CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–16 (FIN MAN); Ex. 5–16 (MAN)

a. Filmed

Entertainment Networks Publishing

Revenues……………………………

…

$14,204.0 $12,018.0 $3,436.0

V

ariable costs………………………

…

4,971.4 3,845.8 2,473.9

Contribution margin………………

…

$ 9,233 $ 8,172 $ 962

Contribution margin ratio………… 65% 68% 28%

b. The Filmed Entertainment and Networks segments sell an information or media

product that has a very small variable cost per unit. For example, the Networks

segment earns revenue monthly from each customer. However, the variable

cost of each customer is rather small. The cost of providing the service is

essentially fixed. The same holds true for the Filmed Entertainment segment.

The variable cost per ticket sold to a motion picture is rather small. The costs

of producing and promoting a new film are essentially fixed to the number of

c. The higher contribution margin ratios of the Filmed Entertainment and Networks

segments should not be interpreted as being the most profitable. The fixed costs

cannot be ignored. These segments will have high fixed costs. If the volume of

business is not sufficient to exceed the break-even point, then the segments would

20-21

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–17 (FIN MAN); Ex. 5–17 (MAN)

a.

Effect of change in sales:

b. The sales will increase by $31,875. If the variable cost per unit were $10, and

there were 3,750 more units than planned, then the variable cost will increase

by $37,500 due to the variable cost quantity factor. Thus, the contribution margin

will decrease by $5,625 ($37,500 – $31,875) as a result of the price reduction.

Ex. 20–18 (FIN MAN); Ex. 5–18 (MAN)

Effect of change in sales:

Sales quantity factor (38,000 – 41,000) × $200 $(600,000)

BUY BEST INC.

ROMERO PRODUCTS INC.

Contribution Margin Analysis—Sales

For the Year Ended December 31

Contribution Margin Analysis—Sales

For the Year Ended December 31

20-22

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–19 (FIN MAN); Ex. 5–19 (MAN)

Effect of changes in variable costs of goods sold:

Variable cost quantity factor (41,000 – 38,000) × $80 $ 240,000

Unit cost factor ($80 – $92) × 38,000 (456,000)

Total effect of change in variable cost of

ROMERO PRODUCTS INC.

Contribution Margin Analysis—Variable Costs

For the Year Ended December 31

20-23

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–20 (FIN MAN); Ex. 5–20 (MAN)

a.

Atlanta/ Baltimore/ Pittsburgh/

Baltimore Pittsburgh Atlanta Total

Revenues $255,000 $594,000 $542,080 $1,391,080

Variable costs:

Labor costs for loading

Revenues: Revenue per railcar × Number of railcars

Labor costs for loading and unloading railcars: $46.00 × Number of railcars

b. The Atlanta/Baltimore route performs significantly worse than do the other two routes.

A close examination of the operating statistics indicates that this route runs very few

railcars, combined with fairly high total mileage. This combination suggests that the

railroad is running many short trains on the railroad. That is, the railroad’s profitability

ratios of train-miles to railcars, indicating that their train sizes are larger.

Note to Instructors: Part (b) is somewhat subtle but a worthy discussion. The cost

behavior issues discussed in (b) are common in service companies. For example,

large classes in a university are inherently more profitable than small classes, dense

data traffic on a telecommunication system is more profitable than less traffic, full

EAST COAST RAILROAD

For the Month Ended April 30

Contribution Margin by Route

20-24

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–21 (FIN MAN); Ex. 5–21 (MAN)

a.

Revenues ($500 × 700 railcars) $350,000

Labor costs for loading and unloading railcars

($46.00 × 700 railcars) $ 32,200

Fuel costs ($12.40 × 12,835 train-miles) 159,154

b.

Planned contribution margin (from Exercise 20–20) $(29,291)

Effect of change in sales:

Sales quantity factor (700 – 425) × $600 $165,000

Unit price factor ($500 – $600) × 700 (70,000)

Total effect of change in sales 95,000

Contribution Margin Analysis—Atlanta/Baltimore Route

For the Month Ended May 31

EAST COAST RAILROAD

Contribution Margin for Atlanta/Baltimore Route

For the Month Ended May 31

EAST COAST RAILROAD

20-25

CHAPTER 20 Variable Costing for Management Analysis

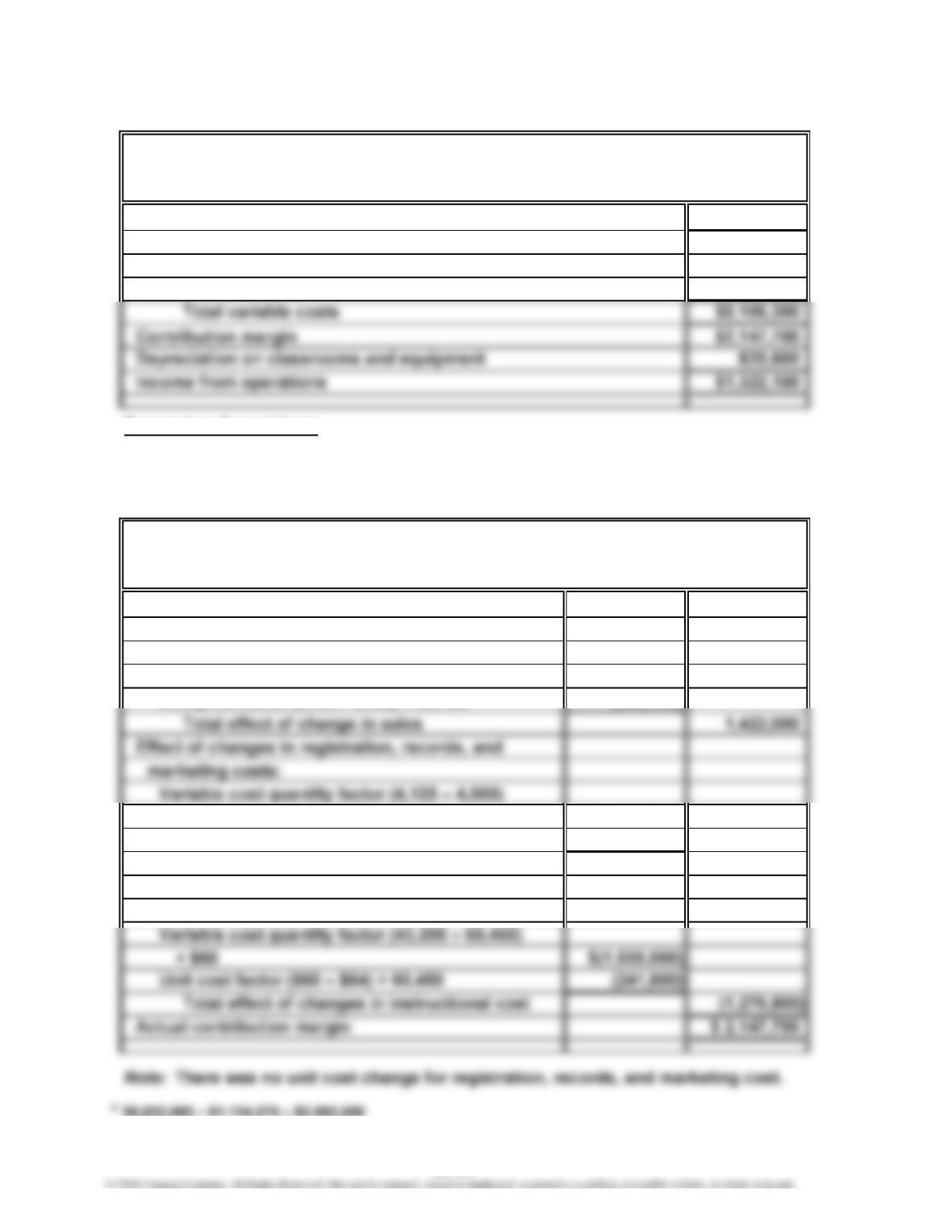

Ex. 20–22 (FIN MAN); Ex. 5–22 (MAN)

a.

Revenue $7,254,000

Variable costs:

Registration, records, and marketing cost $1,237,500

Instructional costs 3,868,800

Supporting Calculations

Revenue: $120 × 60,450 credit hours

Registration, records, and marketing costs: $275 × 4,500 students

Instructional costs: $64 × 60,450 credit hours

b.

Planned contribution margin* $ 2,105,625

Effect of change in revenue:

Revenue quantity factor (60,450 – 43,200)

× $135 $ 2,328,750

Unit price factor ($120 – $135) × 60,450 (906,750)

× $275 $ (103,125)

Unit cost factor ($275 – $275) × 4,500 0

Total effect of changes in registration, (103,125)

records, and marketing costs

Effect of changes in instructional costs:

Contribution Margin Analysis

For the Fall 2016 Term

UNDERWATER UNIVERSITY

Variable Costing Income Statement

For the Fall 2016 Term

UNDERWATER UNIVERSITY

20-26

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–1A (FIN MAN); Prob. 5–1A (MAN)

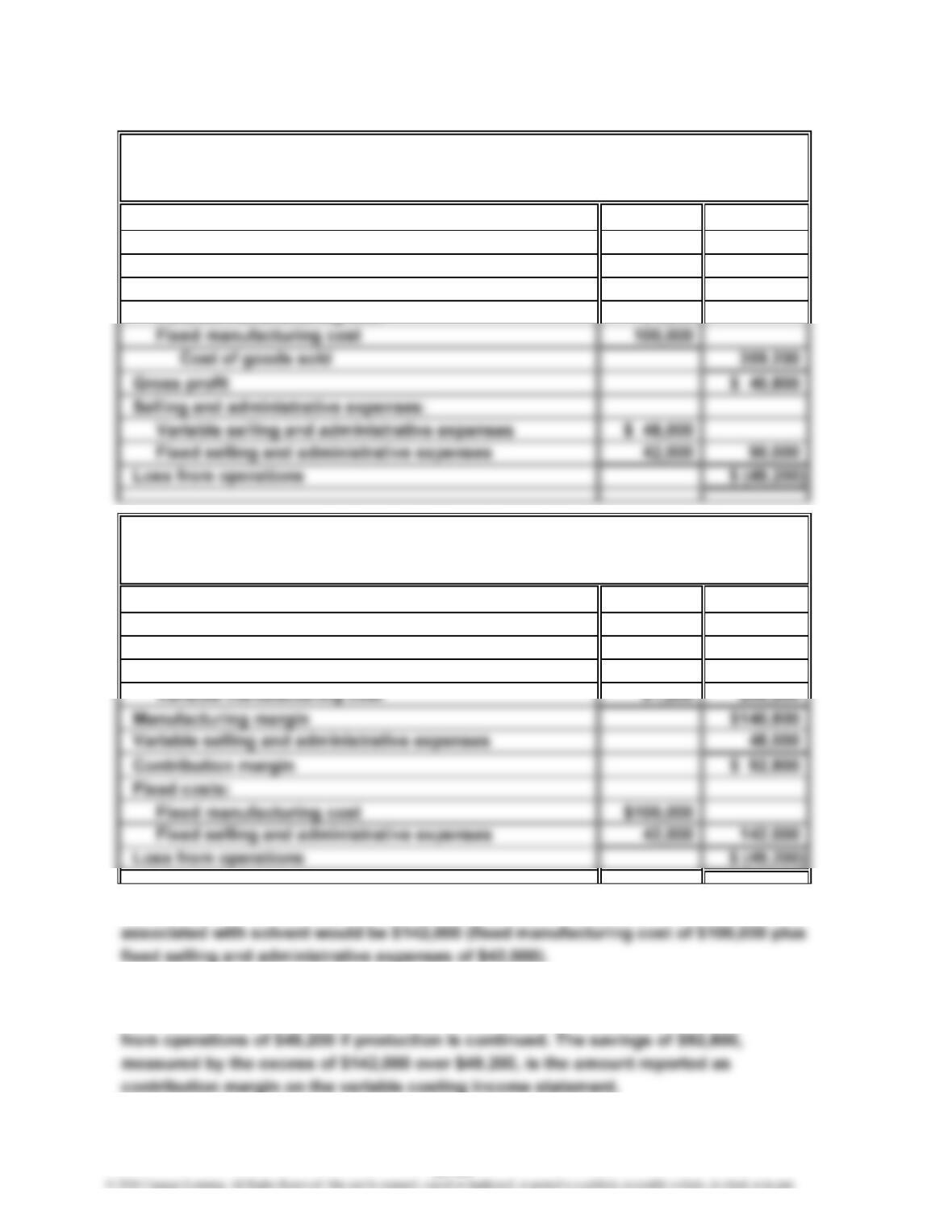

1.

Sales $6,480,000

Cost of goods sold:

Cost of goods manufactured $5,760,000

Less inventory, May 31 (4,000 units × $144.00*) 576,000

*$5,760,000 ÷ 40,000 units = $144.00

2.

Sales $6,480,000

Variable cost of goods sold:

Variable cost of goods manufactured $5,200,000

Less inventory, May 31 (4,000 units × $130.00*) 520,000

Variable cost of goods sold 4,680,000

*$5,200,000 ÷ 40,000 units = $130.00

3. The income from operations reported under absorption costing exceeds the

income from operations reported under variable costing by $56,000 ($360,000 –

FROST POINT FRIDGE COMPANY

Variable Costing Income Statement

For the Month Ended May 31, 2016

PROBLEMS

FROST POINT FRIDGE COMPANY

Absorption Costing Income Statement

For the Month Ended May 31, 2016

20-27

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–2A (FIN MAN); Prob. 5–2A (MAN)

1.

Sales (3,200 units) $400,000

Cost of goods sold:

Direct materials $144,000

Direct labor 64,000

Variable manufacturing cost 51,200

2.

Sales (3,200 units) $400,000

Variable cost of goods sold:

Direct materials $144,000

Direct labor 64,000

3. $142,000. The loss from operations from temporarily closing the portion of the plant

4. Production of solvent should be continued. Temporary suspension of production

would result in an operating loss of $142,000 [from (3) above], compared with a loss

MAC ‘N CHEESE INDUSTRIES INC.

Estimated Income Statement—Absorption Costing—Solvent

For the Month Ending May 31, 2016

For the Month Ending May 31, 2016

Estimated Income Statement—Variable Costing—Solvent

MAC ‘N CHEESE INDUSTRIES INC.

20-28

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–3A (FIN MAN); Prob. 5–3A (MAN)

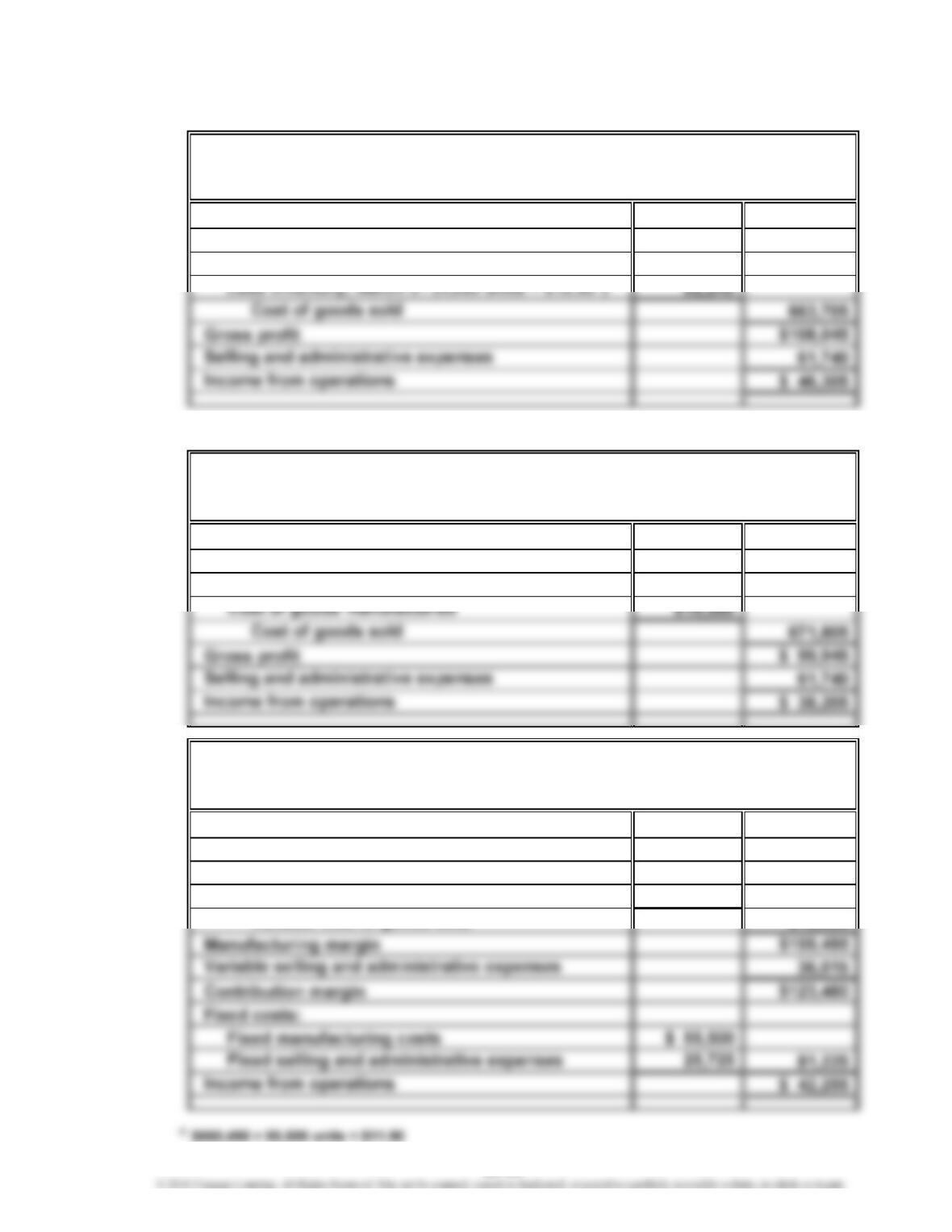

1. a.

Sales $771,750

Cost of goods sold:

Cost of goods manufactured $715,950

*$715,950 ÷ 55,500 units = $12.90

b.

Sales $771,750

Cost of goods sold:

Inventory, April 1 (4,050 units × $12.90) $ 52,245

2. a.

Sales $771,750

Variable cost of goods sold:

Variable cost of goods manufactured $660,450

Less inventory, March 31 (4,050 units × $11.90*) 48,195

Variable cost of goods sold 612,255

HIP AND CONSCIOUS CLOTHING COMPANY

Absorption Costing Income Statement

For the Month Ended March 31, 2016

HIP AND CONSCIOUS CLOTHING COMPANY

For the Month Ended March 31, 2016

HIP AND CONSCIOUS CLOTHING COMPANY

Absorption Costing Income Statement

For the Month Ended April 30, 2016

Variable Costing Income Statement

20-29

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–3A (FIN MAN); Prob. 5–3A (MAN) (Concluded)

2. b.

Sales $771,750

Variable cost of goods sold:

Inventory, April 1 (4,050 units × $11.90) $ 48,195

Variable cost of goods manufactured 564,060

Variable cost of goods sold 612,255

3. a. For March, the income from operations reported under absorption costing

exceeds the income from operations reported under variable costing by

$4,050. This difference is due to including $4,050 of fixed manufacturing

variable costing.

b. For April, the income from operations reported under absorption costing

is less than the income from operations reported under variable costing by

$4,050. This difference is due to including $4,050 of fixed manufacturing

4. The Hip and Conscious Clothing Company was equally profitable in March and

April under the variable costing concept. Sales and the variable cost per unit

were the same for both March and April. The difference in income reported

HIP AND CONSCIOUS CLOTHING COMPANY

Variable Costing Income Statement

For the Month Ended April 30, 2016

20-30

CHAPTER 20 Variable Costing for Management Analysis

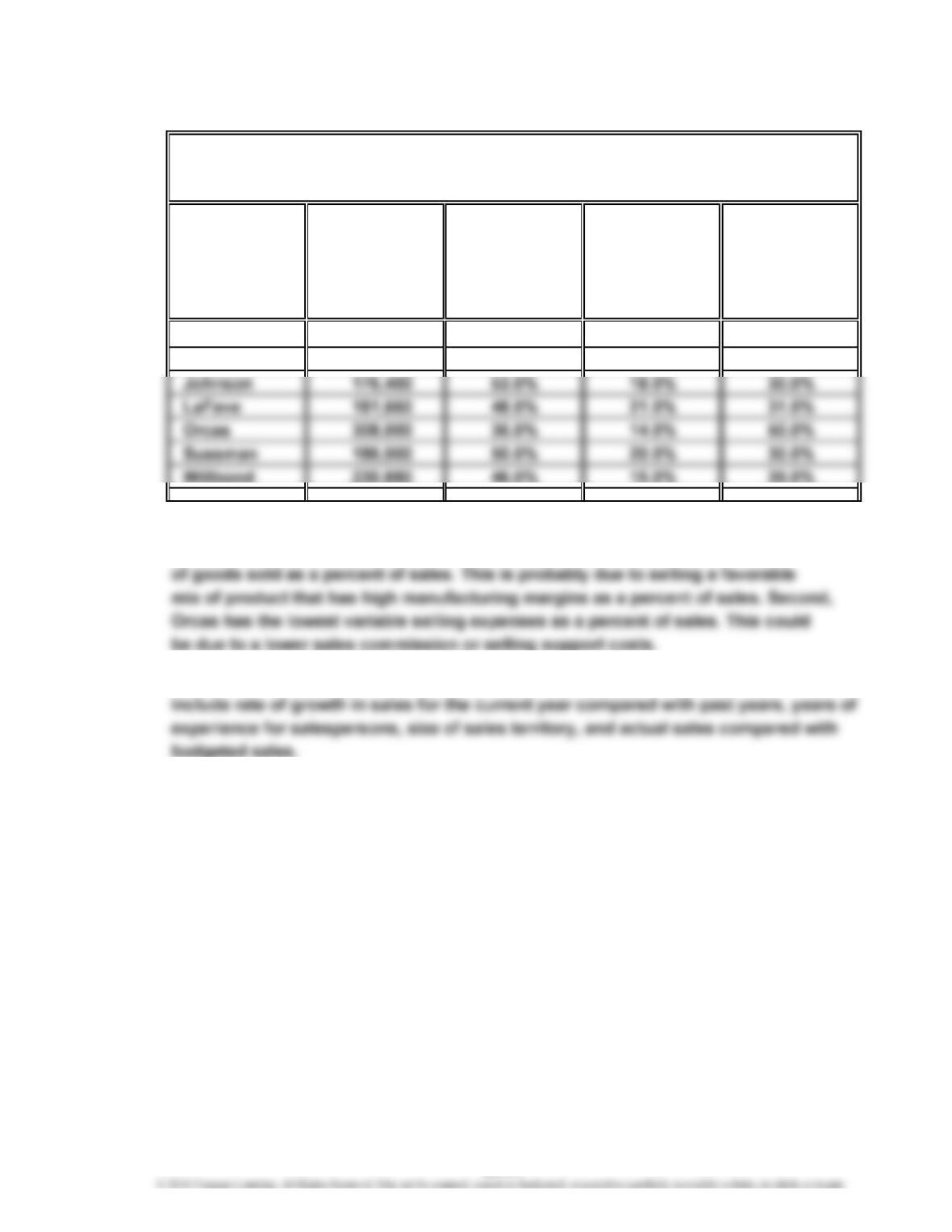

Prob. 20–4A (FIN MAN); Prob. 5–4A (MAN)

1.

Variable

Variable Cost Selling

of Goods Sold Expenses Contribution

Contribution as a Percent as a Percent Margin

Salesperson Margin of Sales of Sales Ratio

Case $231,800 44.0% 18.0% 38.0%

Dix 265,320 40.0% 16.0% 44.0%

2. Orcas has the highest contribution margin and contribution margin ratio for the

year. This is because of two factors. First, Orcas has the smallest variable cost

3. Other factors that should be considered in evaluating the performance of salespersons

WALTHMAN INDUSTRIES INC.

Salespersons’ Analysis

For the Year Ended December 31

20-31

CHAPTER 20 Variable Costing for Management Analysis

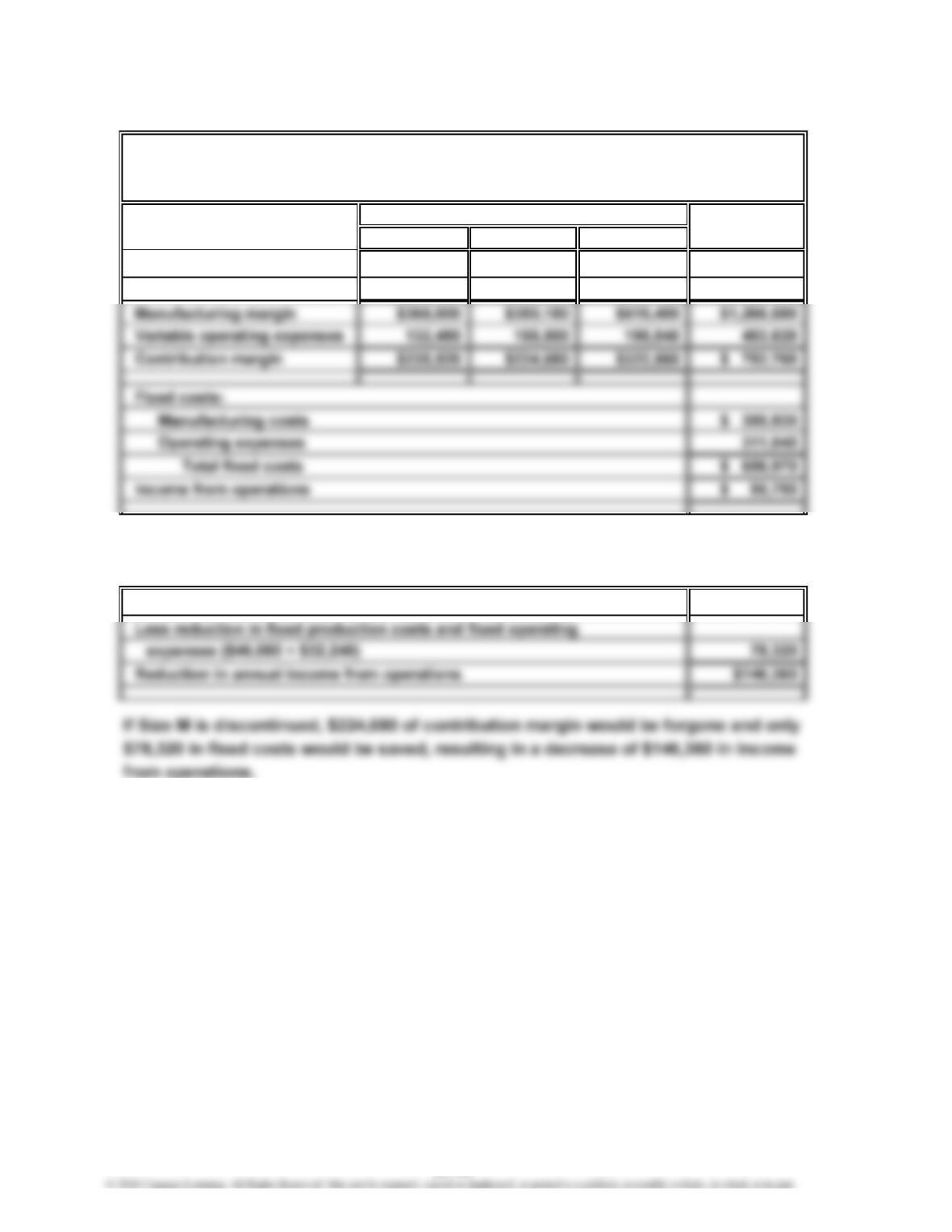

Prob. 20–5A (FIN MAN); Prob. 5–5A (MAN)

1.

S M L Total

Sales $668,000 $737,300 $956,160 $2,361,460

Variable cost of goods sold 300,000 357,120 437,760 1,094,880

2. Annual income from operations would be reduced below its present level by $146,360

if Size M were to be discontinued (Proposal 2), as indicated below:

Contribution margin for Size M $224,680

VALDESPIN COMPANY

For the Year Ended June 30, 2016

Variable Costing Income Statement

Size

20-32

CHAPTER 20 Variable Costing for Management Analysis

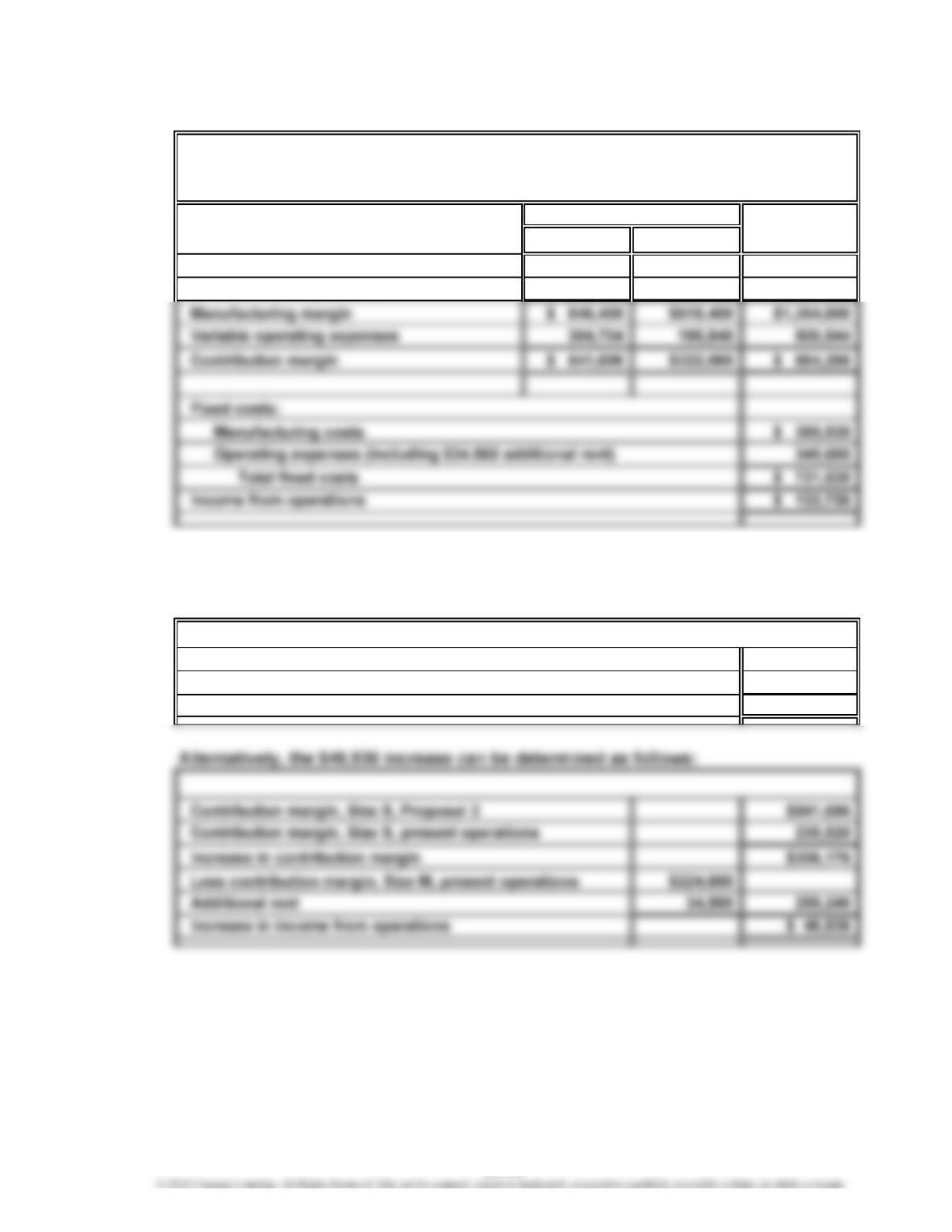

Prob. 20–5A (FIN MAN); Prob. 5–5A (MAN) (Concluded)

3.

S L Total

Sales $1,536,400 $956,160 $2,492,560

Variable cost of goods sold 690,000 437,760 1,127,760

4. $46,936. A comparison of the amount of income from operations under present

conditions, as indicated in (1), and under Proposal 3, as indicated in (3), suggests an

increase of $46,936 if Proposal 3 is accepted, as illustrated below.

Income from operations, Proposal 3 $132,726

Income from operations, present conditions 85,790

Increase in income from operations $ 46,936

Size

VALDESPIN COMPANY

For the Year Ended June 30, 2016

Variable Costing Income Statement

20-33

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–6A (FIN MAN); Prob. 5–6A (MAN)

1.

Planned contribution margin $1,386,000

Effect of change in sales:

Sales quantity factor (19,250 – 22,000) × $125 $(343,750)

Unit price factor ($144 – $125) × 19,250 365,750

Total effect of change in sales 22,000

2. The president’s first statement appears correct taken at face value. The president is

incorrect regarding variable cost of goods sold. The majority of the decrease in the

$4.00, which more than offset the favorable variable cost quantity factor, resulting

in an overall decrease in the contribution margin. The increase in the variable selling

DOZIER INDUSTRIES INC.

Contribution Margin Analysis

For the Year Ended December 31