2

Cost Concepts and Behavior

Solutions to Review Questions

2-1.

Cost is a more general term that refers to a sacrifice of resources and may be either an

2-2.

2-7.

Both accounts represent the cost of the goods acquired from an outside supplier, which

include all costs necessary to ready the goods for sale (in merchandising) or production

2-8.

Direct materials:

converting the materials into finished product. Assembly workers,

Materials in their raw or unconverted form, which become an integral

part of the finished product are considered direct materials. In some

2-9.

2-13.

A value income statement typically uses a contribution margin framework, because the

contribution margin framework is more useful for managerial decision-making. In

Solutions to Critical Analysis and Discussion Questions

2-15.

The statement is not true. Materials can be direct or indirect. Indirect materials include

2-16.

2-17.

Marketing and administrative costs are treated as period costs and expensed for

2-21.

Answers will vary. The major cost categories include servers (mostly fixed), personnel

2-22.

2-23.

Answers will vary. Common suggestions are number of students in each program,

2-24.

No, R&D costs are relevant for many decisions. For example, should a program of

2-25.

This question can create a good discussion of the different roles of financial and

Solutions to Exercises

2-26. (15 min.) Basic Concepts.

2-27. (15 min.) Basic Concepts.

Cost Item

Fixed (F)

Variable (V)

Period (P)

Product (M)

a.

Depreciation on buildings for administrative staff offices ……

F

P

b.

Cafeteria costs for the factory ……………………………………….

F

M

Overtime pay for assembly workers ……………………………….

d.

Transportation-in costs on materials purchased ………………

V

M

e.

F

P

Sales commissions for sales personnel ………………………….

g.

Assembly line workers’ wages ………………………………………

V

M

h.

Controller’s office rental ……………………………………………….

F

P

Administrative support for sales supervisors ……………………

j.

Energy to run machines producing units of output in the

V

M

2-28. (10 min.) Basic Concepts.

a.

Assembly line worker’s salary. ……………………………………………………………

B

Direct materials used in production process. ………………………………………..

Property taxes on the factory. …………………………………………………………….

C

d.

Lubricating oil for plant machines. ………………………………………………………

C

Transportation-in costs on materials purchased. …………………………………..

2-29. (15 min.) Basic Concepts.

Concept

Definition

9

Period cost ……………………

Cost that can more easily be attributed to

time intervals.

2

Indirect cost …………………..

cost object.

Fixed cost ……………………..

Cost that does not vary with the volume of

activity.

8

Opportunity cost …………….

Lost benefit from the best forgone

alternative.

Outlay cost ……………………

Past, present, or near-future cash flow.

6

Direct cost …………………….

Cost that can be directly related to a cost

object.

5

Expense ……………………….

Cost charged against revenue in a

particular accounting period.

Cost ……………………………..

Sacrifice of resources.

4

Full absorption cost ………..

Cost used to compute inventory value

according to GAAP.

Product cost ………………….

Cost that is part of inventory.

2-30. (15 min.) Basic Concepts.

Cost Item

Fixed (F)

Variable (V)

Period (P)

Product (M)

a.

Power to operate factory equipment …………………………..

V

M

Commissions paid to sales personnel …………………………

V

Office supplies for the human resources manager ………..

F

2-31. (15 min.) Basic Concepts.

a.

Variable production cost per unit: ($360 + $60 + $15 + $30) …………………..

$465

b.

Variable cost per unit: ($465 + $45) …………………………………………………….

$510

d.

Full absorption cost per unit: [$465 + ($135,000 ÷ 1,500)] ………………………

$555

e.

Prime cost per unit. (materials + labor + outsource) ………………………………

$435

g.

Contribution margin per unit: ($900 – $510)………………………………………..

$390

h.

Gross margin per unit: ($900 – full absorption cost of $555)…………………..

$345

h. Gross margin = $900 – $573 = $327

2-32. (15 min.) Basic Concepts: Intercontinental, Inc.

a.

Prime cost per unit: (materials + labor) ………………………………………………..

$40

Gross margin per unit: ($100 – full absorption cost of $74)…………………….

Conversion cost per unit: (labor + overhead) ………………………………………..

Full absorption cost per unit: [$60 + ($4,200,000 ÷ 300,000)] ………………….

g.

Variable production cost per unit: ($16 + $24 + $20) ……………………………..

2-33. (15 min.) Cost Allocation—Ethical Issues

This problem is based on the experience of the authors’ research at several companies.

a. Answers will vary as there are several defensible bases on which to allocate the

product development costs. As an example, many government-purchasing contracts

2-34. (15 min.) Cost Allocation—Ethical Issues

This problem is based on the experience of the authors’ research at several companies.

a. Answers will vary as there are several defensible bases on which to allocate the

2-35. (30 min.) Prepare Statements for a Manufacturing Company: Tappan

Parts.

Tappan Parts

Cost of Goods Sold Statement

For the Year Ended December 31

Beginning work in process inventory …………..

$1,354,000

Manufacturing costs:

Direct materials:

Materials available ………………………….

$1,196,000

Other manufacturing costs ………………….

(c)

$2,860,000

Less ending work in process ……………

manufactured ………………………………………….

Beginning finished goods inventory …………….

Finished goods available for sale ……………….

Ending finished goods inventory ………………..

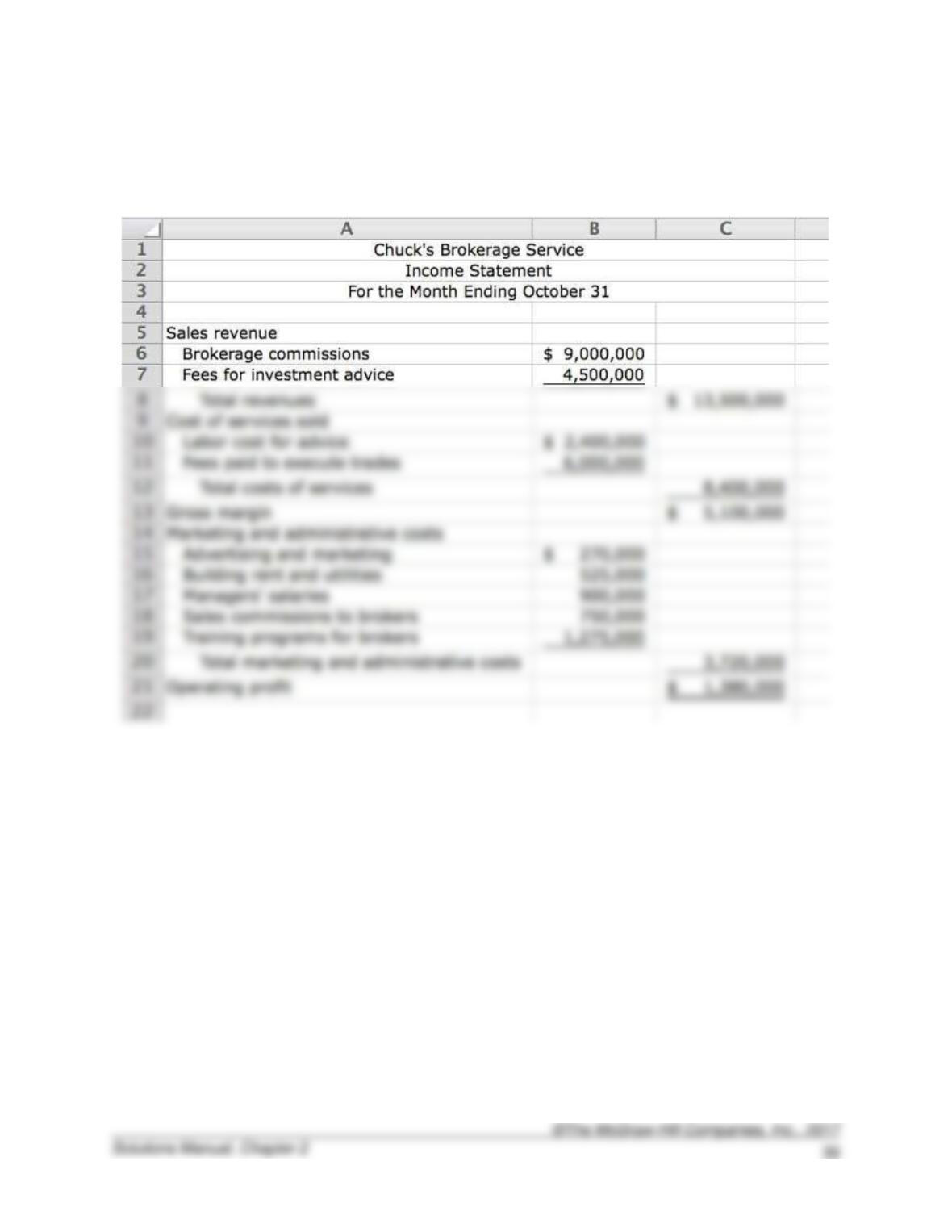

2-36. (10 min.) Prepare Statements for a Service Company: Chuck’s Brokerage

Service.

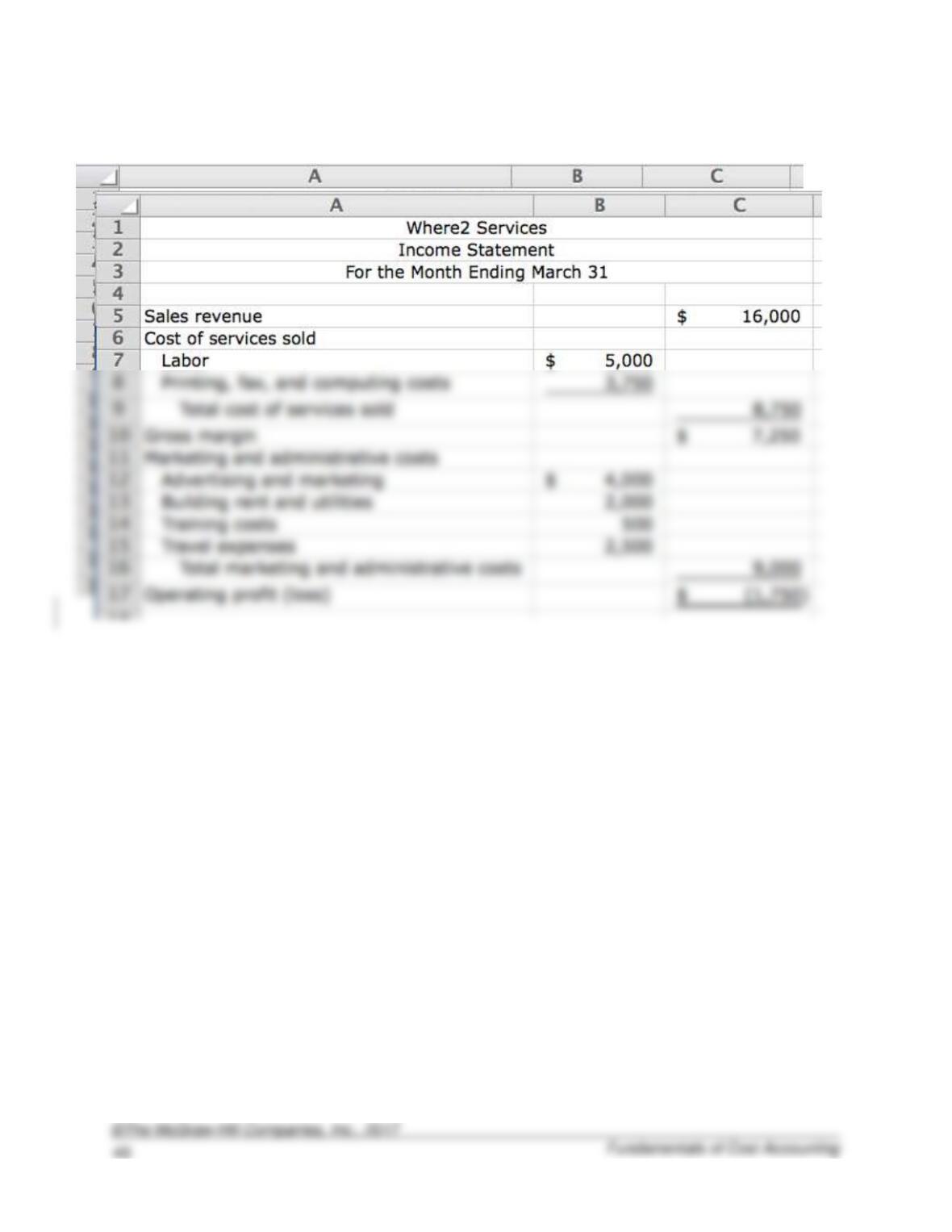

2-37. Prepare Statements for a Service Company: Where2 Services.

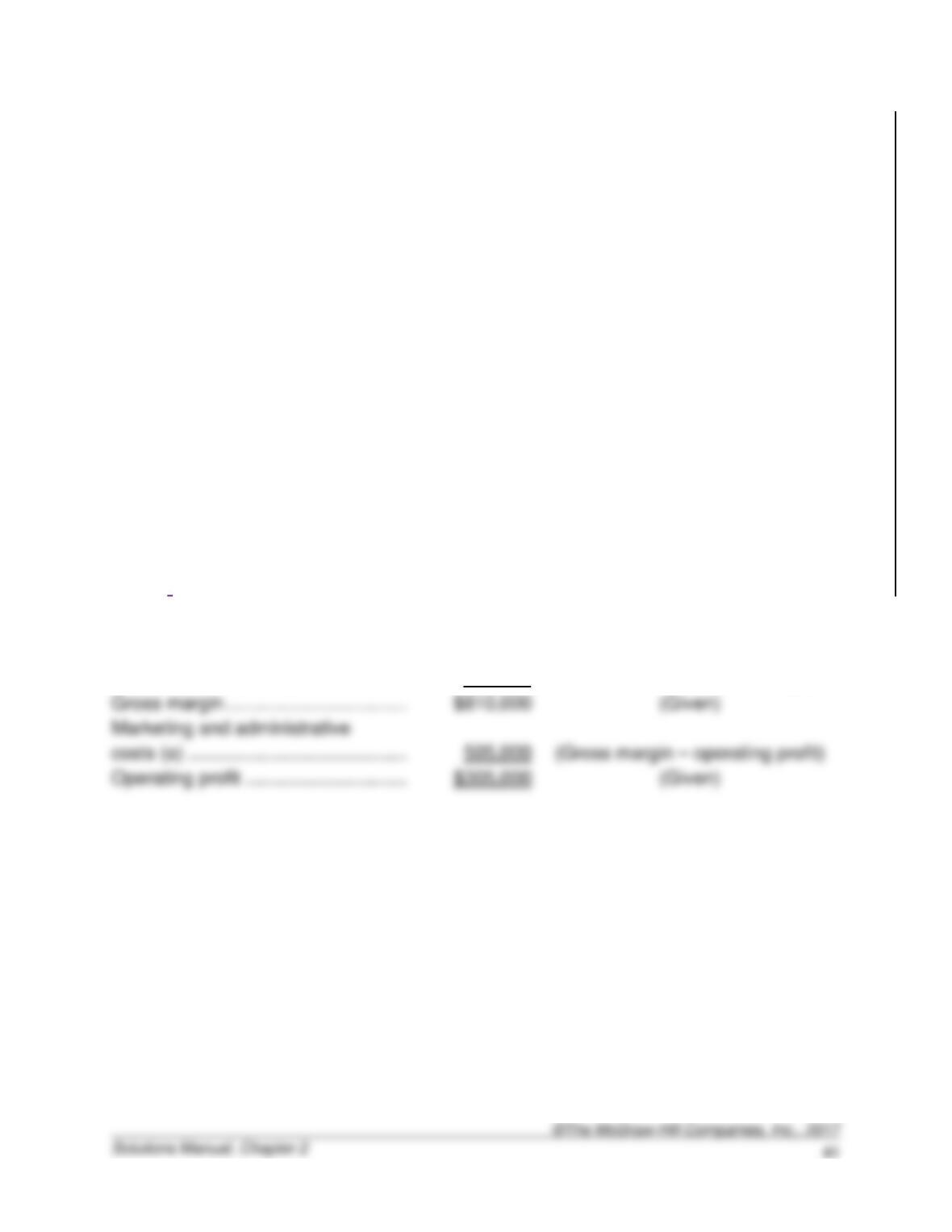

2-38. (10 min.) Prepare Statements for a Service Company: Remington

Advisors

Sales revenue ……………………………..

$1,700,000

(Given)

Cost of services sold (b) ………………..

890,000

(Sales revenue – gross margin)

Gross margin ……………………………….

(Given)

costs (a) ……………………………………..

505,000

2-39. (20 min.) Prepare Statements for a Service Company: Lead! Inc.

You can solve this in the order shown below.

Lead!, Inc.

Income Statement

For the Month Ended April 30

Sales revenue ……………………………………………………………………………..

$600,000

a

2-40. (30 min.) Prepare Statements for a Manufacturing Company: Crabtree

Machining Company.

Crabtree Machining Company

Cost of Goods Sold Statement

For the Year Ended December 31

Beginning work-in-process inventory ….

$ 139,200

Manufacturing costs:

Direct materials:

Beginning inventory …………………..

$115,200

Purchases ………………………………..

717,600

Materials available ………………….

$832,800

Less ending inventory ………………..

Direct materials used ………………

(a)*

Other manufacturing costs ………….

Total manufacturing costs ……….

(c)

Total costs of work in process ……..

Less ending work in process ……

Cost of goods manufactured …

(b)

Beginning finished goods inventory …….

Finished goods available for sale ……….

Ending finished goods inventory ………..

2-41. (15 min.) Basic Concepts: Monroe Fabricators

a.

From the basic inventory equation,

Beginning Inventory + Transferred in

2-42. (15 min.) Basic Concepts: Talmidge Co.

a.

Purchases of direct materials = Ending direct materials

From the basic inventory equation,

Beginning work-in-process inventory + Total manufacturing

cost

= Cost of goods manufactured + Ending work-in-process

inventory, so

2-43. (15 min.) Prepare Statements for a Merchandising Company: Angie’s

Apparel.

Angie’s Apparel

Income Statement

For the Month Ended July 31

Sales revenue ……………………………………………………………………………..

$570,000

Cost of goods sold (see statement below) ……………………………………….

388,500

Gross margin ………………………………………………………………………………

For the Month Ended July 31

Merchandise inventory, July 1 ……………………………………….

Merchandise purchases ……………………………………………….

Total cost of goods purchased ………………………………………

Cost of goods available for sale …………………………………….

Merchandise inventory, July 31 ……………………………………..

2-44. (15 min.) Prepare Statements for a Merchandising Company: University

Electronics.

University Electronics

Income Statement

For the Year Ended February 28

Sales revenue ……………………………………………………………………………..

$4,000,000

Cost of goods sold (see statement below) ……………………………………….

2,830,000

Gross margin ………………………………………………………………………………

$1,170,000

1,295,000

For the Year Ended February 28

Merchandise inventory, March 1 ……………………………………

Merchandise purchases ……………………………………………….

Total cost of goods purchased ………………………………………

Cost of goods available for sale …………………………………….

Merchandise inventory, February 28 ………………………………

2-45. (10 min.) Cost Behavior for Forecasting: Dayton, Inc.

The variable costs will be 20 percent higher because there will be an increase of 36,000

– 30,000 = 6,000 units (20% = 6,000 ÷ 30,000).

Variable costs:

Direct materials used ($510,000 x 1.2) …………………………...

$ 612,000

Direct labor ($1,120,000 x 1.2)……………………………………….

1,344,000

Indirect materials and supplies ($120,000 x 1.2) ……………….

Power to run plant equipment ($140,000 x 1.2) ………………..

Total variable costs ………………………………………………………

Fixed costs:

Supervisory salaries ……………………………………………………..

Plant utilities (other than power to run plant equipment) …….

Depreciation on plant and equipment ……………………………..

Property taxes on building …………………………………………….

Total fixed costs …………………………………………………………..

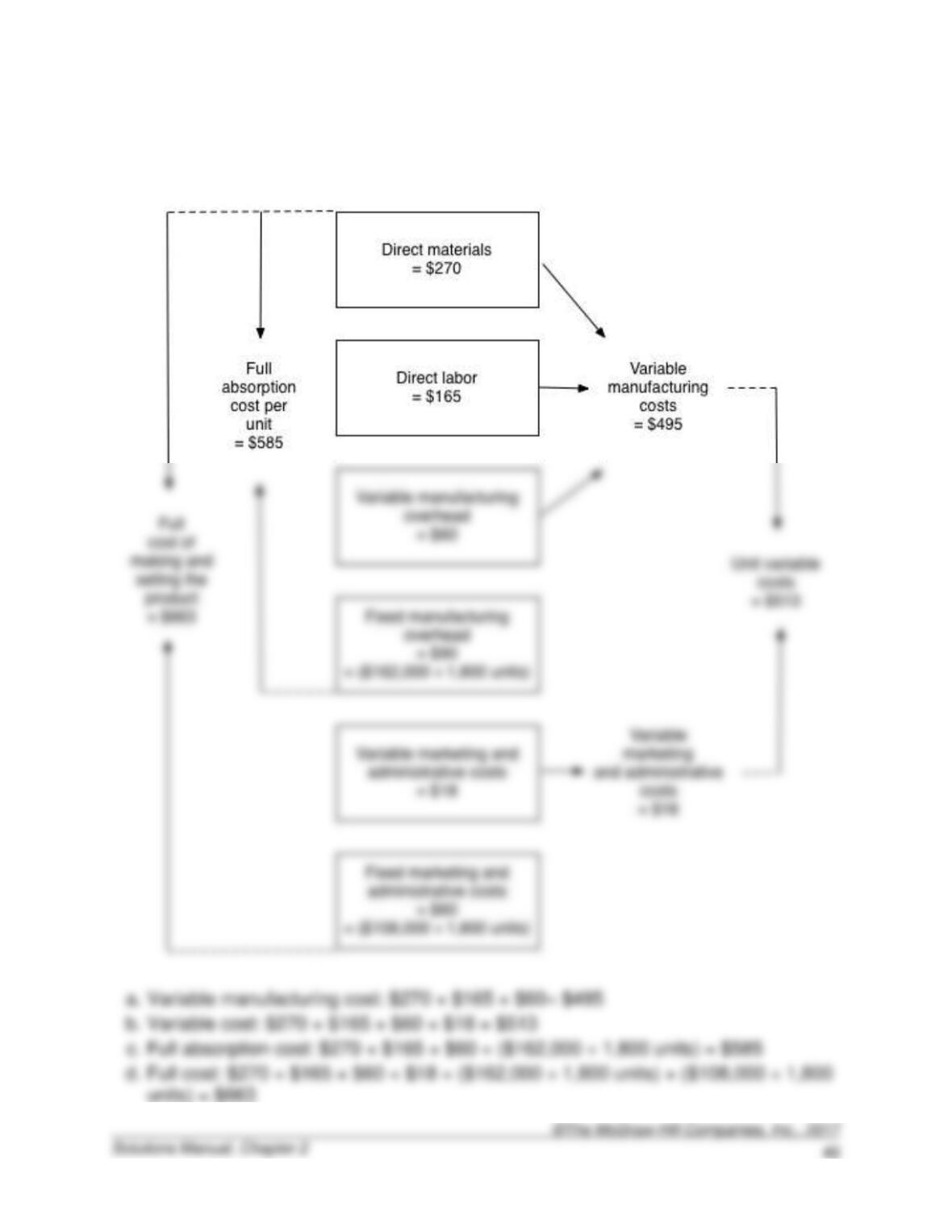

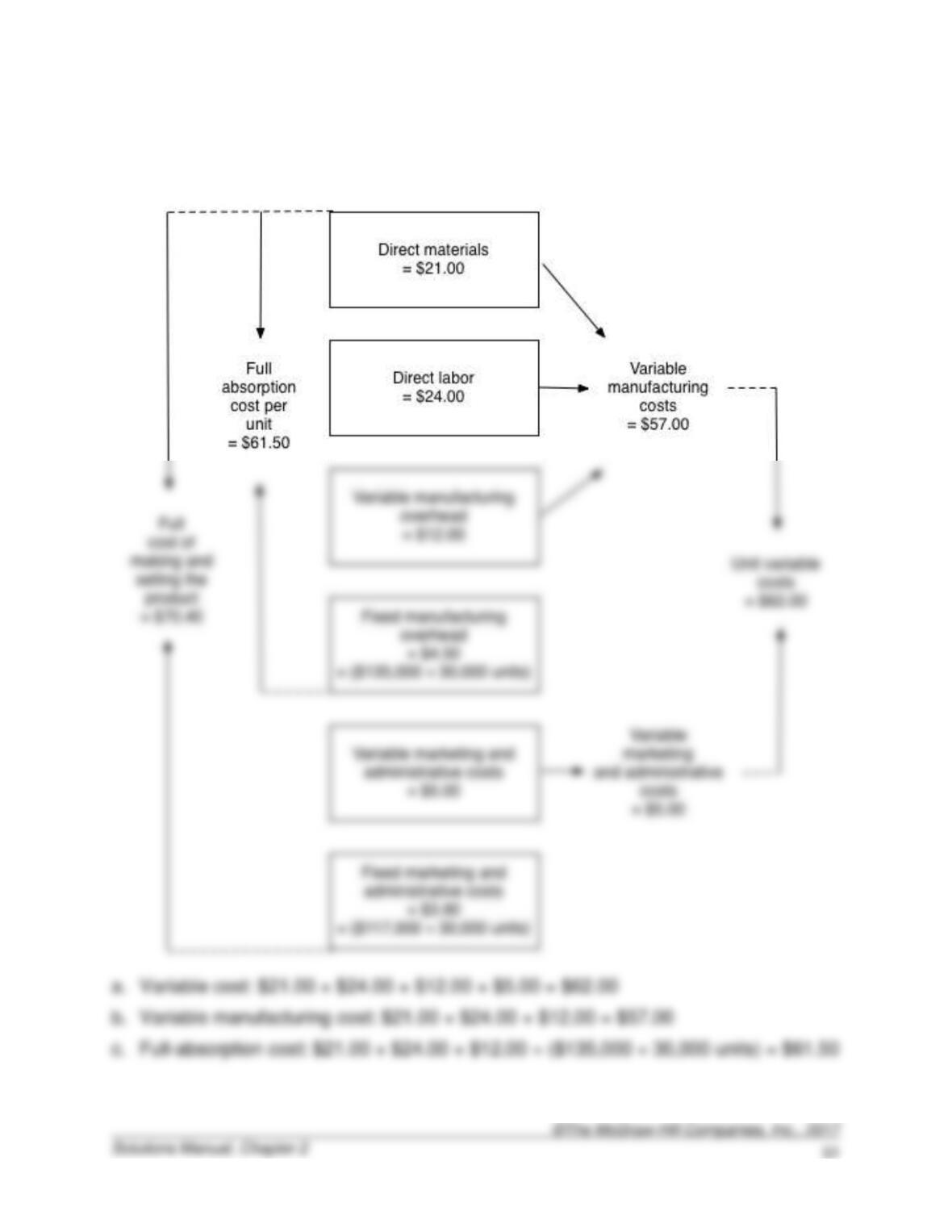

2-46. (30 min.) Components of Full Costs: Madrid Corporation

2-47. (15 min.) Components of Full Costs: Madrid Corporation.

2-48. (30 min.) Components of Full Cost: Larcker Manufacturing.

2-48. (continued)

2-49. (20 Min.) Gross Margin and Contribution Margin Income Statements:

Larcker Manufacturing.

Gross Margin Income Statement

Contribution Margin Income Statement

Sales revenue(a) ………….

………………………………….

$2,370,000

Sales revenue …………………

$2,370,000

Variable manufacturing

costs (b) ……………………..

1,710,000

Variable manufacturing

costs ……………………………..

1,710,000

………………………………….

Gross margin ……………….

Contribution margin ………….

Variable marketing and

administrative costs (c) ….

Fixed manufacturing

overhead costs ………………..

Fixed marketing and

administrative costs ………

Fixed marketing and

administrative costs …………

2-50. (20 Min.) Gross Margin and Contribution Margin Income Statements: Niles

Castings.

Gross Margin Income Statement

Contribution Margin Income Statement

Sales revenue …………….

$264,000

Sales revenue …………………

$264,000

Variable manufacturing

costsa …………………………

119,000

Variable manufacturing

costs ………………………………

119,000

Gross margin ……………….

Contribution margin ………….

$131,400

Variable marketing and

administrative costs ………

Fixed marketing and

administrative costs ………

Fixed marketing and

administrative costs ………….

2-51. (20 Min.) Gross Margin and Contribution Margin Income Statements: Alpine

Coffee Roasters.

Gross Margin Income Statement

Contribution Margin Income Statement

Sales revenuea ………………….

$230,400

Sales revenue ……………………

$230,400

Variable manufacturing

costsb ………………………………

126,000

Variable manufacturing

costs ………………………………..

126,000

administrative costs ……………

Gross margin …………………….

Contribution margin ……………

overhead costs ………………….

administrative costs ……………

2-52. (30 min.) Value Income Statement: Ralph’s Restaurant.

a.

Ralph’s Restaurant

Value Income Statement

For the year 2 ending December 31

Nonvalue-

added

activities

Value-

added

activities

Total

Sales revenue ………………………………….

$1,000,000

$1,000,000

Cost of merchandise …………………………

Cost of food serveda ……………………..

$ 52,500

297,500

350,000

Gross margin …………………………………..

$ (52,500)

$ 702,500

Operating expenses ………………………….

Employee salaries and wagesb ……….

212,500

250,000

Managers’ salariesc ……………………….

100,000

b. The information in the value income statement enables Ralph to identify nonvalue-

2-53. (30 min.) Value Income Statement: DeLuxe Limo Service.

a.

b. The information in the value income statement enables the managers at DeLuxe to

identify nonvalue-added activities. They could eliminate such activities without

Solutions to Problems

2-54. (30 min.) Cost Concepts: Chelsea, Inc.

a.

Prime costs = direct materials + direct labor

b.

e.

Cost of

Goods

=

Cost of

Goods

+

Beginning

Finished

–

Ending

Finished

2-55. (30 Minutes) Cost Concepts: Lawrence Components.

a. $58,000.

Prime costs

=

Direct materials used + Direct labor costs

Direct materials used

=

Prime costs – Direct labor costs

=

=

b. $12,000.

Direct materials used

=

Beginning inventory + purchases – ending inventory

beginning inventory

=

$12,000

c. $120,000.

costs

Conversion cost

=

Total manufacturing costs – Prime costs + Direct labor

cost

=

$178,000 – $98,000 + $40,000

=

$120,000

=

$6,000 + $178,000 – $180,000

=

$4,000

Conversion cost

=

Direct labor costs + Manufacturing overhead

Manufacturing overhead

=

Conversion costs – Direct labor costs

=

$120,000 – $40,000

=

$80,000

Total manufacturing

=

Prime costs + Conversion costs – Direct labor cost

2-55. (continued)

f. $10,000.

Cost of goods sold

=

Finished goods, beginning + Cost of goods

manufactured – Finished goods, ending

Finished goods,

beginning

=

Cost of goods sold – Cost of goods manufactured +

Finished goods, ending

$142,000 – $180,000 + $48,000

=

$10,000

2-56. (30 minutes) Cost Concepts: Columbia Products.

a. Amounts per unit:

(1) $217.

2-56. (continued)

b. As the number of units increases (reflected in the denominator), fixed manufacturing

2-57. (30 min.) Prepare Statements for a Manufacturing Company: Yolo

Windows.

Yolo Windows

Statement of Cost of Goods Sold

For the Year Ended December 31

($000)

Work in process, Jan. 1 ……………………………………

$ 48

Manufacturing costs:

Direct materials:

Beginning inventory, Jan. 1 ………………………..

$ 36

Add material purchases …………………………….

Direct materials available …………………………..

Less ending inventory, Dec. 31 …………………..

Direct materials used ………………………………..

Direct labor …………………………………………………

Manufacturing overhead:

Indirect factory labor …………………………………

Indirect materials and supplies ……………………

Factory supervision …………………………………..

Factory utilities …………………………………………

Factory and machine depreciation ………………

Property taxes on factory …………………………..

Total manufacturing overhead …………………

Total manufacturing costs ……………………

Total cost of work in process during the year ………

14,924

Less work in process, Dec. 31 ……………………….

Costs of goods manufactured during the year

Beginning finished goods, Jan. 1 ………………………

Finished goods inventory available for sale ………..

15,524

2-57. (continued)

Yolo Windows

Income Statement

For the Year Ended December 31

($000)

Sales revenue ………………………………………………………………….

$18,160

Less: Cost of goods sold …………………………………………………..

14,936

Administrative costs ………………………………………………………….

Marketing costs ………………………………………………………………..

2-58. (30 min.) Prepare Statements for a Manufacturing Company: Mesa

Designs.

Mesa Designs

Statement of Cost of Goods Sold

For the Year Ended December 31

($000)

Work in process, Jan. 1 ……………………………………

$ 152

Manufacturing costs:

Direct materials:

Beginning inventory, Jan. 1 ………………………..

$ 96

Add materials purchases …………………………..

10,300

Direct materials available …………………………..

$10,396

Less ending inventory, Dec. 31 …………………..

Direct materials used ………………………………..

Direct labor …………………………………………………

Manufacturing overhead:

Depreciation (factory) ………………………………..

$5,560

Depreciation (machines) …………………………...

Indirect labor (factory) ……………………………….

Indirect materials (factory)………………………….

Property taxes on factory …………………………..

Utilities (factory) …………………………..…………..

Total manufacturing overhead …………………

Total manufacturing costs ……………………

Total cost of work in process during the year ………

Less work in process, Dec. 31 ……………………….

Costs of goods manufactured during the year

$43,832

Beginning finished goods, Jan. 1 ………………………

Finished goods inventory available for sale ………..

2-58. (continued)

Mesa Designs

Income Statement

For the Year Ended December 31

($000)

Sales revenue ………………………………………………………………….

$60,220

Less: Cost of goods sold …………………………………………………..

Administrative costs ………………………………………………………….

Selling costs…………………………………………………………………….

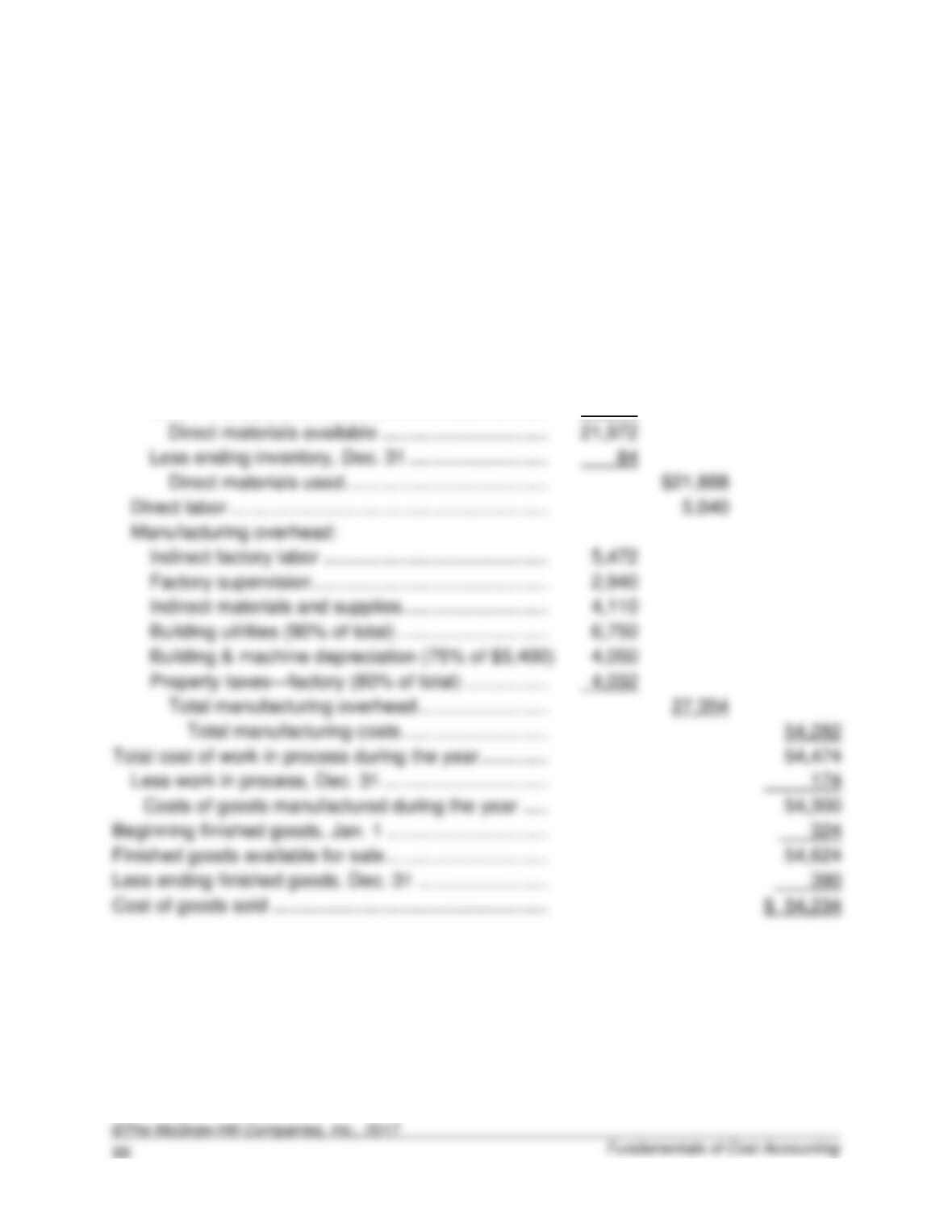

2-59. (30 min.) Prepare Statements for a Manufacturing Company: Billings Tool

& Die.

.

Billings Tool & Die

Statement of Cost of Goods Sold

For the Year Ended December 31

($ 000)

Beginning work in process, Jan. 1…………………………

$ 192

Manufacturing costs:

Direct materials:

Beginning inventory, Jan. 1 …………………………...

$ 72

Add: Purchases ……………………………………………

21,900

Direct materials available …………………………..

Less ending inventory, Dec. 31 ………………………

Direct materials used …………………………………

Direct labor …………………………………………………….

Manufacturing overhead:

Indirect factory labor …………………………………….

Factory supervision ………………………………………

Indirect materials and supplies ……………………….

Building utilities (90% of total) ………………………..

Building & machine depreciation (75% of $5,400)

Property taxes—factory (80% of total) …………….

Total manufacturing overhead …………………….

27,354

Total manufacturing costs ……………………….

Total cost of work in process during the year ………….

Less work in process, Dec. 31 …………………………..

Beginning finished goods, Jan. 1 ………………………….

Finished goods available for sale ………………………….

Less ending finished goods, Dec. 31 …………………….

2-59. (continued)

Billings Tool & Die

Income Statement

For the Year Ended December 31

($ 000)

Sales revenue ……………………………………………………..

$77,820

Less: Cost of goods sold (per statement) …………………

54,234

Gross profit …………………………..…………………………….

$ 23,586

Marketing and administrative costs:

17,934

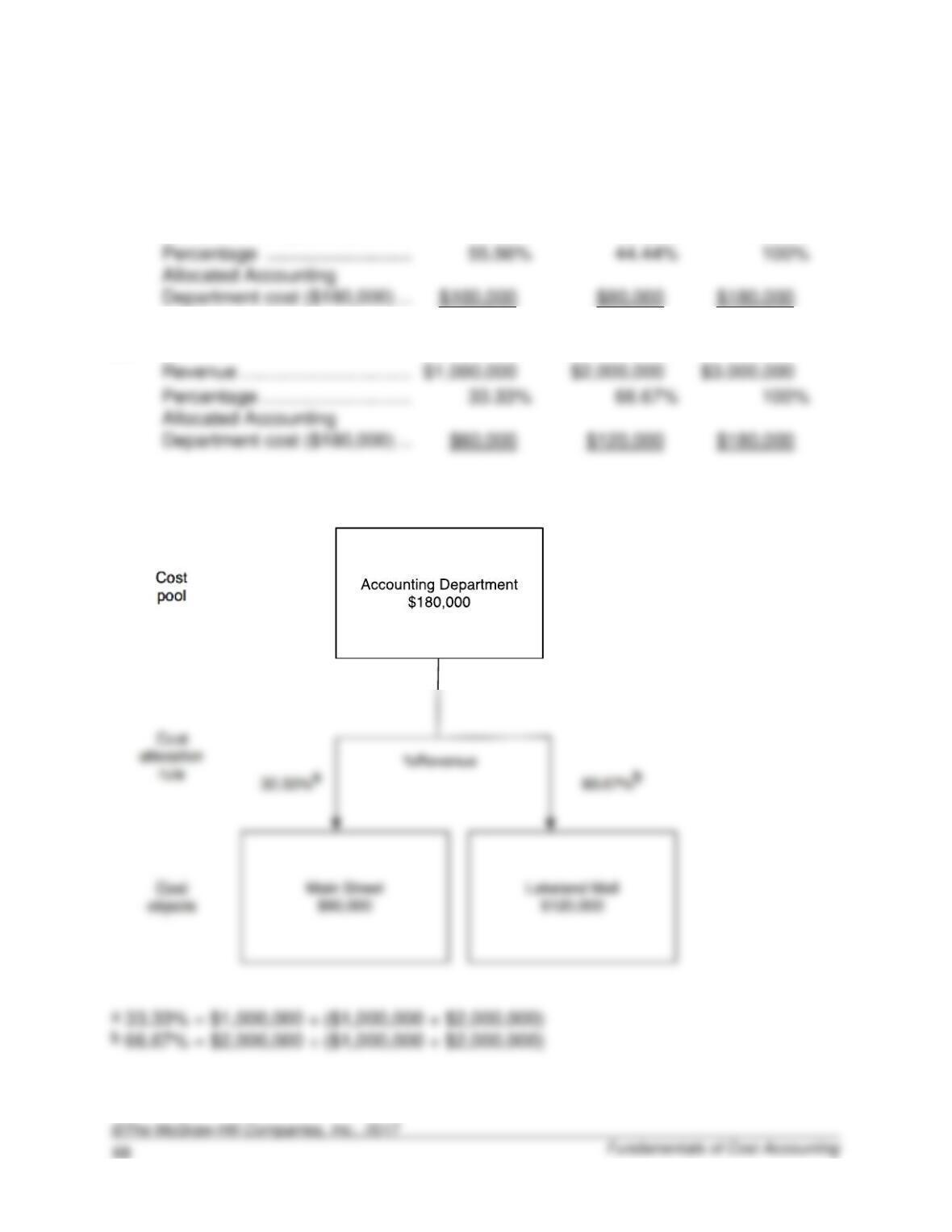

2-60. (10 Min.) Cost Allocation with Cost Flow Diagram: Coastal Computer.

a.

(1)

Main Street

Lakeland Mall

Total

Number of computers sold ……..

2,000

1,600

3,600

Percentage …………………………

Department cost ($180,000) …..

(2)

Main Street

Lakeland Mall

Total

Revenue ……………………………..

$3,000,000

Percentage ………………………….

b.

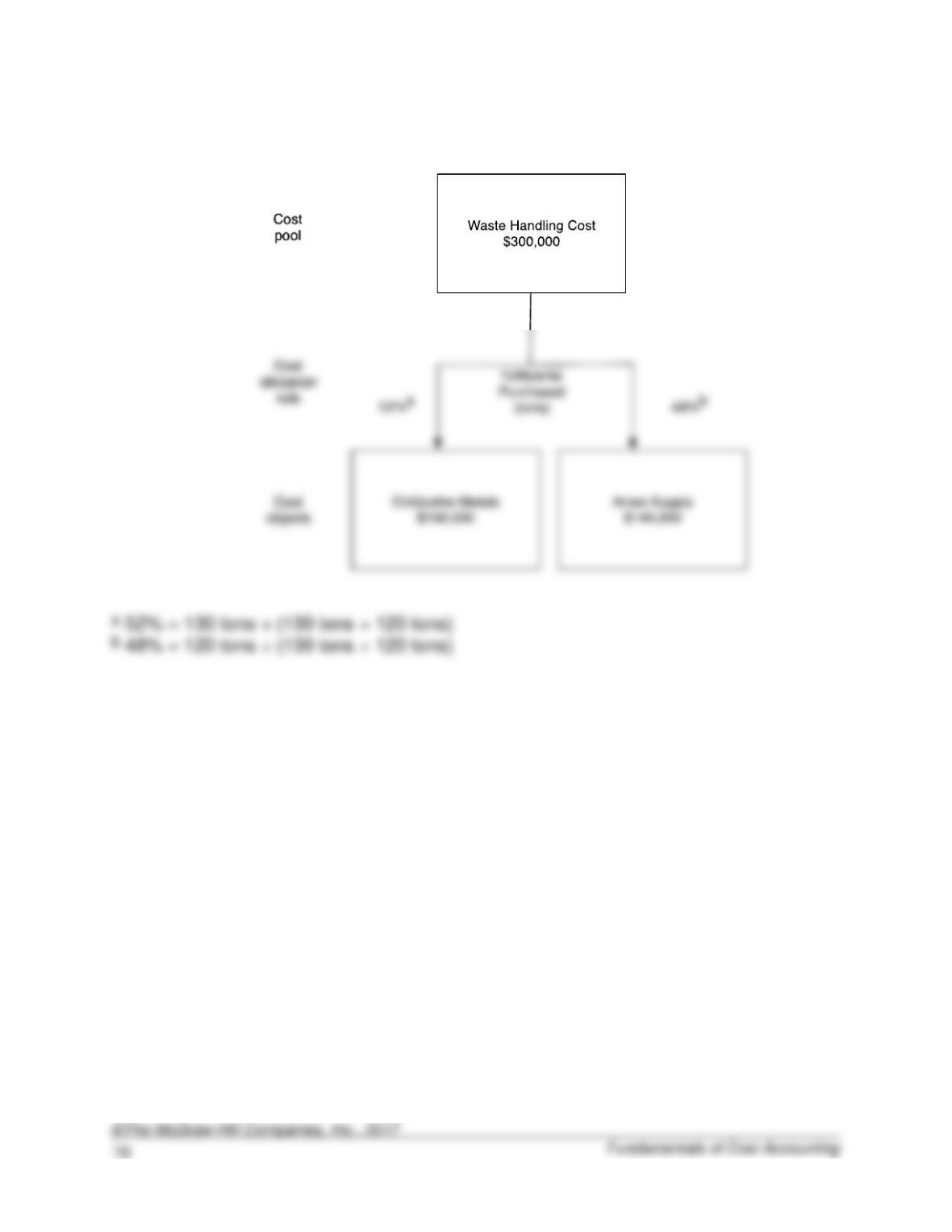

2-61. (20 Min.) Cost Allocation with Cost Flow Diagram: Wayne Casting, Inc.

a.

(1)

Chillicothe

Metals

Ames

Supply

Total

Material purchased (tons) ………

130

120

250

Percentage …………………………

Allocated waste handling

cost ($300,000) …………………….

$144,000

Metals

Supply

Total

Amount of waste (tons) ………….

Allocated waste handling

cost ($300,000) …………………….

(3)

Chillicothe

Metals

Ames

Supply

Total

2-61. (continued)

b.

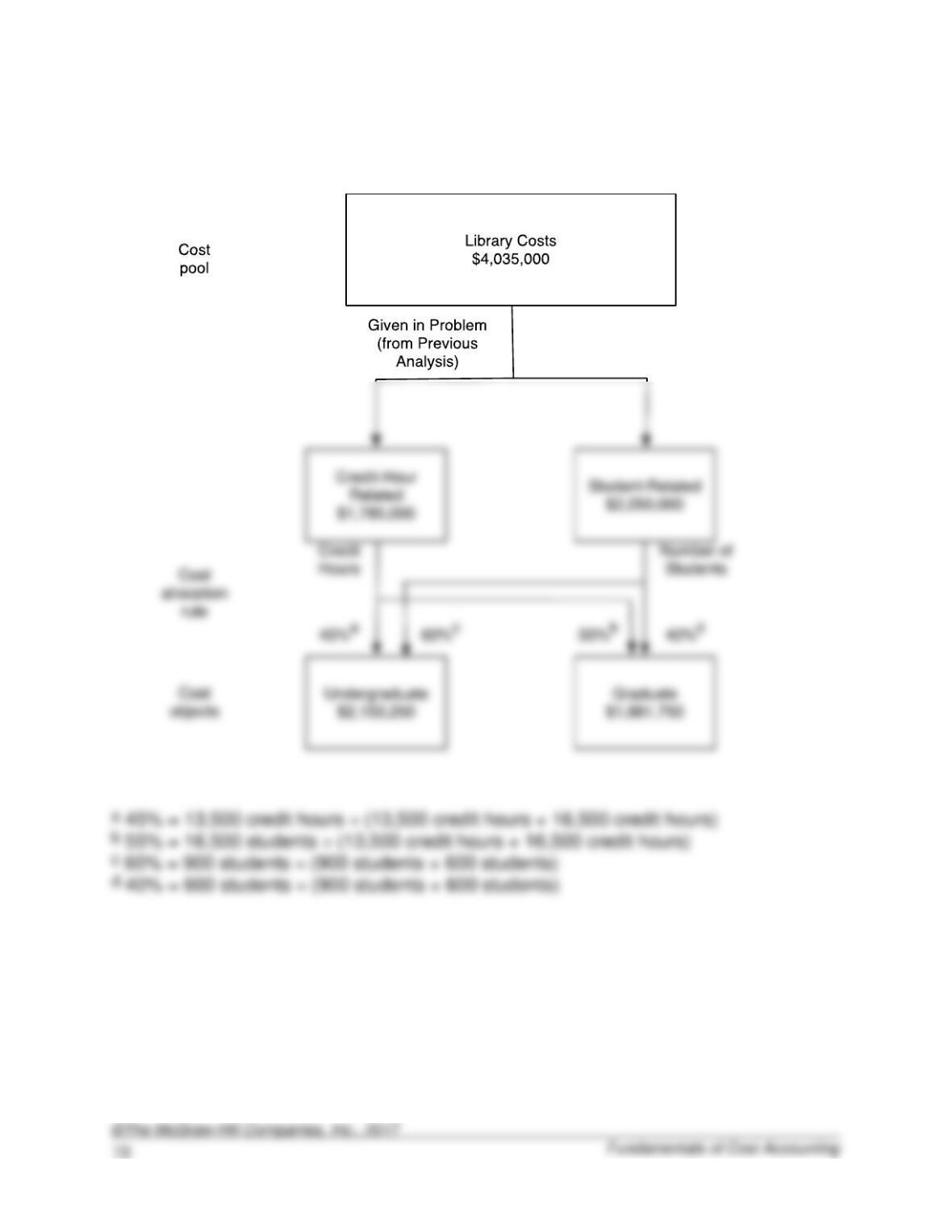

2-62. (20 Min.) Cost Allocation with Cost Flow Diagram: Pacific Business School.

a.

Undergraduate

Graduate

Total

Number of students ………………….

900

600

1,500

Credit Hours …………………………...

2-62. (continued)

b.

2-63. (40 Min.) Find the Unknown Information.

a.

Finished goods

beginning inventory

+

Cost of goods

manufactured

–

Cost of

goods sold

=

Finished goods

ending inventory

Finished goods

beginning inventory

Finished goods

beginning inventory

b.

Direct

materials

used

+

Direct

labor

+

Manufacturing

overhead

=

Total

manufacturing

costs

used

+

+

used

=

c.

Gross margin %

=

Gross margin

÷

Sales revenue

=

(Sales revenue – COGS)

÷

Sales revenue

Rearranging,

Sales revenue

=

(1.0 – Gross Margin %)

2-64. (40 Min.) Find the Unknown Information.

a.

Cost of

goods sold

=

Finished goods

beginning inventory

+

Cost of goods

manufactured

–

Finished goods

ending inventory

=

+

Cost of

goods sold

b.

Total

manufacturing

costs

=

Direct

materials

used

+

Direct

labor

+

Manufacturing

overhead

materials

+

=

$116,920

c.

Direct

materials

used

=

Beginning

inventory

+

Materials

purchased

–

Ending

inventory

$116,920

Materials

$2,088

Materials

d.

Gross margin %

=

Gross margin

÷

Sales revenue

38%

=

(Sales revenue –

Cost of goods sold)

÷

Sales revenue

Sales revenue

Cost of goods sold

Cost of goods sold

=

x

(1 – 38%)

Sales revenue

$595,200 (from a)

2-65. (40 min.) Cost Allocation and Regulated Prices: The City of Imperial Falls.

a. The rate is 20 percent above the average cost of collection:

Total cost of collection

=

$400,000 + $1,280,000 + $320,000

=

$2,000,000

=

16,000 tons

=

=

$.0625 per pound

b.

First, allocate costs to the two cost objects: households and businesses:

Allocation of administrative costs and truck costs:

Total costs

=

$400,000 + $1,280,000

=

=

15,000 customers

customers

=

4,000 + 12,000

=

16,000 tons

=

2-65. (continued)

Allocation to customer types:

Households

Business

Allocation of customer cost:

Allocated cost per customer …………….

$112

$112

Number of customers ……………………..

Allocated cost ………………………………..

Allocation of other costs:

Allocated cost per ton ……………………..

Number of tons ………………………………

Allocated cost ………………………………..

Total allocated cost …………………………

Total number of tons ……………………….

Number of pounds ………………………….

Average allocated cost per pound …….

c. Answers will vary. This problem illustrates that cost allocation can have an important

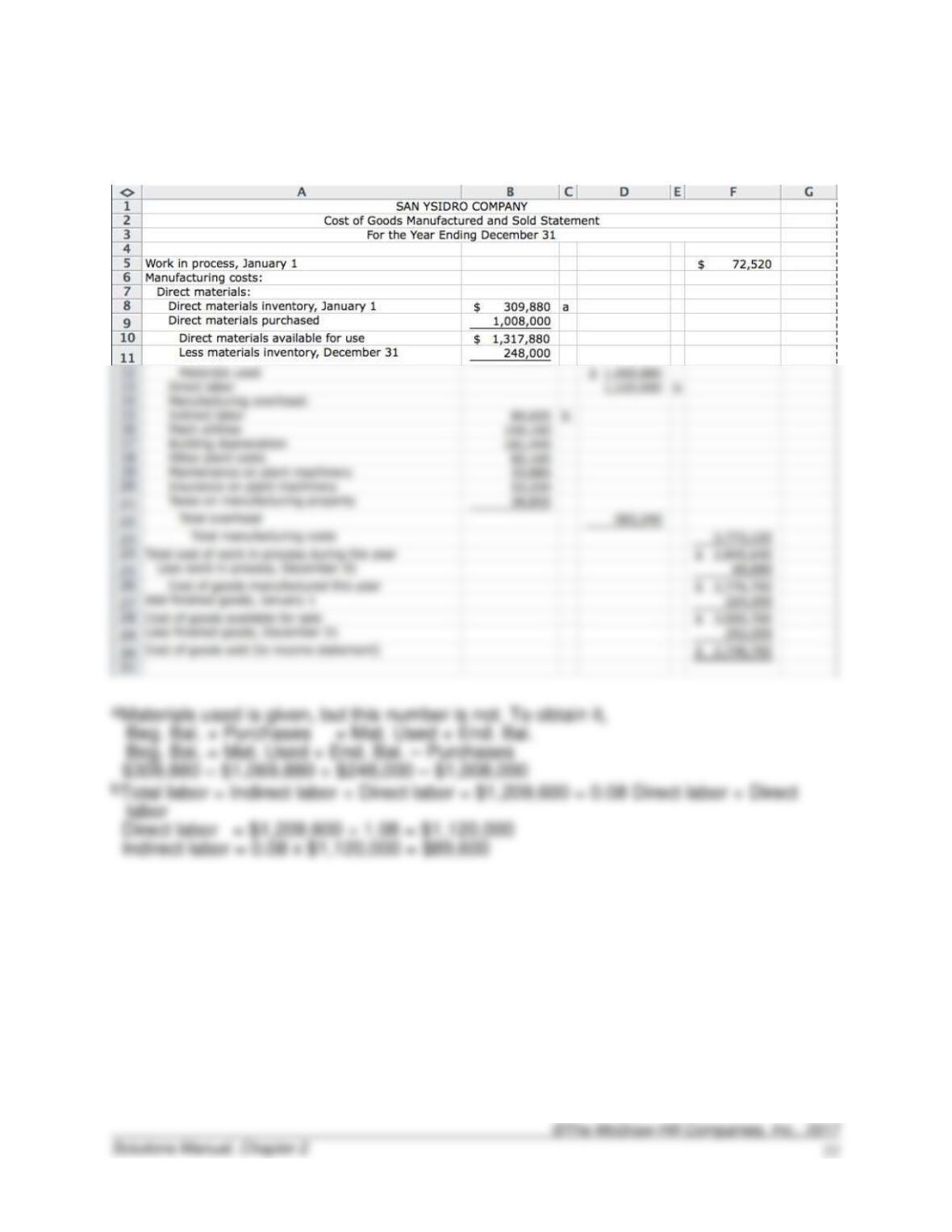

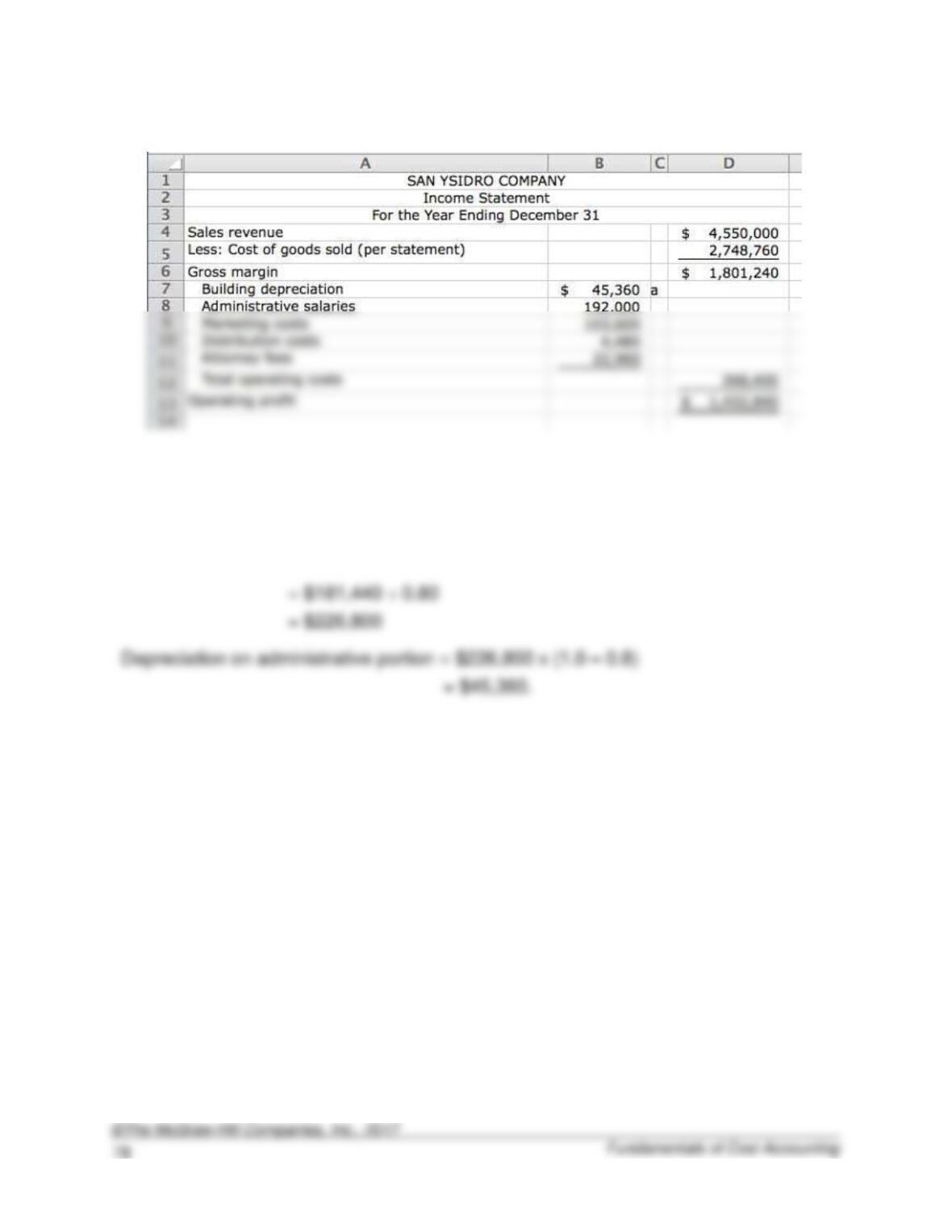

2-66. (30 min.) Reconstruct Financial Statements: San Ysidro Company.

2-66 (continued)

a Total depreciation = Depreciation on plant + Depreciation on administrative building

portion

Depreciation on plant is 80% of the total depreciation, so total depreciation is,

2-67. (20 Min.) Finding Unknowns: Mary’s Mugs.

a. $2,812.50.

Direct materials cost per unit = Direct materials cost ÷ Units produced

2-68. (40 Min.) Finding Unknowns: BS&T Partners.

Note: This problem is challenging, because there is no indication of how to begin or the

order in which to solve for the unknowns.

We begin by computing the following unit costs:

Manufacturing cost per unit = Direct materials + Direct labor + Manufacturing overhead

Full cost per unit = Manufacturing cost per unit + Selling, general & administrative

= $27.00 + $12.00 = $39.00

2-68 (continued)

c. Full costs = Cost of goods sold + Selling, general, and administrative costs

Then,

Operating profit = Sales revenue – Cost of goods sold – Selling, general, and

d. Sales revenue = Selling price per unit x Units sold

e. Finished goods ending (units) = Finished goods beginning (units) + Units produced

– Units sold

Solutions to Integrative Case

2-69. (30 min.) Analyze the Impact of a Decision on Income Statements:

Tunes2Go.

a. This year’s income statement:

Baseline

(Status Quo)

Rent

Equipment

Difference

Sales revenue …………………………..

$4,800,000

$4,800,000

0

Operating costs:

Fixed (cash expenditures) ……….

(2,250,000)

Equipment depreciation …………..

Other depreciation ………………….

Loss from equipment write-off ….

lower

b. Next year’s income statement:

Baseline

(Status Quo)

Rent

Equipment

Difference

Sales revenue …………………………..

$4,800,000

$5,136,000

a

$336,000

higher

Operating costs:

Equipment rental ……………………

0

(690,000)

690,000

higher

Variable ………………………………..

(600,000)

(600,000)

0

Fixed cash expenditures ………….

(2,250,000)

135,000

lower

Equipment depreciation …………..

450,000

lower

Other depreciation ………………….

0