Ex. 20.14 a. Vests Skis Ropes

Unit selling prices $120 $300 $50

Unit variable costs (60) (210) (10)

Unit contribution margins $60 $90 $40

c.

To maximize operating income, the marketing manager should pursue a strategy

SOLUTIONS TO PROBLEMS SET A

25 Minutes, Easy

PROBLEM 20.1A

IONIC CHARGE

a. Required contribution margin per unit

Budgeted operating Income

700,000$

Fixed costs 800,000

Total required contribution margin 1,500,000$

Number of units to be produced and sold 60,000

c. Margin of safety at 60,000 units:

Sales volume at 60,000 units ($75 × 60,000 units)

4,500,000$

Variable costs and expenses per unit 50

PROBLEM 20.1A

IONIC CHARGE (concluded)

d.

No. With a unit sales price of $60, the break-even sales volume is 80,000 units:

25 Minutes, Medium PROBLEM 20.2A

BLASTER CORPORATION

a. Sales price per unit:

Budgeted costs

2,250,000$

Add: Budgeted operating income 900,000

Budgeted sales revenue 3,150,000$

Sales price per pair ($3,150,000 ÷ 30,000 pairs) 105$

Manufacturing overhead ($24 × 25%) 6

Selling and administrative expense ($20 × 20%) 4

Total variable costs per pair 41$

(3) Contribution margin per pair of boots:

Sales price per pair

121$

Less: Variable costs per pair [from (2) ]41

Contribution margin per pair 80$

(4) Number of pairs required to break even:

Contribution margin per pair [from (3) ]80$

Number of pairs required to break even ($1,020,000 ÷ $80) 12,750

Selling and administrative expenses ($600,000 × 80%) 480,000

Total fixed costs 1,020,000$

(2) Variable costs and expenses per pair of boots:

Direct labor 10

PROBLEM 20.3A

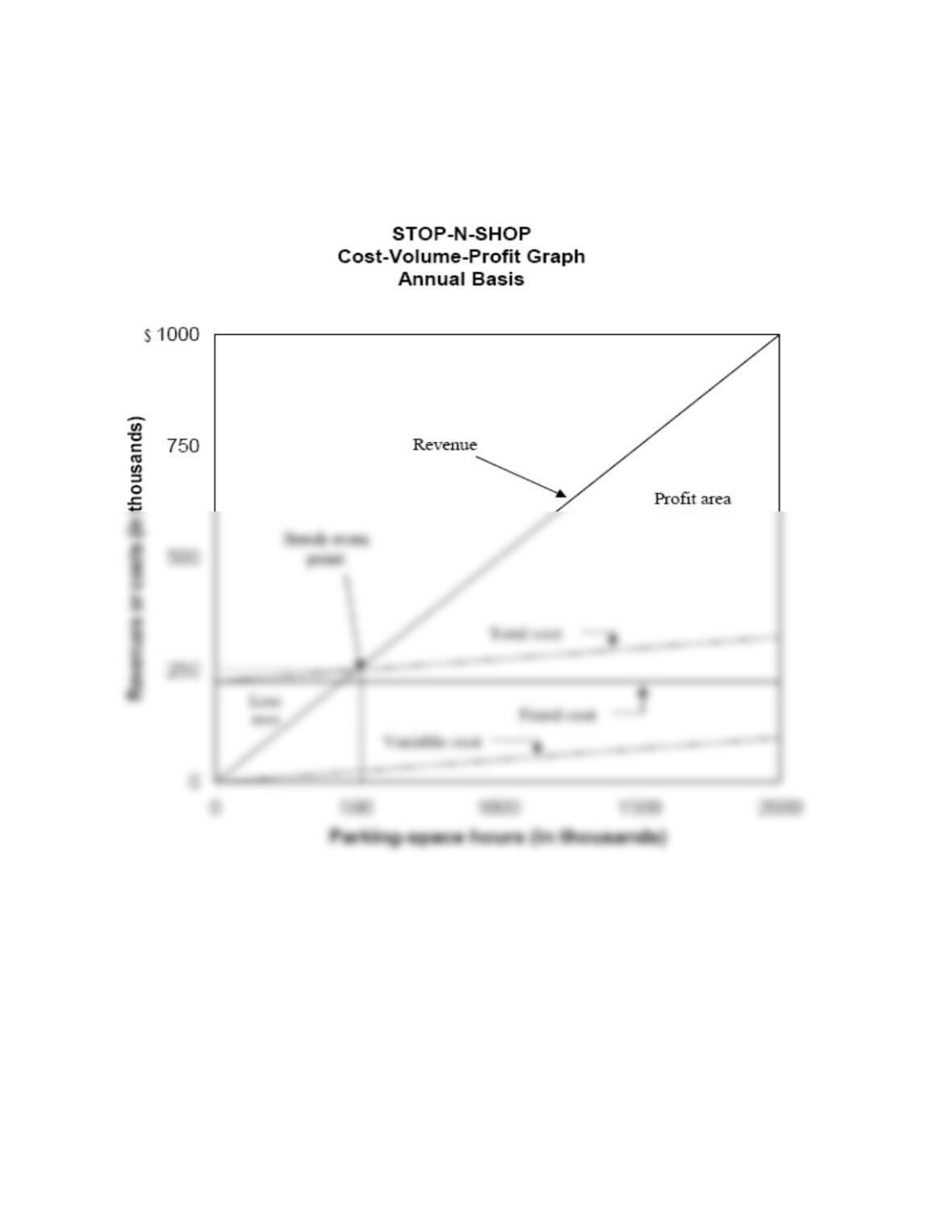

STOP-N-SHOP

a.

30 Minutes, Medium

PROBLEM 20.3A

STOP-N-SHOP (continued)

The following information is used for parts b. and c. of this problem.

Operating data:

Revenue per parking-space hour 50 cents

Variable costs per parking-space hour 5 cents

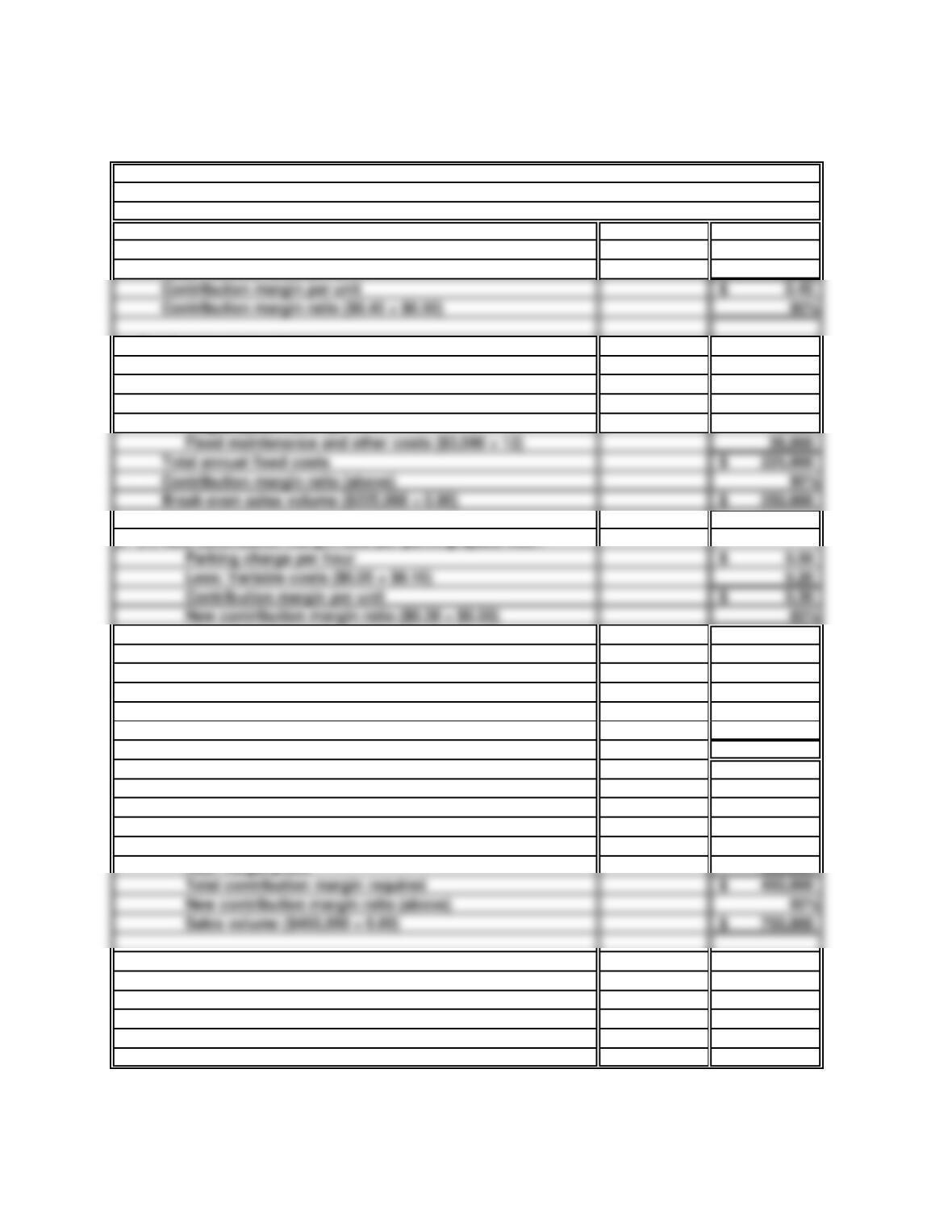

PROBLEM 20.3A

STOP-N-SHOP (concluded)

b. Contribution margin ratio:

Parking charge per hour 0.50$

Less: Variable costs per unit 0.05

Break-even sales volume:

Fixed costs:

Rent on lot ($7,250 × 12) 87,000$

Supervisor’s salary 24,000

Wages ($300 × 52 × 5) 78,000

Fixed maintenance and other costs ($3,000 × 12) 36,000

Break-even sales volume ($225,000 ÷ 0.90) 250,000$

Less: Variable costs ($0.05 + $0.15) 0.20

New contribution margin ratio ($0.30 ÷ $0.50) 60%

c. (1) New contribution margin ratio per parking-space hour:

New level of fixed costs:

Rent on lot ($7,250 × 12) 87,000$

Supervisor’s salary 24,000

Vacation pay ($300 × 2 × 5) 3,000

Fixed maintenance and other costs ($3,000 × 12) 36,000

Total fixed costs under new arrangement 150,000$

(2) Required sales revenue to produce desired operating

income:

Total fixed costs under new arrangement (above) 150,000$

Add: Target profit 300,000

Sales volume ($450,000 ÷ 0.60) 750,000$

Contribution margin ratio ($0.45 ÷ $0.50) 90%

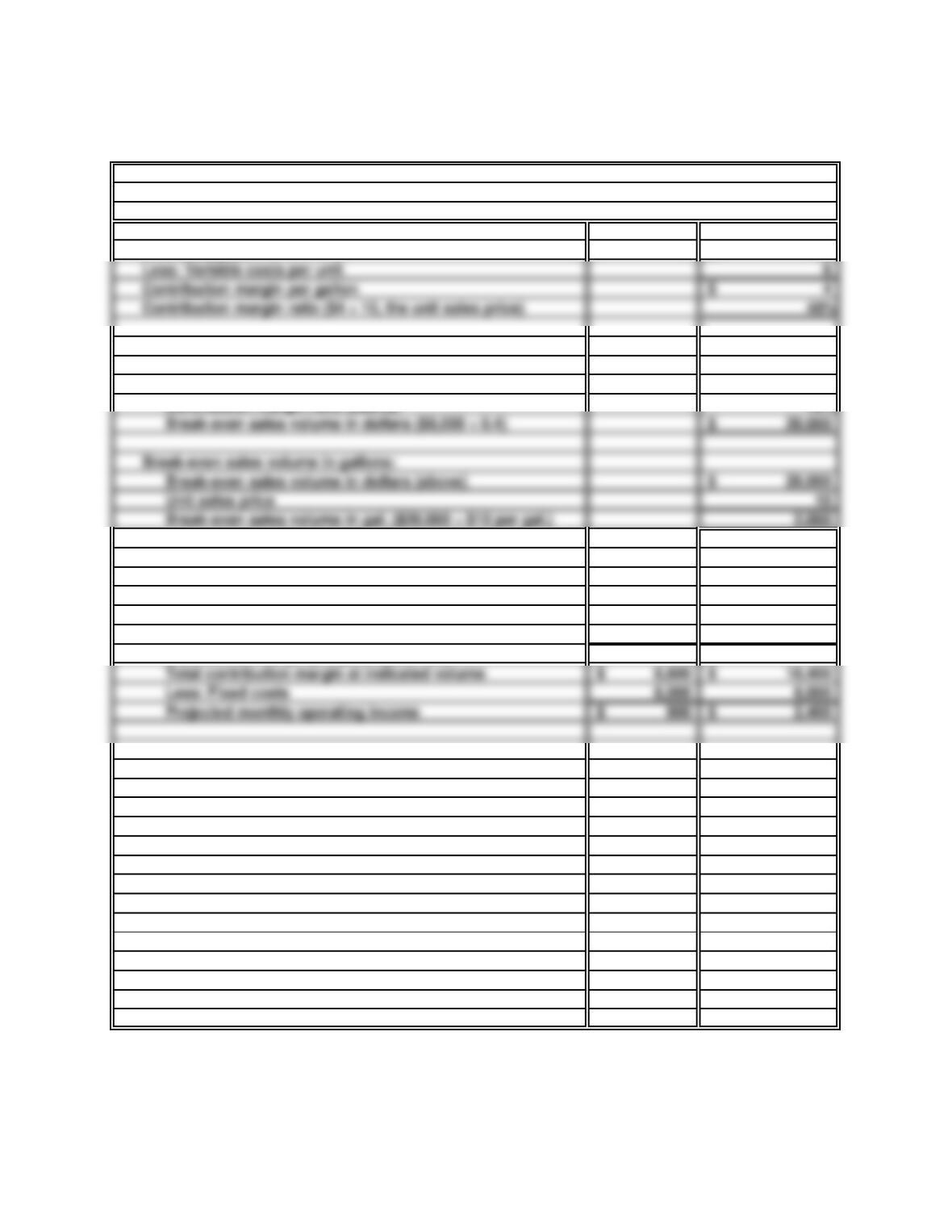

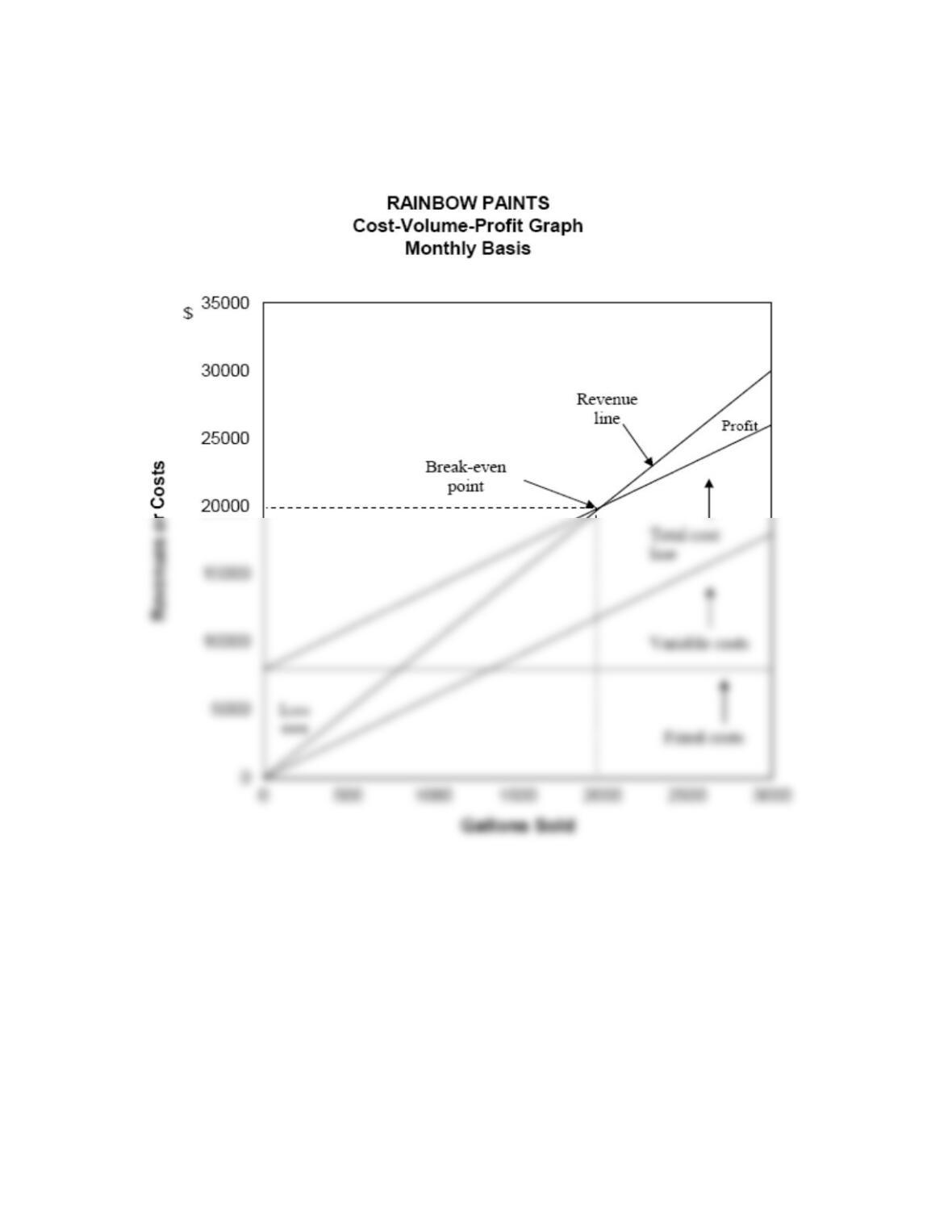

PROBLEM 20.4A

RAINBOW PAINTS

a. Contribution margin ratio:

Unit sales price 10$

Break-even sales volume in dollars:

Fixed costs ($3,160 + $3,640 + $1,200) 8,000$

Contribution margin ratio (above) 40%

b. On the following page.

c. Projected operating income at various levels:

2,200 Gallons 2,600 Gallons

Contribution margin per gallon ($10 – $6) 4$ 4$

30 Minutes, Medium

PROBLEM 20.4A

RAINBOW PAINTS (concluded)

b.

40 Minutes, Strong

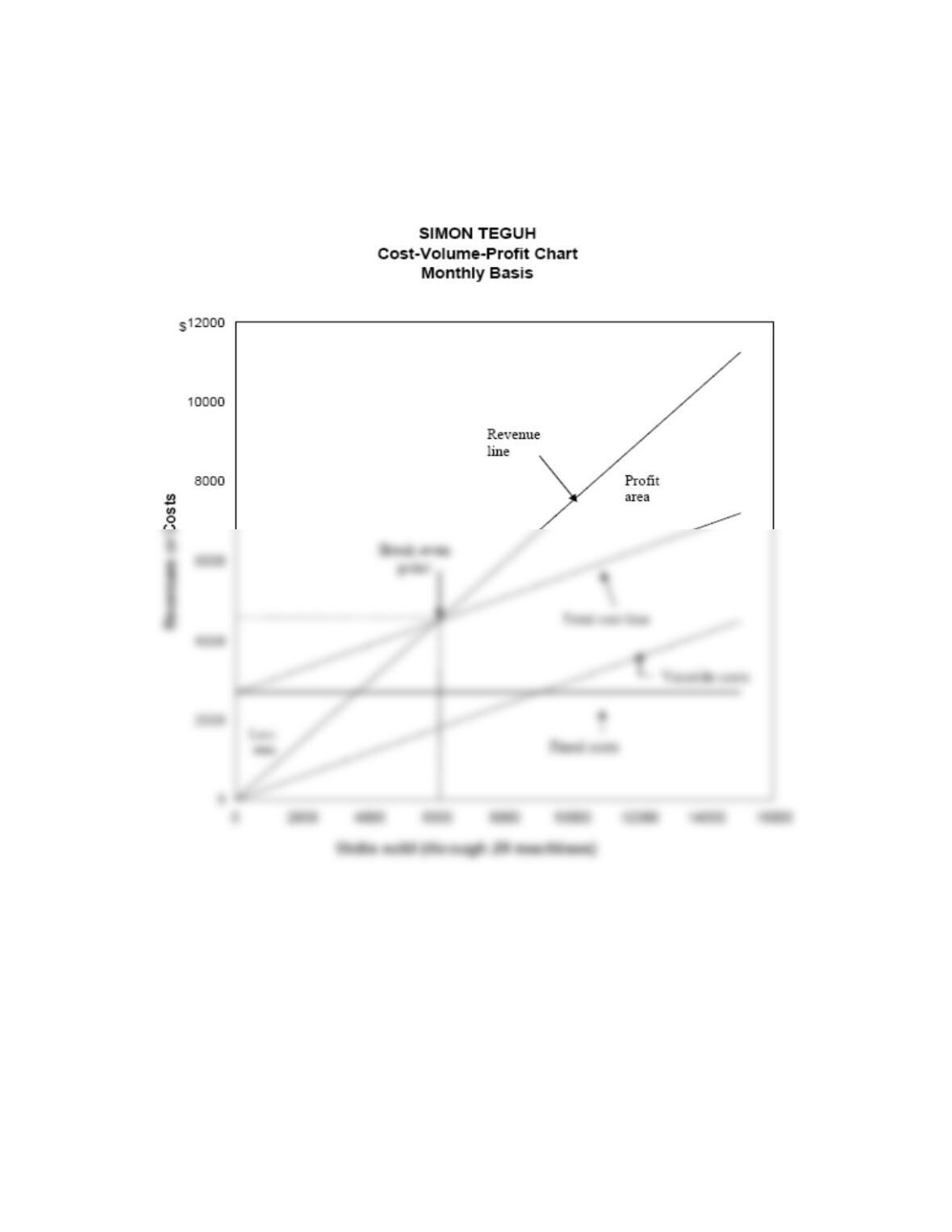

PROBLEM 20.5A

SIMON TEGUH

a. Unit contribution margin:

Sales price per unit 0.75$

Less: Variable costs per unit:

Break-even volume in units:

Monthly fixed costs:

Depreciation ($36,000 × 0.20 × 1/12) 600$

Wages 1,500

Contribution margin per unit (above) 0.45$

Break-even volume in units ($2,700 ÷ $0.45) 6,000

Break-even volume in dollars:

Break-even volume in units (above) 6,000

Unit sales price 0.75$

Break-even volume in dollars (6,000 units × $0.75) 4,500$

b. See following page.

c. Sales volume to produce operating income equal to 30%

return on investment:

Total monthly fixed costs (part a)2,700$

Desired operating income ($45,000 × 30% × 1/12) 1,125

Contribution margin per unit (part a)0.45$

Sales volume in units ($3,825 ÷ $0.45 per unit) 8,500

Less: Variable costs per unit (only merchandise cost) 0.25 0.50$

Unit contribution margin 0.45$

PROBLEM 20.5A

SIMON TEGUH (concluded)

b.

30 Minutes, Strong PROBLEM 20.6A

PRECISION SYSTEMS

a. Variable costs per unit before 15% increase in the cost of

direct labor 60$

Increase in cost of direct labor, 15% of $20 3

Variable costs and expenses per unit

after 15% increase in the cost of direct labor 63$

Because the contribution margin ratio of 40% is required,

the variable costs of $63 per unit must equal 60%

of sales price after the wage increase.

c. Current After

Capacity Expansion

(20,000 Units) (25,000 Units)

Total contribution margin ($37 per unit) 740,000$ 925,000$

Less: Fixed costs 390,000 530,000*

Operating income at full capacity 350,000$ 395,000$

Sales volume required to maintain current operating income:

Sales price before increase 100

Required increase in sales price per unit 5$

Unit contribution margin 37$

35 Minutes, Strong PROBLEM 20.7A

PERCULA FARMS

a. Raising clownfish will result in the highest

operating income.

Clownfish Angelfish

Number of salable fish 100,000 50,000

× sale price 4$ 10$

Total revenue 400,000$ 500,000$

b.

c. and d.

Operating income with new filter material:

Clownfish Angelfish

Number of salable fish 120,000 60,000

× sale price 4$ 10$

Total revenue 480,000$ 600,000$

Heating and lighting 14,000 20,000

Total variable costs 138,500$ 239,500$

Fixed costs: 88,000 88,000

Operating income 253,500$ 272,500$

The most important factors in determining operating income are survival rates, and the

costs of feeding and water changes.

Heating and lighting 14,000 20,000

Total variable costs 133,250$ 279,500$

Fixed costs: 80,000 80,000

Operating income 186,750$ 140,500$

PROBLEM 20.7A

PERCULA FARMS (concluded)

c. and d.

Operating income with new heating and lighting

equipment: Clownfish Angelfish

Number of salable fish 105,000 55,000

× sale price 4$ 10$

Total revenue 420,000$ 550,000$

Operating income 202,250$ 187,500$

PROBLEM 20.8A

LIFEFIT PRODUCTS

a. Contribution margins of product lines:

Shoes ($15 contribution margin ÷ $50 sales price) 30%

Shorts ($4 contribution margin ÷ $5 sales price) 80%

b. (1) Average contribution margin ratio:

From shoes (30% contribution margin × 80% of sales mix) 24%

(2) Monthly operating income:

Total sales 1,000,000$

Average contribution margin ratio × 40%

Total contribution margin ($1,000,000 × 40%) 400,000$

Less: Fixed costs and expenses 378,000

Operating income 22,000$

Average contribution margin ratio ÷ 40%

Break-even sales volume ($378,000 ÷ 40%) 945,000$

(3) Monthly break-even sales volume (in dollars):

From shorts (80% contribution margin × 30% of sales) 24%

Average contribution margin ratio 45%

c. Assuming new sales mix (shoes, 70%; shorts, 30%)

(1) Average contribution margin ratio:

(2) Monthly operating income:

Total sales 1,000,000$

Average contribution margin ratio × 45%

Less: Fixed costs and expenses 378,000

Average contribution margin ratio ÷ 45%

Break-even sales volume ($378,000 ÷ 45%) 840,000$

35 Minutes, Strong

From shorts (80% contribution margin × 20% of sales mix) 16%

Average contribution margin ratio 40%

PROBLEM 20.8A

LIFELIFT PRODUCTS (concluded)

d.

In the new sales mix, increased sales of shorts have replaced some sales of shoes. Shorts

SOLUTIONS TO PROBLEMS SET B

25 Minutes, Medium

PROBLEM 20.1B

NATHE, INC.

a. Required contribution margin per unit

Budgeted operating Income 200,000$

Fixed costs 600,000

Required sales price per unit:

Required contribution margin per unit 20$

c. Margin of safety at 40,000 units:

Sales volume at 40,000 units ($100 x 40,000) 4,000,000$

PROBLEM 20.1B

NATHE, INC. (concluded)

d.

Yes. With a unit sales price of $96, the break-even sales volume is 37,500 units: