20–1

CHAPTER 20

UNDERSTANDING THE ISSUES

1. Several of the important goals of estate

planning are to identify and clearly commu-

nicate the desires and wishes of the dece-

dent, maximize the value of the estate’s net

2. Given a married couple, when the first

spouse dies the decedent’s estate may be

passed to the surviving spouse without

incurring any estate tax at the time of the

3. It is important to separately account for the

income and principal of an estate for sev-

eral reasons. First, the decedent may have

created a will that has special provisions

quires that legacies be satisfied to whatever

extent possible, beginning with the highest

priority level of legacies. If demonstrative

legacy cannot be satisfied, the unsatisfied

Ch. 20—Exercises 20–2

EXERCISES

EXERCISE 20-1

Scenario A Scenario B

General legacies as set forth in will:

Amount due The Nature Conservancy ……………………. $ 50,000 $ 50,000

Equal amounts due three grandchildren ………………….. 150,000 150,000

Unsatisfied demonstrative legacies that constitute a

general legacy:

Amount not satisfied by insurance proceeds ……………. 20,000 20,000

Total needed to satisfy general legacies ………………………… $220,000 $ 220,000

Available cash to satisfy general legacies:

Cash at date of death …………………………………………… $ 40,000 $ 15,000

Sale of Kachina collection……………………………………… 45,000 —

Note A: Under scenario A, there is enough cash available to satisfy all general legacies.

Therefore, Riley will receive the stated amount of $50,000.

20–3 Ch. 20—Exercises

EXERCISE 20-2

(1) The unified gift and estate tax exclusion amount is ……………… $ 5,340,000

(2) Taxable estate ……………………………………………………………….. $12,000,000

Post 1976 taxable gifts:

Prior taxable gift …………………………………………………………. 856,000

Taxable gifts to children (($50,000 – $14,000) × 4) …………. 144,000

(3) Helen George

Taxable estate ……………………………………………………………….. $10,000,000 $8,160,000

Less marital deduction …………………………………………………….. (6,160,000) 0

Taxable estate ……………………………………………………………….. $ 3,840,000 $8,160,000

(4) Residual legacy:

Remaining bank balance to sister Ann ($60,000 – $40,000) …………….. $ 20,000

(5) The sum of the residual legacies would be:

Remaining bank balance to sister Ann ($60,000 – $40,000) …………….. $ 20,000

EXERCISE 20-3

(1) Only $1,000 of the gift to the grandson would be considered taxable. Gifts to charities and

(2) Previous taxable gifts to grandchildren

[($25,000 – $14,000) × 4 × 3 years] ………………………………………………….. $ 132,000

Lifetime exclusion …………………………………………………………………………… $5,340,000

(3) Cumulative taxable gifts:

Gift to 3 children [($200,000 – $14,000) × 3] …………………………………… $ 558,000

Gift to brother ($50,000 – $14,000) ……………………………………………….. 36,000

(4) Spouse Spouse

Total of prior gifts ……………………………………………………………. $ 666,000 $ 100,000

EXERCISE 20-4

Principal

Income

Assets received:

Personal residence ………………………………………………. $350,000

Cash ………………………………………………………………….. 230,000

Securities ……………………………………………………………. 210,000

Personal effects …………………………………………………… 12,000

Assets disbursed:

Amount conveyed to Sierra Club ……………………………. $200,000

Mortgage principal ……………………………………………….. 16,000

Mortgage interest …………………………………………………. 2,000 $ 6,000

Funeral and administrative fees ……………………………… 27,000

Balance before distributions/transfers ……………………………. $492,400 $ 6,200

EXERCISE 20-5

(1) Determination of estate tax:

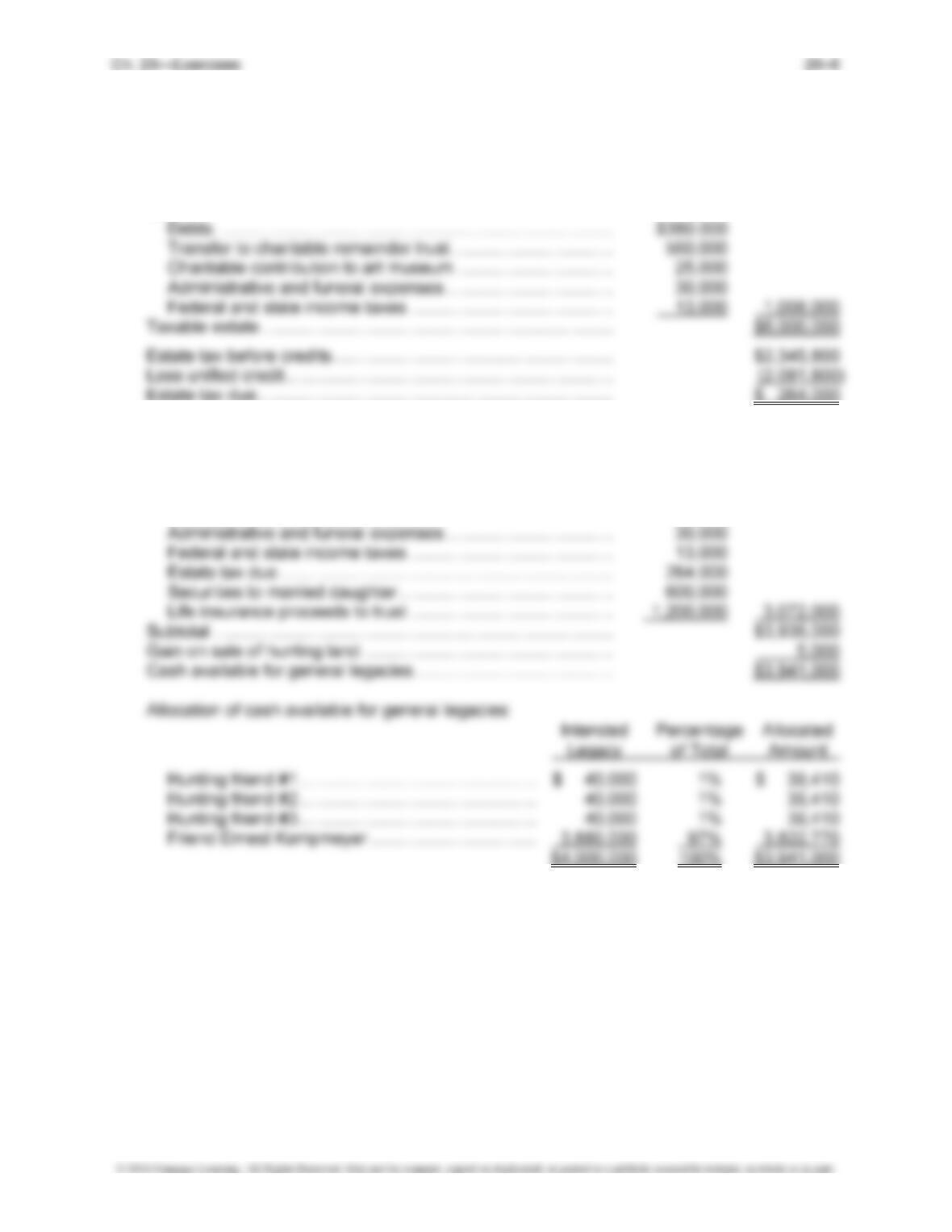

Gross estate ………………………………………………………………….. $7,008,000

Less:

(2) Gross estate ………………………………………………………………….. $7,008,000

Distribution before general legacies:

Debts ………………………………………………………………………… $ 380,000

Transfer to charitable remainder trust ……………………………. 560,000

Charitable contribution to art museum …………………………… 25,000

EXERCISE 20-6

Determination of estate tax liability assuming not trusts are created:

Edith Leppert Gerald Leppert

Initial gross estate equal to net assets ……….. $4,300,000 $2,400,000

Add:

Edith’s unused credit ………………………….. (2,081,800)

Available to Gerald …………………………….. (815,401)

Estimated estate tax due …………………………. $ 0 $ 0

Determination of estate tax liability assuming a credit shelter trust is created:

Edith Leppert Gerald Leppert

Estate tax before credits ………………………….. $1,345,800 $1,657,389

Less unified credit:

Available to Edith ………………………………. (1,345,800)

Edith’s unused credit ………………………….. (736,000)

Available to Gerald …………………………….. (921,389)

Exercise 20-6, Concluded

Note A: This is the amount of the marital deduction.

Note B: Subsequent appreciation is on $2,400,000 traceable to husband plus $4,125,000

EXERCISE 20-7

(a) + (b) = (c) + (d)

Noncash Trust Trust

Cash

Assets Principal Income

Transfer of assets into trust ………………………….. $ 100,000 $ 750,000 $ 850,000

Subsequent discovery of assets ……………………. 40,000 40,000

Sale of real estate partnership ………………………. 220,000 (200,000) 20,000

Receipt of IBM dividend ……………………………….. 20,000 20,000

Receipt of interest income ……………………………. 5,000 $ 5,000

Distribution of assets to children ……………………. (32,000) (27,000) (5,000)

Payment of trustee’s fees …………………………….. (10,000) (5,000) (5,000)

20–9 Ch. 20—Exercises

EXERCISE 20-8

Principal Cash ……………………………………………………………………………. 15,000

Land …………………………………………………………………………………………. 130,000

(1) Funeral and Administrative Expenses …………………………………….. 22,000

(2) Investment in IRA Account ……………………………………………………. 37,000

(3) Principal Cash …………………………………………………………………….. 1,000

Income Cash ………………………………………………………………………. 2,700

(4) Principal Cash …………………………………………………………………….. 140,000

(5) Income Cash ………………………………………………………………………. 400

Principal Cash …………………………………………………………………….. 19,000

(6) Debts of Decedents Paid ………………………………………………………. 28,000

(7) Legacies Distributed …………………………………………………………….. 15,000

(8) Funeral and Administrative Expenses …………………………………….. 3,100

Expenses Chargeable against Income ……………………………………. 100

(1) Estate of Jason Jackson

________________ , Executor

Charge and Discharge Statement

For Period _________ to _________

As to Principal

I charge myself with:

Assets per original inventory ……………………………………………… $272,000

Assets subsequently discovered ………………………………………… 37,000

Gain on sale of principal assets …………………………………………. 10,000

As to Income

I charge myself with:

Estate income …………………………………………………………………. $3,100

(2) Entries to transfer assets to trust:

Principal Assets Transferred to Trust ……………………………………….. 250,900

Cash—Principal ……………………………………………………………… 106,900

20–11 Ch. 20—Problems

PROBLEMS

PROBLEM 20-1

Strategies to minimize estate tax should include:

1. Maximizing the use of the annual gift tax exclusion amount per donor per donee. Both

James and Susan could gift to their children and grandchildren.

3. Recognition that tuition payments to an educational organization made on another’s behalf

are not considered taxable gifts if paid directly to the organization.

5. The executor of the decedent’s estate should make the election to insure the portability of

the unified credit.

Consideration of the above strategies and factors set forth in the problem could result in a signif-

icant reduction in estate taxes determined as follows:

James Wagner Susan Wagner

Initial gross estate ………………………………….. $12,700,000 $4,800,000

Add:

Spouse’s remaining estate (see Note A) . $6,805,000

Subsequent appreciation (see Note B) … 450,000 7,255,000

Taxable estate ………………………………………. $5,340,000 $7,750,000

Estate tax before credits …………………………. $2,081,800 $3,045,800

Less unified credit ………………………………….. (2,081,800) (2,081,800)

Estimated estate tax due ………………………… $ 0 $964,200

Remaining estate after payment of estate taxes $6,786,000

Problem 20-1, Concluded

Note C: Gifts to each of the two children and the three grandchildren could be made by both

spouses as follows:

PROBLEM 20-2

Entries to record activities of estate:

Principal Cash …………………………………………………………………….. 50,000

Personal Residence …………………………………………………………….. 450,000

Automobile and Sailboat ……………………………………………………….. 65,000

Investment in Mutual Funds ………………………………………………….. 3,280,000

Collection of Antique Duck Decoys ………………………………………… 85,000

Devises Distributed ………………………………………………………………. 300,000

Mortgage on Personal Residence ………………………………………….. 150,000

Personal Residence ………………………………………………………… 450,000

To record transfer of personal residence to sister.

20–13 Ch. 20—Problems

Problem 20-2, Continued

Principal Cash …………………………………………………………………….. 450,000

Life Insurance Policy Loan ……………………………………………………. 50,000

Death Benefit of Life Insurance ………………………………………… 500,000

To record collection of death benefit and payment of

policy loan.

Credit Cards Payable …………………………………………………………… 5,000

Principal Assets Transferred to Trust ……………………………………… 3,929,000

Income Assets Transferred to Trust ……………………………………….. 10,000

Investment in Mutual Funds ……………………………………………… 3,110,000

Farmland in Ozaukee County …………………………………………… 800,000

Estate Principal ……………………………………………………………………. 5,025,000

Estate Income ……………………………………………………………………… 10,000

Problem 20-2, Concluded

Entries to record activities of trust:

Principal Cash …………………………………………………………………….. 19,000

Income Cash ………………………………………………………………………. 10,000

Investment in Mutual Funds ………………………………………………….. 3,110,000

To record property taxes and operating expenses.

Principal Cash …………………………………………………………………….. 170,000

Income Cash ………………………………………………………………………. 7,000

Investment in Mutual Funds ……………………………………………… 170,000

Trust Income ………………………………………………………………….. 7,000

To record sale of mutual funds.

PROBLEM 20-3

(1) Assuming no credit shelter trust is employed:

Decedent Decedent

Spencer Cook Sara Cook

Gross estate ………………………………………….. $8,600,000 $ 13,300,000

(2) Assuming a credit shelter trust is employed:

Decedent Decedent

Spencer Cook Sara Cook

Gross estate ………………………………………….. $ 8,600,000 $11,400,000

PROBLEM 20-4

Calculation of estate tax:

Gross estate:

Rug and pottery collection ……………………………………………………………. $ 120,000

Personal residence …………………………………………………………………….. 550,000

Brokerage account at Wachovia Securities ……………………………………. 2,200,000

Brokerage account at Schmidt Investment Services ………………………… 900,000

Less allowable deductions:

Deductions excluding charitable donations …………………………………….. $ 235,000

Donation to Museum of Northern New Mexico ……………………………….. 120,000

Donation to First Church of Brookfield …………………………………………… 200,000

Total ……………………………………………………………………………………. $ 555,000

Taxable estate ……………………………………………………………………………………… $ 5,800,000

Available cash to satisfy general legacies:

Excess amount realized on Buffalo County hunting land ………………….. $ 50,000

Excess insurance policy proceeds ………………………………………………… 50,000

Liquidated value of other assets …………………………………………………… 1,500,000

Unsatisfied demonstrative legacies that constitute a general legacy:

Not satisfied by Wachovia Securities account for brother Thomas …….. 300,000

Not satisfied by Schmidt Investment Services account for two sisters .. 100,000

Total needed to satisfy general legacies …………………………………………………… $ 2,000,000

General legacies can be satisfied at the rate of 70.8% ($1,416,000/$2,000,000) and are satis-

fied as follows:

Amount due eight grandchildren (allocated equally) ………………………… $ 283,200

PROBLEM 20-5

At Date At Alternative

of Death

Valuation Date

Gross estate:

Google stock …………………………………………………………………… $2,700,000 $2,340,000

Macon County real estate …………………………………………………. 3,250,000 3,050,000

Household effects ……………………………………………………………. Excluded Excluded

Deductions allowed:

Loan against real estate ……………………………………………………. $307,200 $307,200

Funeral and administrative expenses …………………………………. 45,000 45,000

Property taxes …………………………………………………………………. 4,000 4,000

Income taxes …………………………………………………………………… 27,000 27,000

Total ………………………………………………………………………………. $383,200 $383,200

Taxable estate ……………………………………………………………………… $6,678,800 $6,059,800

Post-1976 taxable gifts:

Total …………………………………………………………………………. $6,201,000 $6,201,000

Unified tax base ……………………………………………………………………. $12,879,800 $12,260,800

Estate tax:

Tentative tax on total transfers …………………………………………… $ 4,850,120

Less unified credit ……………………………………………………………. (2,081,800)

Problem 20-5, Concluded

Year Prior to Year of Year of

Tax due by year: Diagnosis Diagnosis Death Total

*The amount of these gifts has been reduced by the $14,000 annual exclusion.

** This is tax of $2,426,200 on a gift of $6,201,000 less the lifetime exclusion amount of

$2,081,800.

***The gift tax for each year is determined as follows:

Year Prior to Year of Year of

Diagnosis Diagnosis Death

Cumulative gift……………. $ 6,000,000 $ 6,146,000 $ 6,201,000

Tentative tax………………….. $ 2,345,800 $ 2,404,200 $ 2,426,200

20–19 Ch. 20—Problems

PROBLEM 20-6

(1) Estate of Eleanor Matsun

James Madison, Personal Representative

Charge and Discharge Statement

For the Period June 1 through December 31 of the Year of Death

As to Principal

I charge myself with:

Assets per original inventory ……………………………………………… $441,300

Assets subsequently discovered:

Gold coin collection …………………………………………………….. 18,000

Dividend on Pal Corp. common stock ……………………………. 2,500

I credit myself with:

Payment of credit cards ……………………………………………………. $ 2,900

Funeral expenses …………………………………………………………….. 16,000

Legal fees 2,500

Cost associated with sale of residence ……………………………….. 28,000

Payment to personal representative …………………………………… 4,000

As to Income

I charge myself with:

Income from partnership …………………………………………………… $ 5,000

PROBLEM 20-7

(1) Cash—Principal [($40,000 × 1.03) + accrued interest] ………………. 41,467

Cash—Income ($40,000 × 0.08 × 1/12) ………………………………….. 267

(2) Investment in 5% Detroit Bonds …………………………………………….. 50,000

Accrued Interest on Detroit Bonds ($50,000 × 0.05 × 5/12) ……….. 1,042

(3) Investment in 7% Newark Bonds ……………………………………………. 10,000

Accrued Interest on Newark Bonds ($10,000 × 0.07 × 3/12) ……… 175

(4) Cash—Principal …………………………………………………………………… 1,042

Cash—Income ($50,000 × 0.05 × 1/12) ………………………………….. 208

Accrued Interest on Detroit Bonds …………………………………….. 1,042

Estate Income ………………………………………………………………… 208

(5) Cash—Principal (amortization + accrued interest) ……………………. 202

Cash—Income …………………………………………………………………….. 148

Premium on Newark Bonds [($200 ÷ 21 months) × 3 months] . 29

(6) Cash—Income ($50,000 × 0.05 × 5/12) ………………………………….. 1,042

Cash—Principal ($50,000 × 1.01) ………………………………………….. 50,500