Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 20

Chapter 20

Process Costing

QUESTIONS

1. The main deciding factor in choosing between a job order costing system or a

process costing system is the type of product or service. Examples where a

3. Yes, services can be delivered by processes. For example, Federal Express delivers

4. The journal entries to match cost flows with product flows are primarily the same

for both process costing and job order costing. In process costing, the materials

6. The computation of equivalent units of production focuses on converting partially

completed units to a measure in terms of completed units. We need to use EUP

7. The two main methods of process costing are the weighted-average and the first-in,

first-out (FIFO) methods. The weighted-average method considers “average flow”

8. A process cost accounting system treats labor that is used entirely within one

9. Direct labor costs flow to the Work in Process Inventory account. Then the direct

10. At the end of the accounting period the Factory Overhead account should have a

11. Yes, it is possible to have either underapplied or overapplied overhead in a process

12. Equivalent units for direct materials differ from that for direct labor (and overhead) if

direct materials and direct labor (and overhead) are added at different stages in the

13. The four steps in accounting for production activity (for process operations) are: 1)

14. The process cost summary serves at least three purposes: (a) to help department

managers control their departments; (b) to help factory managers evaluate

15. Yes. Google might use process costing to determine the cost of manufacturing its

16. Likely processing steps for digital televisions include making the frame and

17. General Mills, like most food processors, faces risks due to water scarcity and

climate change that could disrupt its supply and lower profits. The company also

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 20

QUICK STUDIES

Quick Study 20-1 (5 minutes)

Quick Study 20-2 (5 minutes)

Quick Study 20-3 (10 minutes)

Quick Study 20-4 (10 minutes)

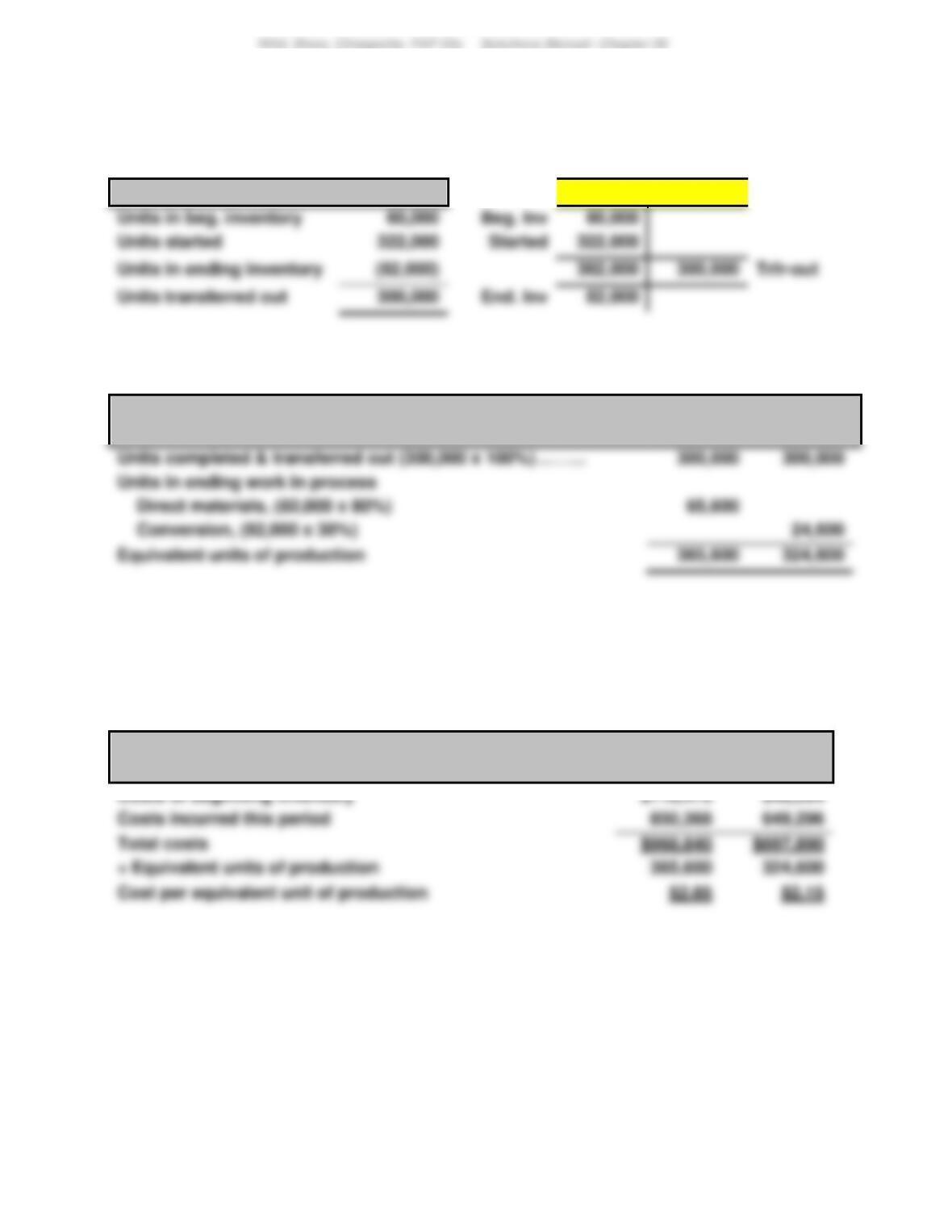

Units

Units in beginning inventory

150,000

Units started

310,000

Total units to account for

460,000

Units completed and transferred out

340,000

Units in ending inventory

120,000

Total units accounted for

460,000

1064

Quick Study 20-5 (10 minutes)

Equivalent units under the weighted-average method

Equivalent

EUP for conversion—Weighted average

Units

Equivalent units of production …………………………………………………….

Quick Study 20-6 (10 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for conversion—FIFO

Units

Equivalent units to complete beginning WIP (150,000 x 20%) ……….

Equivalent units started and completed* ……………………………………..

Equivalent units of production …………………………………………………….

Quick Study 20-7 (5 minutes)

Cost per equivalent unit of production—weighted-average method

Quick Study 20-8 (10 minutes)

Equivalent units under the weighted-average method

Equivalent

EUP for conversion—Weighted average

Units

Equivalent units of production …………………………………………………….

1065

Quick Study 20-9 (15 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for conversion—FIFO

Units

Equivalent units to complete beginning WIP (320,000 x 75%) ……….

Equivalent units started and completed* ……………………………………..

Quick Study 20-10 (15 minutes)

Equivalent units of production—Weighted

average

Direct

Materials

Conversion

Units of ending work in process

Quick Study 20-11 (25 minutes)

Cost per equivalent unit—Weighted average

Direct

Materials

Conversion

Costs of beginning work in process………………

$ 996

$ 585

Costs incurred this period…………………………..

Total costs……………………………………………..

÷ Equivalent units of production (from QS 20–10)…

Units of ending work in process

Quick Study 20-12 (10 minutes)

Cost assignment—Weighted average

Direct

Materials

Conversion

Costs of units transferred out

Quick Study 20-13 (5 minutes)

Work in Process Inventory—Painting …………………….

Quick Study 20-14 (15 minutes)

Equivalent units of production—FIFO

Direct

Materials

Conversion

1067

Quick Study 20-15 (5 minutes)

Cost per equivalent unit – FIFO

Direct

Materials

Conversion

Costs incurred this period …………………………………

÷ Equivalent units of production (from QS 20–14)

Quick Study 20-16 (20 minutes)

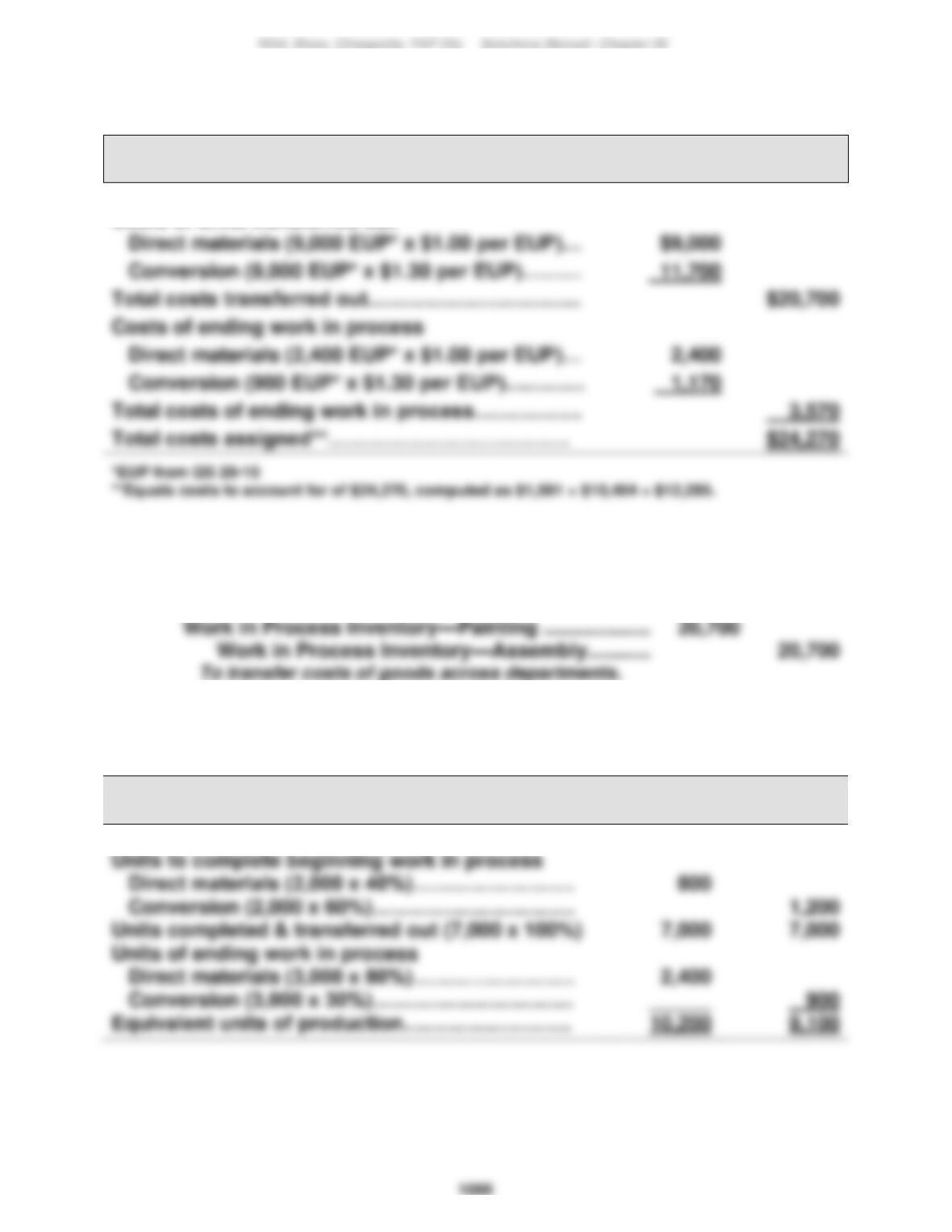

Assignment of costs to output of department—FIFO

Costs of ending work in process

Quick Study 20-17 (5 minutes)

Quick Study 20-18 (10 minutes)

a)

Equivalent units of production—Weighted average

Direct

Materials

Units completed & transferred out (17,000 x 100%)

Units of ending work in process

b)

Cost per equivalent unit—Weighted average

Direct

Materials

Costs of beginning work in process ………………….

Costs incurred this period …………………………………

Quick Study 20-19 (10 minutes)

Cost assignment—Weighted average

Direct

Materials

1069

Quick Study 20-20 (10 minutes)

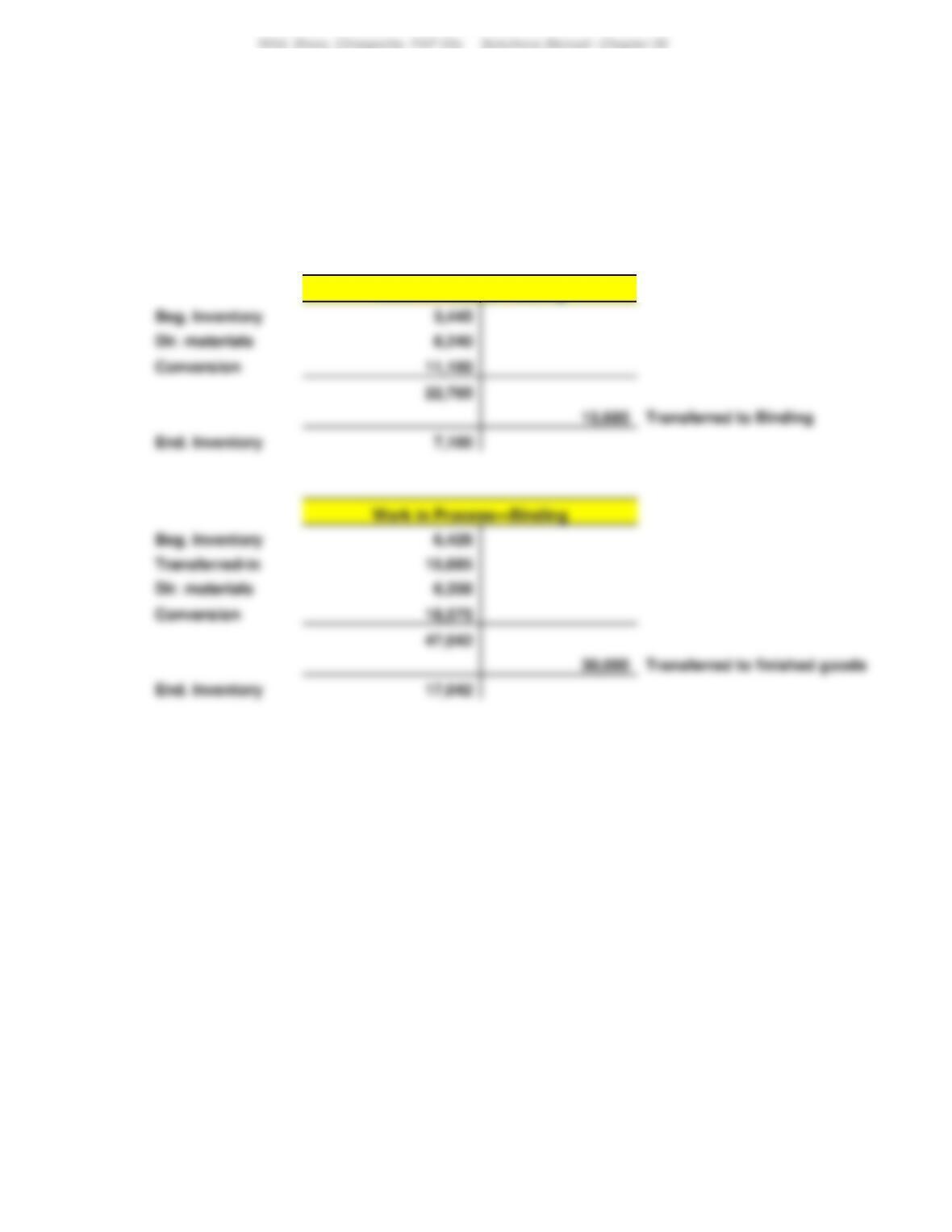

The ending balance in Work in Process Inventory—Cutting is $7,100 and

the ending balance in Work in Process Inventory—Binding is $17,042, as

computed below.

Work in Process—Cutting

Cost of ending work in process inventory

Quick Study 20-21 (15 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for materials—FIFO

Units

Equivalent units to complete beginning WIP (2,000 x 30%)….

600

Equivalent units started and completed* ……………………………..

Cost per equivalent unit—FIFO

Direct

Materials

Costs incurred this period …………………………………

Quick Study 20-22 (15 minutes)

Assignment of direct materials costs to output of department—FIFO

Costs transferred out

Quick Study 20-23 (10 minutes)

1.

Raw Materials Inventory ………………………………………..

62,000

2.

Work in Process Inventory …………………………………….

50,000

Quick Study 20-24 (10 minutes)

1.

Work in Process Inventory …………………………………….

125,000

2.

Factory Overhead ………………………………………………….

10,000

3.

Factory Wages Payable …………………………………………

135,000

Quick Study 20-25 (15 minutes)

1.

Factory Overhead ………………………………………………….

9,000

2.

Factory Overhead ………………………………………………….

156,000

3.

Work in Process Inventory …………………………………….

175,000

Quick Study 20-26 (10 minutes)

Quick Study 20-27 (5 minutes)

If the company is successful in reducing water usage, its raw materials

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 20

1073

EXERCISES

Exercise 20-1 (10 minutes)

1. Process operation 7. Job order operation

Exercise 20-2 (10 minutes)

a. Job order operation e. Job order operation

Exercise 20-3 (10 minutes)

1074

Exercise 20-4 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Units of

Product

Ending work in process (16,000 EUP x 100%) ……………………..

2. Beginning inventory is 40% complete with respect to materials.

EUP for Materials

Product

Ending work in process (16,000 EUP x 75%) ……………………….

3. Beginning inventory is 60% complete with respect to materials.

EUP for Materials

Product

Ending work in process (16,000 EUP x 30%) ……………………….

To complete beginning work in process (24,000 EUP x 40%) …….

Exercise 20-5 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

To complete beginning work in process (24,000 EUP x 0%) ………

2. Beginning inventory is 40% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

To complete beginning work in process (24,000 EUP x 60%) …….

3. Beginning inventory is 60% complete with respect to materials.

Ending inventory is 30% complete with respect to materials.

Units of

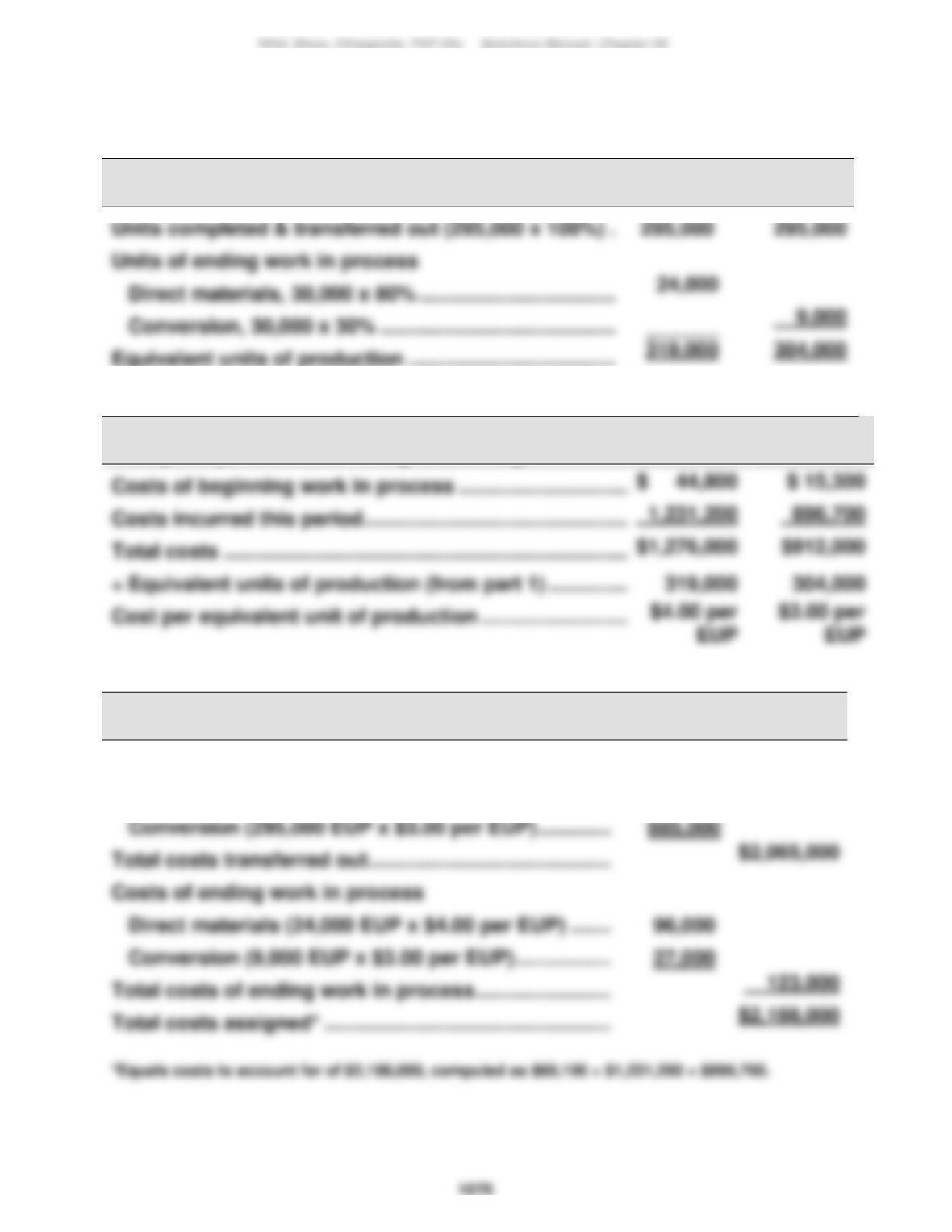

Conversion (295,000 EUP x $3.00 per EUP) …………………………..

885,000

Total costs transferred out ………………………………………………………

Costs of ending work in process

Direct materials (24,000 EUP x $4.00 per EUP) ………………………

96,000

Conversion (9,000 EUP x $3.00 per EUP) …………………………..

27,000

Total costs of ending work in process …………………………..

Total costs assigned* ……………………………………………………….

Exercise 20-6 (30 minutes)

1.

Equivalent units of production—Weighted average

Direct

Materials

Conversion

Units completed & transferred out (295,000 x 100%) ………………..

295,000

Units of ending work in process

Direct materials, 30,000 x 80% ………………………………………………

Conversion, 30,000 x 30% …………………………………………………….

Equivalent units of production ………………………………………………..

2.

Cost per equivalent unit—Weighted average

Direct

Materials

Conversion

Costs of beginning work in process …………………………..

Costs incurred this period ……………………………………………………….

Total costs ……………………………………………………………………………..

÷ Equivalent units of production (from part 1) ………………………….

3.

Cost assignment—Weighted average

Costs of units transferred out

Direct materials (295,000 EUP x $4.00 per EUP) …………………….

$1,180,000

1077

Exercise 20-7 (30 minutes)

1.

Equivalent units of production—FIFO

Direct

Materials

Conversion

Units of ending work in process

Equivalent units of production ………………………………………………..

Units to complete beginning work in process

2.

Cost per equivalent unit—FIFO

Direct

Materials

Conversion

Costs incurred this period ……………………………………….

÷ Equivalent units of production (from part 1) ………….

1078

Exercise 20-8 (20 minutes)

1. Units transferred out

Units

Dept. 1 – units

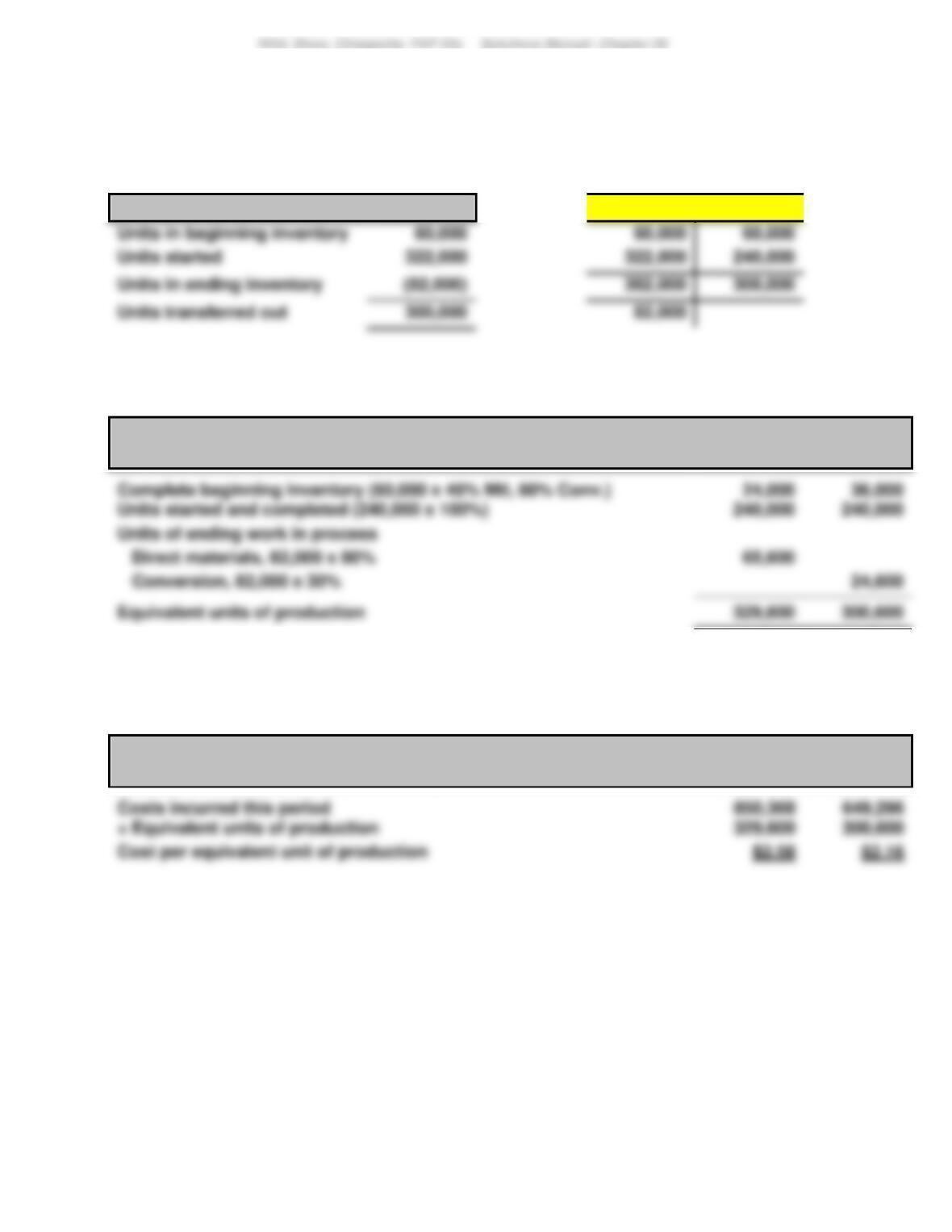

Units started

322,000

Units in ending inventory

Units transferred out

300,000

End. Inv

2. EUP

Equivalent units of production – weighted-average

Direct

Materials

Conversion

Equivalent units of production

Exercise 20-9 (20 minutes)

1. Cost per EUP

Cost per equivalent unit – weighted-average

Direct

Materials

Conversion

Cost per equivalent unit of production

1079

Exercise 20-9 (continued)

2.

Cost assignment and reconciliation – weighted-average

Costs of units transferred out

Direct materials (300,000 EUP x $2.65 per EUP)

$795,000

Conversion costs (300,000 EUP x $2.15 per EUP)

Total cost of 300,000 units transferred out

Costs of units in ending inventory

Total cost of 82,000 units in ending inventory

Costs to be assigned:

Beginning inventory

$167,066

Beg. Inv

End. Inv.

1080

Exercise 20-10 (20 minutes)

1.

Units

Units

2.

Equivalent units of production – FIFO

Direct

Materials

Conversion

Exercise 20-11 (20 minutes)

1.

Cost per equivalent unit – FIFO

Direct

Materials

Conversion