CHAPTER 20 Process Cost Systems

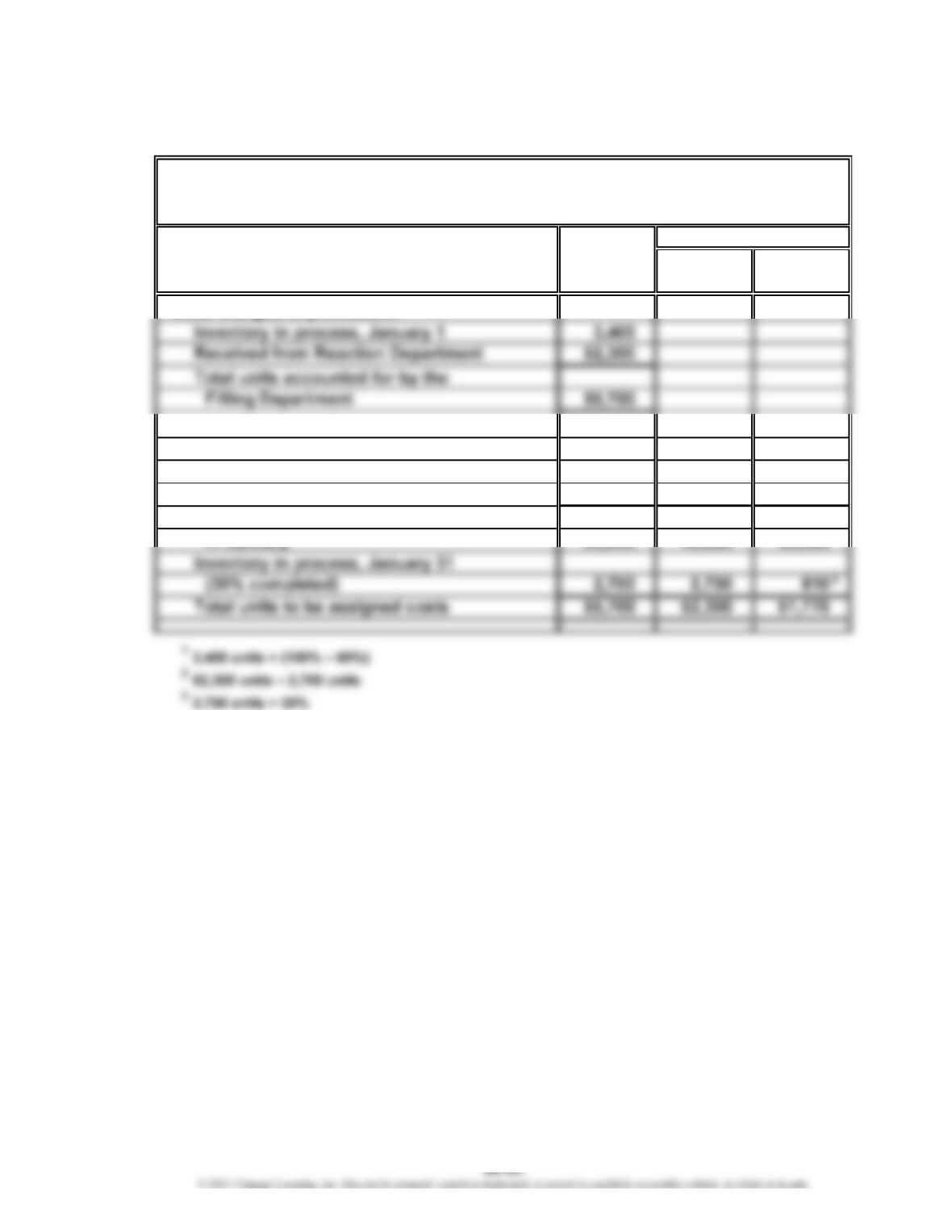

Prob. 20-3A (Continued)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

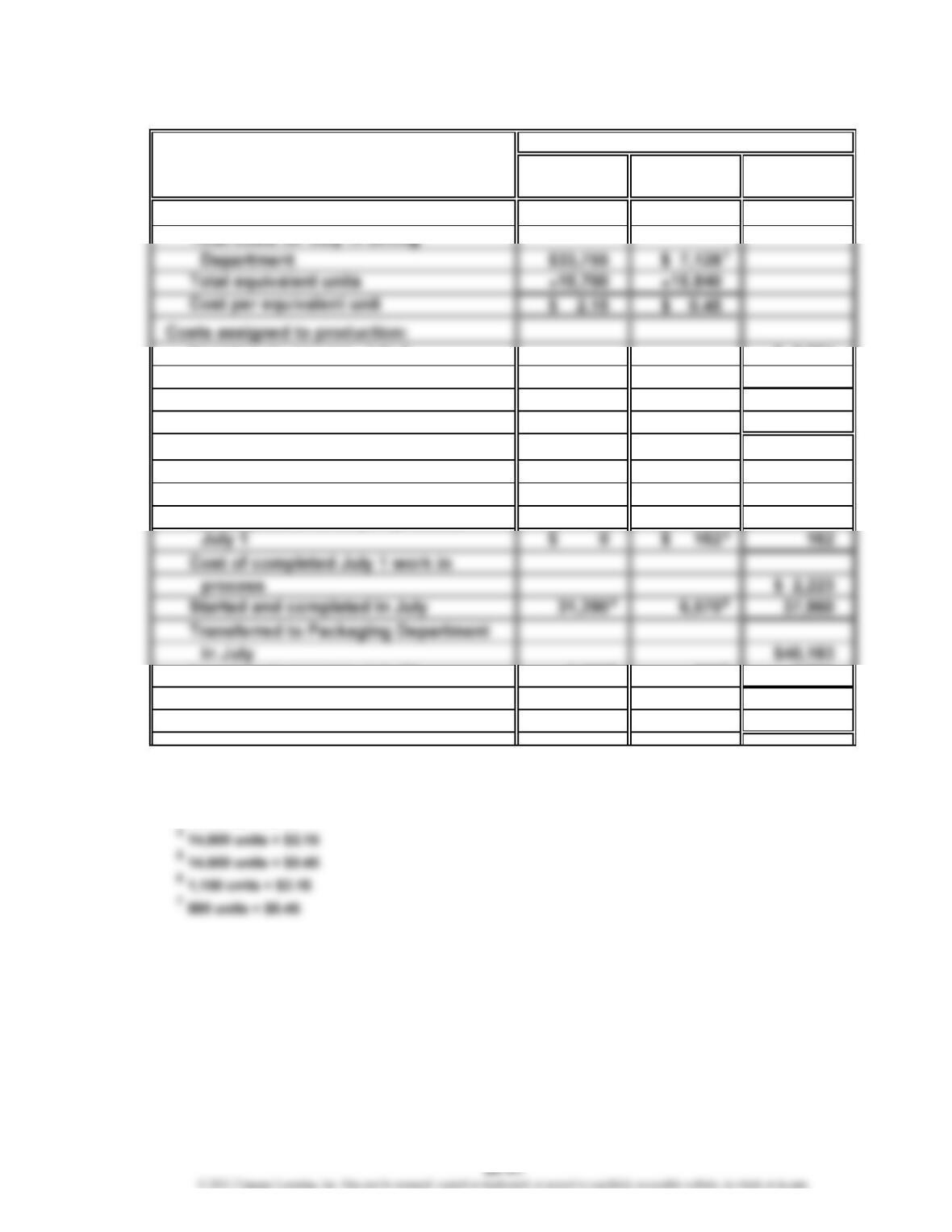

Inventory in process, July 1 $ 2,061

Costs incurred in July 40,883

Total costs accounted for by the

Sifting Department $42,944

Cost allocated to completed and

partially completed units:

Inventory in process, July 1 balance $ 2,061

To complete inventory in process,

Inventory in process, July 31 2,365 396 2,761

Total costs assigned by the Sifting

Department $42,944

1

$4,420 + $2,708

2

$33,755 + $4,420 + $2,708

3

360 units × $0.45

Costs

2

67

CHAPTER 20 Process Cost Systems

Prob. 20-3A (Concluded)

2. Work in Process—Sifting Department 33,755

Work in Process—Milling Department 33,755

Work in Process—Packaging Department 40,183

Work in Process—Sifting Department 40,183

4. The cost of production report may be used as the basis for allocating product costs

between Work in Process and Transferred-Out (or Finished) Goods. The report can

also be used to control costs by holding each department head responsible for the

units entering production and the costs incurred in the department. Any differences

in unit product costs from one month to another, such as those in part (3), can be

studied carefully and any significant differences investigated.

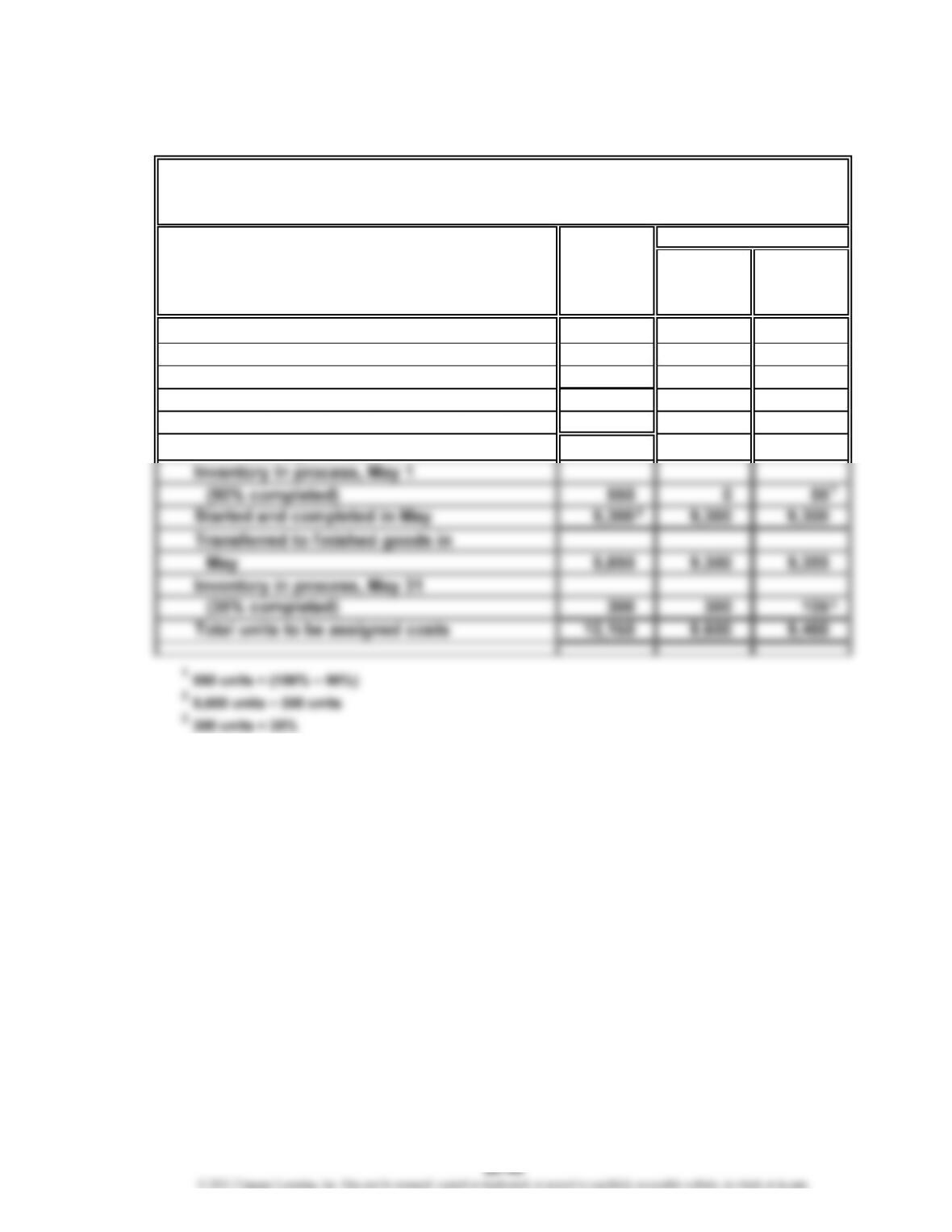

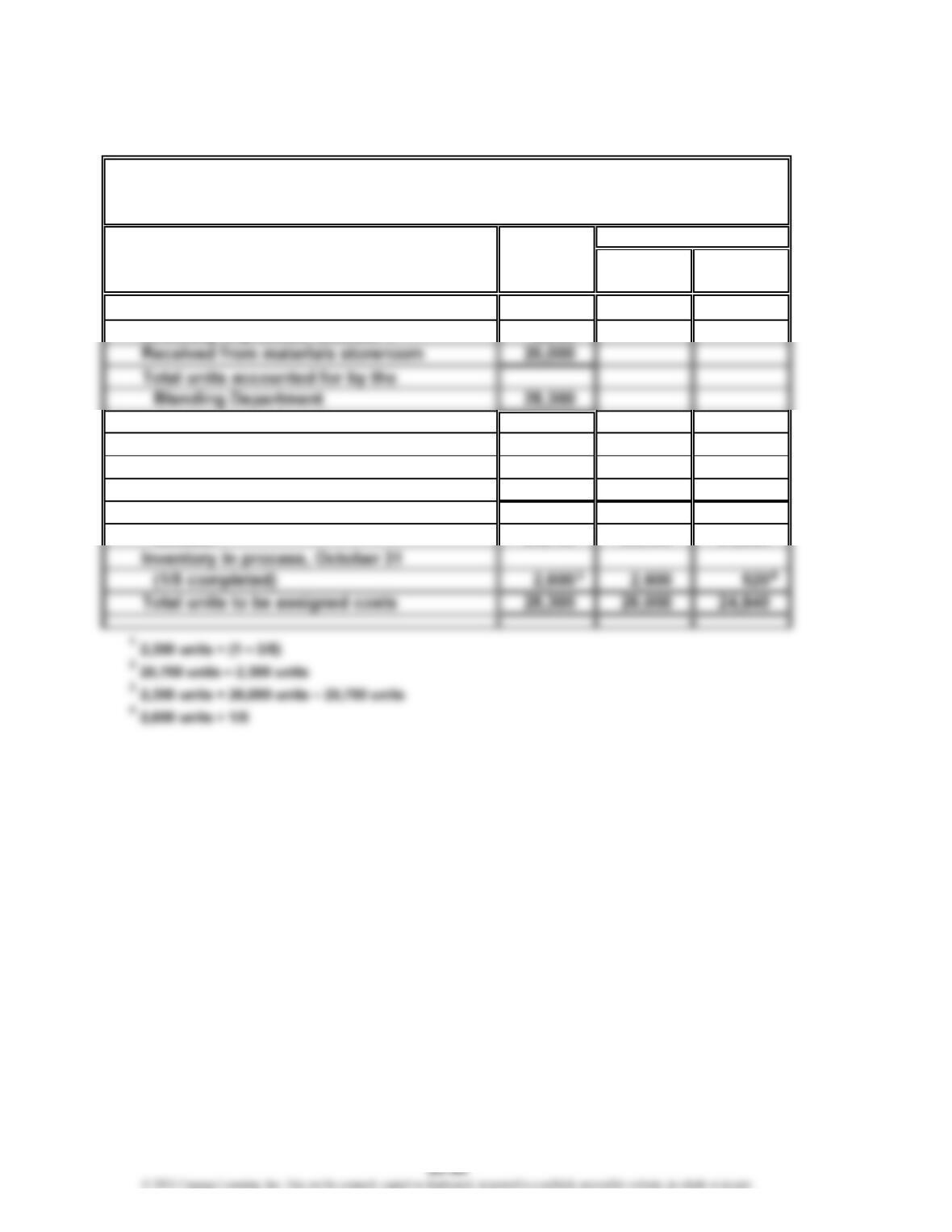

Prob. 20-4A

1. and 2.

Item Dr. Cr. Dr. Cr.

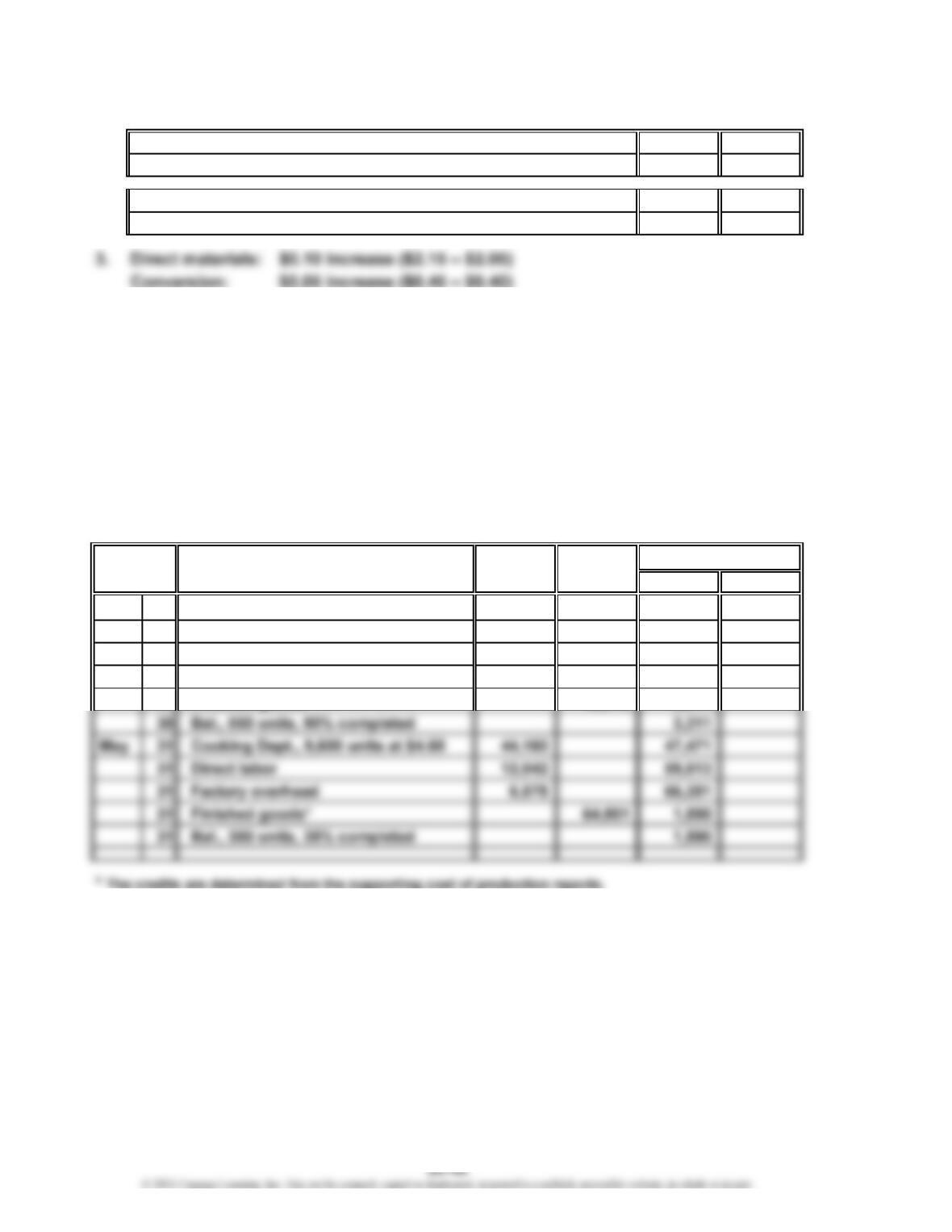

Apr. 1 Bal., 800 units, 30% completed 3,860

30 Cooking Dept., 7,800 units at $4.40 34,320 38,180

30 Direct labor 8,562 46,742

30 Factory overhead 6,387 53,129

30 Finished goods* 49,818 3,311

*

The credits are determined from the supporting cost of production reports.

Date

Balance

Work in Process—Filling

CHAPTER 20 Process Cost Systems

Prob. 20-4A (Continued)

1.

Direct

Whole Materials Conversion

UNITS Units (a) (a)

Units charged to production:

Units to be assigned costs:

Inventory in process, April 1

(30% completed) 800 0560

Started and completed in April 7,250 7,250 7,250

Hearty Soup Co.

Cost of Production Report—Filling Department

For the Month Ended April 30

Equivalent Units

1

2

CHAPTER 20 Process Cost Systems

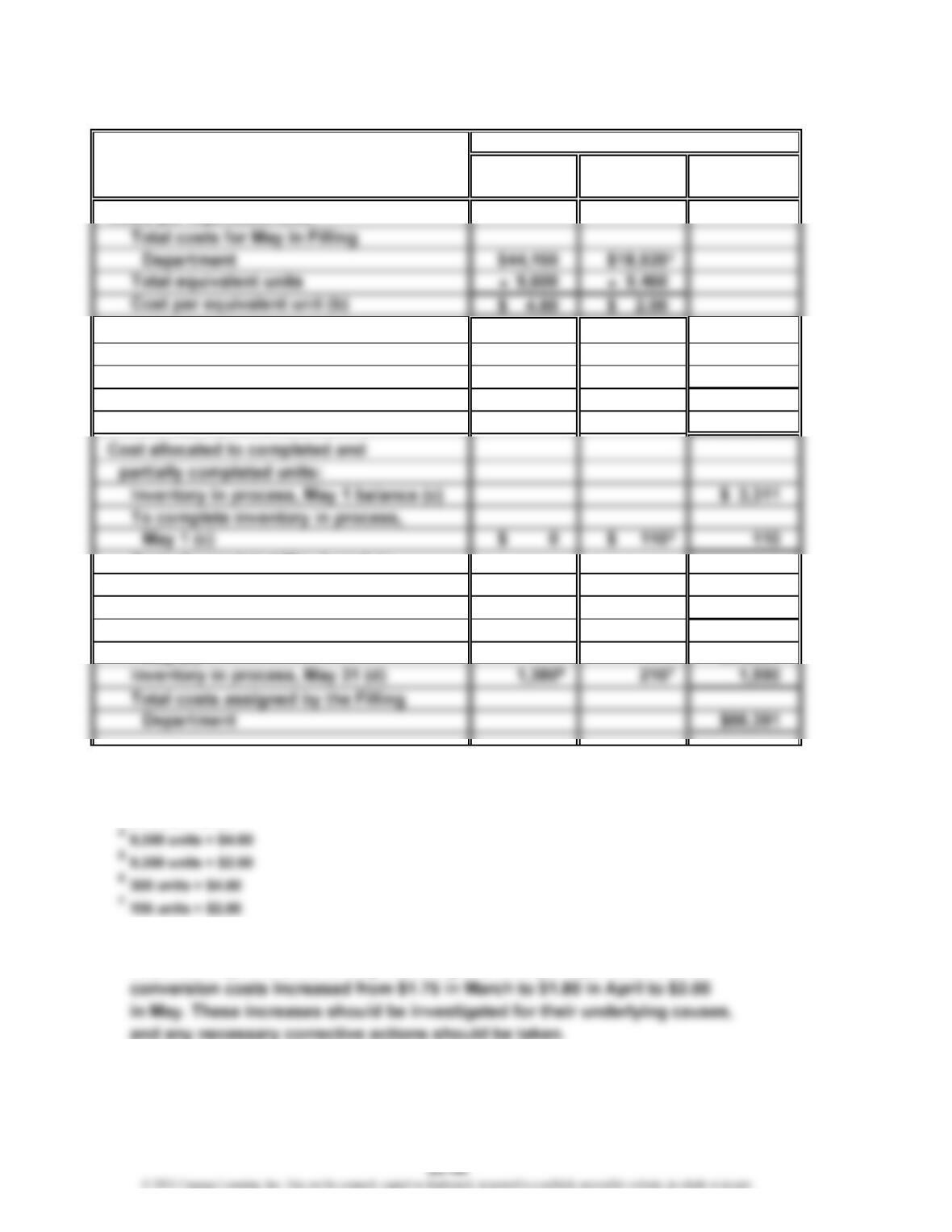

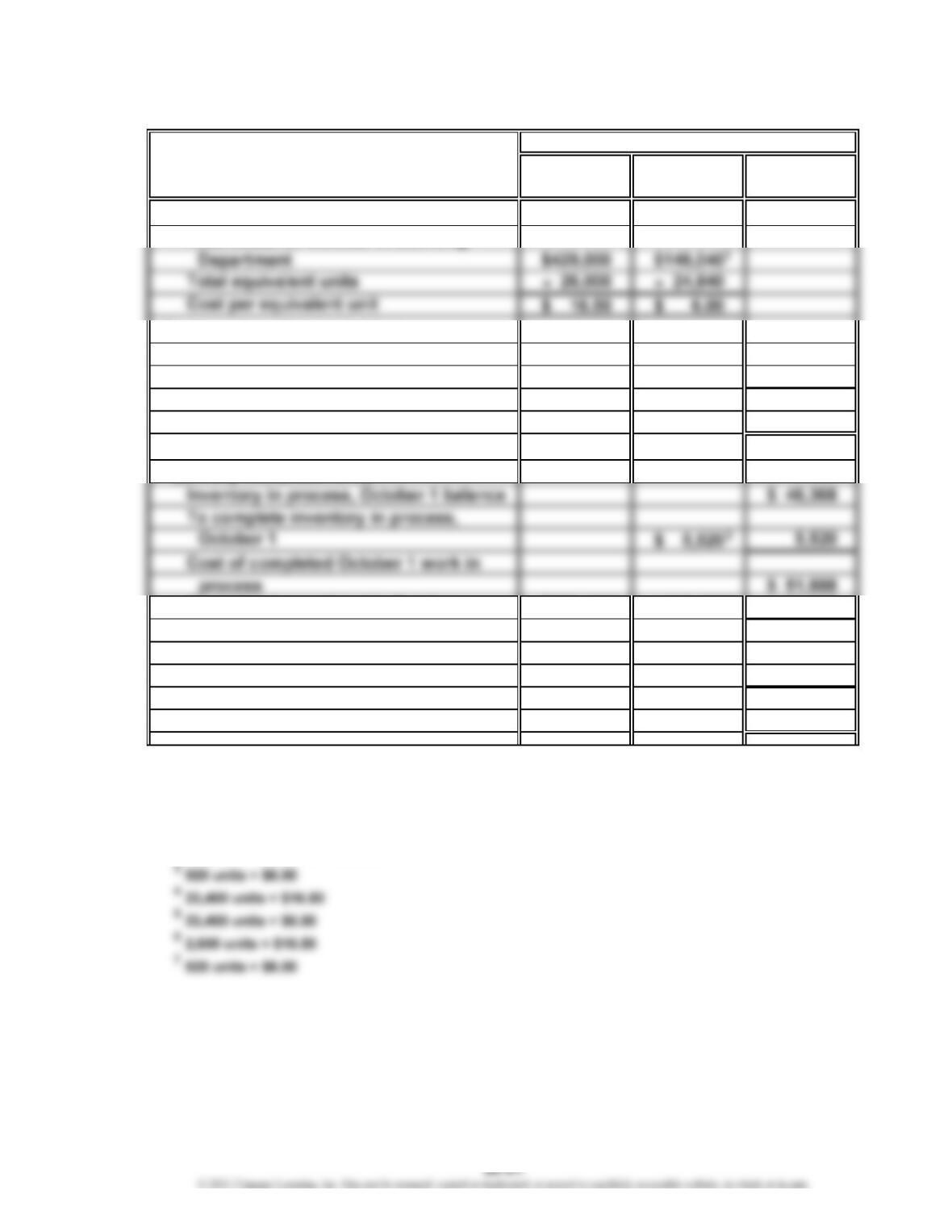

Prob. 20-4A (Continued)

Direct

COSTS Materials Conversion Total

Costs assigned to production:

Inventory in process, April 1 $ 3,860

Costs incurred in April 49,269

Total costs accounted for by the

Filling Department $53,129

Started and completed in April (c) 31,900 13,050 44,950

Transferred to finished goods

in April (c) $49,818

Inventory in process, April 30 (d) 2,420 891 3,311

Total costs assigned by the Filling

Department $53,129

1

$8,562 + $6,387

2

$34,320 + $8,562 + $6,387

3

560 units × $1.80

Costs

2

4

5

67

CHAPTER 20 Process Cost Systems

Prob. 20-4A (Continued)

2.

Direct

Whole Materials Conversion

UNITS Units (a) (a)

Units charged to production:

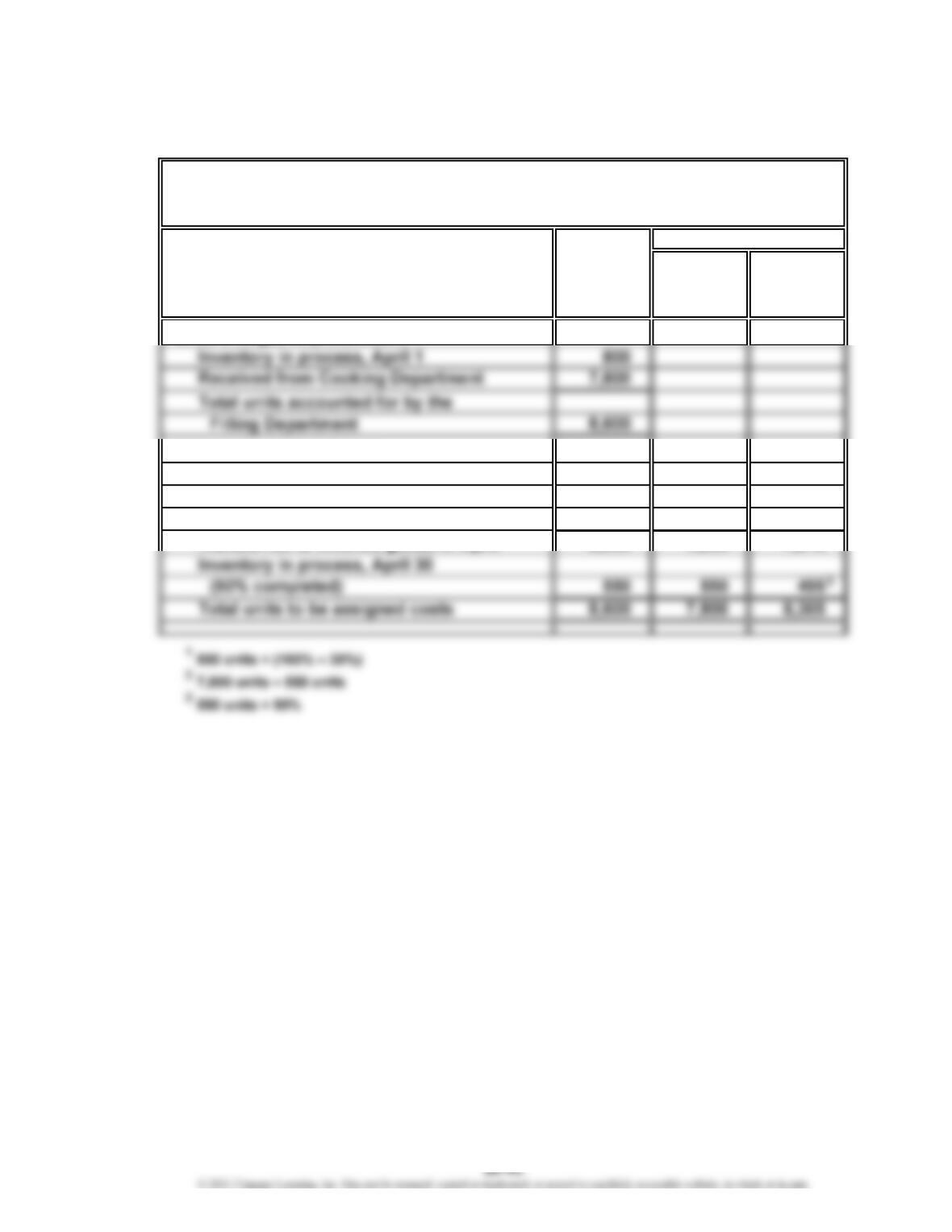

Inventory in process, May 1 550

Received from Cooking Department 9,600

Total units accounted for by the

Filling Department 10,150

Units to be assigned costs:

Hearty Soup Co.

Cost of Production Report—Filling Department

For the Month Ended May 31

Equivalent Units

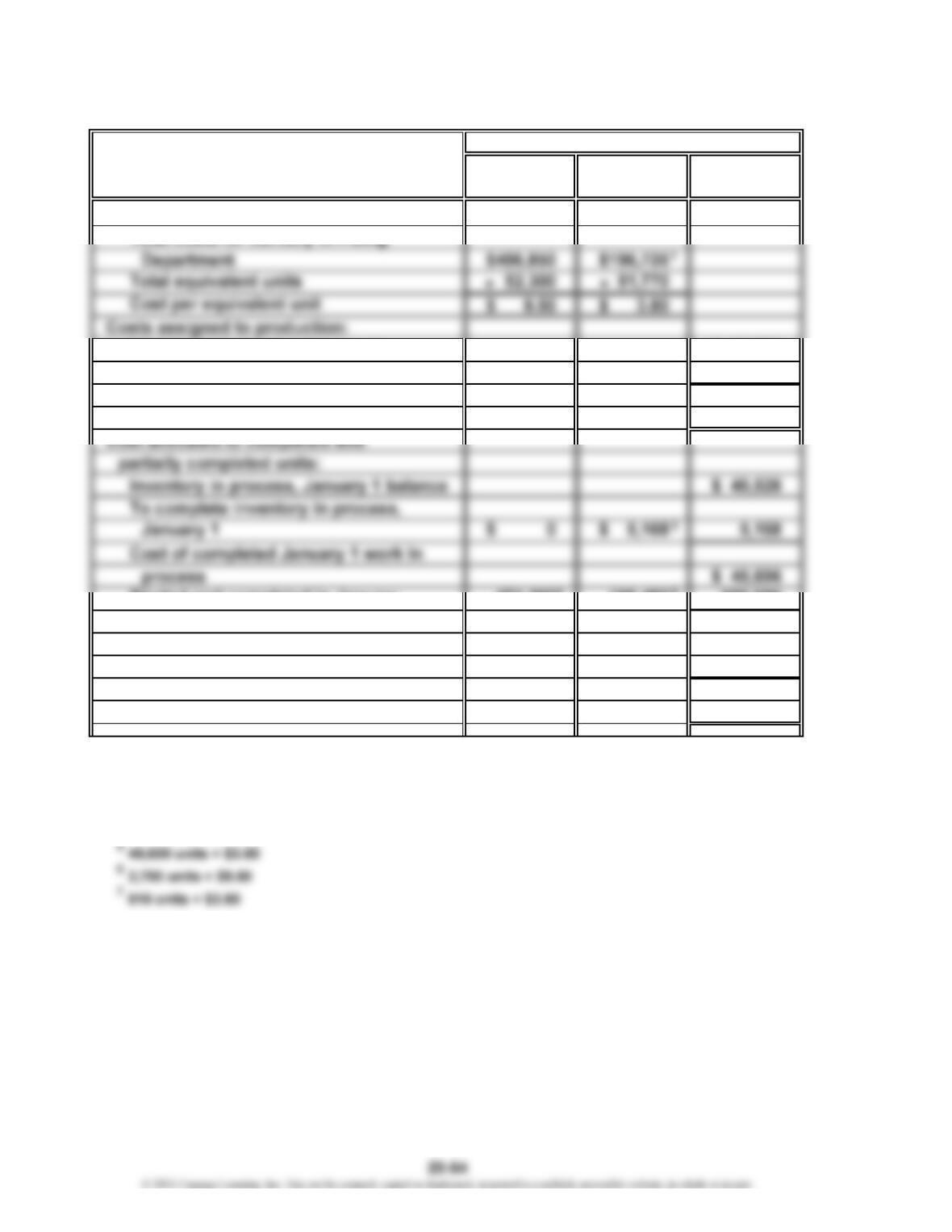

CHAPTER 20 Process Cost Systems

Prob. 20-4A (Concluded)

Direct

COSTS Materials Conversion Total

Costs assigned to production:

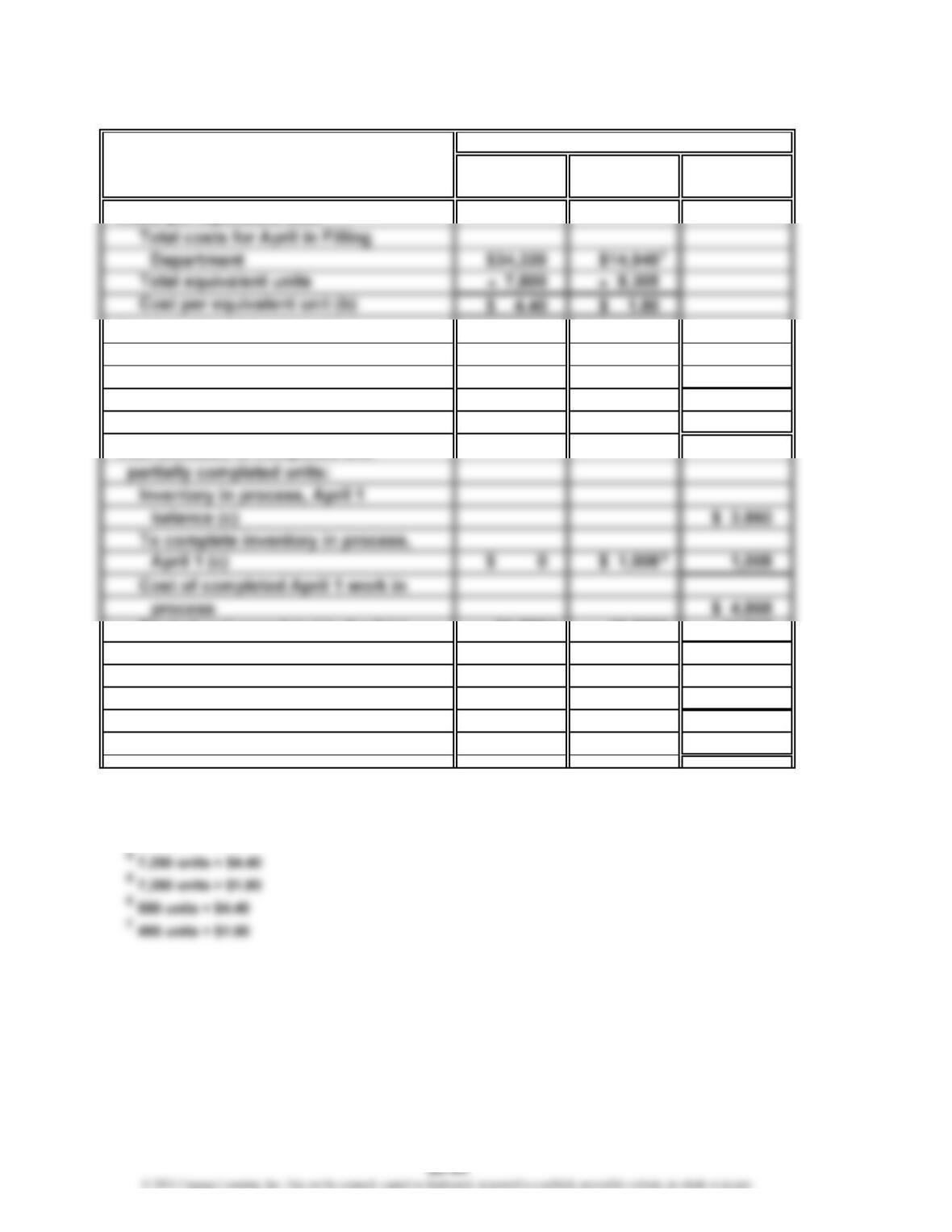

Inventory in process, May 1 $ 3,311

Costs incurred in May 63,080

Total costs accounted for by the

Filling Department $66,391

Cost of completed May 1 work in

process $ 3,421

Started and completed in May (c) 42,780 18,600 61,380

Transferred to finished goods in

May (c) $64,801

1

$12,042 + $6,878

2

$44,160 + $12,042 + $6,878

3

55 units × $2.00

3. The cost per equivalent unit for direct materials increased from $4.30 in March

to $4.40 in April to $4.60 in May. Similarly, the cost per equivalent unit for

Costs

2

4

5

CHAPTER 20 Process Cost Systems

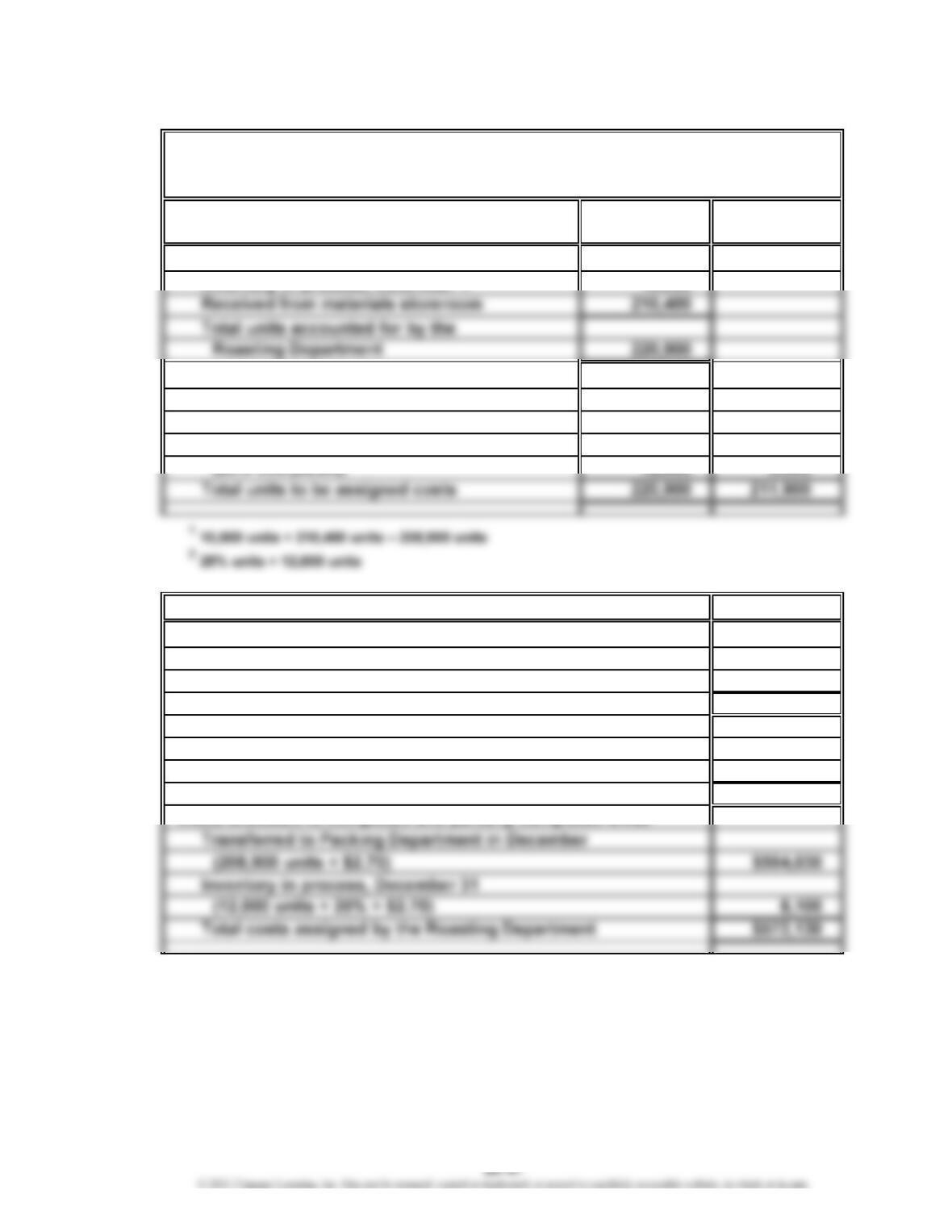

Appendix Prob. 20-5A

Whole Equivalent Units

UNITS Units of Production

Units to account for during production:

Units to be assigned costs:

Transferred to Packing Department in

December 208,900 208,900

Inventory in process, December 31

COSTS Costs

Unit costs:

Total costs for December in Roasting Department $572,130

Total equivalent units 211,900

Cost per equivalent unit $ 2.70

Costs assigned to production:

Inventory in process, December 1 $ 21,000

Costs incurred in Decembe

r

551,130

Total costs accounted for by the Roasting Department $572,130

*

$246,800 + $135,700 + $168,630

Sunrise Coffee Company

Cost of Production Report—Roasting Department

For the Month Ended December 31

*

12

÷

CHAPTER 20 Process Cost Systems

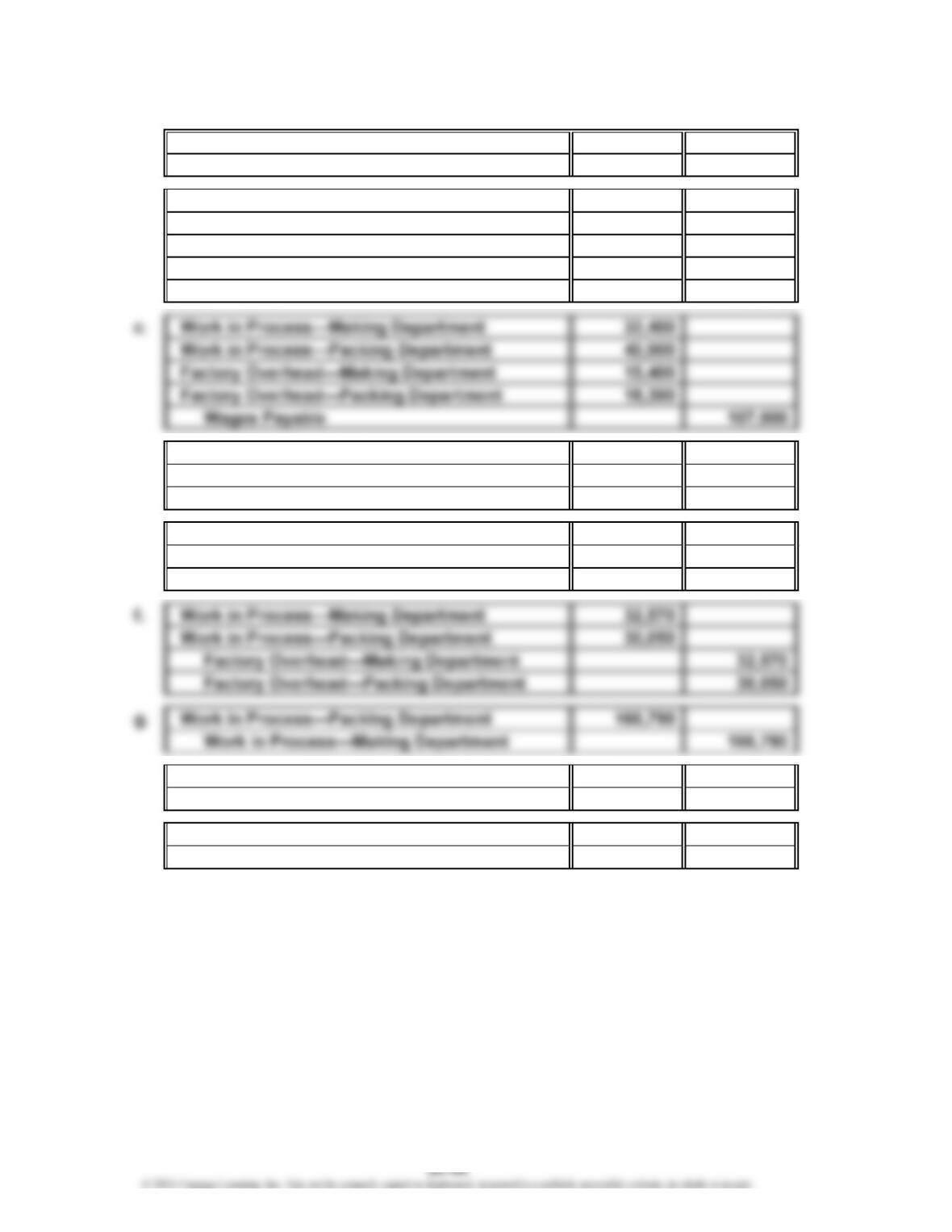

Prob. 20-1B

1. a. Materials 149,800

Accounts Payable 149,800

b. Work in Process—Making Department 105,700

Work in Process—Packing Department 31,300

Factory Overhead—Making Department 4,980

Factory Overhead—Packing Department 1,530

Materials 143,510

d. Factory Overhead—Making Department 10,700

Factory Overhead—Packing Department 7,900

Accumulated Depreciation 18,600

e. Factory Overhead—Making Department 2,000

Factory Overhead—Packing Department 1,500

Prepaid Insurance 3,500

h. Finished Goods 263,400

Work in Process—Packing Department 263,400

i. Cost of Goods Sold 265,200

Finished Goods 265,200

CHAPTER 20 Process Cost Systems

Prob. 20-1B (Concluded)

2.

Work in Work in

Process— Process— Finished

Materials Making Dept. Packing Dept. Goods

Balance, July 1……

…

$ 5,100 $ 6,790 $ 7,350 $ 13,500

3.

Balance, July 1……

…

Debits………………

…

Credits………………

Balance, July 31…

…

Factory Overhead— Factory Overhead—

Making Dept. Packing Dept.

$ 510 $ (820)

$0 $0

33,080 29,230

(32,570) (30,050)

Dr. Cr.

12

21

…

…

CHAPTER 20 Process Cost Systems

Prob. 20-2B

1.

Whole Direct

UNITS Units Materials Conversion

Units charged to production:

Inventory in process, October 1 2,300

Units to be assigned costs:

Inventory in process, October 1

(3/5 completed) 2,300 0920

Started and completed in Octobe

r

23,400 23,400 23,400

Transferred to Molding Department in

October 25,700 23,400 24,320

Bavarian Chocolate Company

Cost of Production Report—Blending Department

For the Month Ended October 31

Equivalent Units

1

2

CHAPTER 20 Process Cost Systems

Prob. 20-2B (Continued)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

Total costs for October in Blending

Costs assigned to production:

Inventory in process, October 1 $ 46,368

Costs incurred in Octobe

r

578,040

Total costs accounted for by the

Blending Department $624,408

Cost allocated to completed and

partially completed units:

Started and completed in Octobe

r

$386,100 140,400 526,500

Transferred to Molding Department

in October $578,388

Inventory in process, October 31 42,900 3,120 46,020

Total costs assigned by the Blending

Department $624,408

Costs transferred to Molding Department: $578,388

Work in process, October 31: 2,600 units at a cost of $46,020

1

$100,560 + $48,480

2

$429,000 + $100,560 + $48,480

Costs

2

4

5

67

CHAPTER 20 Process Cost Systems

Prob. 20-2B (Concluded)

2. Direct materials cost decreased $0.15, from $16.65 in September to $16.50 in October.

Conversion cost increased $0.15, from $5.85 in September to $6.00 in October.

Computations:

Direct materials: $16.65 ($38,295 ÷ 2,300 units)

Conversion: $5.85, determined as follows:

CHAPTER 20 Process Cost Systems

Prob. 20-3B

1.

Whole Direct

UNITS Units Materials Conversion

Units to be assigned costs:

Inventory in process, January 1

(60% completed) 3,400 01,360

Started and completed in January 49,600 49,600 49,600

Transferred to finished goods

Dover Chemical Company

Cost of Production Report—Filling Department

For the Month Ended January 31

Equivalent Units

1

2

CHAPTER 20 Process Cost Systems

Prob. 20-3B (Continued)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

Inventory in process, January 1 $ 40,528

Costs incurred in January 693,576

Total costs accounted for by the

Filling Department $734,104

Started and completed in January 471,200 188,480 659,680

Transferred to finished goods in

January $705,376

Inventory in process, January 31 25,650 3,078 28,728

Total costs assigned by the Filling

Department $734,104

1

$101,560 + $95,166

2

$496,850 + $101,560 + $95,166

3

1,360 units × $3.80

4

49,600 units × $9.50

Costs

2

4

5

67