Chapter 2 – The Accounting Cycle: During the Period

Exercise 2-13 (LO 2-4)

Corrections

External Transaction

Accounts

Debit

Credit

1.

Pay cash dividends of $800 to

stockholders.

Dividends

800

Cash

800

2.

Provide services on account for

customers, $3,400

Accounts Receivable

3,400

Service Revenue

3,400

Cash

Accounts Payable

Note: Accounts in blue are corrected items.

Accounts in black need no correction.

Chapter 2 – The Accounting Cycle: During the Period

Exercise 2-14 (LO 2-5)

Cash

5,000

Exercise 2-15 (LO 2-5)

Cash

Accounts Receivable

(3)

(6)

3,400

10,200

1,100

1,000

3,700

(4)

(5)

(1)

4,200

8,400

10,200

(3)

10,000

2,400

8,400

Chapter 2 – The Accounting Cycle: During the Period

Exercise 2-16 (LO 2-5)

1. Provide services to customers for cash, $20,000.

2. Provide services to customers on account, $5,000.

Exercise 2-17 (LO 2-6)

Sooner Company

Trial Balance

April 30

Accounts

Debit

Credit

Cash

$ 3,900

Accounts Receivable

6,100

Prepaid Rent

7,400

Land

Accounts Payable

Deferred Revenue

Common Stock

Retained Earnings

Service Revenue

Supplies Expense

9,400

Salaries Expense

Chapter 2 – The Accounting Cycle: During the Period

Exercise 2-18 (LO 2-6)

Cobras Incorporated

Trial Balance

March 31

Accounts

Debit

Credit

Cash

$ 3,500

Accounts Receivable

4,200

Supplies

1,000

Prepaid Insurance

Buildings

$ 2,200

Salaries Payable

Common Stock

Retained Earnings

Service Revenue

Salaries Expense

6,400

Utilities Expense

Chapter 2 – The Accounting Cycle: During the Period

Exercise 2-19 (LO 2-4, 2-5, 2-6)

Requirement 1

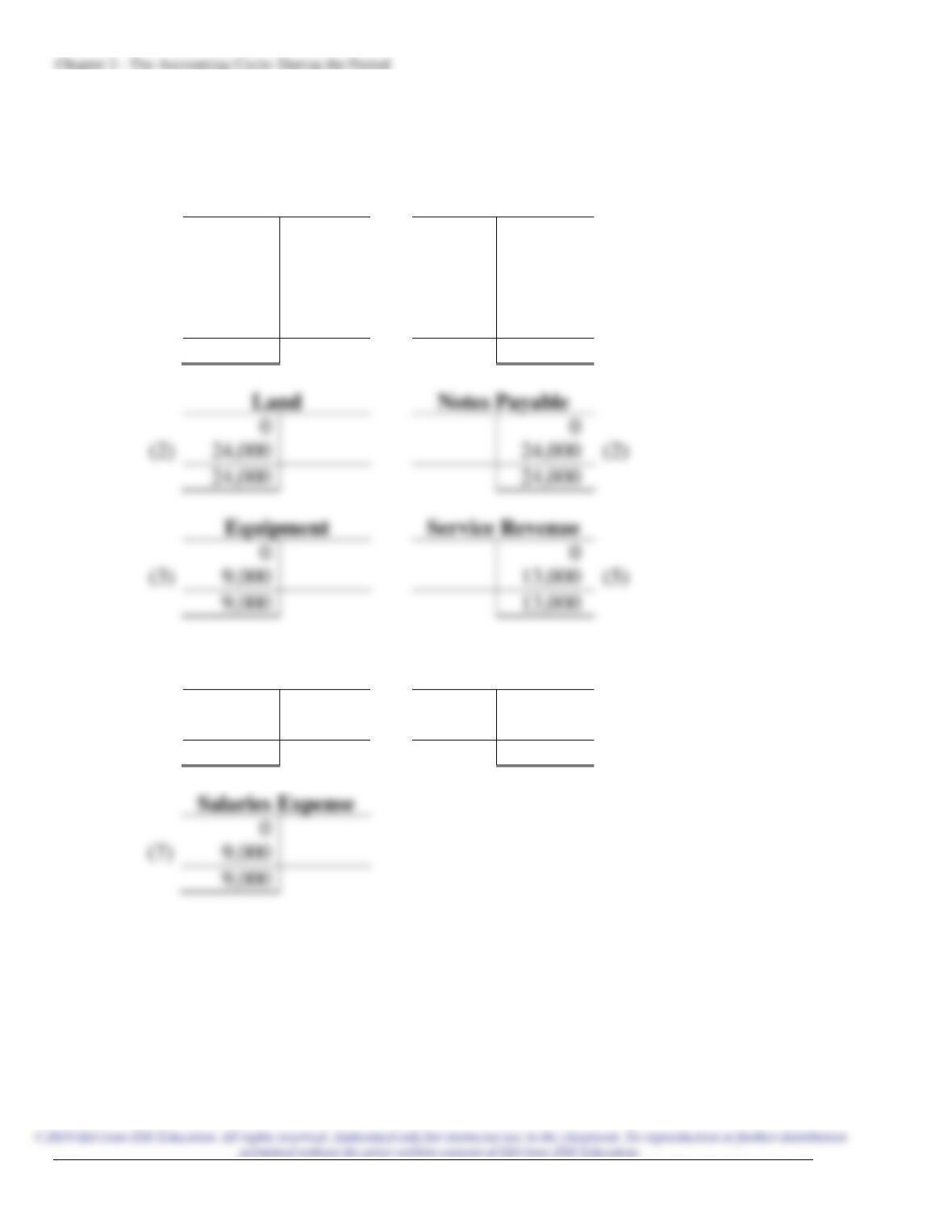

(1) January 1

Debit

Credit

Cash

42,000

Common Stock

42,000

(Issue common stock)

(2) January 5

Land

Notes Payable

(3) January 9

Equipment

Cash

(Purchase storage containers)

(4) January 12

No entry

(5) January 18

Cash

13,000

Service Revenue

13,000

(Receive cash for current month’s rent)

(6) January 23

Supplies

Accounts Payable

Salaries Expense

Cash

2-26 Financial Accounting, 5e

Exercise 2-19 (continued)

Requirement 2

Cash

Common Stock

(1)

(5)

0

42,000

13,000

9,000

9,000

(3)

(7)

0

42,000

(1)

37,000

42,000

(2)

0

0

(2)

0

0

Supplies

Accounts Payable

(6)

0

3,000

0

3,000

(6)

3,000

3,000

Chapter 2 – The Accounting Cycle: During the Period

Exercise 2-19 (concluded)

Requirement 3

Green Wave Company

Trial Balance

Accounts

Debit

Credit

Cash

$37,000

Supplies

3,000

Land

Equipment

9,000

Accounts Payable

Notes Payable

Common Stock

Service Revenue

Salaries Expense

9,000

Chapter 2 – The Accounting Cycle: During the Period

2-28 Financial Accounting, 5e

Exercise 2-20 (LO 2-4, 2-5, 2-6)

Requirement 1

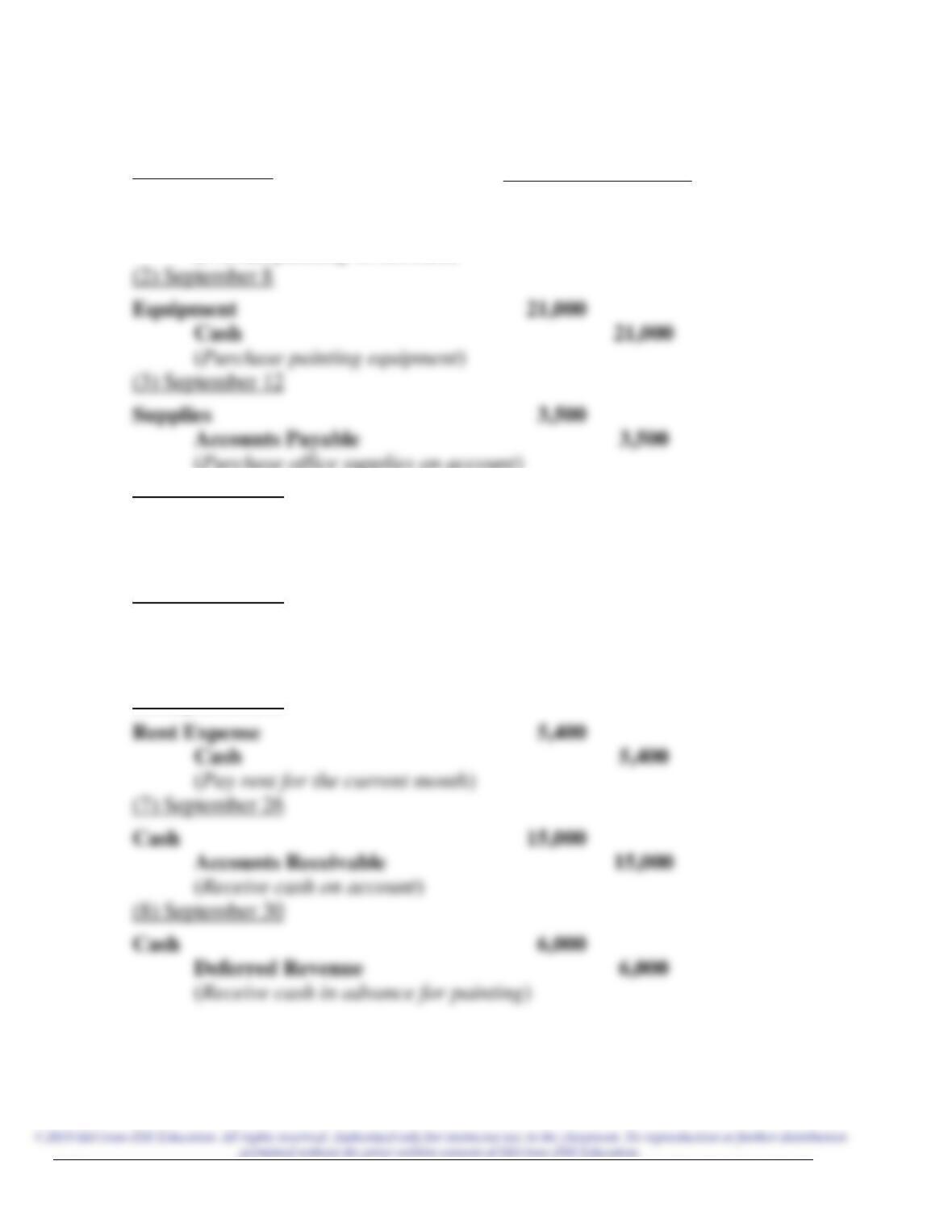

(1) September 3

Debit

Credit

Accounts Receivable

20,000

Service Revenue

20,000

(Provide painting on account)

(2) September 8

Equipment

(Purchase painting equipment)

Supplies

3,500

Accounts Payable

3,500

(Purchase office supplies on account)

(4) September 15

Salaries Expense

4,200

Cash

4,200

(Pay salaries for the current month)

(5) September 19

Advertising Expense

1,000

Cash

1,000

(Pay advertising for the current month)

(6) September 22

Rent Expense

Cash

5,400

(Pay rent for the current month)

(7) September 26

Cash

(Receive cash on account)

(8) September 30

Cash

6,000

Deferred Revenue

6,000

(Receive cash in advance for painting)

Chapter 2 – The Accounting Cycle: During the Period

Exercise 2-20 (continued)

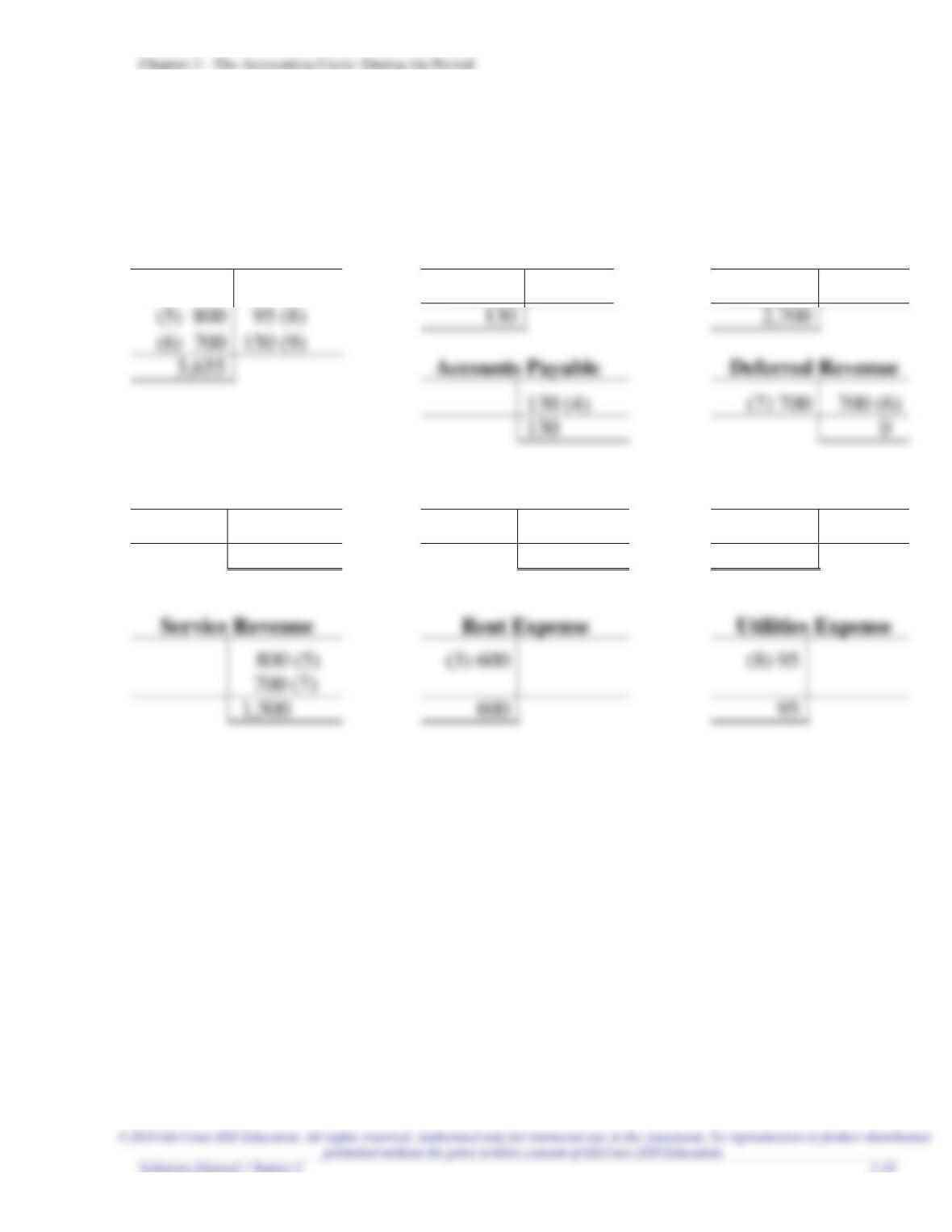

Requirement 2

Accounts Receivable

Service Revenue

Beg.

(1)

1,700

20,000

15,000

(7)

0

20,000

Beg.

(1)

6,700

20,000

Supplies

Accounts Payable

Beg.

(3)

500

3,500

1,200

3,500

Beg.

(3)

4,000

4,700

Salaries Expense

Advertising Expense

Beg.

(4)

0

4,200

Beg.

(5)

0

1,000

4,200

1,000

Beg.

(6)

6,000

Beg.

6,000

Retained Earnings

Beg.

Beg.

Chapter 2 – The Accounting Cycle: During the Period

2-30 Financial Accounting, 5e

Exercise 2-20 (concluded)

Requirement 3

Boilermaker House Painting Company

Trial Balance

Accounts

Debit

Credit

Cash

$35,500

Accounts Receivable

6,700

Supplies

4,000

Equipment

Accounts Payable

Deferred Revenue

6,000

Common Stock

Retained Earnings

Service Revenue

Salaries Expense

4,200

Advertising Expense

1,000

Rent Expense

$85,200

$85,200

Chapter 2 – The Accounting Cycle: During the Period

PROBLEMS: SET A

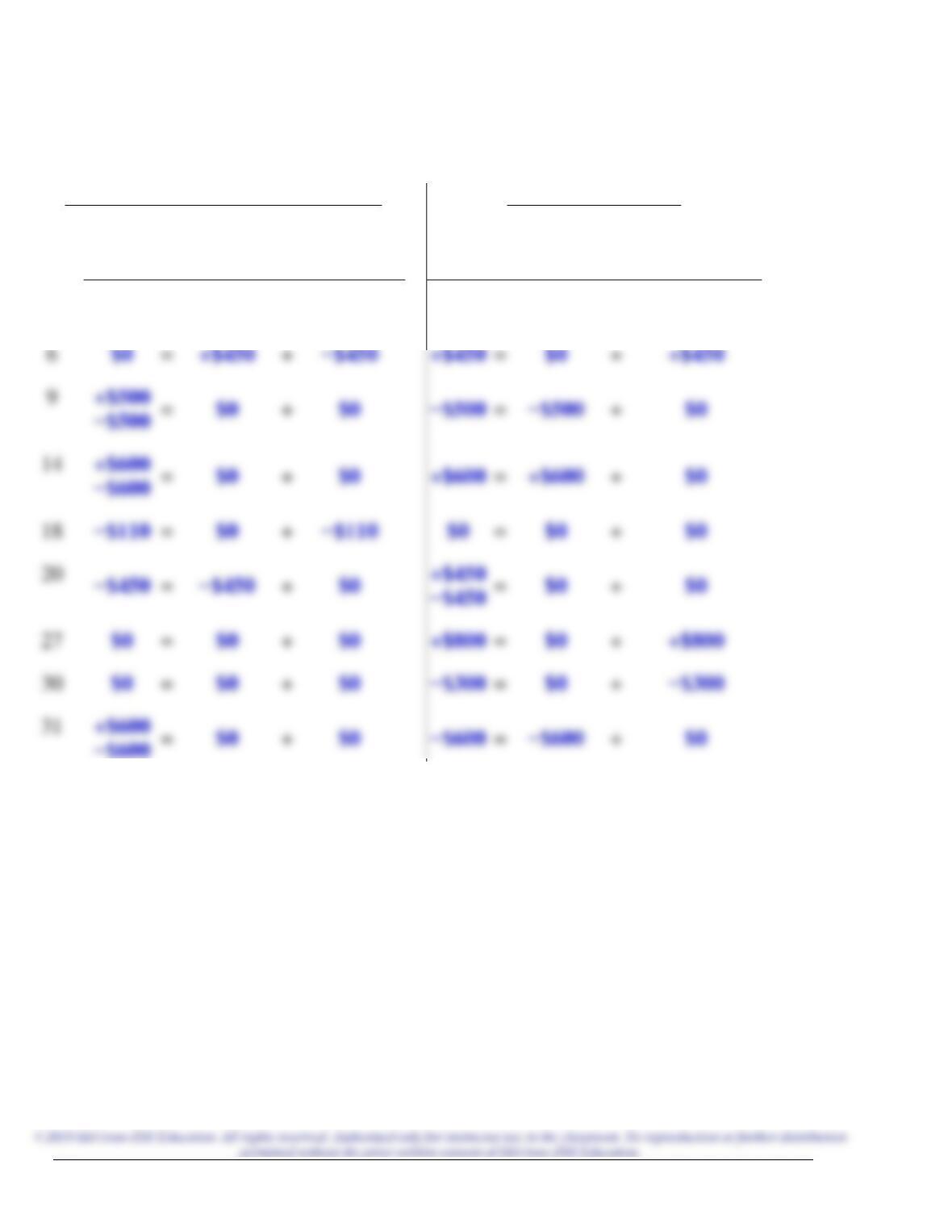

Problem 2-1A (LO 2-2)

Transaction

Assets

=

Liabilities

+

Stockholders’

Equity

1. Issue common stock in

exchange for cash.

Increase

=

No effect

+

Increase

2. Purchase business

supplies on account.

Increase

=

+

No effect

for the current month.

4. Provide services to

Increase

=

No effect

+

Increase

5. Pay employee salaries

for the current month.

Decrease

=

No effect

+

Decrease

6. Provide services to

customers for cash.

Increase

=

No effect

+

Increase

7. Pay for advertising for

the current month.

Decrease

=

No effect

+

Decrease

8. Repay loan from the

bank.

9. Pay dividends to

Decrease

=

No effect

+

Decrease

10. Receive cash from

customers in (4)

above.

No effect*

=

No effect

+

No effect

Decrease

Decrease

No effect

Chapter 2 – The Accounting Cycle: During the Period

2-32 Financial Accounting, 5e

Problem 2-2A (LO 2-2)

Transaction

Assets

=

Liabilities

+

Stockholders’

Equity

1. Provide services to

customers on account,

$1,600.

+$1,600

=

$0

+

+$1,600

2. Pay $400 for current

month’s rent.

−$400

=

$0

+

−$400

4. Pay $100 for advertising

−$100

=

$0

+

−$100

=

$0

+

$0

6. Receive cash of $1,000

from customers in (1)

above.

+$1,000

−$1,000

=

$0

+

$0

7. Obtain a loan from the bank

for $7,000.

+$7,000

=

+$7,000

+

$0

=

+

=

$0

+

8. Receive a bill of $200 for

Chapter 2 – The Accounting Cycle: During the Period

Problem 2-3A (LO 2-3)

Accounts

Type of Account

Normal Balance

(Debit or Credit)

1. Salaries Payable

Liability

Credit

2. Common Stock

Stockholders’ equity

Credit

3. Prepaid Rent

Asset

Debit

4. Buildings

Asset

Debit

6. Equipment

Asset

Debit

7. Rent Expense

Expense

Debit

8. Notes Payable

Liability

Credit

9. Salaries Expense

Expense

Debit

Asset

Debit

Revenue

Credit

Chapter 2 – The Accounting Cycle: During the Period

Problem 2-4A (LO 2-4)

Transactions for Jake’s Lawn Maintenance Company

July 3

Debit

Credit

Accounts Receivable

500

Service Revenue

500

(Provide services on account)

July 6

Repairs and Maintenance Expense

450

Accounts Payable

450

(Receive maintenance on account)

July 9

Cash

500

Accounts Receivable

500

(Receive cash on account)

July 14

Notes Receivable

600

Cash

600

(Loan cash by accepting note receivable)

July 18

Advertising Expense

110

Cash

(Pay advertising for the current month)

July 20

Accounts Payable

(Pay cash on account)

July 27

No entry for Jake.

No entry for Jake.

July 31

Cash

600

Notes Receivable

600

(Receive cash on note receivable)

Chapter 2 – The Accounting Cycle: During the Period

Problem 2-5A (LO 2-2, 2-4)

Transactions for Luke’s Repair Shop

July 3

Debit

Credit

Repairs and Maintenance Expense

500

Accounts Payable

500

(Receive services on account)

July 6

Accounts Receivable

450

Service Revenue

450

(Provide services on account)

July 9

Accounts Payable

500

Cash

500

(Pay cash on account)

July 14

Cash

600

Notes Payable

600

(Borrow by signing note payable)

July 18

No entry for Luke.

July 20

Cash

Accounts Receivable

(Receive cash on account)

July 27

Cash

800

Service Revenue

800

(Provide services for cash)

July 30

Salaries Expense

300

Cash

300

(Pay salaries to employees)

July 31

Notes Payable

600

Cash

600

(Pay note payable)

Chapter 2 – The Accounting Cycle: During the Period

2-36 Financial Accounting, 5e

Problem 2-5A (concluded)

Jake’s Lawn Maintenance Company

Luke’s Repair Shop

Assets

=

Liabilities

+

Stockholders’

Equity

Assets

=

Liabilities

+

Stockholders’

Equity

July 3

+$500

=

$0

+

+$500

$0

=

+$500

+

−$500

+

=

+

Chapter 2 – The Accounting Cycle: During the Period

Problem 2-6A (LO 2-6)

Bruins Company

Trial Balance

November 30

Accounts

Debit

Credit

Cash

$ 40,000

Accounts Receivable

50,000

Supplies

1,100

Equipment

Accounts Payable

Salaries Payable

Interest Payable

Deferred Revenue

Notes Payable

Common Stock

50,000

Retained Earnings

35,000

Dividends

1,100

Service Revenue

65,000

Salaries Expense

30,000

Rent Expense

12,000

Interest Expense

Supplies Expense

Utilities Expense

$214,000

Chapter 2 – The Accounting Cycle: During the Period

Problem 2-7A (LO 2-4, 2-5, 2-6)

Requirement 1

Entries are numbered for posting.

(1)

March 1

Debit

Credit

Cash

3,000

Common Stock

3,000

(Issue common stock)

(2)

March 3

Equipment

2,700

2,700

(Purchase sewing equipment with note payable)

(3)

March 5

Cash

600

(Pay rent for current month)

March 7

(4)

March 12

Supplies

130

130

(Purchase sewing supplies on account)

(5)

March 15

Cash

800

Service Revenue

800

(Provide services for cash)

(6)

March 19

Cash

700

Deferred Revenue

700

(Receive cash in advance from customer)

(7)

March 25

Deferred Revenue

700

Service Revenue

700

(Provide services to customer)

(8)

March 30

(Pay utilities for current month)

(9)

March 31

Dividends

150

150

(Pay dividends)

Problem 2-7A (continued)

Requirements 2 and 3

Cash

Supplies

Equipment

(1) 3,000

600 (3)

(4) 130

(2) 2,700

150 (9)

130 (4)

(7) 700

Notes Payable

Common Stock

Dividends

2,700 (2)

3,000 (1)

(9) 150

2,700

3,000

150

Chapter 2 – The Accounting Cycle: During the Period

2-40 Financial Accounting, 5e

Problem 2-7A (concluded)

Requirement 4

Ute Sewing Shop

Trial Balance

March 31

Accounts

Debit

Credit

Cash

$3,655

Supplies

130

Equipment

Accounts Payable

$ 130

Notes Payable

2,700

Common Stock

3,000

Dividends

150

Utilities Expense