CHAPTER 20

COST-VOLUME-PROFIT ANALYSIS

Brief Learning

Exercises Topic Objectives Skills

B. Ex. 20.1 Cost behavior patterns 20-1 Analysis

B. Ex. 20.2 Cost classifications 20-1 Analysis

B. Ex. 20.3 Using a cost formula 20-1, 20-9 Analysis

B. Ex. 20.4 Using a cost formula

20-1, 20-4,

20-5, 20-9

Analysis

B. Ex. 20.5 Computing required sales volumes 20-4–20-6 Analysis

B. Ex. 20.6 Computing required sales volumes 20-4–20-6 Analysis

B. Ex. 20.7 Contribution margins and selling prices

20-1, 20-4 –

20-6

Analysis

B. Ex. 20.8 Evaluating marketing strategies 20-7 Analysis

B. Ex. 20.9 Selecting an activity base 20-1 Judgment, analysis

B. Ex. 20.10 CVP with multiple products 20-8 Analysis

Learning

Exercises Topic Objectives Skills

20.1 Accounting terminology

20-1, 20-2,

20-4

Analysis

20.2 High-low method of cost estimation 20-1, 20-9 Analysis

20.3 Determining required sales volumes 20-4, 20-5 Analysis

20.4 Computing break-even points 20-4–20-6 Analysis

20.5 Solving for missing information 20-1, 20-4 Analysis

20.6 Ethical implications of CVP 20-5–20-7 Judgment, communication

20.7 Using CVP 20-4–20-6 Analysis

20.8 Using CVP 20-4–20-6 Analysis

20.9 Understanding break-even relationships

20-1, 20-2,

20-4–20-6

Analysis

20.10 Margin of safety 20-4, 20-5 Analysis

20.11 Applying CVP

20-1, 20-2,

20-4–20-6

Analysis

20.12 Solving for missing information 20-5, 20-6 Analysis

20.13 Formulating bid prices using CVP

20-1, 20-4 –

20-6

Analysis

20.14 CVP with multiple products 20-7, 20-8 Analysis

20.15 Estimating semivariable costs 20-9 Analysis

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Learning

Topic Objectives Skills

20.1 A,B Establishing selling prices 20-4–20-7 Analysis, communication

20.2 A,B Estimating costs and profitability

20-1, 20-4,

20-5

Analysis

20.3 A,B Preparing a break-even graph

20-3–20-6,

20-9

Analysis, communication

20.4 A,B Preparing a break-even graph

20-3, 20-4,

20-6, 20-9

Analysis, communication

20.5 A,B CVP analysis

20-3–20-7,

20-9

Analysis, communication

20.6 A,B Cost analysis

20-4–20-7,

20-9

Analysis, communication

20.7 A,B Cost analysis

20-4, 20-6,

20-7

Analysis, communication

20.8 A,B CVP with multiple products 20-4–20-8 Analysis, communication

CRITICAL THINKING CASES

20.1 CVP from differing perspectives 20-1 Judgment, communication

20.2

Evaluating marketing strategies costing

information

20-1, 20-4,

20-5, 20-6,

20-7

Communication, analysis

20.3 Deciding whether to file a Form 8-K 20-1 Analysis, judgment,

Ethics, Fraud & Corporate Governance communication

20.4 Real World: Ford Motor Company 20-8 Communication,

Internet technology, research

Sets A, B

Problems

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

Ionic Charge/Nathe, Inc. Medium

Use of cost-volume-profit relationships in a pricing decision. Student

is to compute the unit sales prices necessary to achieve a target

operating income. Also determine whether the company can break

even if sales price is reduced to achieve market penetration.

Blaster Corporation/Snug-As-A-Bug Medium

Illustrates a pricing decision: compute the unit sales price necessary

to achieve a target income at a given unit sales volume. Also

compute the number of units that must be sold annually to break

even at an alternative unit sales price.

Stop-n-Shop/Moor-n-More 30 Medium

A profit-volume problem requiring an annual profit graph. Draw a

profit-volume graph on an annual basis. Compute the contribution

margin and break-even point. Consider the effect of a change in

employee compensation and determine sales necessary to produce a

given income.

20.4 A,B Rainbow Paints/Green Thumb 30 Medium

Create a cost-volume-profit graph for a retail business. Compute the

break-even sales volume and the operating income likely to result at

the highest and lowest expected sales volume.

20.5 A,B Simon Teguh/Ed Winslow 40 Strong

Draw a monthly cost-volume-profit graph for a vending machine

business. Determine the break-even point and the sales volume

needed to provide the owner with a given return on investment. Also

consider the effect of a change in costs upon the break-even point.

20.6 A,B Precision Systems/Electro Systems 30 Strong

Compute the increase in selling price necessary to maintain

contribution margin ratio after increase in direct labor cost. Compute

sales volume after wage increase in order to earn a given net income.

Consider the effect of expansion on maximum income that can be

earned.

Below are brief descriptions of each problem, case, and the first Internet assignment. These

descriptions are accompanied by the estimated time (in minutes) required for completion and by a

difficulty rating. The time estimates assume use of the partially filled-in working papers.

20.2 A,B

25

20.3 A,B

20.1 A,B

25

20.7 A,B Percula Farms/Dorsal Ranch 35 Strong

Students must analyze two alternative production strategies and

determine which factors or costs have the greatest influence on

operating income. Given two investment options, students must first

intuitively decide which should result in the greatest increase to

operating income, and then perform calculations to confirm their

answer.

20.8 A,B Lifefit Products/HomeTeam Sports 35 Strong

Calculate break-even in dollars and in units for a multiple product

company. Determine operating income required for a desired margin of

safety. Determine sales level required for a desired level of income if

fixed costs are reduced.

CRITICAL THINKING CASES

20.1 Multiple Perspectives—Attend Our Seminar 20 Medium

Students play the role of a cost-volume-profit seminar leader. They

are asked to motivate individuals to attend their seminar by showing

them how the information can be of benefit. This is a good group

problem that encourages students to think beyond the mechanics of

cost-volume-profit analysis.

20.2 Don’t Mess with the Purple Cow 40 Strong

Students are asked to evaluate two alternative marketing proposals

and make a recommendation to management. The problem contains

an interesting twist: neither proposal is as profitable as the status

quo—but students’ attention is not specifically directed toward this

vital issue. A lesson in the fact that real-life problems do not come

with “instructions” that make the answers clear.

20.3 Filing Form 8-K 10 Easy

Ethics, Fraud and Corporate Governance

Students are asked to determine whether a company should file a

Form 8-K and whether it is legal and/or ethical to withhold certain

information.

20.4 Ford Motor Company 15 Easy

Internet

Using information contained the company’s 10-K, students are asked

to analyze Ford’s income statement and discuss how the company’s

sales mix might influence its profitability.

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

3.

a. Total variable costs increase in approximate proportion to an increase in activity.

4.

5.

6.

a.

Under the high-low method, the levels of a semivariable cost and of the related activity base

are observed at the highest and lowest points of activity within the relevant range. The

It is important for management to understand cost-volume-profit relationships in order to do a

An activity base is a measure of a type of business activity that “drives” variable costs. The

activity base allows us to quantify the expected relationships between variable costs and the

Two factors make the simplifying assumption of straight-line cost-volume relationships useful.

First, unusual patterns of cost behavior (stair-step or curvilinear) tend to offset one another when

The relevant range represents the operating levels (for example, between 40% and 80% of full

7.

a.

8.

9.

11.

The contribution margin is the dollar amount by which revenue exceeds variable costs.

Thus, it is the amount of revenue that is available to cover fixed costs and to contribute to

operating income. Unit contribution margin = unit sales prices – variable costs per unit.

A change in product (sales) mix to a higher proportion of export sales may result in a lower level

of net income if the contribution margin ratio on export sales is lower than the average

contribution margin ratio on all sales. This is often the case with export sales made by American

At the break-even point, a company earns a total contribution margin exactly equal to its fixed

The important relationships shown in a cost-volume-profit graph are changes in revenue, costs,

and operating income in relation to changes in the volume of business activity. The point at

14.

15.

The regional airline will probably have a higher break-even point than a furniture manufacturer

Basic assumptions underlying cost-volume-profit analysis include: (1) a constant selling price

SOLUTIONS TO BRIEF EXERCISES

B. Ex. 20.1 a.

Total variable costs increase approximately in proportion to an increase in the

volume of activity.

e.

Semivariable costs include both fixed and variable cost elements. Because of

f.

On a per-unit basis, the fixed elements of a semivariable cost decline as the

B. Ex. 20.2 a.

Variable. The cost of goods sold normally rises and falls in almost direct

b.

As described in this exercise, the salaries to salespeople are semivariable with

B. Ex. 20.2

(continued)

c.

e.

f.

B. Ex. 20.3 a. (1)

$ 75,000

(300 calls × $200 per call) ………………………

(2)

$ 135,000

Number of calls ……………………………………

Fixed. Use of an accelerated method causes depreciation expense to change from

Fixed element of monthly emergency response cost …

Average cost per call (300 calls per month):

Income taxes are not a fixed, variable, or semivariable cost with respect to net

sales. Income taxes may be viewed as a variable cost, but the relevant activity base

Estimated cost of responding to 300 emergency calls in one

month:

Fixed. Depreciation expense on a sales showroom is independent of the level of

net sales. Fluctuations in net sales have no effect upon the amount of depreciation

B. Ex. 20.3

b.

c. $ 12,000

Variable element of room service costs ($40,000 × 60%) …

B. Ex. 20.5 a.

Fixed element of room service costs …………………………

If the contribution margin ratio is 20%, variable costs must be 80% of

The overall cost of responding to emergency calls is semivariable—that

B. Ex. 20.6 a.

B. Ex. 20.7 a. $ 7,200,000

40%

Break-even sales volume ($90 × 80,000 units) ……………

Variable cost per unit ($4,320,000 ÷ 80,000 units) ………

Fixed costs ($7,200,000 × 40%) …………………………….

Variable cost at 80,000 units ………………………………

B. Ex. 20.8 a. $7,000

Break-even sales volume ($90 × 80,000 units) …………

Contribution margin ratio ……………………………….

If variable costs are 75% of sales revenue, the contribution margin

B. Ex. 20.9

B. Ex. 20.10 a. Contribution Percentage of Average

Margin Ratio × Total Sales = Contribution

40% 14%

Flashlights

Passenger miles driven

Machine hours

Sales dollars

Number of cases

McCauley & Pratt, Attorneys at Law

Billable client hours

Susquehanna Trails Bus

Direct labor hours

35%

Freeman’s Retail Floral Shop

The following activity bases could be suggested to each of your clients:

Possible Activity Bases

Client

Sales dollars

20%

Batteries

SOLUTIONS TO EXERCISES

Ex. 20.1 a.

(1) Machine Manufacturing

Hours Overhead

6,000 $320,000

3,500 $140,000

Estimated manufacturing overhead at activity level

Low point

at 6,000 machine-hour level ……………………….

Changes

Total manufacturing overhead

c. February March

$ 208,000

224,000 264,000

$ (16,000) $ 12,000

Break-even point

Estimated manufacturing overhead:

High point

Ex. 20.2

a.

February:

$80,000 + ($40 per MH × 3,200 MH) …….

c.

e.

Economies of scale

Unit contribution margin

Fixed costs

Relevant range

Contribution margin

Semivariable costs

Ex. 20.3 a.

Ex. 20.4 a. Product 1 Product 2

75% 30%

b. Product 1 Product 2

75% 30%

Contribution

Variable

Margin Ratio

Fixed Operating Units

Sales Costs per Unit Costs Income Sold

(1) $200,000 $120,000 $20 $55,000 $25,000 4,000

Contribution

Variable

Margin Ratio

Fixed Operating

Sales Costs Ratio (%) Costs Income

(1) $900,000 $720,000 20% $85,000 $95,000

Unit contribution margin: $950 – $570 = $380

Contribution margin ratio

Contribution margin ratio

Ex. 20.5

a.

Ex. 20.6

Ex. 20.7

It is never ethical to lie to one’s employees. This type of behavior will only serve

=

a.

Contribution Margin Ratio

Unit Sales Price – Variable Cost per Unit

Unit Sales Price

=

=

=

=

$450,000

=

a.

220,000$

Ad Campaign

Ordering

System

b.

Ex. 20.8

For the ad campaign to result in an equal increase in operating income, the total

contribution margin produced must equal that of the ordering system ($360,000).

Projected operating Income without either investment:

($1,200,000 × 0.25) – $80,000

Total contribution margin

Projected sales revenue

a.

$ 1.75

1.25

Contribution margin per unit $ 0.50

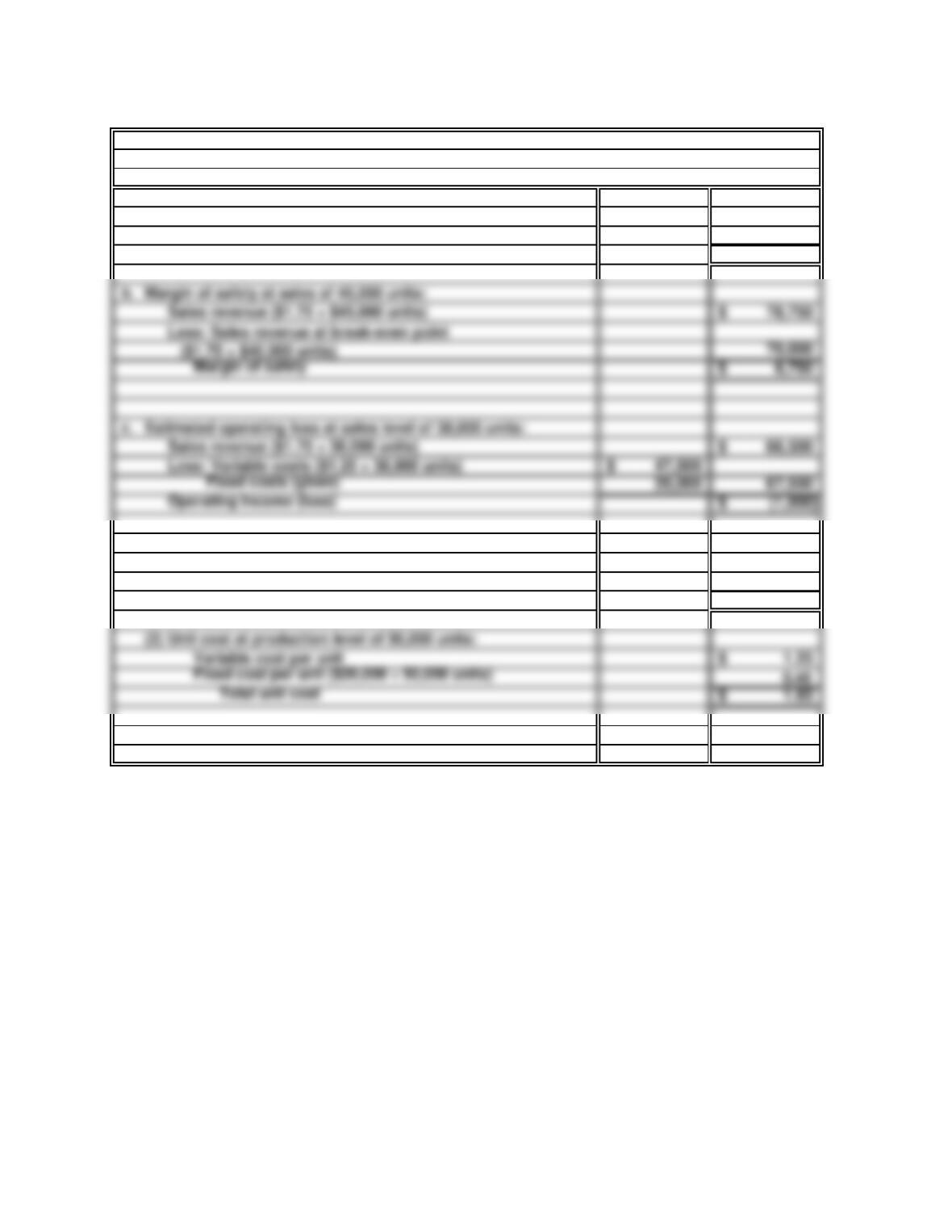

d. (1) Unit cost at production level of 40,000 units:

Variable cost per unit $ 1.25

Fixed cost per unit ($20,000 ÷ 40,000 units) 0.50

Total unit cost $ 1.75

Fixed cost per unit ($20,000 ÷ 50,000 units) 0.40

Total unit cost 1.65$

Total cost per unit declines at higher production levels because the fixed manufacturing costs

are allocated over a greater number of units.

Ex. 20.9

Contribution margin per unit:

Unit sale price

Less: Variable cost per unit ($50,000 ÷ $40,000 units)

b.

Margin of safety 8,750$

c.

Operating Income (loss) (1,000)$

Margin of safety at sales of 45,000 units:

Estimated operating loss at sales level of 38,000 units:

Divided by contribution margin per unit ………………………

Total fixed costs …………………………………………………

Variable selling and administrative costs per unit ……………

Fixed selling and administrative costs ………………………..

Fixed manufacturing costs ……………………………………..

Ex. 20.10 a.

Ex. 20.11 a. 20$

(6)

b.

60%

900,000$

Target monthly income …………………………………………

Divided by contribution margin ratio ………………………….

Current monthly sales level ……………………………………

c. 900,000$

÷ 60%

Total fixed costs …………………………………………………

Total fixed costs …………………………………………………

Contribution margin ratio ………………………………………

Contribution margin ratio (CM ÷ SP) …………………………..

Selling price per unit ……………………………………………

Variable manufacturing costs per unit………………………….

Contribution Margin

Ratio

Unit Sales Price – Variable Costs

Sales Price

=

=

=

=

=

=

Ex. 20.12

20,000 units x $7 per unit = $140,000 total fixed costs

SP = Selling Price = $40 per unit

Fixed Costs ÷ Contribution Margin = Break-Even in Units

Ex. 20.13 a. The lowest bid price required to maintain the current

level of operating income equals total variable cost

per unit: