1081

Exercise 20–11 (continued)

2.

Cost assignment and reconciliation – FIFO

Cost of 60,000 units from beginning inventory

Beginning inventory

$ 167,066

Materials to complete (24,000 EUP x $2.58 per EUP)

61,920

Conversion to complete (36,000 EUP x $2.16 per EUP)

77,760

Total cost of 60,000 units from beginning inventory

Costs of units started and completed

Direct materials (240,000 EUP x $2.58 per EUP)

Conversion costs (240,000 EUP x $2.16 per EUP)

Total cost of 240,000 units started and completed

Costs of units in ending inventory

Direct materials (65,600 EUP x $2.58 per EUP)

Conversion costs (24,600 EUP x $2.16 per EUP)

53,136

Total cost of 82,000 units in ending inventory

Total costs assigned

$1,666,730

Costs to be assigned:

Beginning inventory

$167,066

Direct materials – current period

Conversion costs – current period

Total costs to be assigned

$1,666,730

Beg. Inv

Conv

Transferred out

End. Inv.

1082

Exercise 20-12 (30 minutes)

ASHAD COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended July 31

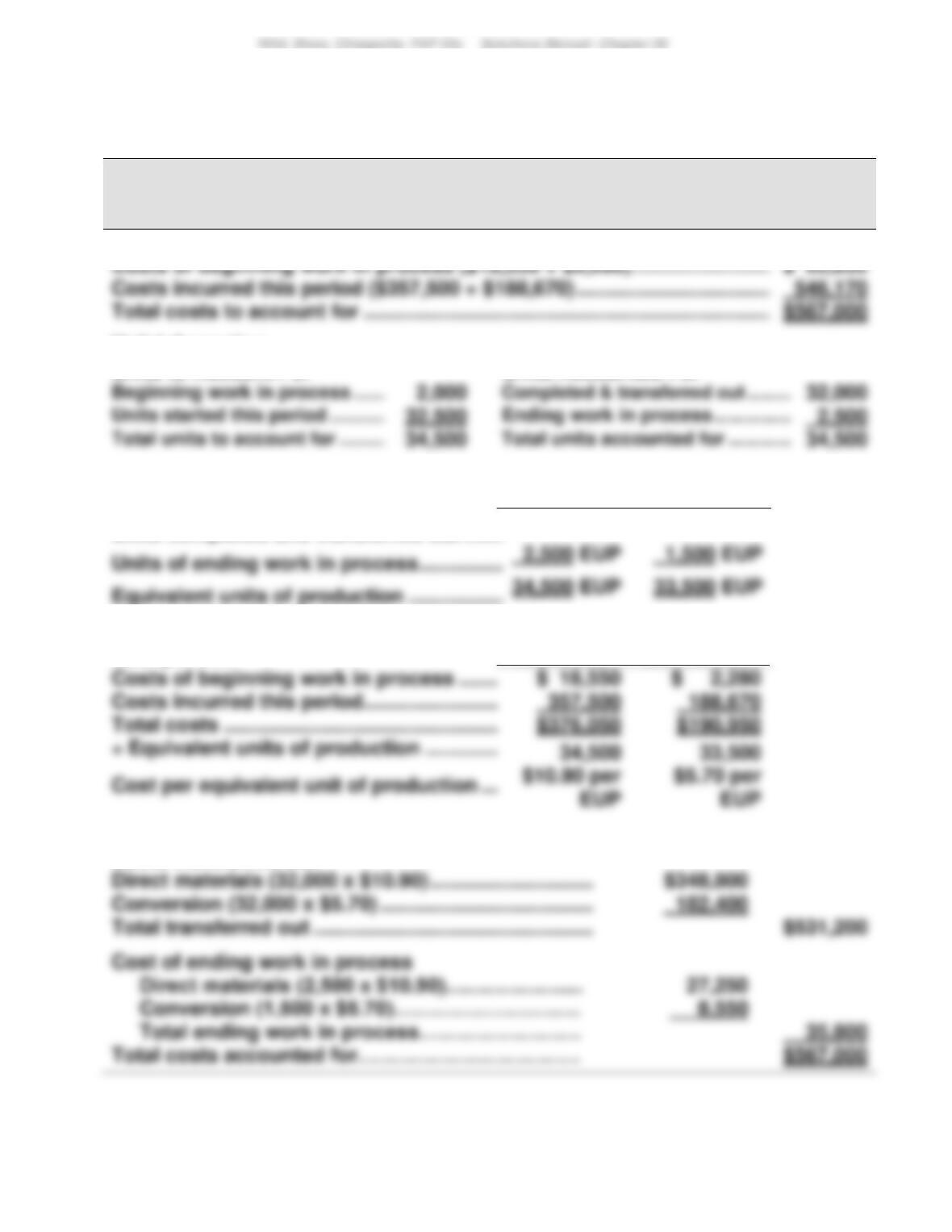

Costs Charged to Production

Costs of beginning work in process ($18,550 + $2,280) ………………………

$ 20,830

Costs incurred this period ($357,500 + $188,670) ……………………………….

Total costs to account for …………………………………………………………………

$567,000

Unit Information

Units to Account For

Units Accounted For

Equivalent Units of Production (EUP)

Direct

Materials

Conversion

Units completed and transferred out …………………………..

32,000 EUP

32,000 EUP

Units of ending work in process …………………………..

Equivalent units of production …………………………..

34,500 EUP

33,500 EUP

Cost per EUP

Direct

Materials

Conversion

Costs of beginning work in process …………………………..

$ 18,550

Costs incurred this period …………………………..

Total costs ……………………………………………………….

$376,050

Cost Assignment and Reconciliation

Costs transferred out

Direct materials (32,000 x $10.90) …………………………..

Cost of ending work in process

1083

Exercise 20-13 (40 minutes)

ASHAD COMPANY

Process Cost Summary – FIFO Method

For Month Ended July 31

Costs Charged to Production

Costs of beginning work in process

Costs incurred this period

Unit cost information

Units to account for

Units accounted for

Total units accounted for …………….

Equivalent units of production

Direct

Materials

Conversion

Units to complete beginning WIP

1084

Exercise 20-13 (Concluded)

Cost per EUP

Direct

Materials

Conversion

Costs incurred this period…………

$ 357,500

$ 188,670

Cost assignment and reconciliation

Costs transferred out

Accounts Receivable …………………………………………….

Cost of Goods Sold ………………………………………………

Exercise 20-14 (30 minutes)

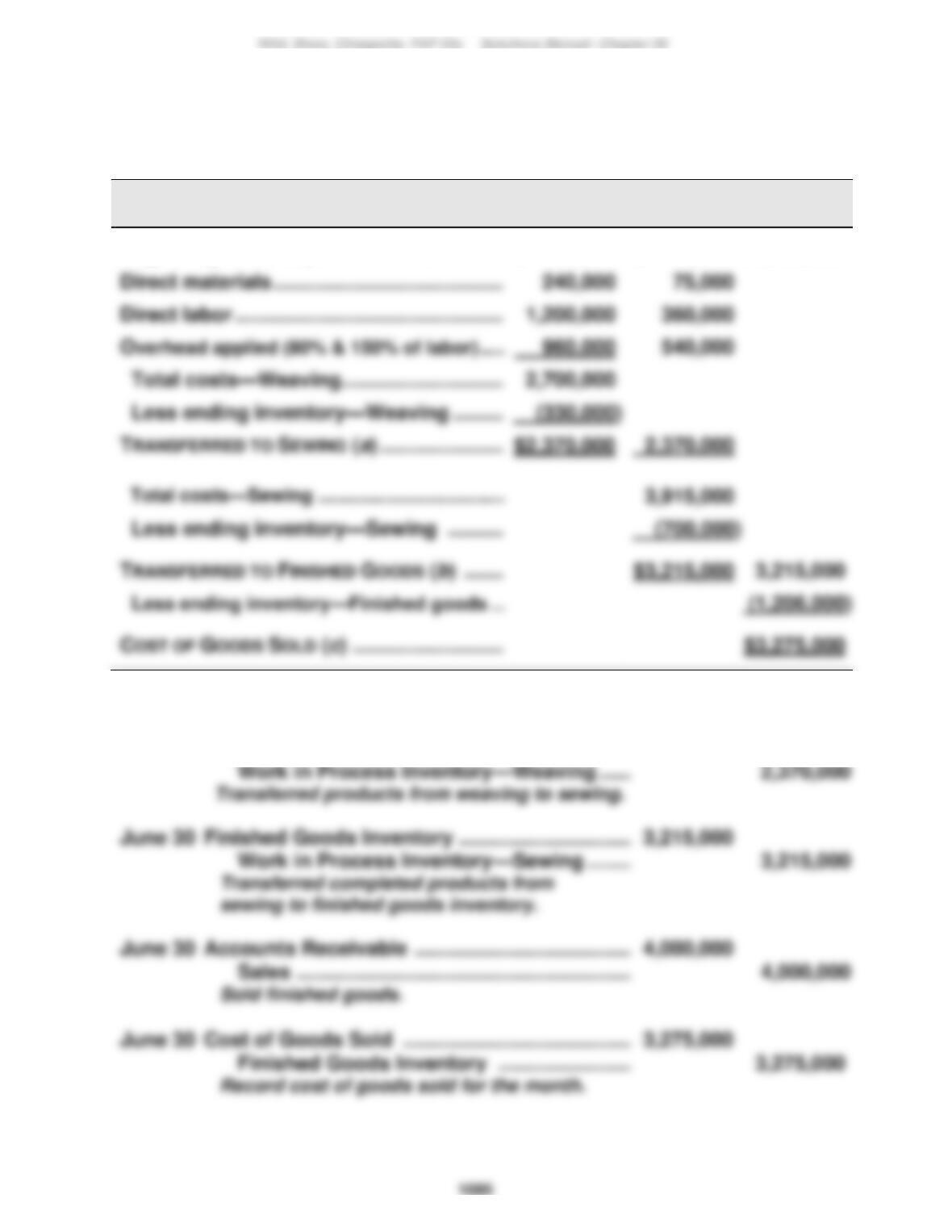

Part 1: Cost of goods transferred and cost of goods sold

Weaving

Sewing

Finished

Department

Department

Goods

Beginning inventory …………………………….

$ 300,000

$ 570,000

$1,266,000

Direct materials ……………………………………

Direct labor ………………………………………….

$3,275,000

Part 2: Summary journal entries.

June 30

Work in Process Inventory—Sewing ……………………..

2,370,000

1086

Exercise 20-15 (25 minutes)

Summary journal entries (all dated June 30)

a.

Raw Materials Inventory ………………………………………..

500,000

Accounts Payable ……………………………………………

500,000

Purchased raw materials.

240,000

Used direct materials.

c.

120,000

Raw Materials Inventory …………………………..

120,000

Used indirect materials.

360,000

Factory Wages Payable …………………………..

e.

Factory Wages Payable …………………………..

Used indirect labor.

156,000

Other Accounts ……………………………………………….

Incurred other overhead costs.

960,000

540,000

Factory Overhead …………………………..………………..

Cash ……………………………………………………….

Paid total payroll.

1087

Exercise 20-16 (25 minutes)

ELLIOTT COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended March 31

Costs Charged to Production

Costs of beginning work in process

Costs incurred this period

Total costs to account for ………………………………..

Unit information

Units to account for

Units accounted for

Beginning work in process …………………………..

Units started this period …………………………..

Total units to account for …………………………..

Total units accounted for …………….

Equivalent units of production

Direct

Materials

Conversion

Units completed & transferred out..

17,000 EUP

17,000 EUP

Units of ending work in process

22,000 EUP

18,750 EUP

Cost per EUP

Direct

Materials

Conversion

Cost of beginning work in process..

22,000 EUP

18,750 EUP

1088

Exercise 20-16 (continued)

Cost assignment and reconciliation

Costs transferred out

Costs of ending work in process

Exercise 20-17 (40 minutes)

OSLO COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended May 31

Costs Charged to Production

Costs of beginning work in process

Costs incurred this period

Beginning work in process ………….

Units started this period ………………

1089

Exercise 20-17 (Concluded)

Equivalent units of production

Direct

Materials

Conversion

Units completed & transferred out…

13,000 EUP

13,000 EUP

Units of ending work in process

3,000 EUP

16,000 EUP

13,750 EUP

Cost per EUP

Direct

Materials

Conversion

Cost of beginning work in process…

$ 2,880

$ 5,358

Costs incurred this period……………

16,000 EUP

13,750 EUP

Cost assignment and reconciliation

Costs transferred out

Costs of ending work in process

Exercise 20-18 (10 minutes)

Equivalent units of production—FIFO

Units of

Percent

Equivalent

EUP (for materials and conversion)

Product

Added

Units

Beginning work in process ………….

1090

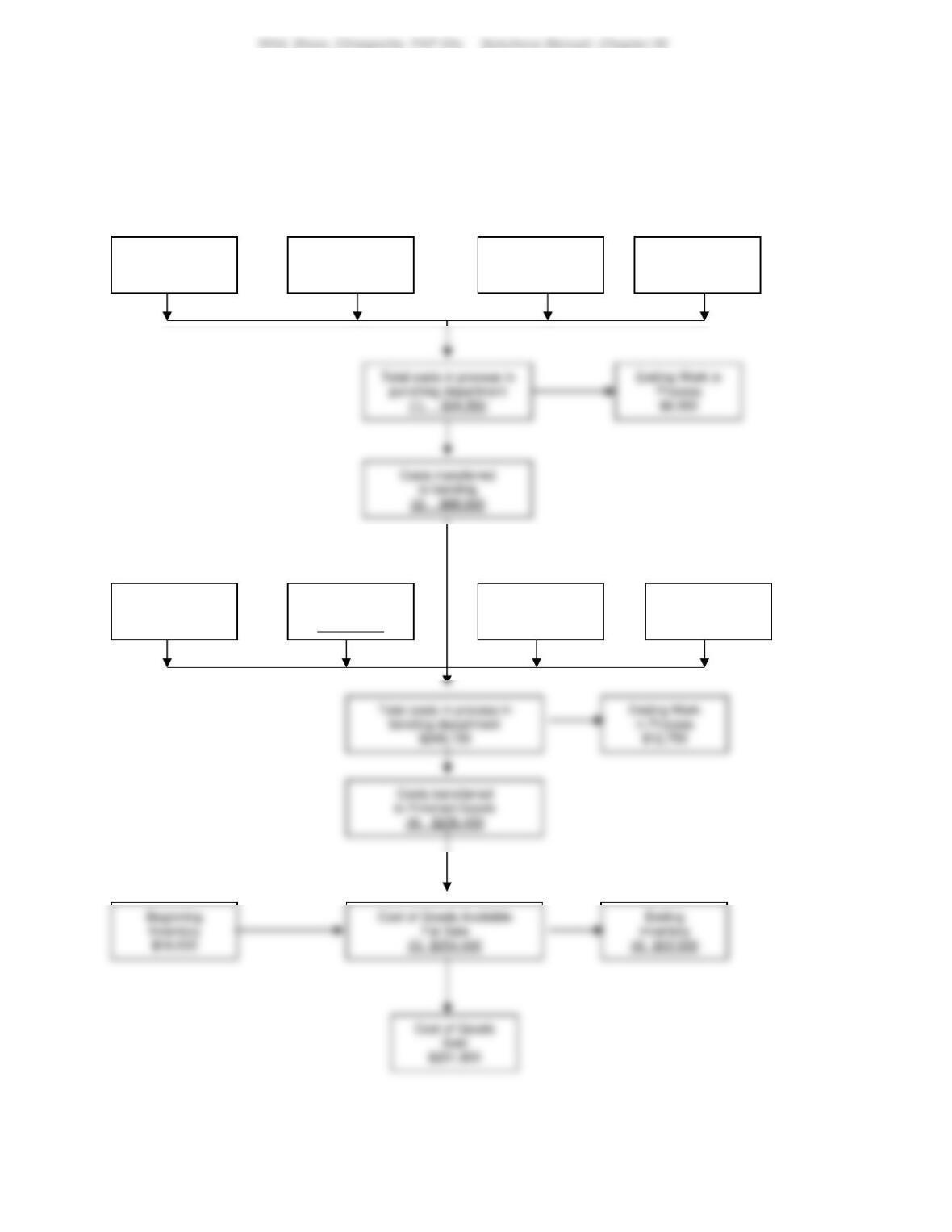

Exercise 20-19 (20 minutes)

[Note: Solution key is on the following page.]

Punching

Bending

Warehouse

$18,000

(6) $22,500

Beginning Work in

Process

$7,500

Direct

Materials

$60,000

Direct

Labor

$12,000

Factory

Overhead

$15,000

Beginning Work in

Process

$9,750

Direct

Materials

(3) $83,250

Direct

Labor

$30,750

Factory

Overhead

$36,900

1091

Exercise 20-19 (Continued)

Key to solution of flowchart:

(1)

Beginning work in process in punching

$ 7,500

Direct materials added

$ 60,000

Direct labor added

Factory overhead added

Total manufacturing costs added

(2)

Total costs in process in punching department

$ 94,500

Less ending work in process

(3)

Beginning work in process in bending

$ 9,750

Total costs added

Total costs added = $249,150 – $9,750 = $239,400

Direct materials added

Direct labor added

Factory overhead added

Costs transferred from punching

(4)

Total costs in process in bending department

$249,150

Ending work in process

(5)

Beginning Finished Goods inventory

$ 18,000

Add costs transferred to finished goods

(6)

Cost of goods available for sale

$254,400

Less ending inventory

1092

Exercise 20-20 (30 minutes)

1.

Units to account for

Units Accounted For

2. and 3.

Equivalent Units of Production (EUP)

Direct

Materials

Conversion

Units of ending work in process………

4. and 5.

Cost per EUP

Direct

Materials

Conversion

Costs of beginning work in process…..

$ 45,000

$ 56,320

1093

Exercise 20-20 (concluded)

6.

Costs transferred out

Direct materials [$14.00 per EUP x 23,000 EUP] ….

Conversion [$15.40 per EUP x 23,000 EUP] ………..

Total transferred out ………………………………………….

7.

Cost of ending work in process

Direct materials [$14.00 per EUP x 7,000 EUP] ……

Conversion [$15.40 per EUP x 2,800 EUP] ………….

Total ending work in process …………………………..

Exercise 20-21 (10 minutes)

1.

Raw Materials Inventory ………………………………………..

80,000

2.

Work in Process Inventory ……………………………………..

42,000

3.

22,500

1094

Exercise 20-22 (10 minutes)

1.

Work in Process Inventory ……………………………………..

75,000

Factory Overhead …………………………………………………..

20,000

3.

Factory Wages Payable ………………………………………….

95,000

Exercise 20-23 (5 minutes)

1.

Factory Overhead ………………………………………………….

38,750

2.

Work in Process Inventory ……………………………………..

82,500

Exercise 20-24 (5 minutes)

1.

Finished Goods Inventory ………………………………………

135,600

2.

Accounts Receivable ……………………………………………..

175,000

1095

Exercise 20-25 (25 minutes)

1.

Oct. 31

Work in Process Inventory ……………………………………..

522,000

Raw Materials Inventory …………………………..

Oct. 31

Work in Process Inventory ……………………………………..

130,000

Factory Wages Payable …………………………..

Oct. 31

Work in Process Inventory ……………………………………..

227,500

Factory Overhead …………………………………………….

Oct. 31

595,000

Work in Process Inventory …………………………..

Oct. 31

Accounts Receivable ……………………………………………..

950,000

Sales ……………………………………………………….

Oct. 31

540,000

Finished Goods Inventory …………………………..

1096

Exercise 20-26 (25 minutes)

a. Purchased raw materials on credit at a cost of $52,000.

b. Used direct materials costing $42,000 in production.

Exercise 20-27 (10 minutes)

A hybrid costing system contains features of both process costing and job

order costing. A hybrid system of processes requires a hybrid costing

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 20

1097

PROBLEM SET A

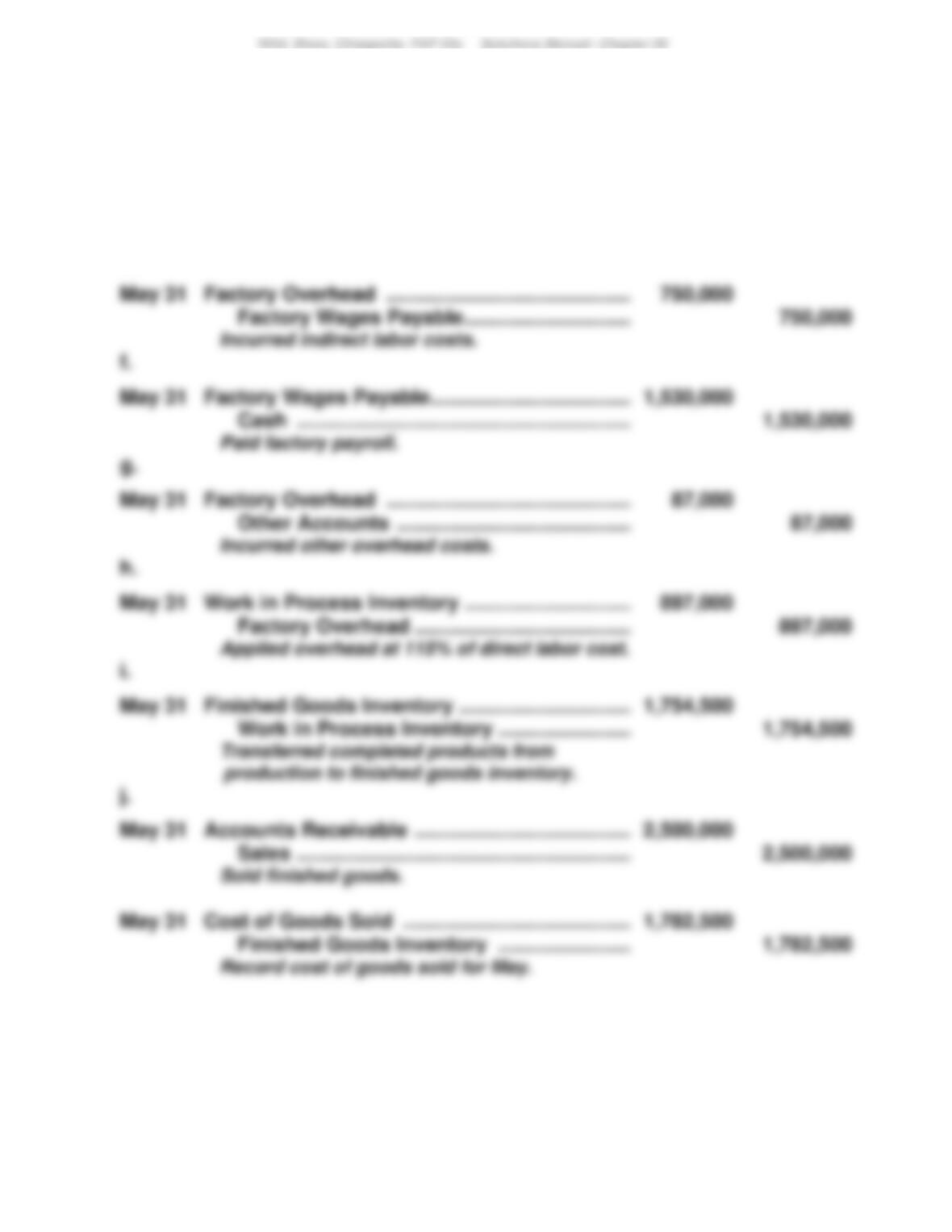

Problem 20-1A (45 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Beginning work in process inventory …………………………..

$ 435,000

Direct materials used in production …………………………..

157,500

Part 2: Summary journal entries

a.

May 31

Raw Materials Inventory ………………………………………..

250,000

May 31

Work in Process Inventory …………………………..

May 31

Direct labor used in production ………………………………………

780,000

Beginning finished goods inventory …………………………..

Less ending finished goods inventory …………………………..

1098

Problem 20-1A (Continued)

d.

May 31

Work in Process Inventory …………………………..

780,000

Factory Wages Payable …………………………..

780,000

Incurred direct labor costs.

e.

May 31

750,000

Factory Wages Payable …………………………..

750,000

Incurred indirect labor costs.

May 31

Cash ……………………………………………………….

Paid factory payroll.

May 31

Other Accounts ……………………………………………….

Incurred other overhead costs.

May 31

Work in Process Inventory …………………………..

Factory Overhead …………………………..………………..

Applied overhead at 115% of direct labor cost.

May 31

Work in Process Inventory …………………………..

May 31

Accounts Receivable …………………………………………….

Sales ……………………………………………………….

Sold finished goods.

May 31

Finished Goods Inventory …………………………..

Record cost of goods sold for May.

1099

Problem 20-2A (50 minutes)

Part 1

(a) and (b) Equivalent units with respect to direct materials and conversion

Direct

Equivalent units of production (EUP)

Materials

Conversion

Units completed and transferred out ……………….

700,000

700,000

Units of ending Work in Process …………………….

180,000

Part 2

Cost per equivalent unit of production

Direct

Materials

Conversion

Costs of beginning Work in Process ………………………

$ 420,000

$ 139,000

Costs incurred this period ……………………………………..

Cost per equivalent unit of production ……………………

Part 3 Assigning product costs to units

Costs transferred out

Direct materials (700,000 EUP x $3.00 per EUP) …….

$2,100,000

Conversion (700,000 EUP x $4.50 per EUP) …………..

Costs of ending work in process

Direct materials (180,000 EUP x $3.00 per EUP) …….

Conversion (54,000 EUP x $4.50 per EUP) …………….

1100

Problem 20-2A (Concluded)

Part 4

MEMORANDUM

TO:

FROM:

DATE:

RE: Percentage of Completion Error Analysis