Page 1 of 9

CHAPTER 2

OVERVIEW OF BUSINESS PROCESSES

Instructor’s Manual

Learning Objectives:

1. Describe the four parts of the data processing cycle and the

major activities in each.

3. Describe the ways information is stored in computer-based

information systems.

Questions to be addressed in this chapter include:

1. How should I organize the accounting records so that financial

statements can be easily produced?

2. How am I going to collect and process data about all of S&S’s

transactions?

3. How do I organize all the data that will be collected?

4. How should I design the AIS so that the information provided is

reliable and accurate?

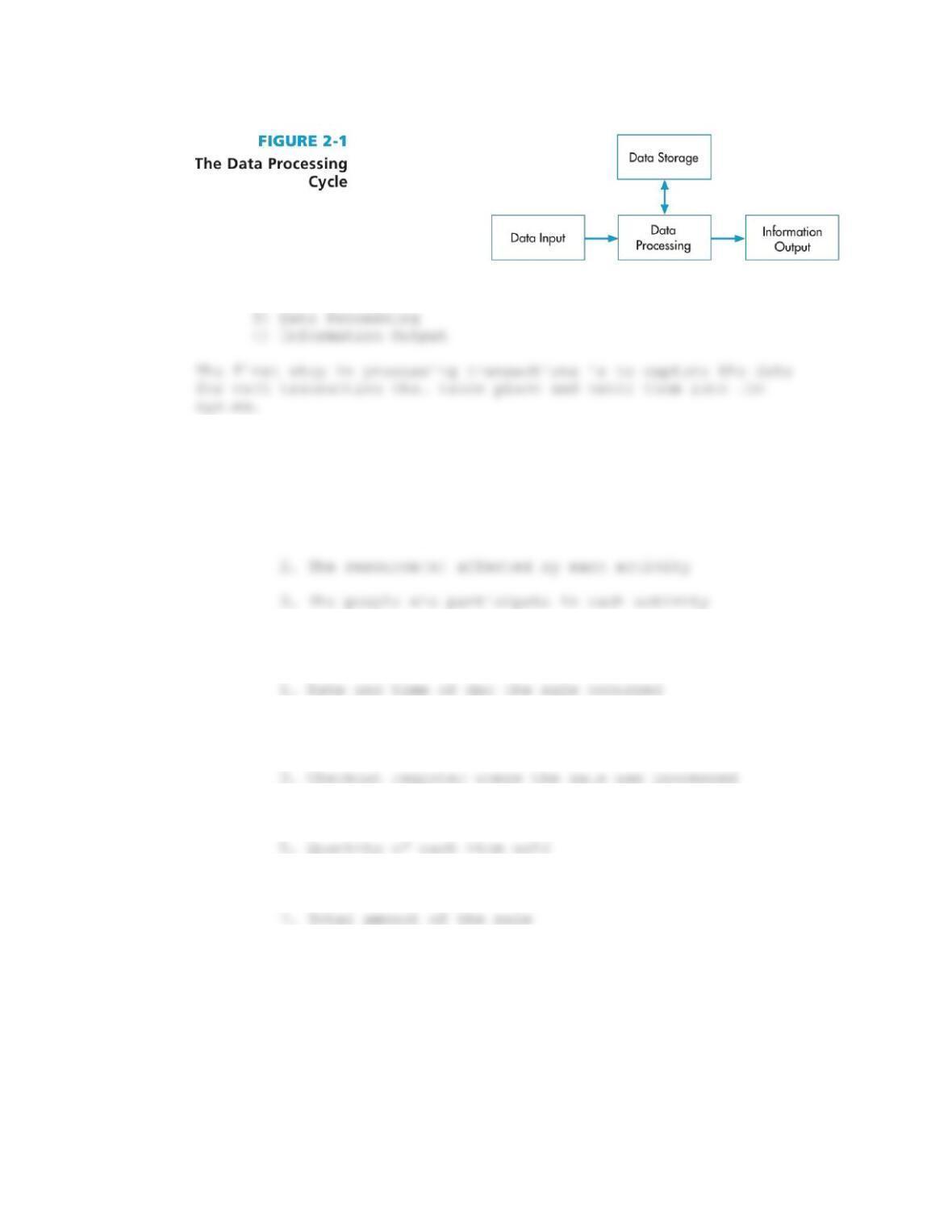

Transaction Processing: The Data Processing Cycle

Four Major Steps in the Data Processing Cycle

Page 2 of 9

1) Data Input

2) Data Storage

Data Input

Data must be collected about three facets of each business

activity:

1. Each activity of interest

For example, collect the following data about a sales

transaction:

2. Employee who made the sale and the checkout clerk who

processed the sale

4. Item(s) sold

6. List price and actual price of each item sold

8. For credit sales: delivery instructions, customer

bill-to and ship-to addresses, customer name

Information Output

This is the final step in the data processing cycle.

Forms of Information Output

Page 3 of 9

Documents are records of transaction or other company

data, such as checks and invoices.

Documents generated at the end of transaction

processing activities are called operational

documents to distinguish them from source documents,

which are used at the beginning of the process.

Purpose of Output

There are four main types of financial reports that were

covered in Principles of Accounting I & II courses, the

balance sheet, income statement, statement of owner’s

equity or statement of stockholder’s equity and the

statement of cash flows. Sometimes a statement of retained

Multiple Choice 1

Which of the following is NOT a step in the data processing cycle?

a. data collection c. data storage

b. data input d. data processing

Learning Objective Two

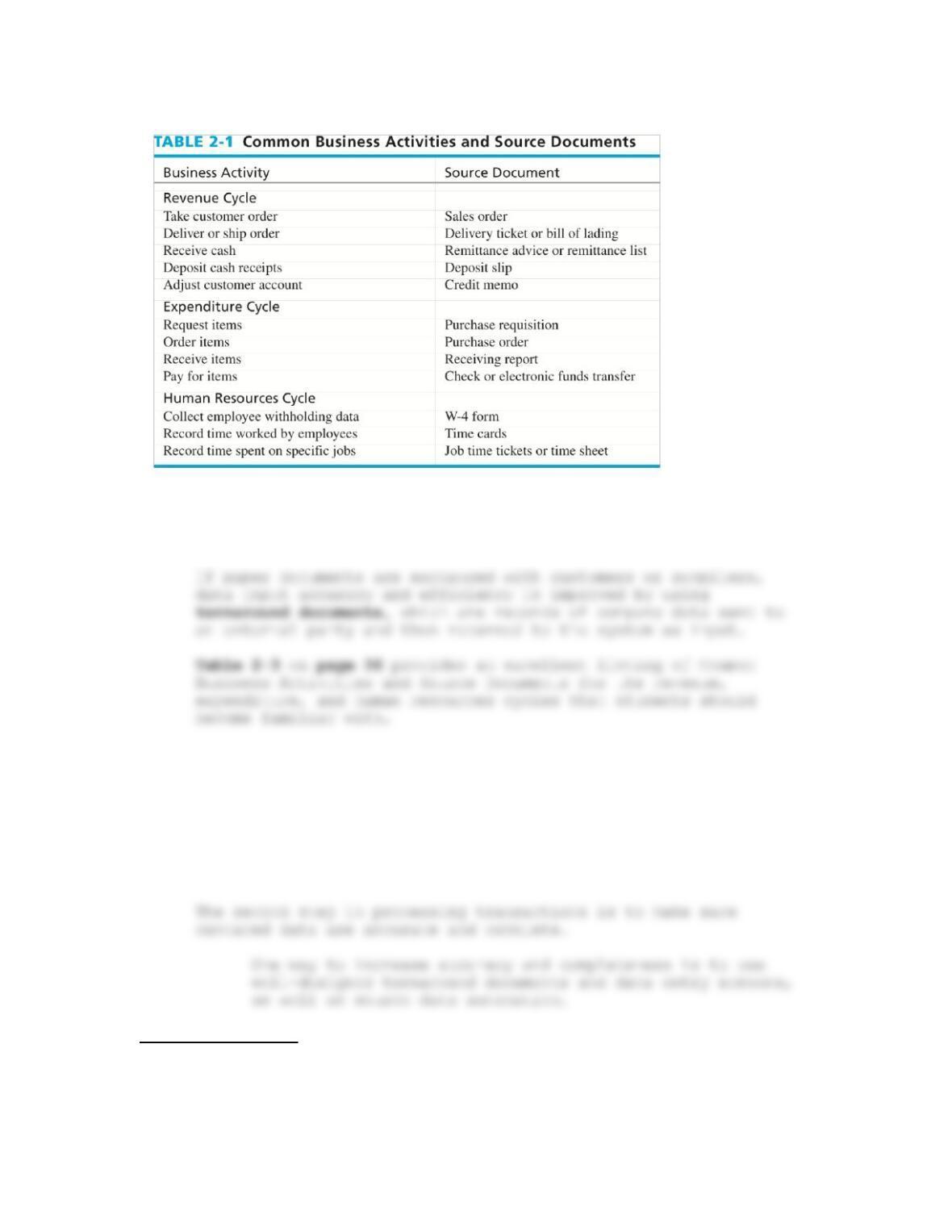

Describe documents and procedures used to collect

and process transaction data.

Page 4 of 9

Source Documents are documents used to collect data about their

business activities. Source documents are also used to support

the validity of the business activities.

Source Data Automation is yet another means to improve the

accuracy and efficiency of data input. An example would be once

the sale of merchandise is rung up on the cash register it would

be interfaced with accounting to automatically record the sale

and also interfaced with the warehouse to automatically reduce

the level of inventory for the item that was sold. This would

also be interfaced with purchasing in which the purchase order

would automatically be printed out for delivery to the vendor.

Multiple Choice 2

Which of the following documents is most likely to be used in the

expenditure cycle?

a. sales orders

Computer–Based Storage Concepts

An entity is something about which information is stored.

For example, employees, inventory items, and customers.

Each entity has attributes, or characteristics of interest,

which need to be stored. For example, an employee’s hourly

rate of pay, unit cost of an inventory item, and a

customer’s address.

Figure 2-5 on page 42 provides examples of data storage

elements:

1. Data values are stored in a physical space called a

2. The sect of fields that contain data about various

3. The contents of each field within a record are called

4. In turn, data elements/data value is composed of

characters such as letters, numbers, and symbols.

6. Two basic types of files exist:

▪ A master file is conceptually similar to a ledger

Page 6 of 9

Data Processing

Once data about a business activity have been collected and

entered into the system they must be processed.

Data processing implies the execution of a certain procedures,

usually involving a series of tasks.

There are four different types of file processing:

1. Updating data previously stored about the activity, the

resources affected by the activity , or the people who

2. Changing data, such as changing a customer’s address

3. Adding data, such as adding a new employee to the

4. Deleting data, such as purging the vendor master file of

all vendors that the company no longer does business

with

Periodic updating of data is referred to as batch processing.

This approach may be combined with either the off-line or on-line

entry of data.

Multiple Choice 3

Recording and processing information about a transaction at the time it

takes place is referred to as which of the following?

a. batch processing

b. online, real-time processing

c. captured transaction processing

d. chart of accounts processing

Page 7 of 9

Data Storage

A company’s data are one of its most important resources.

Accountants need to know how to manage data for maximum corporate

use.

Ledgers

General Ledger contains summary-level data for every

asset, liability, equity, revenue, and expense

account of the organization.

Accounts receivable subsidiary ledger would

record detailed data for customers whom buy

products or services on credit.

The accounts receivable subsidiary ledger would

support the accounts receivable general ledger

controlling account.

Coding Techniques

Coding is the systematic assignment of numbers or

letters to items to classify and organize them.

1. With sequence codes, items are numbered

Page 8 of 9

2. With a block code, blocks of numbers within a

numerical sequence are reserved for categories

having meaning to the user

3. Group codes are often used in conjunction with the

block code. S&S uses a seven-digit product code

1. The code should be consistent with its intended use,

which requires the code designer to determine the types

of system outputs desired by users prior to selecting

the code.

Make sure the coding system is consistent (1) with the company’s

organizational structure and (2) across the different divisions of an

organization

Chart of Accounts

A chart of accounts is a list of all general ledger accounts an

organization uses with each general ledger account being assigned

a specific number.

Audit Trail The accounting data and records should provide a trail

Page 9 of 9

Multiple Choice 4

How does the chart of accounts list general ledger accounts?

a. alphabetical order

b. chronological order

c. size order

d. the order in which they appear in financial statements

Multiple Choice 5

Which of the following is NOT an advantage of an ERP system?

a. better access control

b. standardization of procedures and reports

c. improved monitoring capabilities

d. simplicity and reduced costs

ANSWERS to Multiple Choice Questions: