Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1. a. Under absorption costing, both variable and fixed manufacturing costs are included as a

p

art of the cost of the product manufactured.

4. In the variable costing income statement, the fixed manufacturing costs and the fixed

5. All costs are controllable by someone within the business but not necessarily by the same

6. In the short run, income from operations is maximized if the revenue from the sale of the

7. Product profitability analysis can be used by management to set product prices, to emphasize

8. Rewarding sales personnel on the basis of total sales will normally motivate the sales staff

to expend their efforts promoting high-volume products, which will produce a large total

9. A change in contribution margin can be attributed to a change in the following factors as

they affect sales and/or variable costs: (1) quantity factor—the effect of a difference in the

CHAPTER 20 (FIN MAN); CHAPTER 5 (MAN)

V

ARIABLE COSTING FOR MANAGEMENT ANALYSIS

DISCUSSION QUESTIONS

CHAPTER 20 Variable Costing for Management Analysis

PE 20–1A (FIN MAN); PE 5–1A (MAN)

PE 20–1B (FIN MAN); PE 5–1B (MAN)

PE 20–2A (FIN MAN); PE 5–2A (MAN)

a. Variable costing income from operations is less than absorption costing

PE 20–2B (FIN MAN); PE 5–2B (MAN)

a. Variable costing income from operations is less than absorption costing

PE 20–3A (FIN MAN); PE 5–3A (MAN)

a. Variable costing income from operations is greater than absorption costing

PE 20–3B (FIN MAN); PE 5–3B (MAN)

a. Variable costing income from operations is greater than absorption costing

PRACTICE EXERCISES

CHAPTER 20 Variable Costing for Management Analysis

PE 20–4A (FIN MAN); PE 5–4A (MAN)

a. $15,000 greater in producing 15,000 units. 12,000 units × (6.25* – 5.00**),

PE 20–4B (FIN MAN); PE 5–4B (MAN)

a. $52,500 greater in producing 15,000 units. 10,000 units × (15.75* – 10.50**),

PE 20–5A (FIN MAN); PE 5–5A (MAN)

PE 20–5B (FIN MAN); PE 5–5B (MAN)

PE 20–6A (FIN MAN); PE 5–6A (MAN)

PE 20–6B (FIN MAN); PE 5–6B (MAN)

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–1 (FIN MAN); Ex. 5–1 (MAN)

a. The inventory valuation under the absorption costing concept would include

the fixed factory overhead cost, as follows:

b. The inventory valuation under the variable costing concept would not include

the fixed factory overhead cost, as follows:

EXERCISES

CHAPTER 20 Variable Costing for Management Analysis

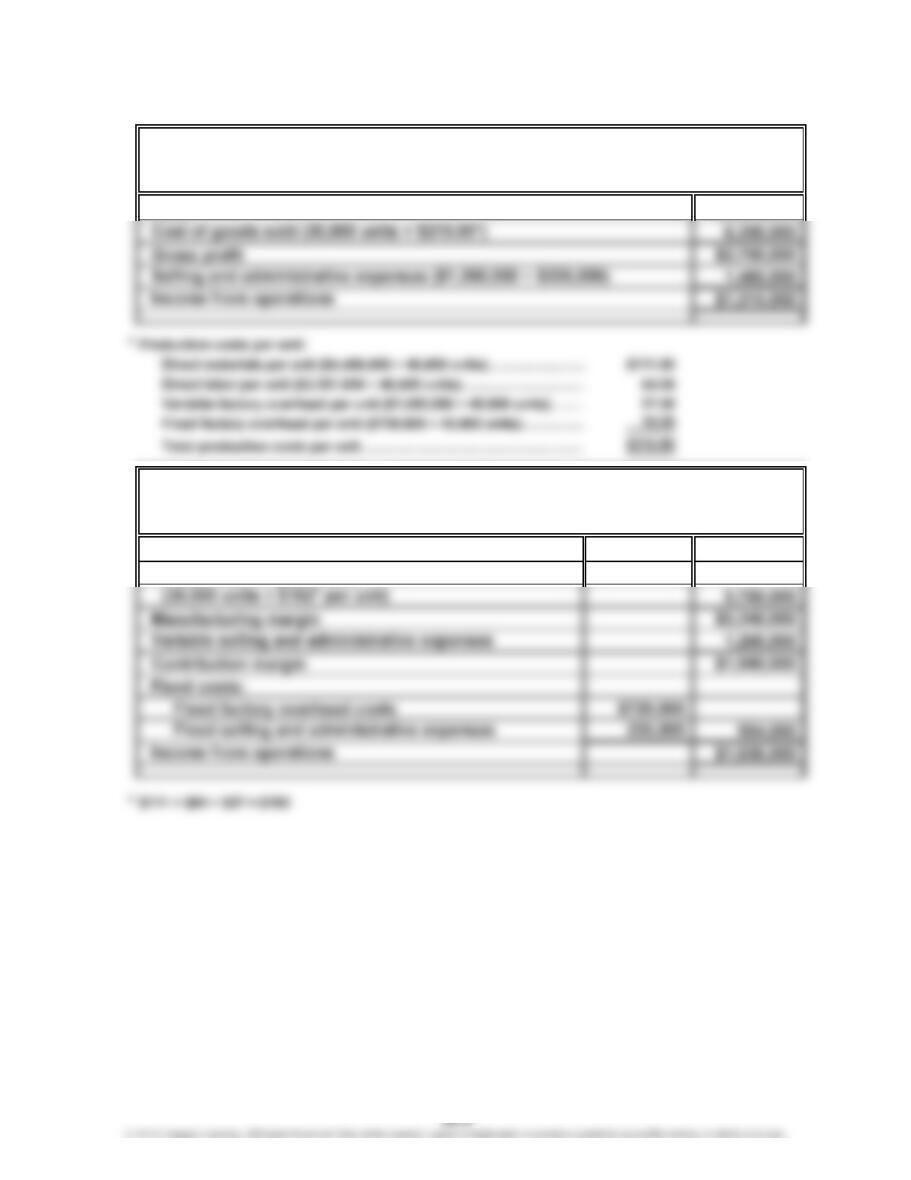

Ex. 20–2 (FIN MAN); Ex. 5–2 (MAN)

a.

Sales $9,000,000

b.

Sales $9,000,000

Variable cost of goods sold

Variable Costing Income Statement

For the Month Ended July 31, 2014

BEACH MOTORS INC.

Absorption Costing Income Statement

For the Month Ended July 31, 2014

BEACH MOTORS INC.

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–2 (FIN MAN); Ex. 5–2 (MAN) (Concluded)

c. The difference between the absorption and variable costing income from operations

of $189,000 ($1,215,000 – $1,026,000) can be explained as follows:

Increase in inventory………………………………………………………………

…

10,500

CHAPTER 20 Variable Costing for Management Analysis

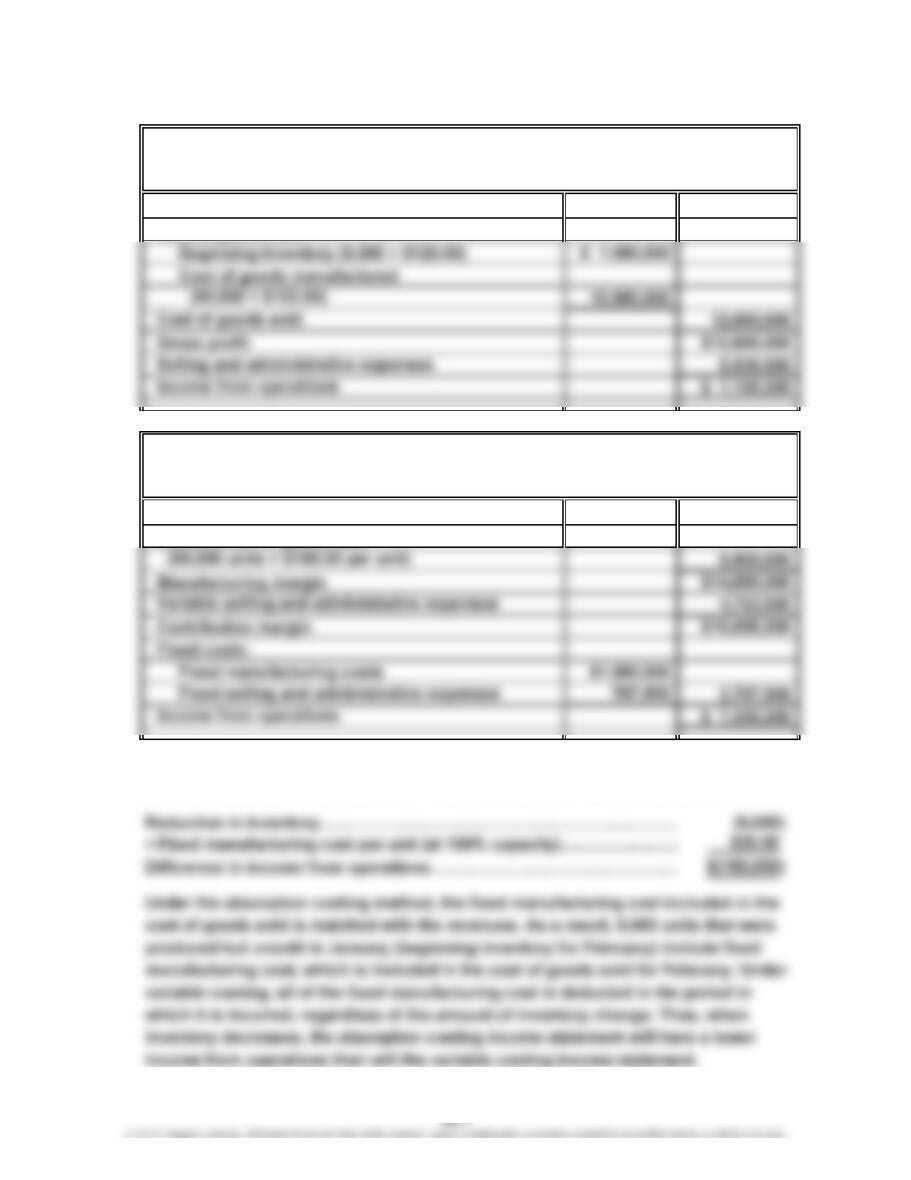

Ex. 20–3 (FIN MAN); Ex. 5–3 (MAN)

a.

Sales $24,750,000

Cost of goods sold:

b.

Sales $24,750,000

Variable cost of goods sold

c. The difference between the absorption and variable costing income from

operations of −$180,000 ($7,150,500 − $7,330,500) can be explained as follows:

Variable Costing Income Statement

For the Month Ended February 28, 2014

EKIN INC.

Absorption Costing Income Statement

For the Month Ended February 28, 2014

EKIN INC.

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–4 (FIN MAN); Ex. 5–4 (MAN)

Ex. 20–5 (FIN MAN); Ex. 5–5 (MAN)

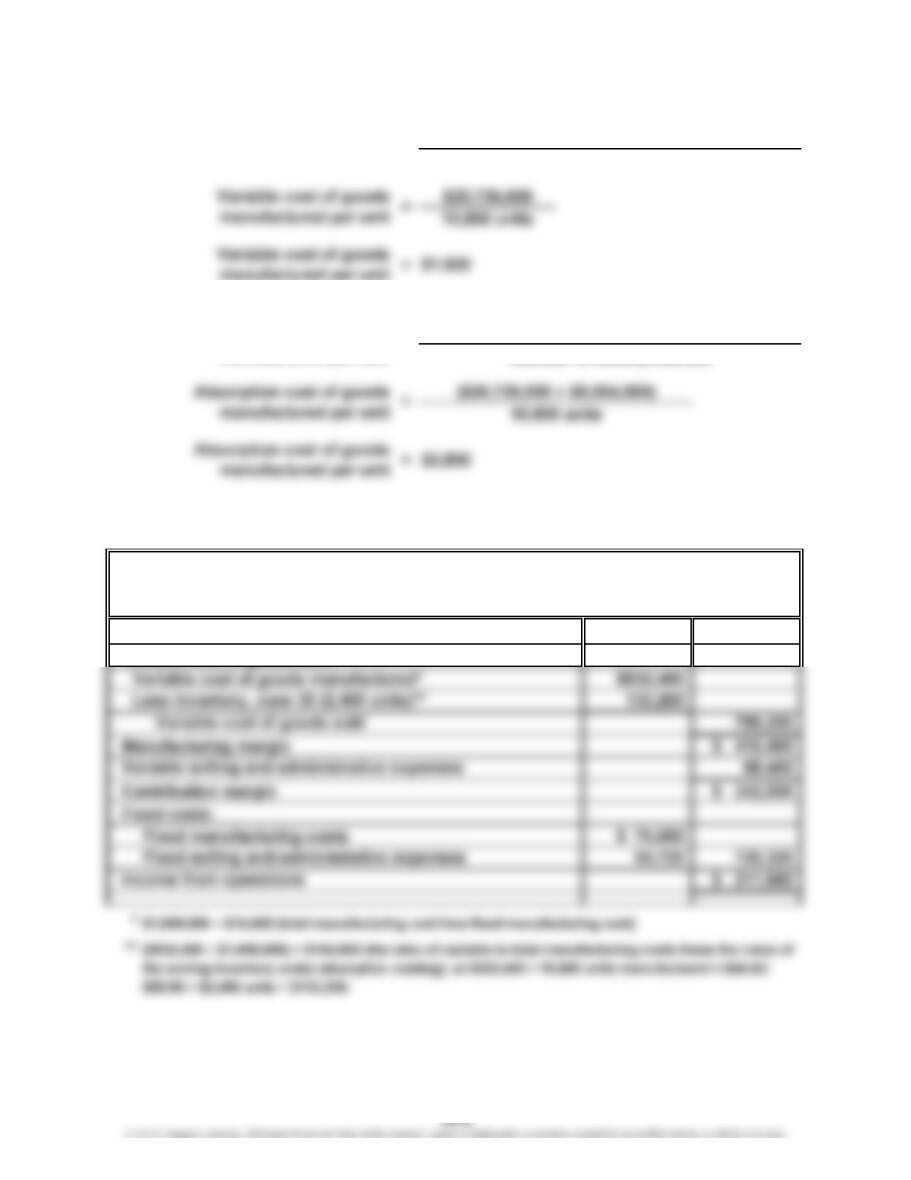

Sales (14,400 units) $1,209,600

Variable cost of goods sold:

=

Absorption cost of goods

manufactured per unit

Number of units produced

For the Month Ended June 30, 2015

b.

HAMAN COMPANY

Variable Costing Income Statement

(variable + fixed)

Number of units produced

a. Variable cost of goods

manufactured per unit =

manufactured per unit =

Variable cost of goods manufactured

Total cost of goods manufactured

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–6 (FIN MAN); Ex. 5–6 (MAN)

Sales (45,000 units) $6,750,000

Cost of goods sold:

Ex. 20–7 (FIN MAN); Ex. 5–7 (MAN)

a.

Net sales $82,559

Variable cost of products sold 22,830

Variable Costing Income Statement (assumed)

(in millions)

COVELLI EQUIPMENT COMPANY

Absorption Costing Income Statement

For the Month Ended July 31, 2014

PROCTER & GAMBLE COMPANY

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–8 (FIN MAN); Ex. 5–8 (MAN)

a. 1.

28,800 Units 36,000 Units

Manufactured Manufactured

Sales $2,160,000 $2,160,000

Cost of goods sold:

*Unit cost of goods manufactured:

Direct materials ($1,324,800 ÷ 28,800)……………………………

…

$46.00

Direct labor ($316,800 ÷ 28,800)…………………………………… 11.00

For the Month Ending July 31, 2014

Absorption Costing Income Statement

MUZENSKI INDUSTRIES INC.

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–8 (FIN MAN); Ex. 5–8 (MAN) (Concluded)

2.

28,800 Units 36,000 Units

Manufactured Manufactured

Sales $2,160,000 $2,160,000

Variable cost of goods sold:

Variable cost of goods manufactured:

*Unit variable cost of goods manufactured:

Direct materials ($1,324,800 ÷ 28,800)……………………………

…

$46.00

b. If 36,000 units rather than 28,800 units are manufactured, the increase in income

from operations of $43,200 ($136,700 – $93,500) under absorption costing is caused

For the Month Ending July 31, 2014

Variable Costing Income Statement

MUZENSKI INDUSTRIES INC.

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–9 (FIN MAN); Ex. 5–9 (MAN)

a.

Sales $18,666

Variable cost of goods sold:

Beginning inventory (70% × $2,792) $ 1,954

*Variable cost of goods manufactured:

Cost of goods sold………………………………………………………

…

$16,089

Plus: Ending inventory…………………………………………………

…

2,354

Variable Costing Income Statement (assumed)

(in millions)

WHIRLPOOL CORPORATION

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–9 (FIN MAN); Ex. 5–9 (MAN) (Concluded)

b. The income from operations under the variable costing concept will not be the same

as the income from operations under the absorption costing concept when the

inventories either increase or decrease during the year. In this case, Whirlpool’s

inventory decreased, meaning it sold more than it produced. As a result, the income

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–10 (FIN MAN); Ex. 5–10 (MAN)

a. Management’s decision and conclusion are incorrect. The profit will not be improved

by $114,000 because the fixed costs used in manufacturing and selling running shoes

b.

Basketball Cross Training Running

Shoes Shoes Shoes

Revenues $696,000 $588,000 $ 504,000

Variable cost of goods sold 252,000 210,000 240,000

c. If the running shoe line were eliminated, then the contribution margin of the product

line also would be eliminated. The fixed costs would not be eliminated. Thus, the

KOBEER, INC

Variable Costing Income Statements—Three Product Lines

For the Year Ended December 31, 2014

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–11 (FIN MAN); Ex. 5–11 (MAN)

Silent

No Noise Candy

Headphone Headphone

Unit volume increase………………………………………………

…

35,700 39,600

Ex. 20–12 (FIN MAN); Ex. 5–12 (MAN)

a.

Revenues

$12,600,000 $5,720,000

SNOW MOTOR SPORTS INC.

Contribution Margin by Product

ARCTIC CAT

CHAPTER 20 Variable Costing for Management Analysis

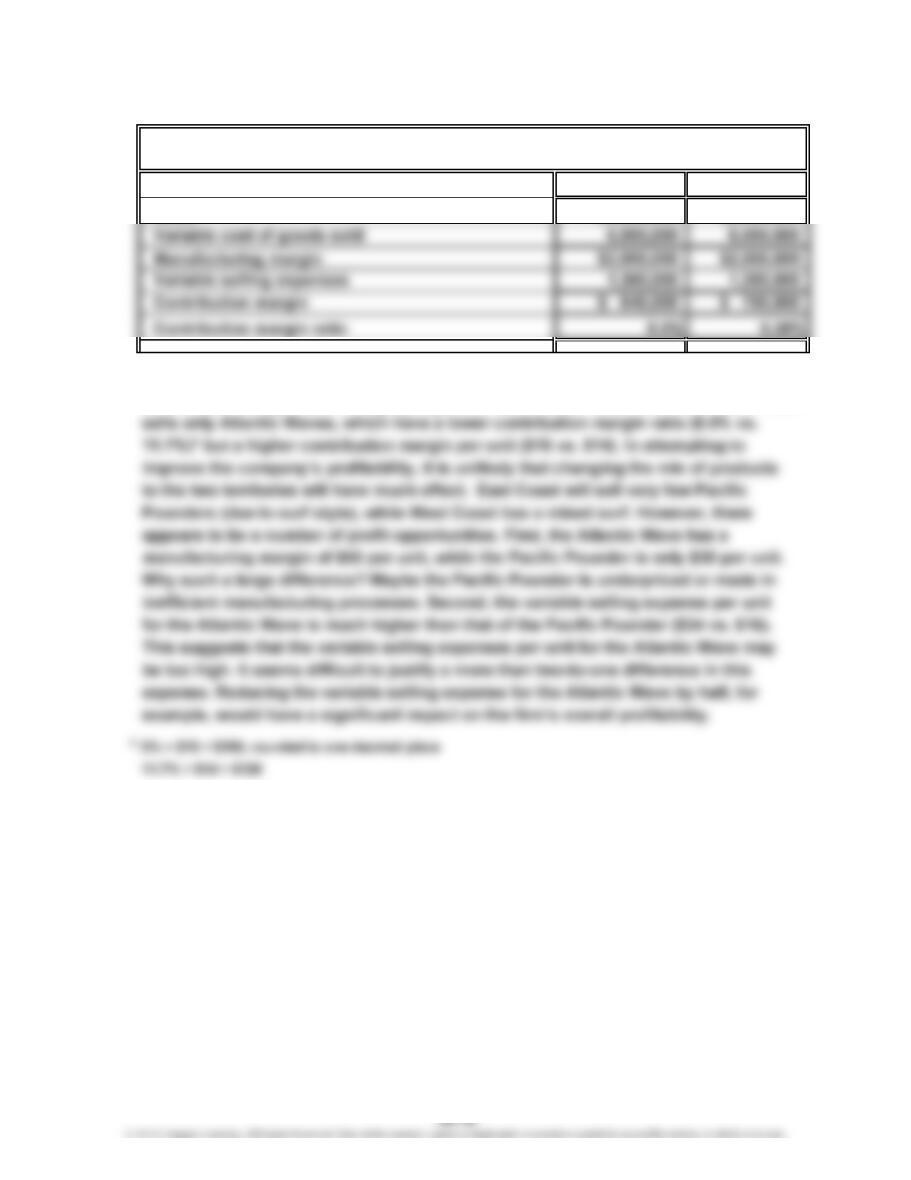

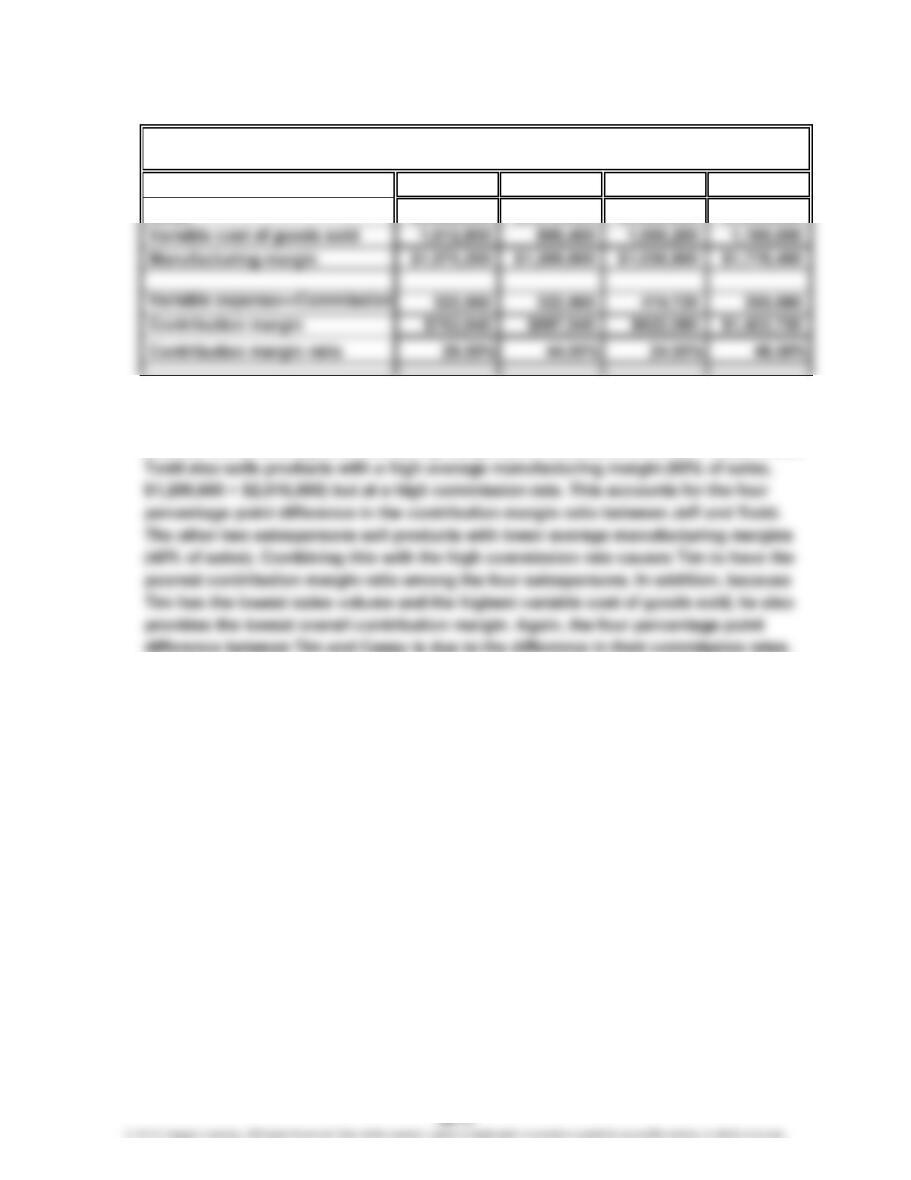

Ex. 20–13 (FIN MAN); Ex. 5–13 (MAN)

a.

Sales

b. The total contribution margin is slightly lower for the East Coast, while the

contribution margin ratio is slightly higher for West Coast. This is because East Coast

COAST TO COAST SURFBOARDS INC.

Contribution Margin by Territory

East Coast West Coast

$8,000,000 $8,000,000

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–14 (FIN MAN); Ex. 5–14 (MAN)

a. 1.

Cassy G. Todd Tim Jeff

Sales $2,688,000 $2,016,000 $2,592,000 $2,964,000

2. Jeff earns the highest contribution margin and has the highest contribution margin

ratio. This is because he sells the most units, has a low commission rate, and sells a

product mix with a high manufacturing margin (60% of sales, $1,778,400 ÷ $2,964,000).

REYES INDUSTRIES INC.

Contribution Margin by Salesperson

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–14 (FIN MAN); Ex. 5–14 (MAN) (Concluded)

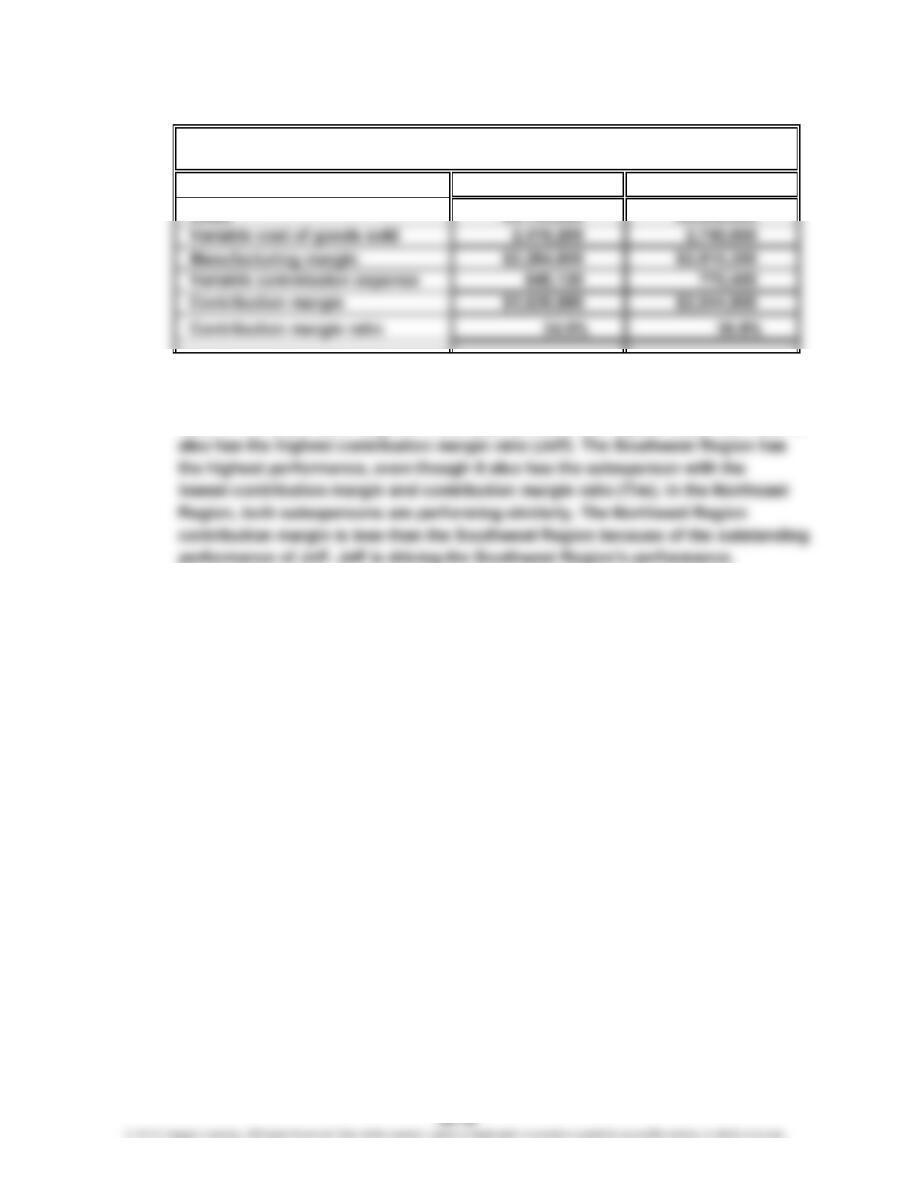

b. 1.

Sales

2. The Southwest Region has $852,000 more sales and $405,120 more contribution

margin. In addition, the Southwest Region has the largest contribution margin

ratio. In the Southwest Region, the salesperson with the highest sales unit volume

$5,556,000

REYES INDUSTRIES INC.

Contribution Margin by Territory

Northeast Southwest

$4,704,000

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–15 (FIN MAN); Ex. 5–15 (MAN)

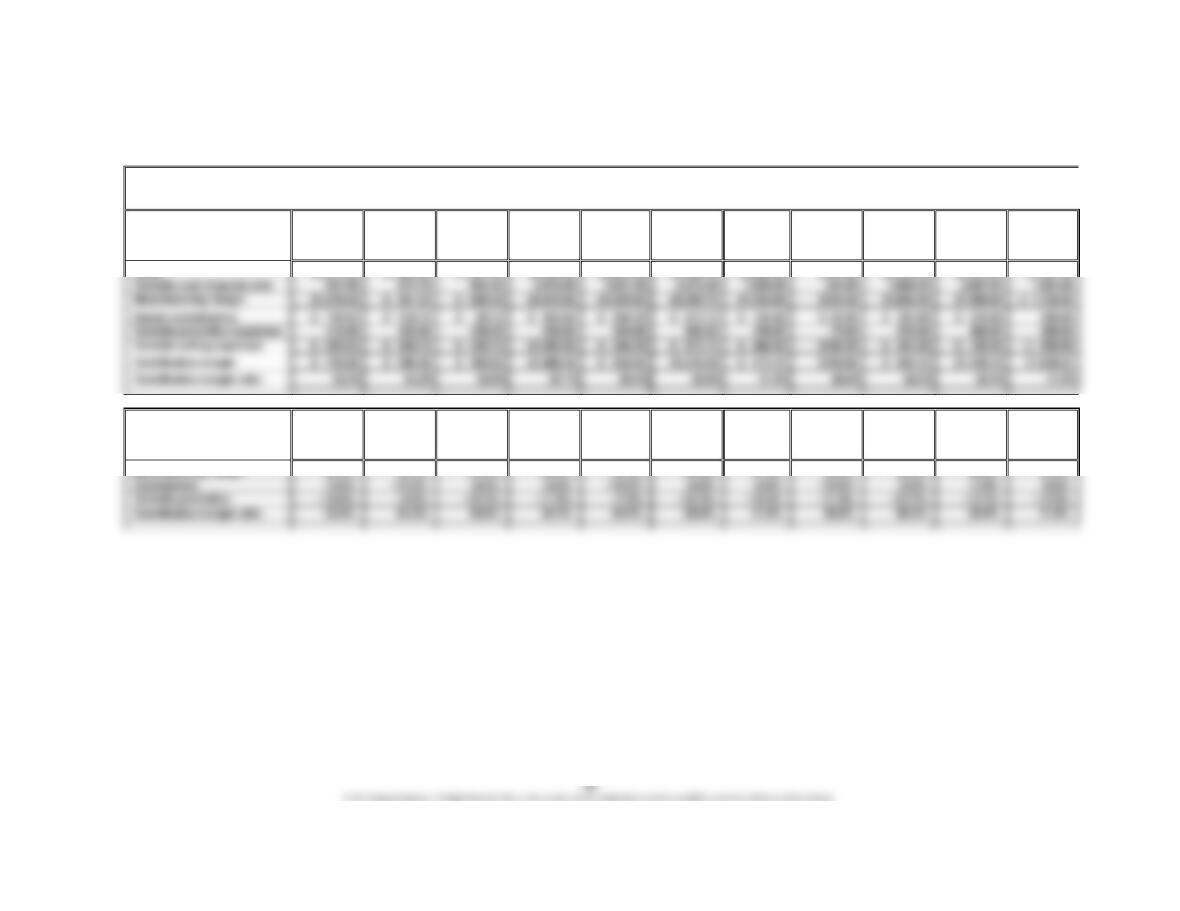

a.

Building Large Marine &

Construction Core Electric Power Petroleum

Products Cat Japan Components Earthmoving Power Excavation Systems Logistics Power Mining Turbines

Sales $2,217.00 $1,225.00 $1,234.00 $5,045.00 $2,847.00 $4,562.00 $2,885.00 $659.00 $2,132.00 $3,975.00 $3,321.00

b.

Building Large Marine &

Construction Core Electric Power Petroleum

Products Cat Japan Components Earthmoving Power Excavation Systems Logistics Power Mining Turbines

Manufacturing margin 55.0% 45.0% 51.0% 49.0% 46.0% 48.0% 47.0% 50.0% 50.0% 48.0% 52.0%

CATERPILLAR, INC.

Contribution Margin by Segment (assumed)

(in millions, except ratio figures)

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–15 (FIN MAN); Ex. 5–15 (MAN) (Concluded)

c. The Building Construction Products segment has the highest contribution margin

ratio. The manufacturing margin is high, while the dealer commission rate is average.