Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 20

Job Order Costing

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe cost systems and

the flow of costs in a job

order system.

1, 2, 3, 4, 5,

6, 7, 8

1, 2

1

1, 2, 3, 4, 6,

7, 8, 9, 11

1A, 2A, 3A,

5A

2. Use a job cost sheet to

assign costs to work in

process.

9, 10, 11, 12

3, 4, 5

2

1, 2, 3, 6, 7,

8, 10, 12

1A, 2A, 3A,

5A

3. Demonstrate how to

determine and use the

predetermined overhead

rate.

13, 14, 15

6, 7

3

2, 3, 5, 6, 7,

8, 11, 12, 13

1A, 2A, 3A,

4A, 5A

4. Prepare entries for

manufacturing and service

jobs completed and sold.

16

8, 9

4

2, 3, 6, 7, 8,

10, 11, 12

1A, 2A, 3A,

5A

5. Distinguish between under-

and overapplied

manufacturing overhead.

17, 18

10

5

4, 5, 9, 13

1A, 2A, 3A,

4A, 5A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare entries in a job order cost system and job cost

sheets.

Simple

30 40

2A

Prepare entries in a job order cost system and partial

income statement.

Moderate

30 40

3A

Prepare entries in a job order cost system and cost of

goods manufactured schedule.

Simple

30 40

4A

Compute predetermined overhead rates, apply overhead,

and calculate under- or overapplied overhead.

Simple

20 30

5A

Analyze manufacturing accounts and determine missing

amounts.

Complex

30 40

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End-of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Describe cost systems and the

flow of costs in a job order

system.

Q20-5

Q20-7

Q20-8

Q20-1 Q20-4

Q20-2 Q20-6

Q20-3 BE20-1

BE20-2

DI20-1

E20-1

E20-2

E20-3

E20-6

E20-7

E20-8

E20-9

E20-11

P20-1A

P20-3A

E20-4

P20-2A

P20-5A

2. Use a job cost sheet to assign

costs to work in process.

Q20-11

Q20-12

Q20-9

Q20-10

BE20-3

BE20-4

BE20-5

DI20-2

E20-1

E20-2

E20-3

E20-6

E20-7

E20-8

E20-10

E20-12

P20-1A

P20-3A

P20-2A

P20-5A

3. Demonstrate how to determine

and use the predetermined

overhead rate.

Q20-15

Q20-13

Q20-14

BE20-6

BE20-7

DI20-3

E20-2

E20-3

E20-6

E20-7

E20-8

E20-11

E20-12

E20-13

P20-1A

P20-3A

P20-4A

E20-5

P20-2A

P20-5A

4. Prepare entries for

manufacturing and service jobs

completed and sold.

Q20-16

BE20-9

BE20-8

DI20-4

E20-2

E20-3

E20-6

E20-7

E20-8

E20-10

E20-11

E20-12

P20-1A

P20-3A

P20-2A

P20-5A

5. Distinguish between under- and

overapplied manufacturing

overhead.

Q20-17

Q20-18

E20-9

BE20-10

E20-13

P20-1A

P20-3A

P20-4A

DI20-5

E20-4

E20-5

P20-2A

P20-5A

Broadening Your Perspective

BYP20-3

BYP20-4

CD20

BYP20-2

BYP20-1

BYP20-5

BYP20-6

BYP20-7

ANSWERS TO QUESTIONS

1. (a) Cost accounting involves the measuring, recording, and reporting of product costs. A cost

accounting system consists of manufacturing cost accounts that are fully integrated into the

2. (a) The two principal types of cost accounting systems are: (1) job order cost system and

(2) process cost system. Under a job order cost system, costs are assigned to each job or

batch of goods; at all times each job or batch of goods can be separately identified. A job

order cost system measures costs for each completed job, rather than for set time periods.

3. A job order cost system is most likely to be used by a company that receives special orders, or

custom builds, or produces heterogeneous items or products; that is, the product manufactured or

4. A process cost system is most likely to be used by manufacturing firms with continuous production

flows usually found in mass production, assembly line, large-volume, uniform, or relatively similar

product industries. Companies producing appliances, chemicals, pharmaceuticals, rubber and tires,

plastics, cement, petroleum, and automobiles utilize process cost systems.

5. The major steps in the flow of costs in a job order cost system are: (1) accumulating the manufacturing

costs incurred and (2) assigning the accumulated costs to work done.

6. The three inventory control accounts and their subsidiary ledgers are:

7. The source documents used in accumulating direct labor costs are time tickets and time cards.

8. Disagree. Entries to Manufacturing Overhead are also made at the end of an accounting period.

For example, there will be adjusting entries for factory depreciation, property taxes, and insurance.

Copyright © 2015 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 12/e, Solutions Manual (For Instructor Use Only) 20-5

Questions Chapter 20 (Continued)

10. The purpose of a job cost sheet is to record the costs chargeable to a specific job and to determine

the total and unit costs of the completed job.

11. The source documents for charging costs to specific jobs are materials requisition slips for direct

materials, time tickets for direct labor, and the predetermined overhead rate for manufacturing

overhead.

14. The relationships for computing the predetermined overhead rate are the estimated annual overhead

costs and an expected activity base such as direct labor hours. The rate is computed by dividing

the estimated annual overhead costs by the expected annual operating activity.

15. At any point in time, the balance in Work in Process Inventory should equal the sum of the costs

shown on the job cost sheets of unfinished jobs. Alternatively, posting to Work in Process Inventory

may be compared with the sum of the postings to the job cost sheets for each of the manufacturing

cost elements.

SOLUTIONS TO BRIEF EXERCISES

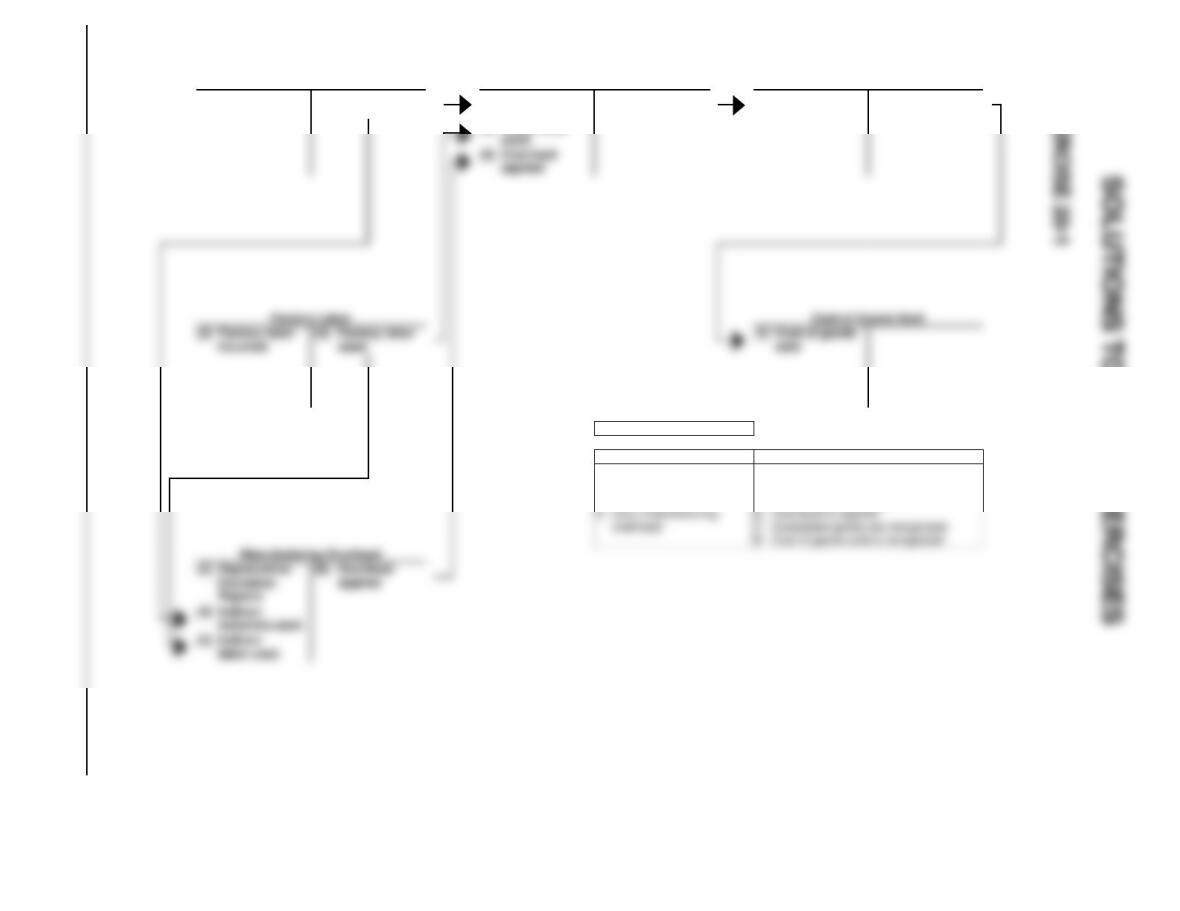

BRIEF EXERCISE 20-1

20-6

Raw Materials Inventory

Work in Process Inventory

Finished Goods Inventory

(1) Purchases

(4) Materials

used

(4) Direct

materials used

(7) Cost of com-

pleted jobs

(7) Cost of com-

pleted jobs

(8) Cost of goods

sold

(5) Direct labor

used

(6) Overhead

applied

Key to Entries:

Accumulation

Assignment

1. Purchase raw materials

4. Raw materials are used

2. Incur factory labor

5. Factory labor is assigned

BRIEF EXERCISE 20-2

Jan. 31 Raw Materials Inventory ...................................... 4,000

Accounts Payable ......................................... 4,000

31 Factory Labor ....................................................... 6,000

BRIEF EXERCISE 20-3

BRIEF EXERCISE 20-4

Jan. 31 Work in Process Inventory .................................. 5,200

BRIEF EXERCISE 20-5

Job 1

Job 2

Date

Direct

Materials

Direct

Labor

Date

Direct

Materials

Direct

Labor

1/31

900

1/31

1,200

BRIEF EXERCISE 20-6

Overhead rate per direct labor cost is 180%, or ($900,000 ÷ $500,000).

BRIEF EXERCISE 20-7

Jan. 31 Work in Process Inventory ............................. 28,000

BRIEF EXERCISE 20-8

Mar. 31 Finished Goods Inventory .............................. 50,000

Work in Process Inventory ...................... 50,000

BRIEF EXERCISE 20-9

Service Contracts in Process ......................... 28,000

Operating Overhead ........................................ 8,000

Service Salaries and Wages ................... 36,000

BRIEF EXERCISE 20-10

Shimeca Company

Dec. 31 Cost of Goods Sold ......................................... 1,200

Manufacturing Overhead ........................ 1,200

Garcia Company

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 20-1

(a) Raw Materials Inventory ............................................ 18,000

Accounts Payable ............................................... 18,000

(Purchases of raw materials on account)

DO IT! 20-2

The three summary entries are:

Work in Process Inventory ($7,200 + $9,000) .................. 16,200

Raw Materials Inventory ............................................ 16,200

(To assign materials to jobs)

DO IT! 20-3

The predetermined overhead for Washburn Company is:

$200,000 2,500 hours = $80.00

DO IT! 20-4

Finished Goods Inventory ................................................ 120,000

Work in Process Inventory ........................................ 120,000

(To record completion of Job 310, costing

$70,000 and Job 312, costing $50,000)

DO IT! 20-5

Manufacturing overhead applied = 130% X $85,000 = $110,500

Underapplied manufacturing overhead = $115,000 – $110,500 = $4,500

SOLUTIONS TO EXERCISES

EXERCISE 20-1

(a) Factory Labor .......................................................... 90,000

Factory Wages Payable .................................. 76,000

Employer Payroll Taxes Payable .................... 8,000

EXERCISE 20-2

(a) May 31 Work in Process Inventory .................... 10,400

Manufacturing Overhead ....................... 800

Raw Materials Inventory ................ 11,200

31 Work in Process Inventory .................... 12,500

(b)

Work in Process Inventory

May 1 Balance 3,500

31 10,400

May 31 7,540

EXERCISE 20-2 (Continued)

Job Cost Sheets

Job

No.

Beginning Work

in Process

Direct

Material

Direct

Labor

Manufacturing*

Overhead

Total

430

$1,500

$3,500

$ 3,000

$1,800

$ 9,800

EXERCISE 20-3

(a) (1) $15,200, or ($5,000 + $6,000 + $4,200).

(b) Jan. 31 Work in Process Inventory ...................... 8,000

Raw Materials Inventory ................... 8,000

31 Work in Process Inventory ...................... 12,000

Factory Labor .................................... 12,000

EXERCISE 20-4

(a) + $50,000 + $42,500 = $145,650

(a) = $53,150

EXERCISE 20-4 (Continued)

[Note: The instructions indicate that manufacturing overhead is applied on the

basis of direct labor cost, and the rate is the same in all cases. From Case A,

a student should note the overhead rate to be 85%, or ($42,500 ÷ $50,000).]

(d) = .85 X $140,000

(d) = $119,000

[Note: (h) and (i) are solved together.]

(i) = .85(h)

(j) = $213,000 + $18,000

(j) = $231,000

EXERCISE 20-5

(a) $2.40 per machine hour ($300,000 ÷ 125,000 MH).

EXERCISE 20-6

(a) (1) The source documents are:

Direct materials—Materials requisition slips.

(2) The predetermined overhead rate is 125% of direct labor cost. For

example, on July 15, the computation is $550 ÷ $440 = 125%. The

same result is obtained on July 22 and 31.

(3) The total cost is:

Direct materials ............................................................ $4,700

(b) July 31 Finished Goods Inventory ............................ 7,760

Work in Process Inventory ................... 7,760

EXERCISE 20-7

1. Raw Materials Inventory ................................................ 46,300

Accounts Payable .................................................. 46,300

EXERCISE 20-7 (Continued)

5. Manufacturing Overhead ....................................... 80,500

Accounts Payable .......................................... 80,500

6. Depreciation Expense ........................................... 8,100

Accumulated Depreciation—Building ........... 8,100

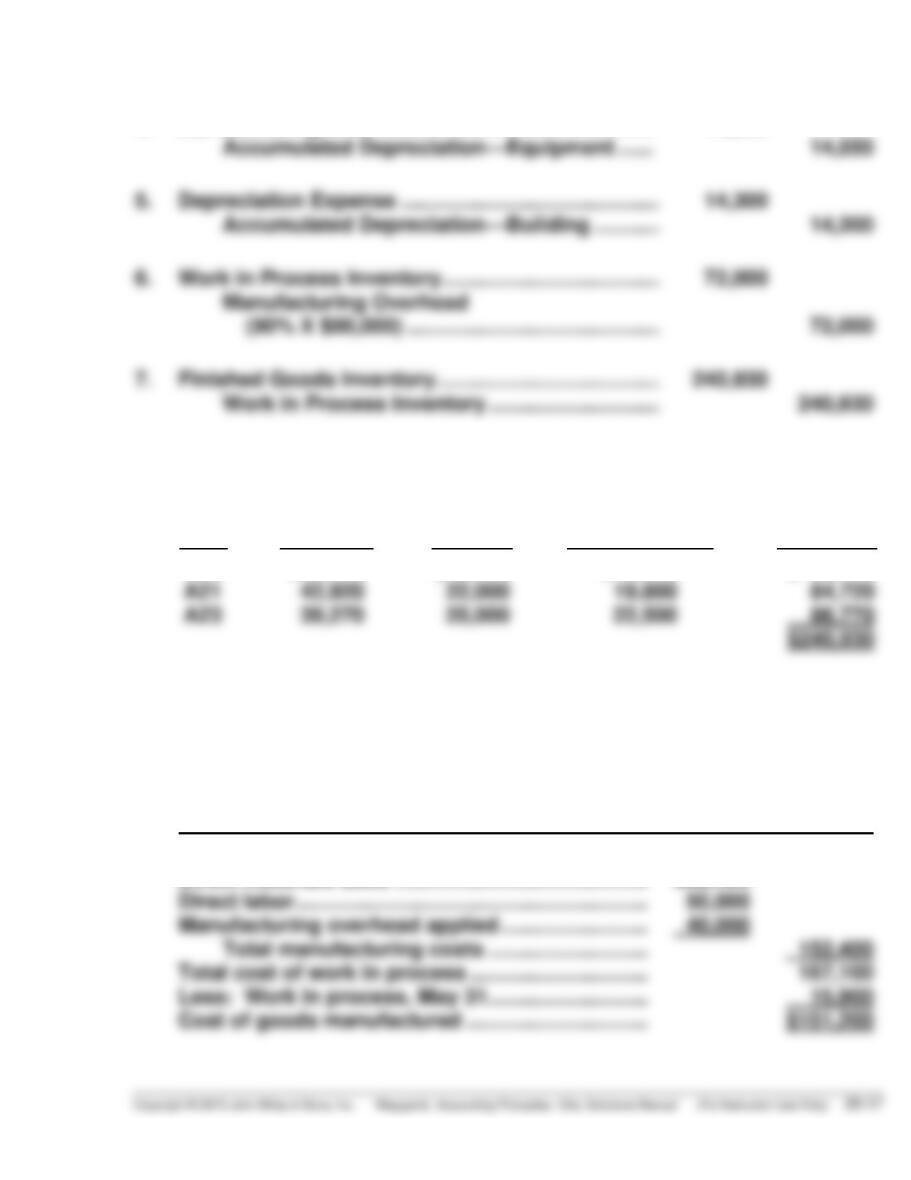

EXERCISE 20-8

1. Raw Materials Inventory ........................................ 192,000

Accounts Payable .......................................... 192,000

Factory Labor ......................................................... 87,300

Factory Wages Payable ................................. 87,300

EXERCISE 20-8 (Continued)

4. Manufacturing Overhead ....................................... 14,550

Accumulated Depreciation—Equipment ...... 14,550

5. Depreciation Expense ............................................ 14,300

Accumulated Depreciation—Building ........... 14,300

Computation of cost of jobs finished:

Job

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Total

A20

$35,240

$18,000

$16,200

$ 69,440

EXERCISE 20-9

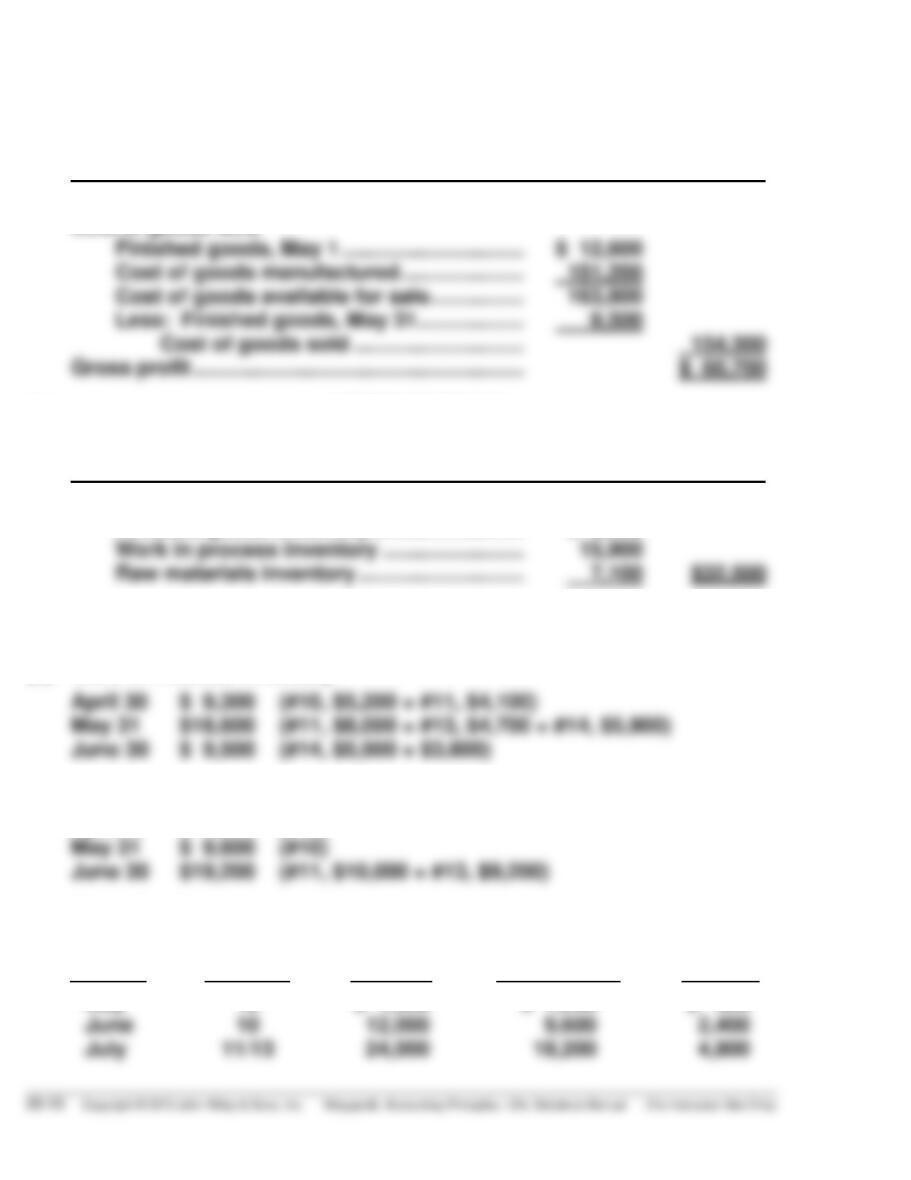

(a) LOPEZ COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended May 31, 2017

Work in process, May 1 ........................................ $ 14,700

Direct materials used ........................................... $62,400

EXERCISE 20-9 (Continued)

(b) LOPEZ COMPANY

(Partial) Income Statement

For the Month Ended May 31, 2017

Sales revenue ..................................................... $215,000

Cost of goods sold

Finished goods, May 1 ............................... $ 12,600

(c) LOPEZ COMPANY

(Partial) Balance sheet

May 31, 2017

Current assets:

Finished goods inventory .......................... $ 9,500

EXERCISE 20-10

(a) Work in Process Inventory

April 30 $ 9,300 (#10, $5,200 + #11, $4,100)

(b) Finished Goods Inventory

April 30 $ 1,200 (#12)

(c) Gross Profit

Month

Job

Number

Sales

Cost of

Goods Sold

Gross

Profit

May

12

$ 1,500

$ 1,200

$ 300

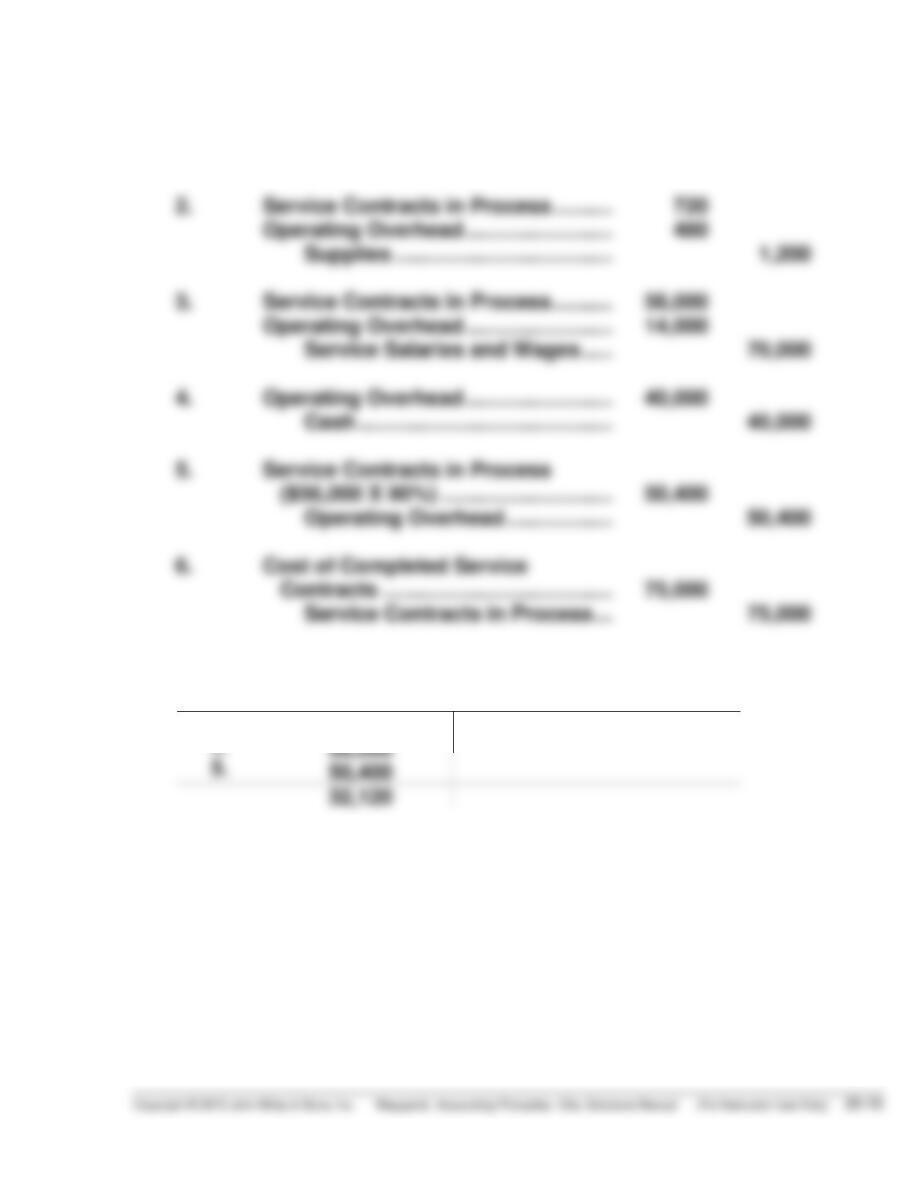

EXERCISE 20-11

(a)

1.

Supplies ............................................

1,800

Accounts Payable .....................

1,800

2.

Service Contracts in Process ..........

720

Operating Overhead .........................

480

Supplies .....................................

1,200

5.

Service Contracts in Process

($56,000 X 90%) .............................

50,400

Operating Overhead ..................

50,400

6.

Cost of Completed Service

Contracts .......................................

75,000

Service Contracts in Process ...

75,000

(b)

Service Contracts in Process

2.

720

75,000

6.

3.

EXERCISE 20-12

(a)

Lynn

Brian

Mike

Direct materials

$ 600

$ 400

$ 200

Auditor labor costs

5,400

6,600

3,375

(b) The Lynn job is the only incomplete job, therefore, $9,600.

(c) Actual overhead

$11,000 (DR)

EXERCISE 20-13

(a) Predetermined overhead rate = Estimated overhead ÷ Estimated

decorator hours

(b) Service Contracts in Process (40,500 hrs X $24) .....

972,000

Operating Overhead .....................................

972,000