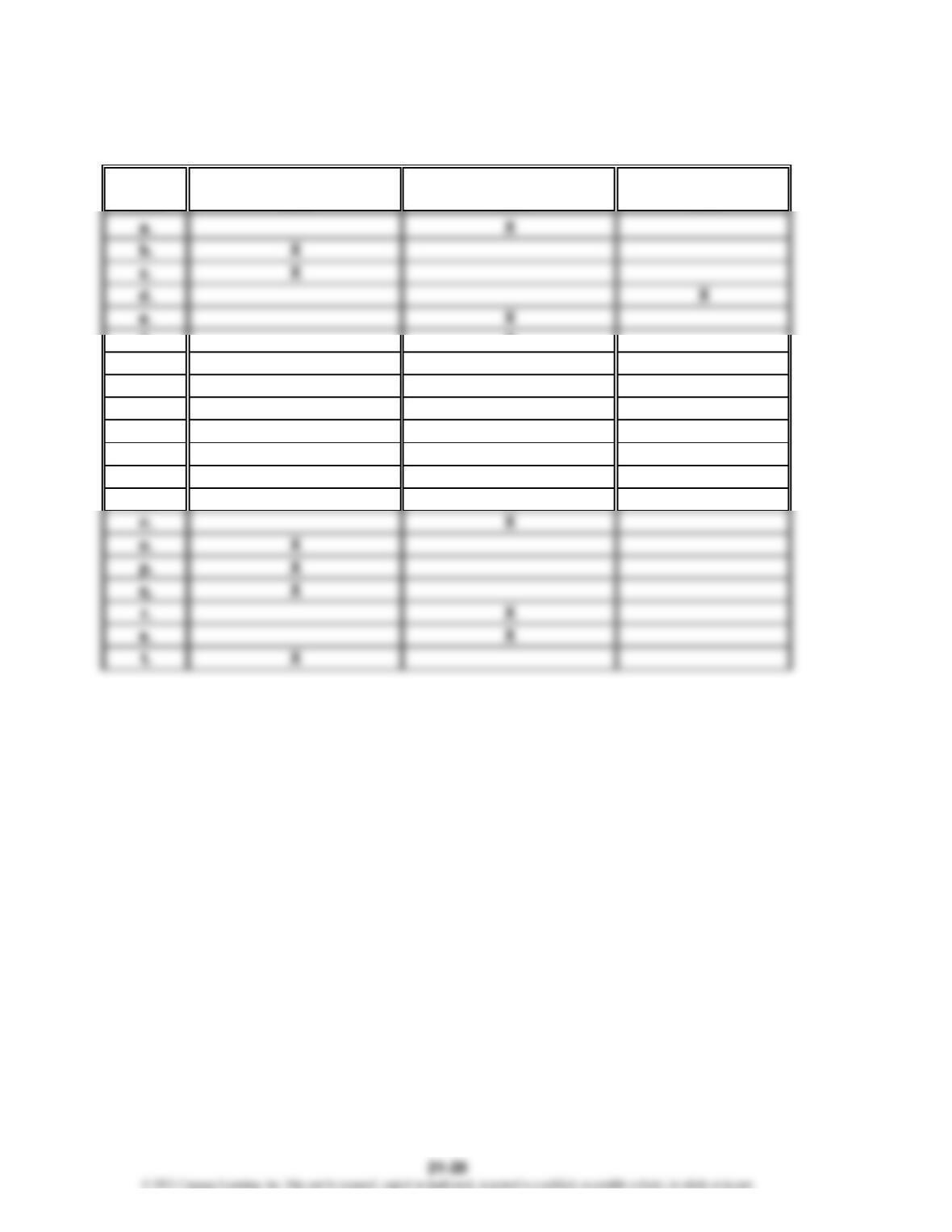

Prob. 21-1A

Fixed Variable Mixed

Cost Cost Cost Cost

f. X

g. X

h. X

i. X

j. X

k. X

l. X

m. X

PROBLEMS