CHAPTER 20 Process Cost Systems

Ex. 20-16 (Concluded)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

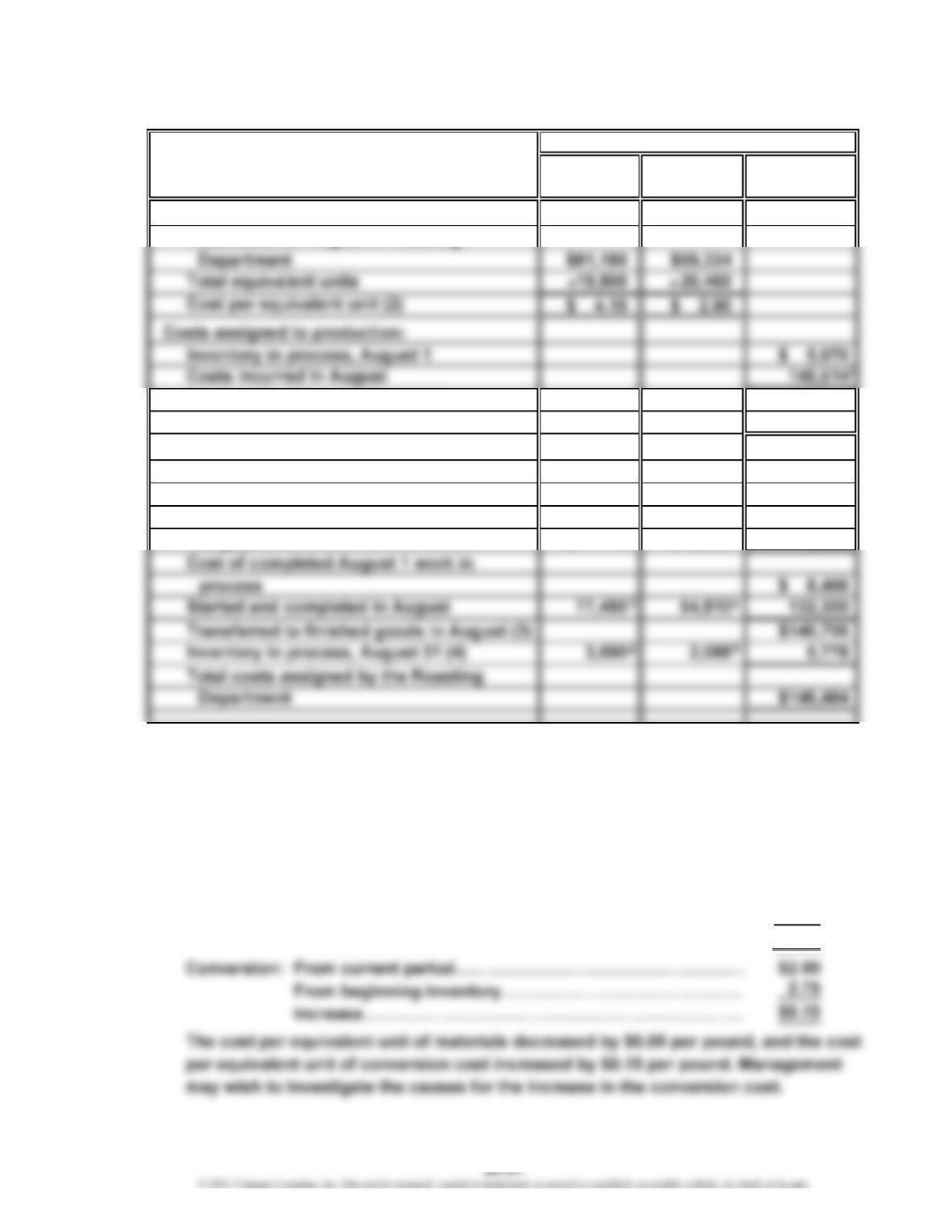

Total costs for August in Roasting

Total costs accounted for by the

Roasting Department $146,484

Costs allocated to completed and

partially completed units:

Inventory in process, August 1 balance $ 5,970

To complete inventory in process,

August 1 $ 0 $ 2,436 2,436

1

$81,180 + $59,334

2

840 units × $2.90

3

18,900 units × $4.10

4

18,900 units × $2.90

5

900 units × $4.10

6

720 units × $2.90

b. Materials: From current period……………………………………………

…

From beginning inventory……………………………………

…

Decrease…………………………………………………………

…

…

…

Costs

$ 4.10

4.15

$(0.05)

2

CHAPTER 20 Process Cost Systems

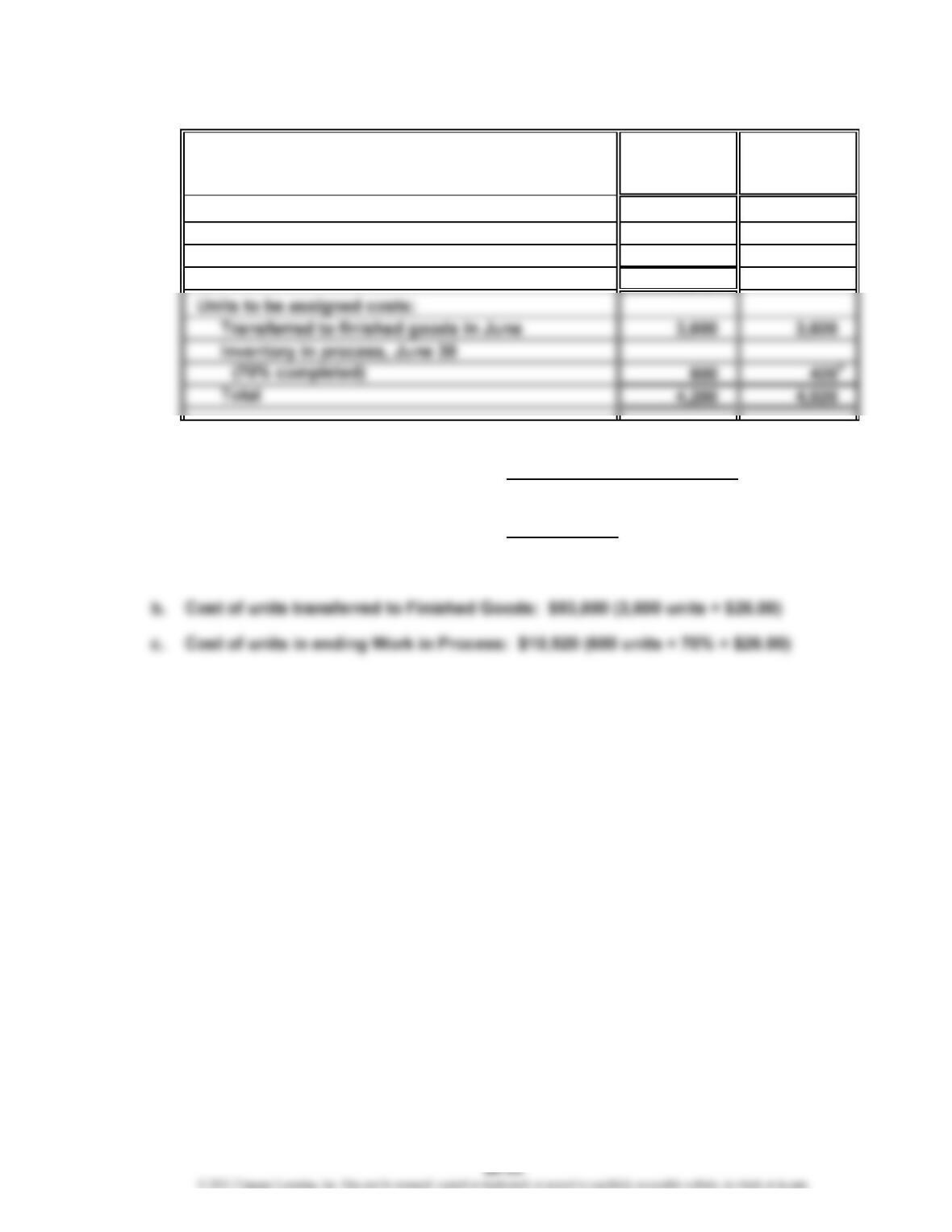

Ex. 20-17

a.

Whole Direct

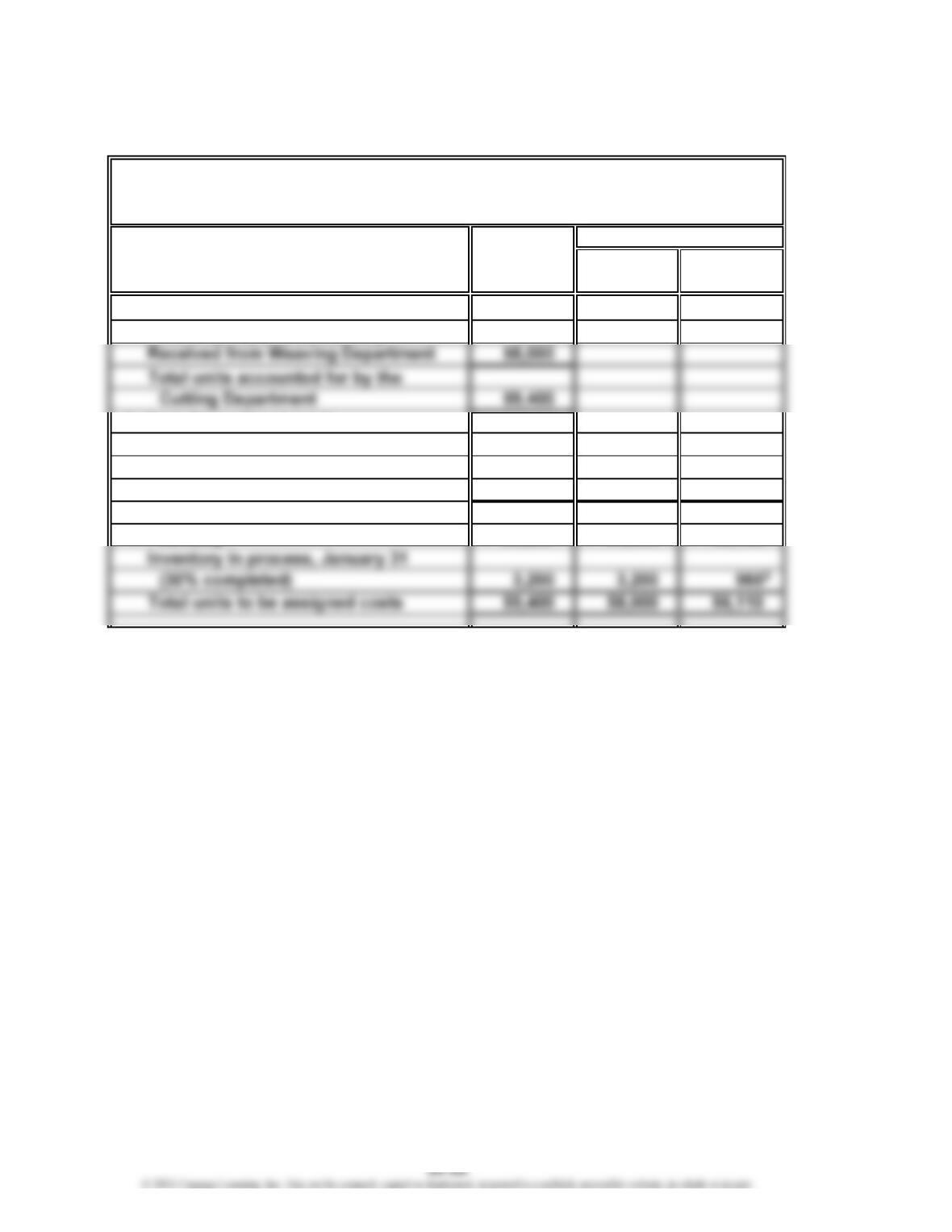

UNITS

Units Materials Conversion

Units charged to production:

Inventory in process, January 1 1,400

Units to be assigned costs:

Inventory in process, January 1

(75% completed) 1,400 0350

Started and completed in January 54,800 54,800 54,800

Transferred to finished goods in

January 56,200 54,800 55,150

1

1,400 units × (100% – 75%)

2

58,000 units – 3,200 units

3

3,200 units × 30%

Karachi Carpet Company

Cost of Production Report—Cutting Department

For the Month Ended January 31

Equivalent Units

1

2

CHAPTER 20 Process Cost Systems

Ex. 20-17 (Concluded)

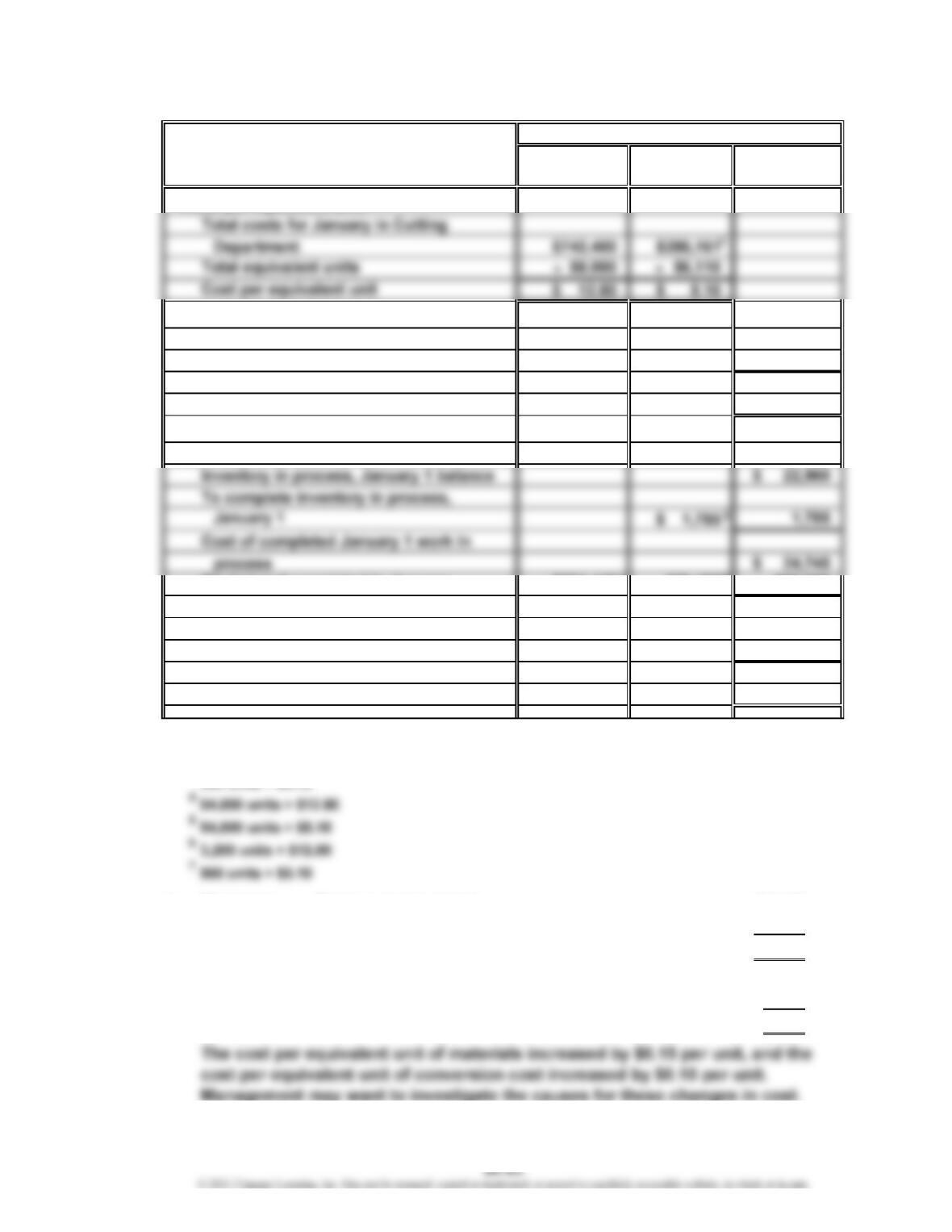

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

Costs assigned to production:

Inventory in process, January 1 $ 22,960

Costs incurred in January 1,028,561

Total costs accounted for by the

Cutting Department $1,051,521

Cost allocated to completed and

partially completed units:

Started and completed in January $701,440 279,480 980,920

Transferred to finished goods in

January $1,005,665

Inventory in process, January 31 40,960 4,896 45,856

Total costs assigned by the Cutting

Department $1,051,521

1

$134,550 + $151,611

2

$742,400 + $134,550 + $151,611

3

b. Materials: From current period………………………………………

…

From beginning inventory………………………………

…

Increase……………………………………………………

…

Conversion: From current period………………………………………

…

From beginning inventory………………………………

…

Increase……………………………………………………

…

$5.10

5.00

$0.10

Costs

$12.80

12.65

$ 0.15

4

5

67

2

CHAPTER 20 Process Cost Systems

Ex. 20-18

a. 1. Work in Process—Casting Department 350,000

Materials—Alloy 350,000

*

$19,840 × 150%

3. Work in Process—Machining Department* 402,684

Work in Process—Casting Department 402,684

*

Supporting calculations:

Cost of 2,530 transferred-out pounds:

Supporting equivalent unit and cost per equivalent unit calculations:

Whole Units Materials Conversion

Inventory in process, May 1

(60% completed) 230 0 92

Started and completed in May 2,300 2,300 2,300

1

230 units × (100% – 60%)

2

2,530 units – 230 units

3

230 units + 2,500 units – 2,530 units

4

200 units × 44%

Equivalent Units

1

2

CHAPTER 20 Process Cost Systems

Ex. 20-18 (Concluded)

b. $29,760, determined as follows:

Direct materials (200 × $140)……………………………

…

$28,000

Conversion (200 × 44% × $20)…………………………… 1,760

$29,760

or $29,760 = $32,844 + $350,000 + $49,600 – $402,684

c. Materials: From current period…………………………………… $140

From beginning inventory……………………………

…

132

Increase…………………………………………………

…

$8

…

…

CHAPTER 20 Process Cost Systems

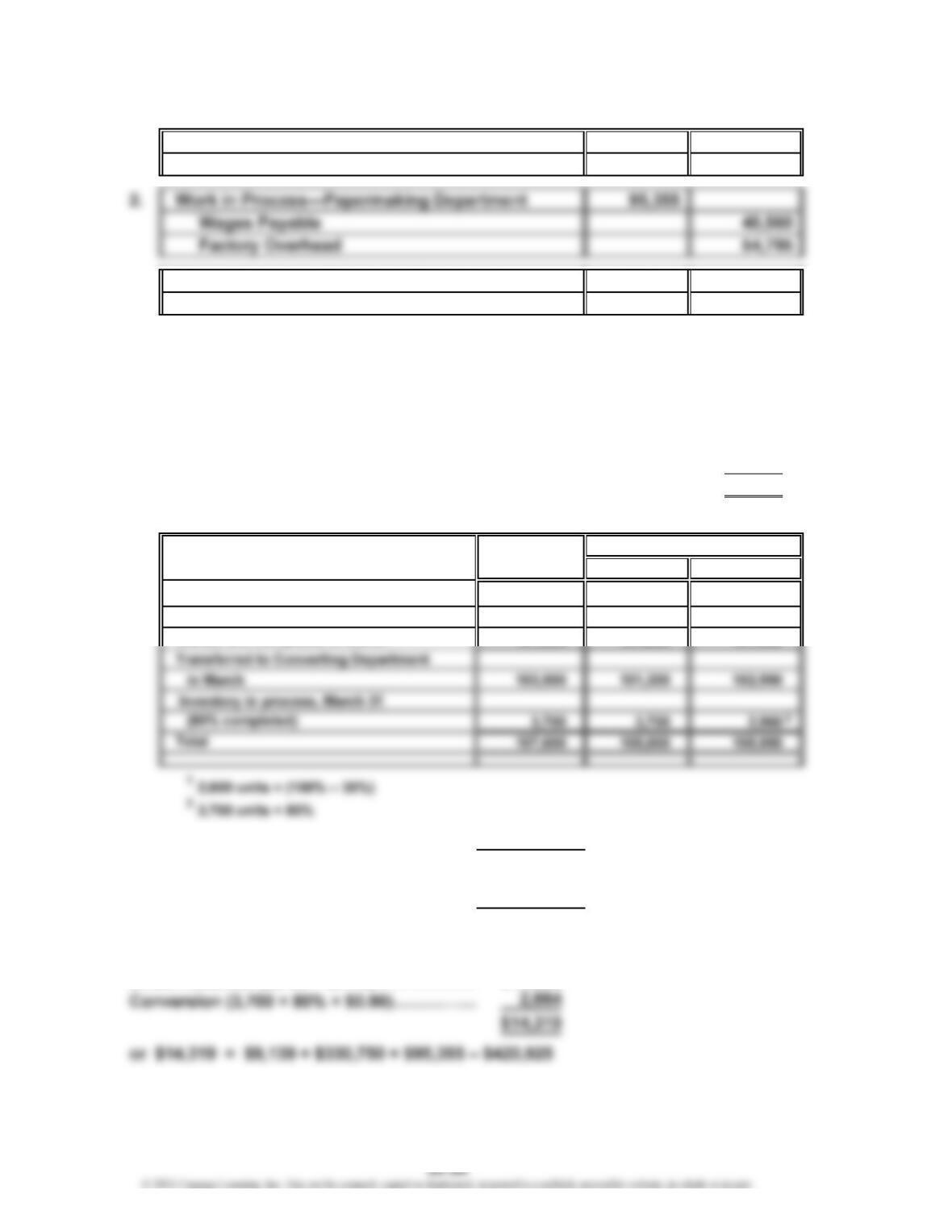

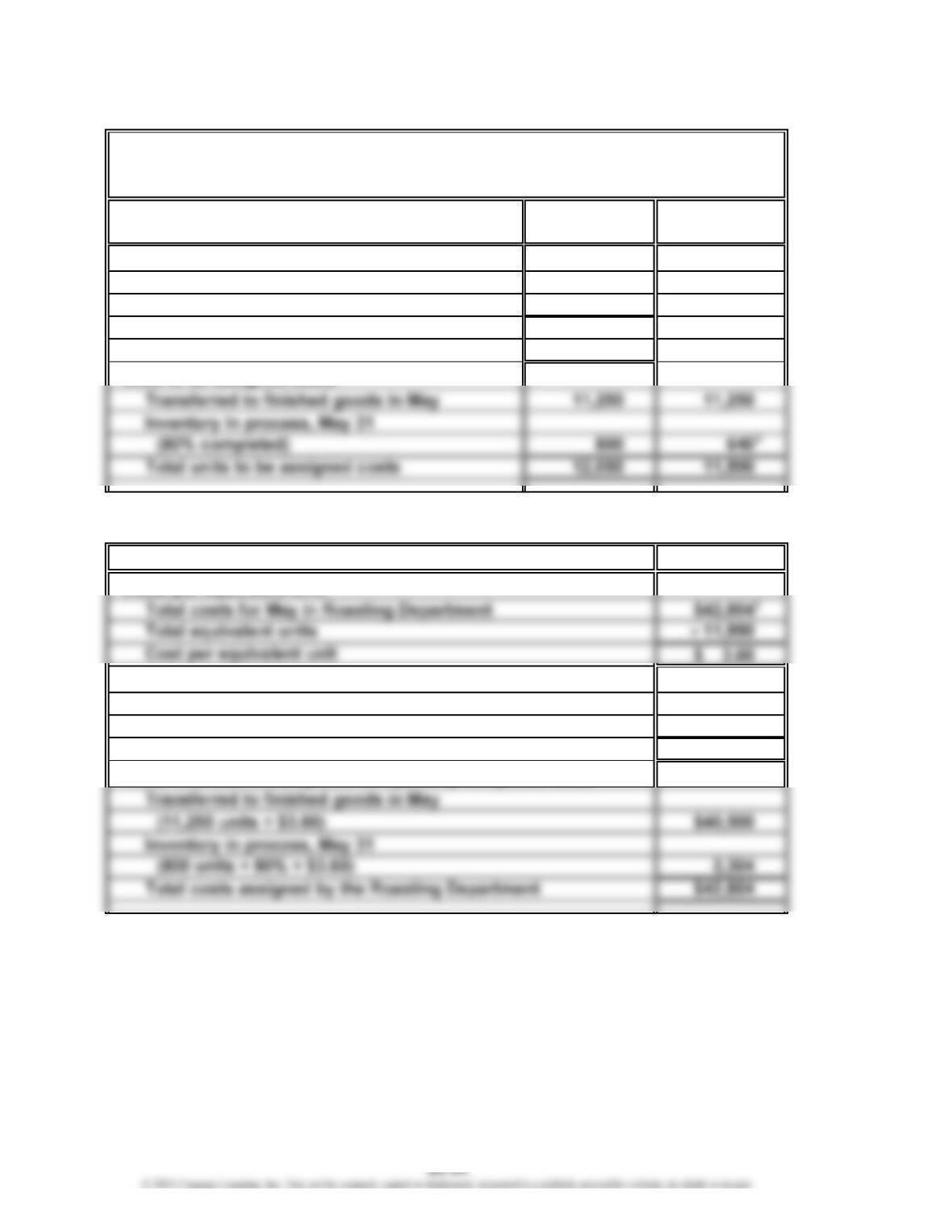

Ex. 20-19

a. 1. Work in Process—Papermaking Department 330,750

Materials—Pulp 330,750

3. Work in Process—Converting Department* 420,925

Work in Process—Papermaking Department 420,925

*

Supporting calculations:

Cost of 103,900 transferred-out units:

Inventory in process, March 1……………………………………………………… $ 9,139

Cost to complete March 1 inventory:

1,690 units × $0.90/unit (see calculations below)……………………………

…

1,521

Pounds started and completed in March

[101,300 units × ($3.15 + $0.90)]………………………………………………

…

410,265

Transferred to Converting Department…………………………………………

…

$420,925

Supporting equivalent unit and cost per equivalent unit calculations:

Whole Units Materials Conversion

Inventory in process, March 1

(35% completed) 2,600 0 1,690

Started and completed in March 101,300 101,300 101,300

$330,750

105,000

$95,355

105,950

b. $14,319; determined as follows:

Direct materials (3,700 × $3.15)……………… $11,655

Cost per equivalent unit of conversion: = $0.90 per unit

Equivalent Units

= $3.15 per unitCost per equivalent unit of materials:

1

CHAPTER 20 Process Cost Systems

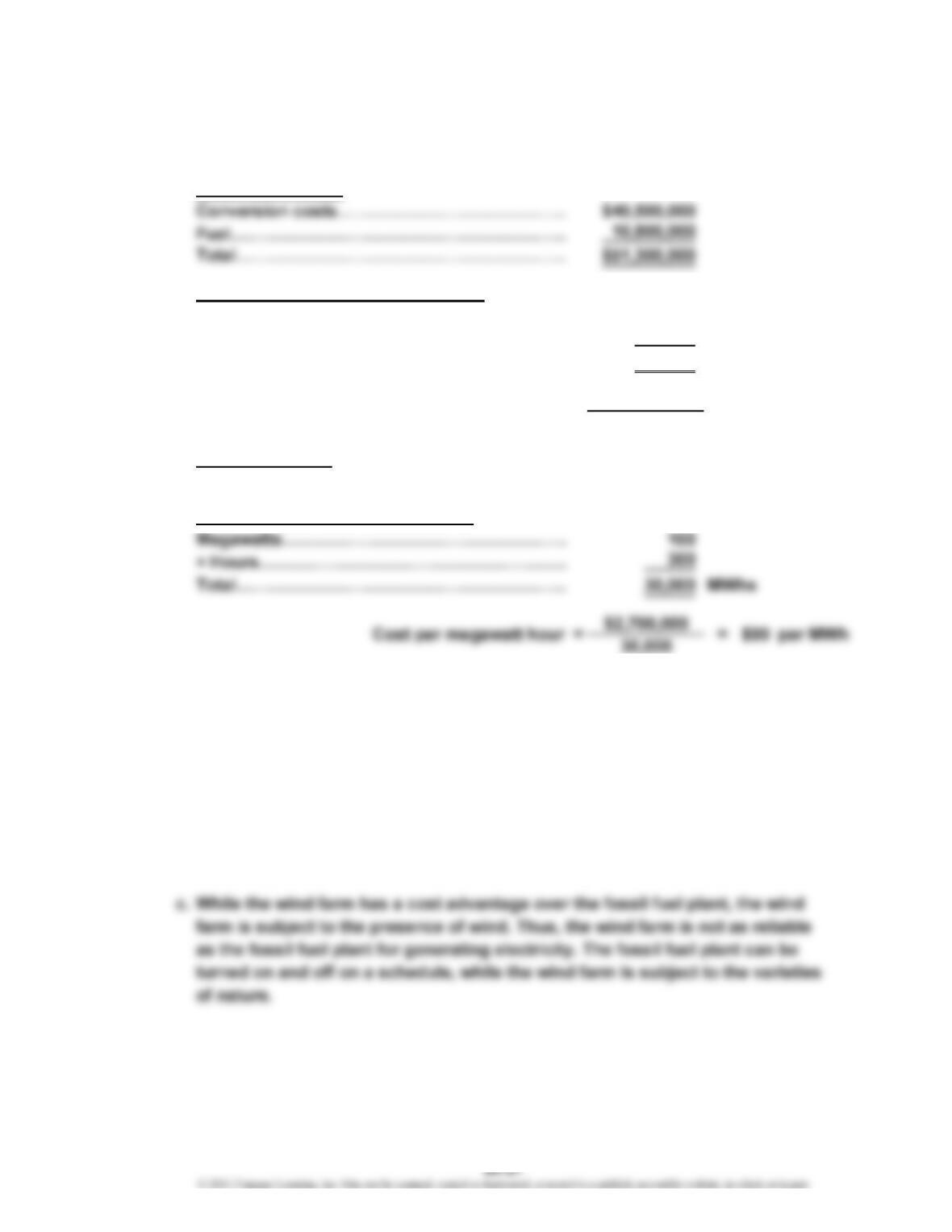

Ex. 20-20

a. Cost per megawatt hour (MWh):

Fossil plant costs:

Fossil plant megawatt hours (MWh):

Megawatts…………………………………………… 900

× Hours………………………………………………

…

600

Total…………………………………………………

…

540,000 MWhs

$51,300,000

540,000

Wind farm costs:

Conversion costs…………………………………

…

$2,700,000

Wind farm megawatt hours (MWh):

…

…

The wind farm cost per megawatt hour was $90, compared to the fossil plant

cost of $95 per megawatt hour. The wind farm is the less costly resource.

Note: These figures are close to the national average and show the slight

advantage of wind farms.

b. Equivalent units of production are calculated when there are beginning or

ending inventories that are partially completed to either coversion costs or

materials. There are no beginning or ending inventories for generating

electricity; thus, there is no need to determine equivalent units of production.

$95 per MWh ==Cost per megawatt hour

…

…

CHAPTER 20 Process Cost Systems

Ex. 20-21

Memo

To: Production Manager

The cost of production report is used to identify the cost per case for each of the

four flavors as follows:

Orange Cola Lemon-Lime Root Beer

Total cost

$19,125 $391,800 $324,000 $36,000

Orange Cola Lemon-Lime Root Beer

Concentrate

$1.85 $2.15 $2.10 $1.90

Water

0.50 0.50 0.50 0.50

Sugar

1.20 1.20 1.20 1.20

Bottles

2.20 2.20 2.20 2.20

Flavor changeover

1.20 0.08 0.08 2.50

Conversion cost

0.70 0.40 0.40 0.70

Total cost per case

$7.65 $6.53 $6.48 $9.00

This table indicates that the concentrate per case is actually less for orange and root

beer than for cola and lemon-lime. This is because the concentrate supplier charges

a higher price for the more popular flavors. The costs per case for water, sugar, and

bottles are the same for each flavor. However, the costs per case for changeover are

much greater for orange and root beer than for the other two flavors. In addition, the

conversion costs per unit for orange and root beer are $0.30 higher than for cola and

lemon-lime. These last two cost elements are sufficient to cause the cost per case of

orange and root beer to be greater than cola and lemon-lime.

Cost per Case by Cost Element

CHAPTER 20 Process Cost Systems

Ex. 20-22

The solution to this exercise is to determine if the cost per pound trends in paper

stock, conversion, and coating costs are remaining stable over time. The

following table can be developed from the data:

a.

January February March April May June

Paper stock

($ ÷ pounds output) $0.70 $0.70 $0.70 $0.70 $0.70 $0.70

Coating

The cost per pound information is determined by dividing the costs by the

pounds transferred out. The yield is determined by dividing the pounds

transferred out by the pounds input.

b. Operator 1 believes that energy consumption is becoming less efficient. The

energy cost is part of the conversion cost. The conversion cost per output

pound has remained constant for the six months. If the energy efficiency were

declining, it would take more energy per pound of output over time. Thus, we

would expect to see the conversion rate per pound increasing if Operator 1

were correct.

CHAPTER 20 Process Cost Systems

Ex. 20-23

The Hawkeye Machining managers are displaying typical fears to a lean manufacturing

system. Lean manufacturing removes the safety provided by materials, in-process,

and finished goods inventory balances. Indeed, these types of comments reflect

conventional manufacturing philosophy, which views inventory as a necessary

buffer against surprises and other unwelcome events. Lean manufacturing focuses

on removing the causes that require a need for inventory.

The in-process inventories can be reduced significantly if the underlying manufacturing

processes are made reliable. The director of manufacturing is correct in his observation

but his solution is wrong. The solution is not to increase inventory but to improve the

reliability of the machines so that they do not experience emergency breakdowns.

Thus, the manufacturing operation must be improved to produce the right product, in

the right quantities, at the right quality, and at the right time. Only with this level of

reliability can a plant responsibly remove in-process inventories from the system.

In other words, inventory covers a “multitude of sins.” When the “sins” are removed,

the inventory can be removed.

Appendix Ex. 20-24

a. and b.

a. Whole b. Equivalent Units

Units of Production

Units to be accounted for:

Beginning work in process 1,900

Units started during period 15,100

Total 17,000

1

CHAPTER 20 Process Cost Systems

Appendix Ex. 20-25

a. Drawing Department

Whole Equivalent Units

Units of Production

Units to be accounted for:

Beginning work in process 500

Units started during period 11,600

Total 12,100

1

11,400 units – 500 units + 700 units

2

55% × 700 units

b. Winding Department

Whole Equivalent Units

Units of Production

Units to be accounted for:

Beginning work in process 350

Units started during period 11,400

Total 11,750

1

10,950 units – 350 units + 800 units

2

25% × 800 units

1

1

CHAPTER 20 Process Cost Systems

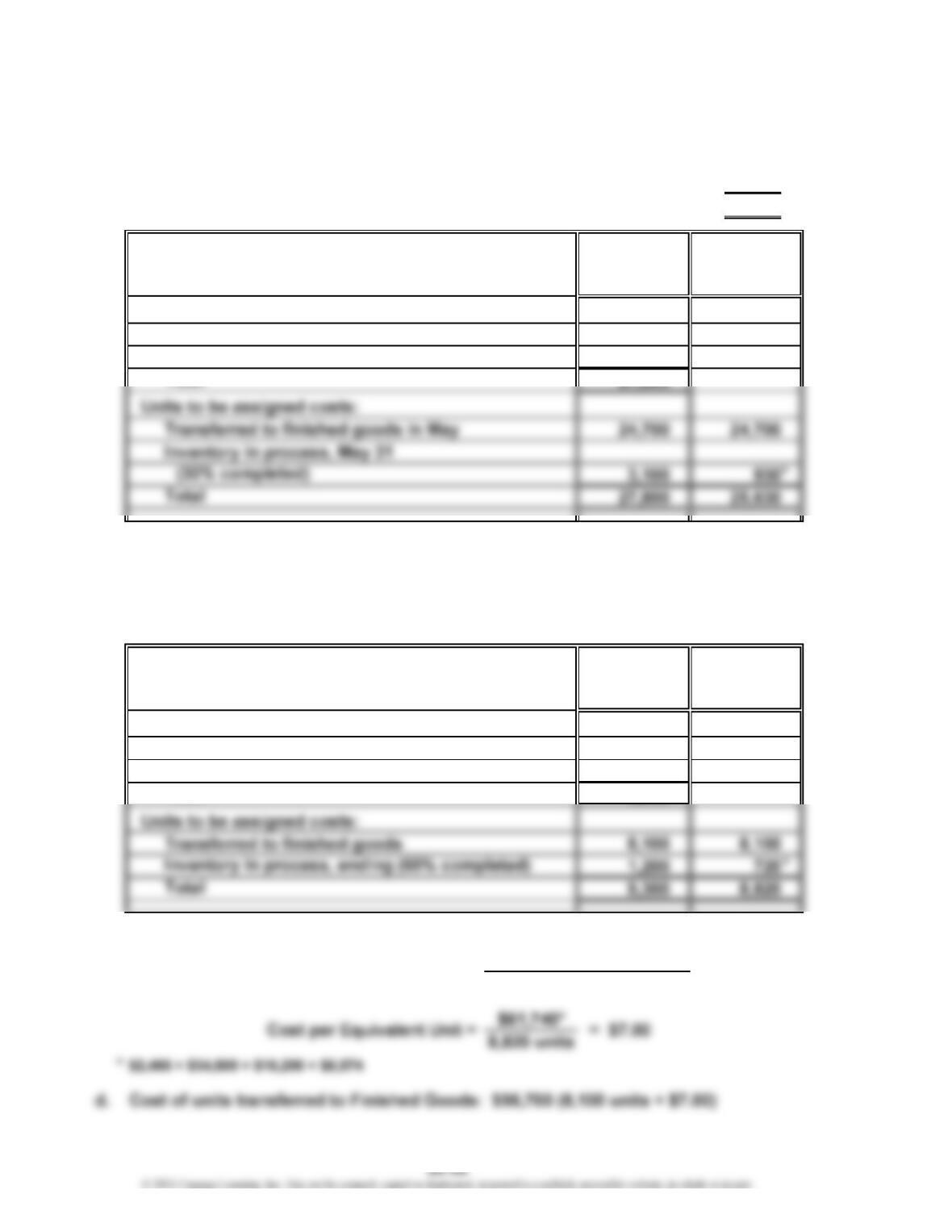

Appendix Ex. 20-26

a. Units in process, May 1…………………………………………………………

…

4,200

Units placed into production for May………………………………………… 23,600

Less units finished during May………………………………………………

…

(24,700)

Units in process, May 31………………………………………………………

…

3,100

b.

Equivalent

Whole Units of

Units Production

Units to be accounted for:

Beginning work in process 4,200

Units started during the period 23,600

*

30% × 3,100 units

Appendix Ex. 20-27

a. and b.

Equivalent

Whole Units of

Units Production

Units to be accounted for:

Beginning work in process 900

Units started during the period 8,400

Total 9,300

*

60% × 1,200 units

e. Cost of units in ending Work in Process: $5,040 (1,200 units × 60% × $7.00)

Total Equivalent Units

c. Cost per Equivalent Unit =

Total Production Costs

CHAPTER 20 Process Cost Systems

Appendix Ex. 20-28

a.

Equivalent

Whole Units of

Units Production

Units to be accounted for:

Beginning work in process 500

Units started during the period 3,700

Total 4,200

*

70% × 600 units

$104,520**

4,020 units

**

$5,000 + $49,200 + $25,200 + $25,120

Total Equivalent Units

Cost per Equivalent Unit =

Cost per Equivalent Unit = = $26.00

Total Production Costs

CHAPTER 20 Process Cost Systems

Appendix Ex. 20-29

Whole Equivalent Units

UNITS Units of Production

Units to account for during production:

Inventory in process, May 1 1,150

Received from materials storeroom 10,900

Total units accounted for by the

Roasting Department 12,050

*

80% × 800 units

COSTS Costs

Costs assigned to production:

Inventory in process, May 1 $ 1,700

Costs incurred in May 41,104

Total costs accounted for by the Roasting Department $42,804

Costs allocated to completed and partially completed units:

1

$1,700 + $28,600 + $12,504

2

$28,600 + $12,504

Highlands Coffee Company

Cost of Production Report—Roasting Department

For the Month Ended May 31

2

CHAPTER 20 Process Cost Systems

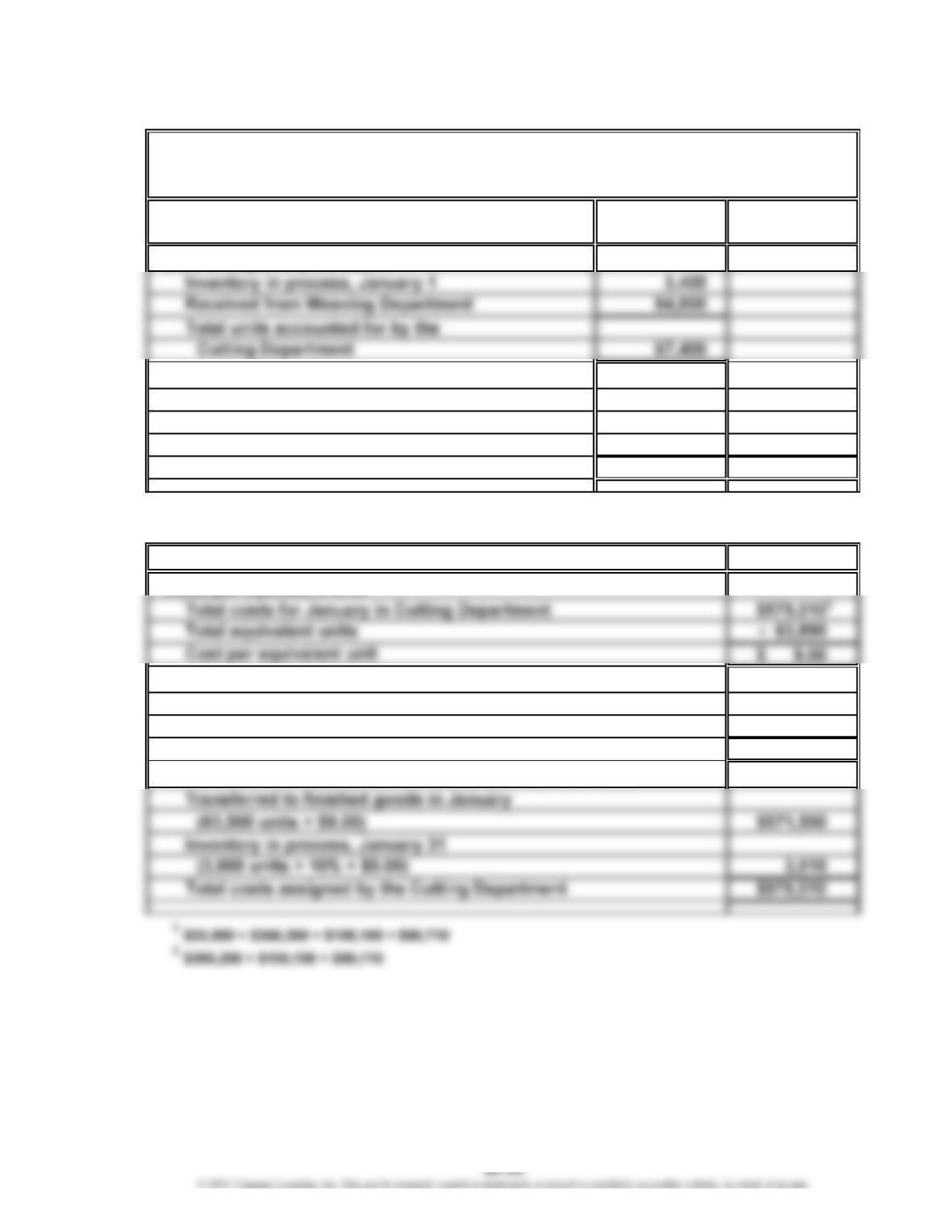

Appendix Ex. 20-30

Whole Equivalent Units

UNITS Units of Production

Units charged to production:

Units to be assigned costs:

Transferred to finished goods in January 63,500 63,500

Inventory in process, January 31

(10% completed) 3,900 390

Total units to be assigned costs 67,400 63,890

*

10% × 3,900 units

COSTS Costs

Costs assigned to production:

Inventory in process, January 1 $ 23,000

Costs incurred in January 552,010

Total costs accounted for by the Cutting Department $575,010

Costs allocated to completed and partially completed units:

Dalton Carpet Company

Cost of Production Report—Cutting Department

For the Month Ended January 31

2

*

CHAPTER 20 Process Cost Systems

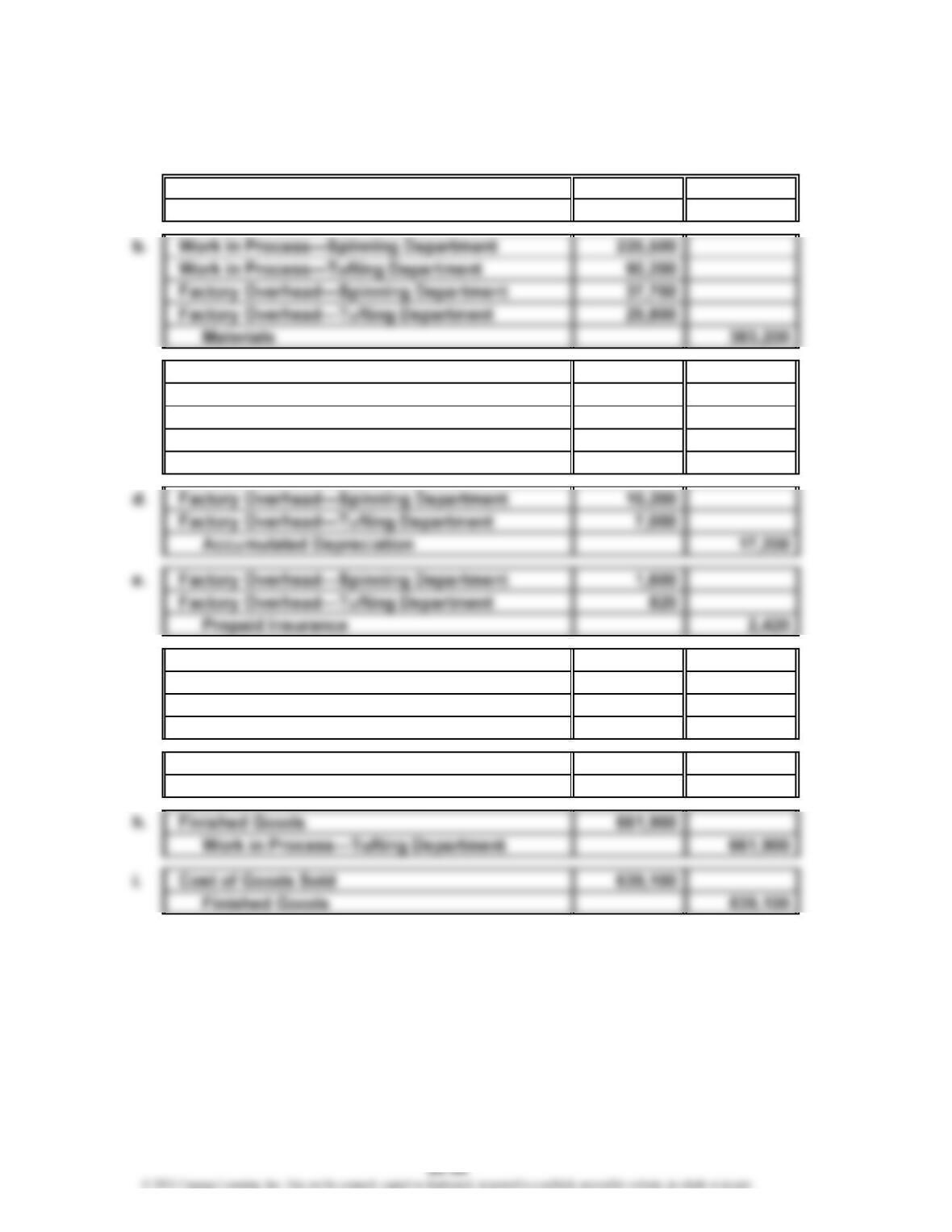

Prob. 20-1A

1. a. Materials 410,000

Accounts Payable 410,000

c. Work in Process—Spinning Department 151,700

Work in Process—Tufting Department 80,300

Factory Overhead—Spinning Department 14,900

Factory Overhead—Tufting Department 7,500

Wages Payable 254,400

f. Work in Process—Spinning Department 64,600

Work in Process—Tufting Department 45,100

Factory Overhead—Spinning Department 64,600

Factory Overhead—Tufting Department 45,100

g. Work in Process—Tufting Department 448,500

Work in Process—Spinning Department 448,500

PROBLEMS

CHAPTER 20 Process Cost Systems

Prob. 20-1A (Concluded)

2.

Work in Work in

Process— Process— Finished

Materials Spinning Dept. Tufting Dept. Goods

Balance, January 1…

…

$ 13,900 $ 28,700 $ 23,400 $ 50,800

Debits…………………

…

410,000 441,800 664,100 661,900

3.

Balance, January 1…

…

Debits…………………

…

Factory Overhead— Factory Overhead—

Spinning Dept. Tufting Dept.

$0 $0

64,400 45,120

12

2

1

CHAPTER 20 Process Cost Systems

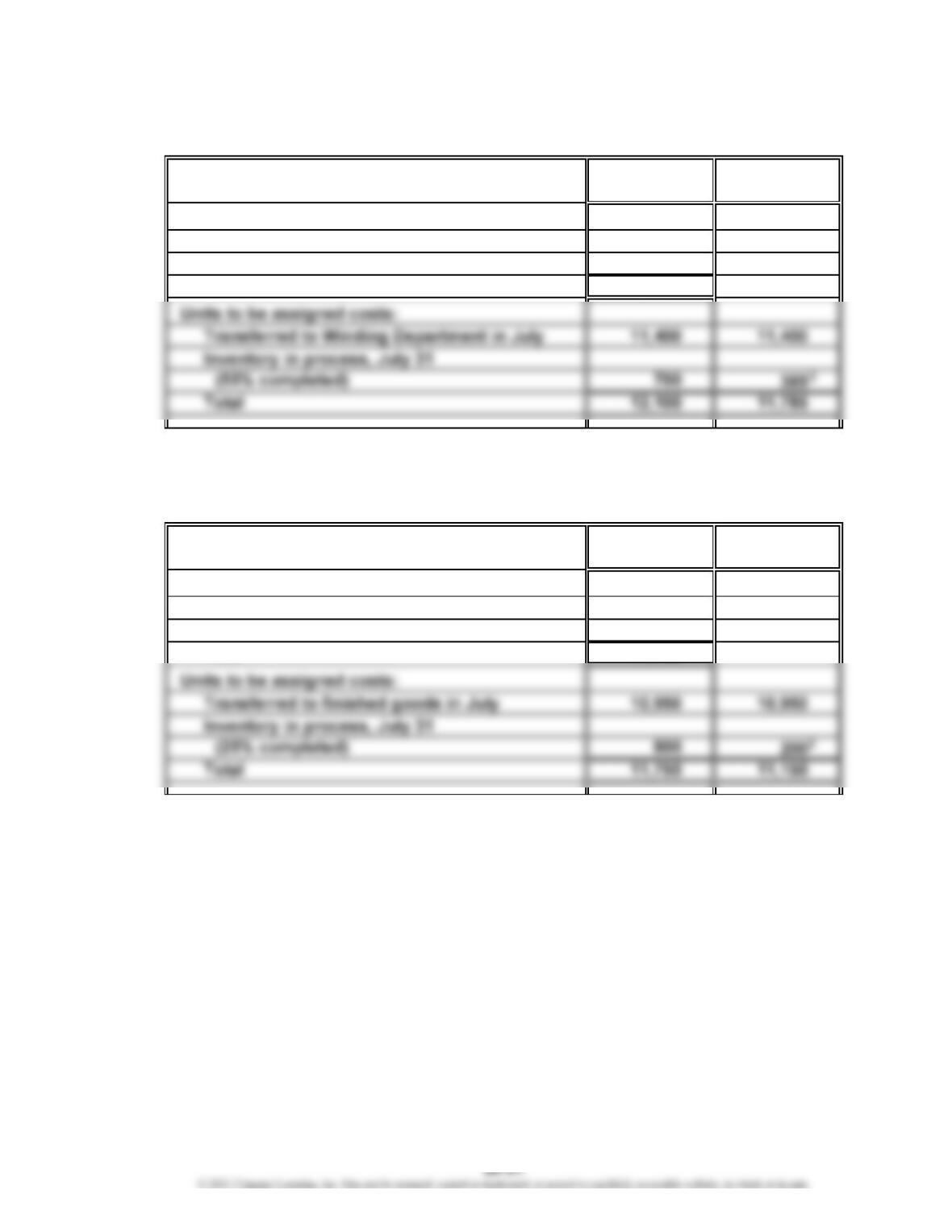

Prob. 20-2A

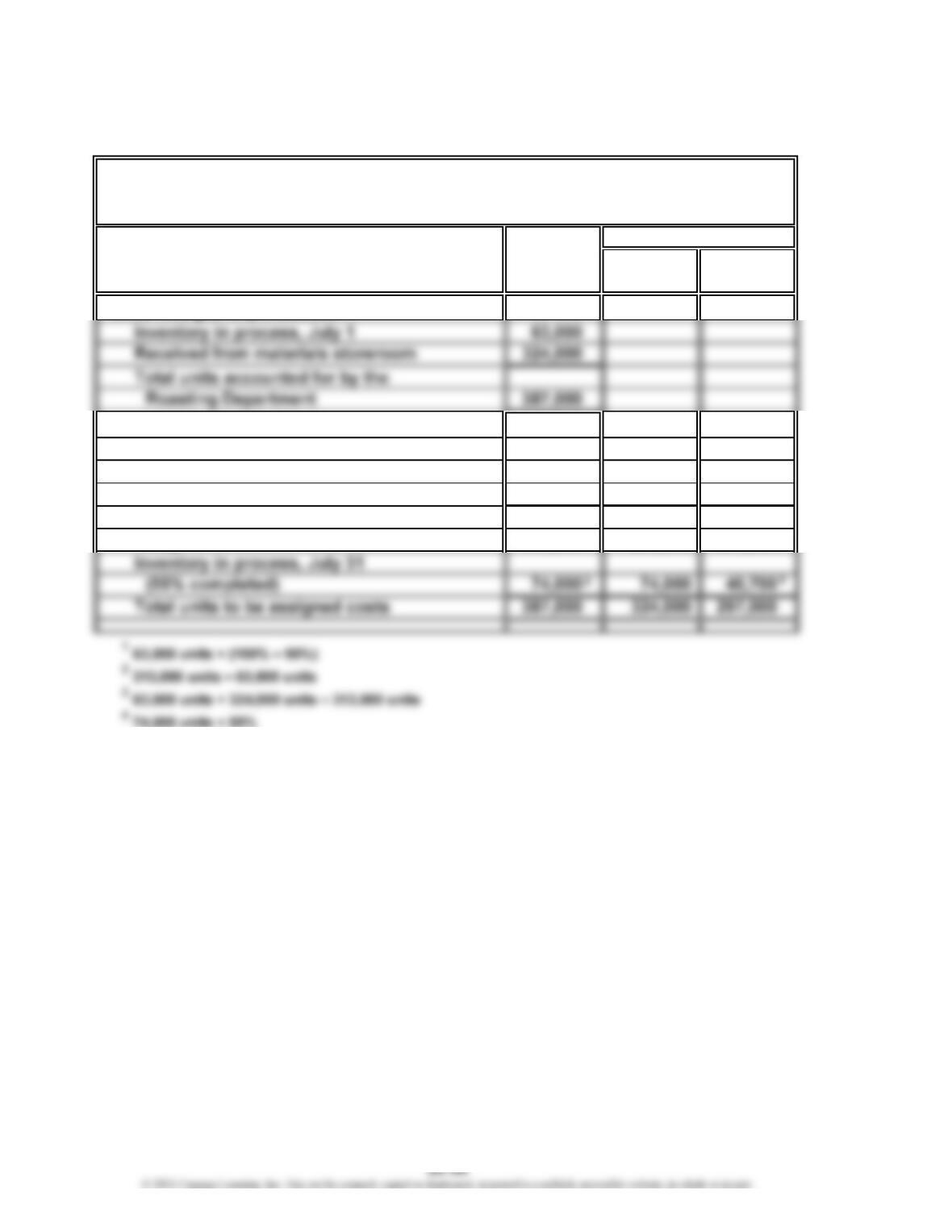

1.

Whole Direct

UNITS Units Materials Conversion

Units charged to production:

Units to be assigned costs:

Inventory in process, July 1

(90% completed) 63,000 06,300

Started and completed in July 250,000 250,000 250,000

Transferred to Packing Department in

July 313,000 250,000 256,300

Mochaccino Express Coffee Company

Cost of Production Report—Roasting Department

For the Month Ended July 31

Equivalent Units

1

2

CHAPTER 20 Process Cost Systems

Prob. 20-2A (Continued)

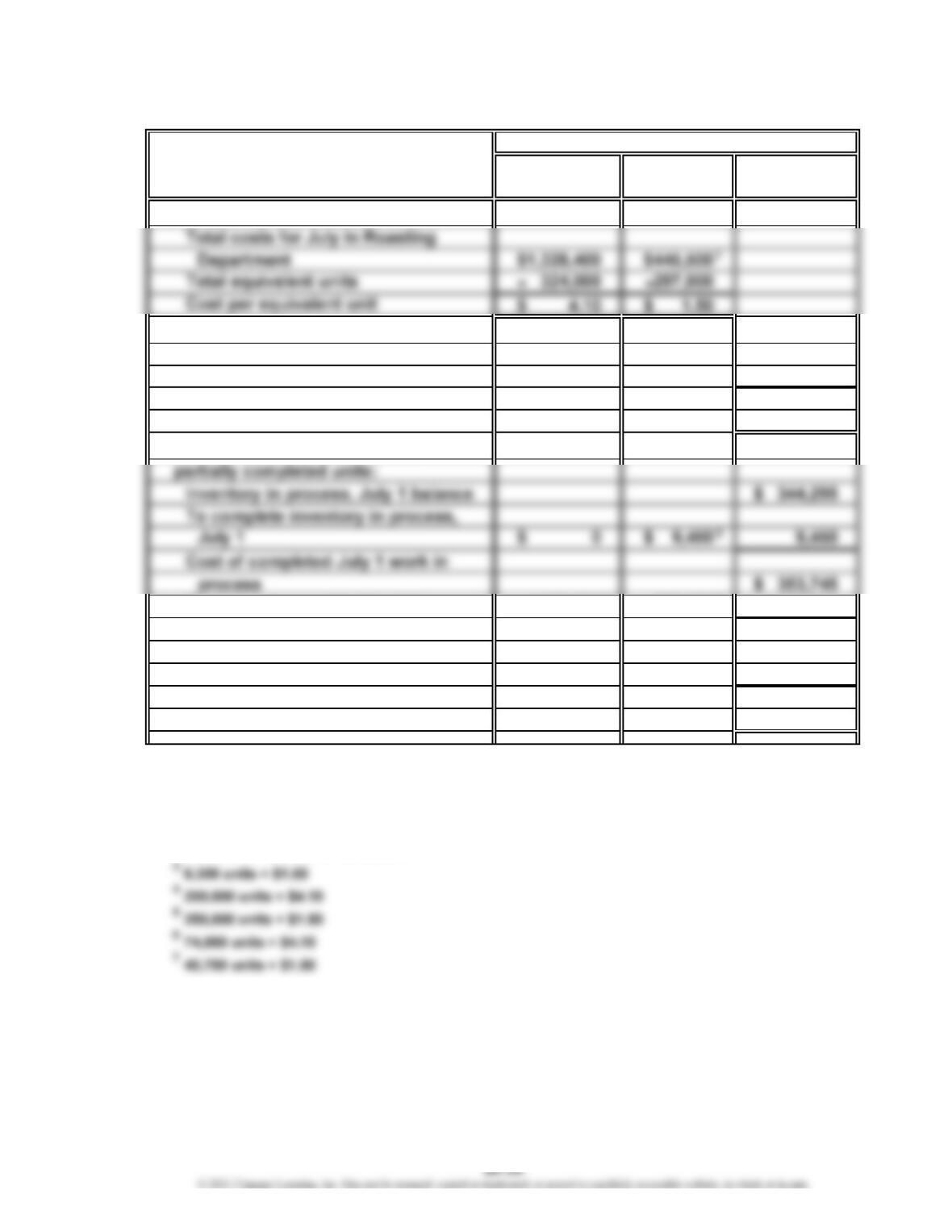

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

Costs assigned to production:

Inventory in process, July 1 $ 344,295

Costs incurred in July 1,773,900

Total costs accounted for by the

Roasting Department $2,118,195

Cost allocated to completed and

Started and completed in July 1,025,000 375,000 1,400,000

Transferred to Packing Department

in July $1,753,745

Inventory in process, July 31 303,400 61,050 364,450

Total costs assigned by the Roasting

Department $2,118,195

Costs transferred to Packing Department: $1,753,745

Work in process, July 31: 74,000 units at a cost of $364,450

1

$325,200 + $120,300

2

$1,328,400 + $325,200 + $120,300

Costs

2

4

5

67

CHAPTER 20 Process Cost Systems

Prob. 20-2A (Concluded)

2. Direct materials cost increased $0.03, from $4.07 in June to $4.10 in July.

Conversion cost decreased $0.05, from $1.55 in June to $1.50 in July.

Computations:

Prob. 20-3A

1.

Whole Direct

UNITS Units Materials Conversion

Units charged to production:

Inventory in process, July 1 900

(3/5 completed) 900 0360

Started and completed in July 14,600 14,600 14,600

Transferred to Packaging Department

in July 15,500 14,600 14,960

White Diamond Flour Company

Cost of Production Report—Sifting Department

For the Month Ended July 31

Equivalent Units

2

1