21-1

CHAPTER 21

CAPITAL BUDGETING AND COST ANALYSIS

21-1 No. Capital budgeting focuses on an individual investment project throughout its life,

recognizing the time value of money. The life of a project is often longer than a year. Accrual

accounting focuses on a particular accounting period, often a year, with an emphasis on income

determination.

21-2 The five stages in capital budgeting are the following:

1. An identification stage to determine which types of capital investments are available to

accomplish organization objectives and strategies.

21-3 In essence, the discounted cash-flow method calculates the expected cash inflows and

outflows of a project as if they occurred at a single point in time so that they can be aggregated

(added, subtracted, etc.) in an appropriate way. This enables comparison with cash flows from

other projects that might occur over different time periods.

21-5 Sensitivity analysis can be incorporated into DCF analysis by examining how the DCF of

each project changes with changes in the inputs used. These could include changes in revenue

assumptions, cost assumptions, tax rate assumptions, and discount rates.

21-6 The payback method measures the time it will take to recoup, in the form of expected

future net cash inflows, the net initial investment in a project. The payback method is simple and

easy to understand. It is a handy method when screening many proposals and particularly when

21-2

understand, and considers profitability. Its weaknesses are that it ignores the time value of money

and does not consider the cash flows for a project.

21-8 No. The discounted cash-flow techniques implicitly consider depreciation in rate of

return computations; the compound interest tables automatically allow for recovery of

investment. The net initial investment of an asset is usually regarded as a lump-sum outflow at

time zero. Where taxes are included in the DCF analysis, depreciation costs are included in the

computation of the taxable income number that is used to compute the tax payment cash flow.

21-10 All overhead costs are not relevant in NPV analysis. Overhead costs are relevant only if

the capital investment results in a change in total overhead cash flows. Overhead costs are not

relevant if total overhead cash flows remain the same but the overhead allocated to the particular

capital investment changes.

21-11 The Division Y manager should consider why the Division X project was accepted and

the Division Y project rejected by the president. Possible explanations are

a. The president considers qualitative factors not incorporated into the IRR computation

and this leads to the acceptance of the X project and rejection of the Y project.

21-12 The categories of cash flow that should be considered in an equipment-replacement

decision are:

1. a. Initial machine investment,

b. Initial working-capital investment,

21-13 Income taxes can affect the cash inflows or outflows in a motor vehicle replacement

decision as follows:

a. Tax is payable on gain or loss on disposal of the existing motor vehicle.

21-3

21-14 A cellular telephone company manager responsible for retaining customers needs to

consider the expected future revenues and the expected future costs of “different investments” to

retain customers. One such investment could be a special price discount. An alternative

investment is offering loyalty club benefits to long-time customers.

21-15 These two rates of return differ in their elements:

21-16 Exercises in compound interest, no income taxes.

To be sure that you understand how to use the tables in Appendix A at the end of this book, solve

the following exercises. Ignore income tax considerations. The correct answers, rounded to the

nearest dollar, appear on pages 838–839.

Required:

1. You have just won $10,000. How much money will you accumulate at the end of 10 years if

you invest it at 8% compounded annually? At 10%?

2. Ten years from now, the unpaid principal of the mortgage on your house will be $154,900.

How much do you need to invest today at 4% interest compounded annually to accumulate

the $154,900 in 10 years?

3. If the unpaid mortgage on your house in 10 years will be $154,900, how much money do you

need to invest at the end of each year at 10% to accumulate exactly this amount at the end of

the 10th year?

4. You plan to save $7,500 of your earnings at the end of each year for the next 10 years. How

much money will you accumulate at the end of the 10th year if you invest your savings

compounded at 8% per year?

5. You have just turned 65 and an endowment insurance policy has paid you a lump sum of

$250,000. If you invest the sum at 8%, how much money can you withdraw from your

account in equal amounts at the end of each year so that at the end of 10 years (age 75) there

will be nothing left?

6. You have estimated that for the first 10 years after you retire you will need a cash inflow of

$65,000 at the end of each year. How much money do you need to invest at 8% at your

retirement age to obtain this annual cash inflow? At 12%?

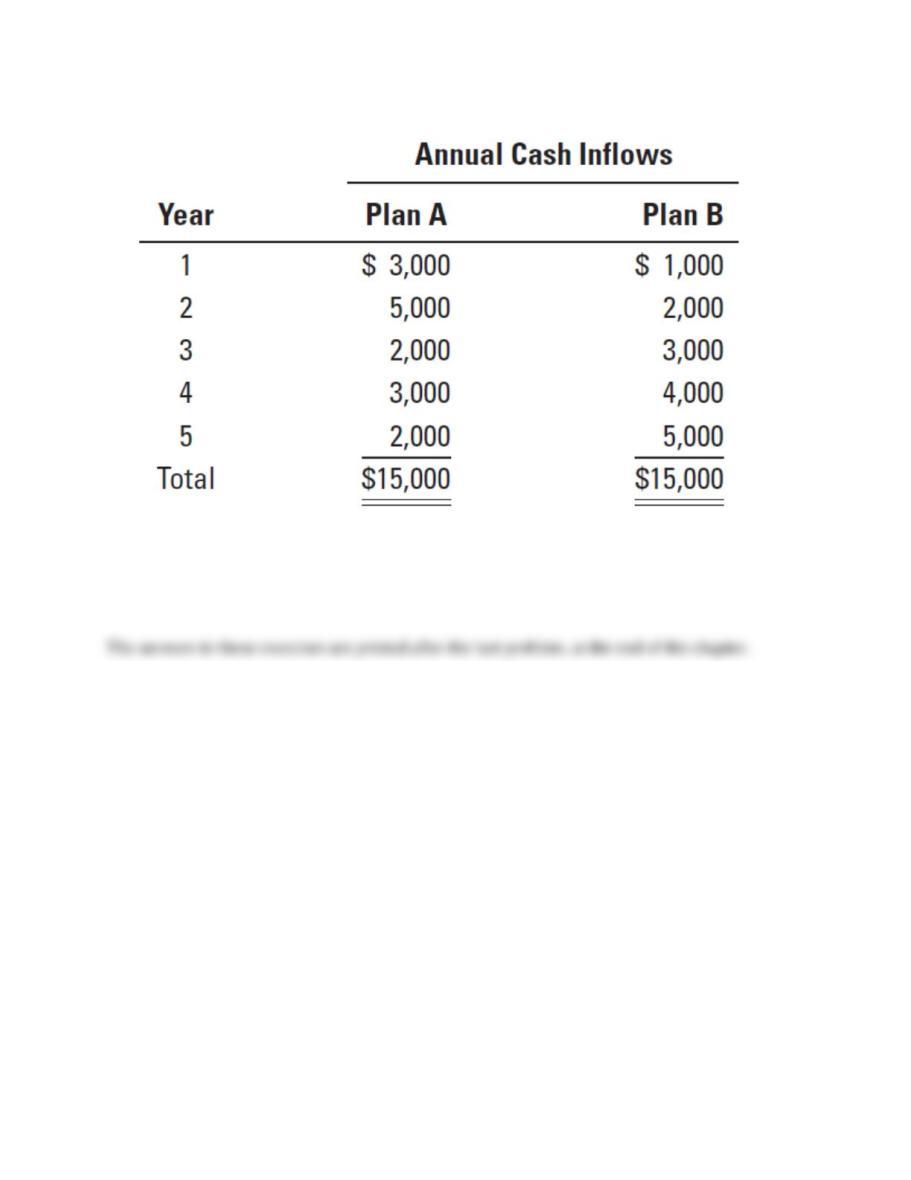

7. The following table shows two schedules of prospective operating cash inflows, each of

which requires the same net initial investment of $10,000 now:

21-4

The required rate of return is 8% compounded annually. All cash inflows occur at the end of

each year. In terms of net present value, which plan is more desirable? Show your computations.

SOLUTION

21-17 (20–25 min.) Capital budgeting methods, no income taxes.

Riverbend Company runs hardware stores in a tristate area. Riverbend’s management estimates

that if it invests $250,000 in a new computer system, it can save $65,000 in annual cash

operating costs. The system has an expected useful life of 8 years and no terminal disposal value.

The required rate of return is 8%. Ignore income tax issues in your answers. Assume all cash

flows occur at year-end except for initial investment amounts.

Required:

1. Calculate the following for the new computer system:

a. Net present value

b. Payback period

c. Discounted payback period

d. Internal rate of return (using the interpolation method)

e. Accrual accounting rate of return based on the net initial investment (assume straight-line

depreciation)

2. What other factors should Riverbend consider in deciding whether to purchase the new

computer system?

21-5

SOLUTION

21-6

21-18 (25 min.) Capital budgeting methods, no income taxes.

City Hospital, a nonprofit organization, estimates that it can save $28,000 a year in cash

operating costs for the next 10 years if it buys a special-purpose eye-testing machine at a cost of

$110,000. No terminal disposal value is expected. City Hospital’s required rate of return is 14%.

Assume all cash flows occur at year-end except for initial investment amounts. City Hospital

uses straight-line depreciation.

Required:

1. Calculate the following for the special-purpose eye-testing machine:

a. Net present value

b. Payback period

c. Internal rate of return

d. Accrual accounting rate of return based on net initial investment

e. Accrual accounting rate of return based on average investment

2. What other factors should City Hospital consider in deciding whether to purchase the special–

purpose eye-testing machine?

21-7

SOLUTION

21-8

21-19 (35 min.) Capital budgeting, income taxes.

Assume the same facts as in Exercise 21-18 except that City Hospital is a taxpaying entity. The

income tax rate is 30% for all transactions that affect income taxes.

Required:

1. Do requirement 1 of Exercise 21-18.

2. How would your computations in requirement 1 be affected if the special-purpose machine

had a $10,000 terminal disposal value at the end of 10 years? Assume depreciation

deductions are based on the $110,000 purchase cost and zero terminal disposal value using

the straight-line method. Answer briefly in words without further calculations.

SOLUTION

21-9

21-10

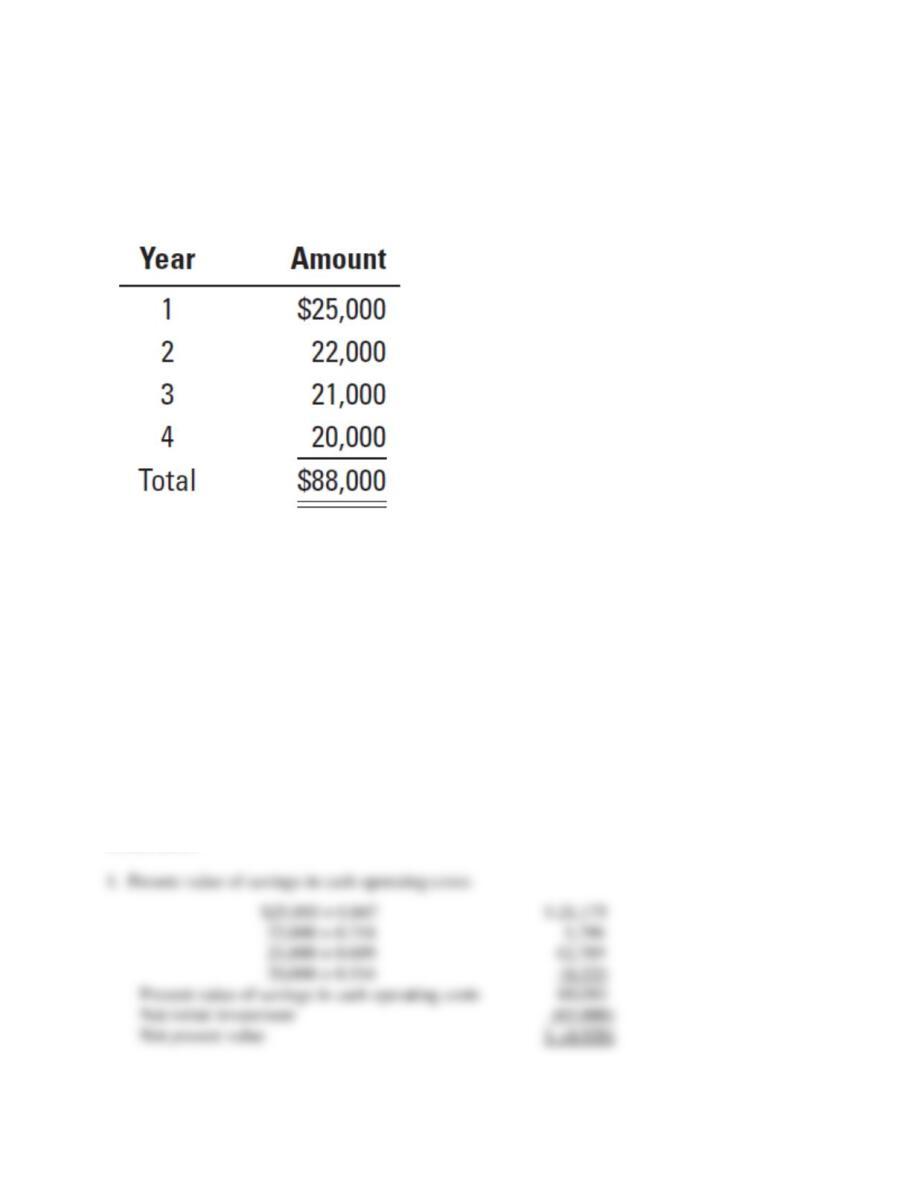

21-20 (25 min.) Capital budgeting with uneven cash flows, no income taxes.

America Cola is considering the purchase of a special-purpose bottling machine for $65,000. It is

expected to have a useful life of 4 years with no terminal disposal value. The plant manager

estimates the following savings in cash operating costs:

Southern Cola uses a required rate of return of 18% in its capital budgeting decisions. Ignore

income taxes in your analysis. Assume all cash flows occur at year-end except for initial

investment amounts.

Calculate the following for the special-purpose bottling machine:

Required:

1. Net present value

2. Payback period

3. Discounted payback period

4. Internal rate of return (using the interpolation method)

5. Accrual accounting rate of return based on net initial investment (Assume straight-line

depreciation. Use the average annual savings in cash operating costs when computing the

numerator of the accrual accounting rate of return.)

SOLUTION

21-11

21-12

21-21 (30 min.) Comparison of projects, no income taxes.

(CMA, adapted) New Tech Corporation is a rapidly growing biotech company that has a

required rate of return of 8%. It plans to build a new facility in Santa Clara County. The building

will take 2 years to complete. The building contractor offered New Bio a choice of three

payment plans, as follows:

▪ Plan I: Payment of $325,000 at the time of signing the contract and $4,825,000 upon

completion of the building. The end of the second year is the completion date.

▪ Plan II: Payment of $1,675,000 at the time of signing the contract and $1,675,000 at the

end of each of the 2 succeeding years.

▪ Plan III: Payment of $425,000 at the time of signing the contract and $1,650,000 at the

end of each of the 3 succeeding years.

Required:

1. Using the net present value method, calculate the comparative cost of each of the three

payment plans being considered by New Tech.

2. Which payment plan should New Tech choose? Explain.

3. Discuss the financial factors, other than the cost of the plan, and the nonfinancial factors that

should be considered in selecting an appropriate payment plan.

SOLUTION

21-14

21-22 (30 min.) Payback and NPV methods, no income taxes.

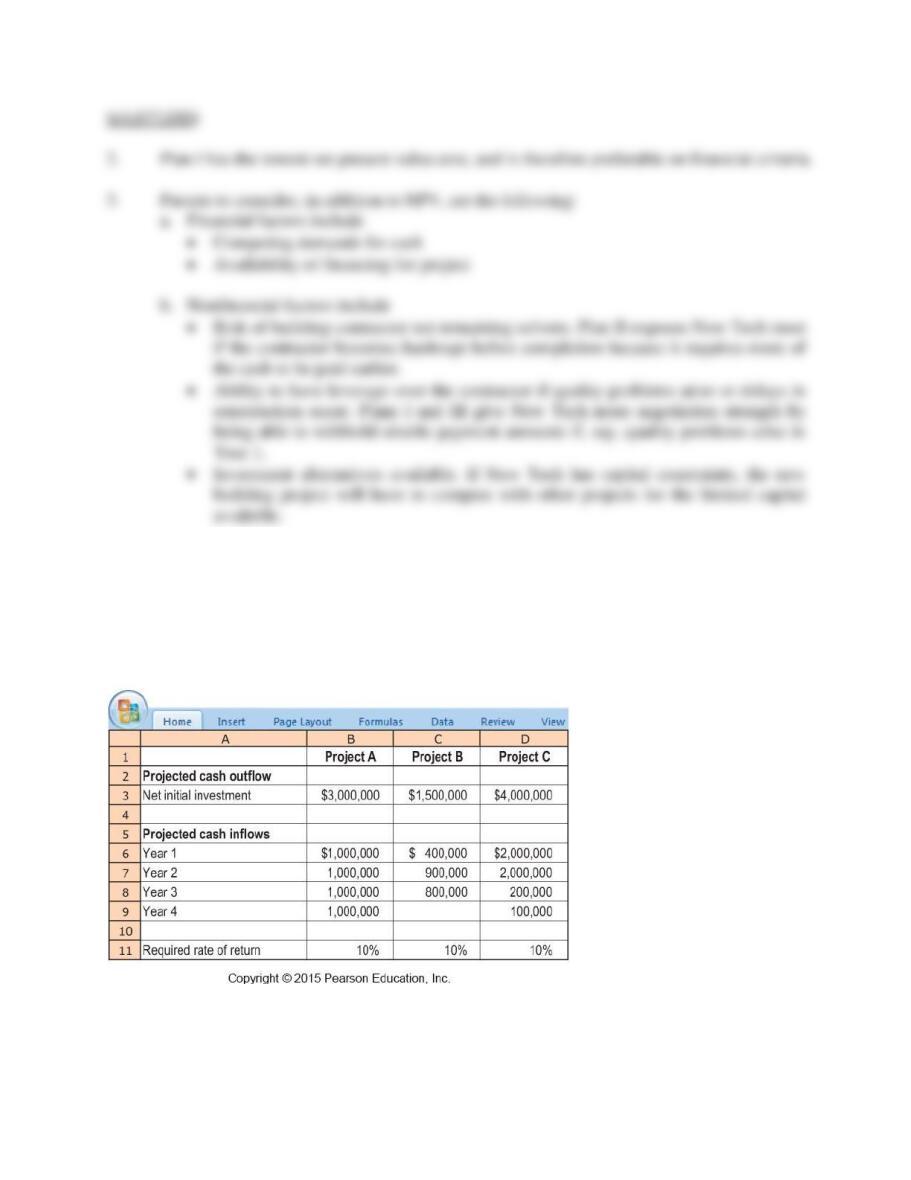

(CMA, adapted) Andrews Construction is analyzing its capital expenditure proposals for the

purchase of equipment in the coming year. The capital budget is limited to $5,000,000 for the

year. Lori Bart, staff analyst at Andrews, is preparing an analysis of the three projects under

consideration by Corey Andrews, the company’s owner.

Required:

1. Because the company’s cash is limited, Andrews thinks the payback method should be used

to choose between the capital budgeting projects.

21-15

a. What are the benefits and limitations of using the payback method to choose between

projects?

b. Calculate the payback period for each of the three projects. Ignore income taxes. Using

the payback method, which projects should Andrews choose?

2. Bart thinks that projects should be selected based on their NPVs. Assume all cash flows

occur at the end of the year except for initial investment amounts. Calculate the NPV for

each project. Ignore income taxes.

3. Which projects, if any, would you recommend funding? Briefly explain why.

SOLUTION

21-16

21-17

SOLUTION EXHIBIT 21-22

21-18

21-23 (25–30 min.) DCF, accrual accounting rate of return, working capital, evaluation of

performance, no income taxes.

Century Lab plans to purchase a new centrifuge machine for its New Hampshire facility. The

machine costs $137,500 and is expected to have a useful life of 8 years, with a terminal disposal

value of $37,500. Savings in cash operating costs are expected to be $31,250 per year. However,

additional working capital is needed to keep the machine running efficiently. The working

capital must continually be replaced, so an investment of $10,000 needs to be maintained at all

times, but this investment is fully recoverable (will be “cashed in”) at the end of the useful life.

Century Lab’s required rate of return is 14%. Ignore income taxes in your analysis. Assume all

cash flows occur at year-end except for initial investment amounts. Century Lab uses straight–

line depreciation for its machines.

Required:

1. Calculate net present value.

2. Calculate internal rate of return.

3. Calculate accrual accounting rate of return based on net initial investment.

4. Calculate accrual accounting rate of return based on average investment.

5. You have the authority to make the purchase decision. Why might you be reluctant to base

your decision on the DCF methods?

SOLUTION

21-19

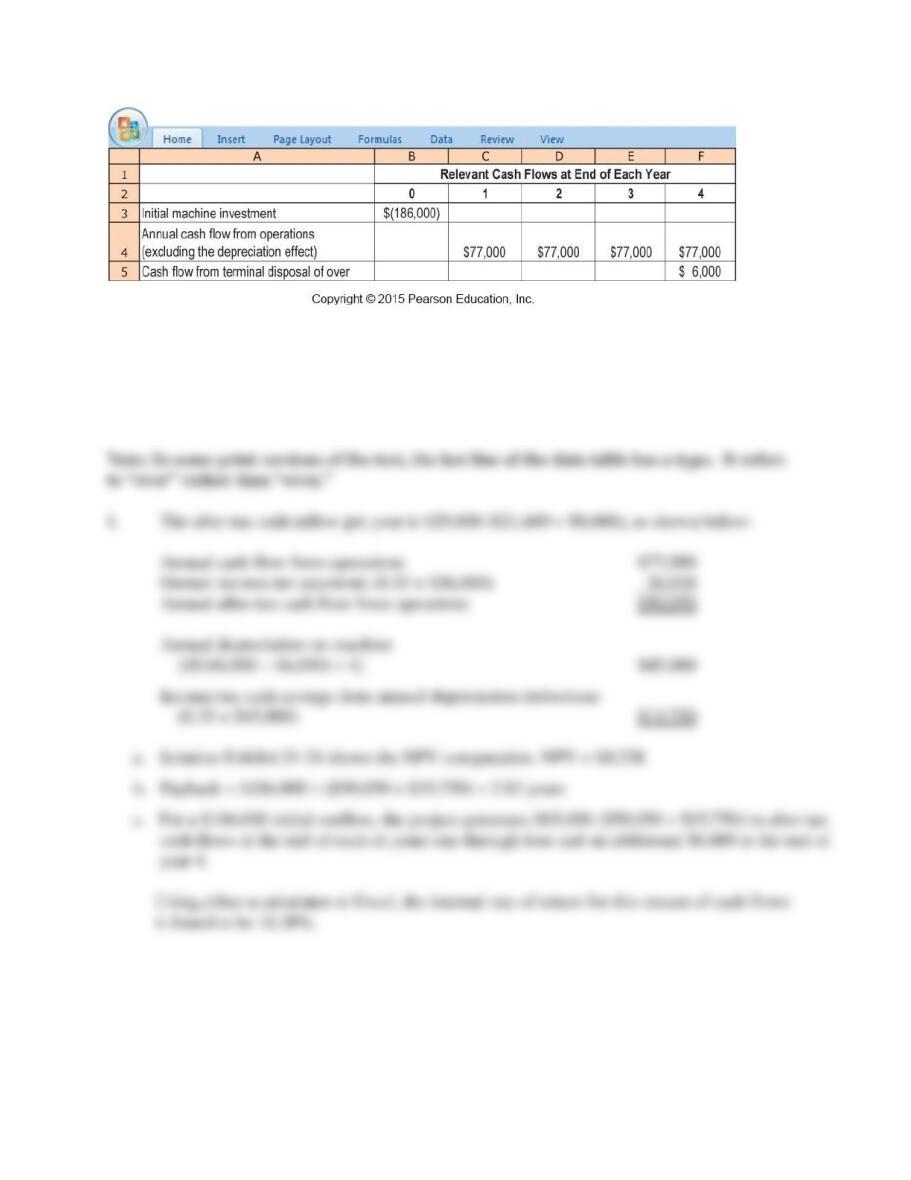

21-24 (40 min.) New equipment purchase, income taxes.

Ella’s Bakery plans to purchase a new oven for its store. The oven has an estimated useful life of

4 years. The estimated pretax cash flows for the oven are as shown in the table that follows, with

no anticipated change in working capital. Ella’s Bakery has a 14% after-tax required rate of

return and a 35% income tax rate. Assume depreciation is calculated on a straight-line basis for

tax purposes using the initial oven investment and estimated terminal disposal value of the oven.

Assume all cash flows occur at year-end except for initial investment amounts.

21-20

Required:

1. Calculate (a) net present value, (b) payback period, and (c) internal rate of return.

2. Calculate accrual accounting rate of return based on net initial investment.

SOLUTION