2-1

Chapter 2

Cost Concepts and Behavior

Learning Objectives

1. Explain the basic concept of “cost.”

2. Explain how costs are presented in financial statements.

3. Explain the process of cost allocation.

4. Understand how material, labor, and overhead costs are added to a product at each stage of

the production process.

5. Define basic cost behaviors, including fixed, variable, semivariable, and step costs.

6. Identify the components of a product’s costs.

2-2

Chapter Overview

I. WHAT IS A COST?

• Cost versus Expenses

II. PRESENTATION OF COSTS IN FINANCIAL STATEMENTS

• Service Organizations

• Retail and Wholesale Companies

• Manufacturing Companies

• Direct and Indirect Manufacturing (Product) Costs

III. COST ALLOCATION

• Direct versus Indirect Costs

IV. DETAILS OF MANUFACTURING COST FLOWS

V. HOW COSTS FLOW THROUGH THE STATEMENTS

• Income Statements

• Cost of Goods Manufactured and Sold Statement

VI. COST BEHAVIOR

• Fixed Versus Variable Costs

VII. COMPONENTS OF PRODUCT COSTS

• Unit Fixed Costs Can Be Misleading for Decision Making

VII. HOW TO MAKE COST INFORMATION MORE USEFUL FOR MANAGERS

• Gross Margin versus Contribution Margin Income Statements

2-3

Chapter Outline

LO 2-1 Explain the basic concept of “cost.”

WHAT IS A COST?

• Cost versus Expenses

o The cost accounting system records and maintains the use of economic resources by the

organization.

▪ The financial statements prepared by the firm for external reporting use information

from the cost accounting system.

▪ Cost accounting systems also provide information to help managers make better

decisions. Managers need to understand the common terms used in cost accounting.

o Cost represents a sacrifice of resources (typically cash or a line of credit). The price of

each item purchased measures the sacrifice made to acquire it.

▪ Expense is a cost charged against (i.e., deducted from) revenue in an accounting

period.

▪ Cost initially recorded as an asset becomes an expense when the asset has been

consumed (e.g., the prepaid rent becomes rent expense after the office space has been

▪ Cost accounting focuses on costs; expenses are referred to only in the context of

external financial reporting (in this text).

o The two major categories of costs are:

▪ Outlay cost: a past, present, or future cash outflow, such as tuition, books, and fees

paid for a college education, and

▪ Opportunity cost: the forgone benefit that could have been realized from the best

forgone alternative course of a resource, such as the time and income sacrificed to get

a college education.

See Demonstration Problem 1

2-4

• Managers tend to overlook or ignore opportunity costs while making decisions

because:

No one can ever know all possible opportunities available at any moment.

LO 2-2 Explain how costs are presented in financial statements.

PRESENTATION OF COSTS IN FINANCIAL STATEMENTS

• Operating profit is the excess of operating revenues over the operating costs incurred to

generate those revenues.

o Operating profit differs from net income.

o Net income is operating profit adjusted for interest, income taxes, extraordinary items,

and other adjustments required to comply with GAAP or other regulations.

o Information generated by the cost accounting system is used to help managers make

decisions that improve firm value. It is a means to an end.

▪ Such information is best (in terms of relevancy) for various decisions but not

necessarily most accurate.

▪ How the cost information is used in decision making and the costs of preparing and

using such information should also be considered.

o A generic income statement for a firm, a division, a product, or any unit has the following

format:

Income statement

Revenue

xxx

Costs

Operating profit

xxx

2-5

• Service Organizations

o Service organizations provide customers an intangible product, such as advice and

analyses. Labor costs and/or costs of information technology represent the most

significant cost category for service organizations.

o Exhibit 2.2 illustrates the income statement of a typical service company. Cost of services

sold includes costs of billable hours, which are the hours billed to clients plus the cost of

• Retail and Wholesale Companies

o Retail and wholesale companies sell but do not make a tangible product, such as food,

clothes, or a book.

o Exhibit 2.3 illustrates an income statement for a merchandising company. Cost of goods

sold keeps track of the tangible goods the company buys and sells.

o A typical income statement for a merchandising company has the following format:

Income Statement

Sales revenue

xxx

Cost of goods sold

(xx)

Gross margin

xxx

Marketing and administrative costs

(xx)

Operating profit

xxx

o The cost of goods sold statement shows how the cost of goods sold was computed. The

typical format follows:

Cost of Goods Sold Statement

Beginning inventory

xxx

Cost of goods purchased

Transportation-in costs

xxx

Total costs of goods purchased

xxx

Cost of goods available for sale

xxx

Less cost of goods in ending inventory

Cost of goods sold

xxx

2-6

▪ The gross margin reflects the amount available to cover marketing and administrative

costs and earn a profit.

• Manufacturing Companies

o Manufacturing companies make the goods for sale and need to know the different costs

associated with making them.

• Direct and Indirect Manufacturing (Product) Costs

o Product costs are those costs assigned to units of production and recognized (i.e.,

expensed) when the product is sold. Product costs follow the product through inventory.

▪ Direct manufacturing costs are product costs that can be identified with units (or

batches of units) at relatively low cost, including:

• Prime Costs and Conversion Costs

o Prime costs = Direct materials + Direct labor.

▪ Companies with relatively low manufacturing overhead tend to focus on managing

prime costs.

• Indirect manufacturing costs are all product costs other than direct

manufacturing costs, often referred to in total as manufacturing overhead.

• Manufacturing overhead represents all other costs of transforming the materials

into a finished product, including:

2-7

Indirect materials (materials not a part of the finished product but are necessary

to manufacture it, such as lubricants, polishing and cleaning materials, etc.)

o Conversion costs = Direct labor + Manufacturing overhead.

▪ Conversion costs are the costs that convert direct materials into the final product.

Companies with high direct labor and/or manufacturing overhead tend to emphasize

more about conversion costs.

• Nonmanufacturing (Period) Costs

o Period costs (nonmanufacturing costs are all other costs recognized for financial

reporting when incurred, including marketing and administrative costs.

▪ Marketing costs are the costs required to obtain customer orders and provide

customers with finished products, including advertising, sales commissions, and

shipping costs.

▪ Administrative costs are the costs required to manage the organization and provide

staff support, including executive and clerical salaries, costs for legal, financial, data

processing, accounting services, and building space for administrative personnel.

• The distinction between manufacturing and nonmanufacturing costs is not always clear-cut.

Companies usually set their own guidelines and follow them consistently.

o Service companies often have costs that are mostly indirect. Managing indirect costs is

extremely important in these firms if they are to remain profitable. (See Business

Application box “Indirect Costs in Banking.”)

o Most firms are made up of activities that combine features of all three types of activities

(service, retailing, and manufacturing).

2-8

LO 2-3 Explain the process of cost allocation.

COST ALLOCATION

• Direct versus Indirect Costs

o Cost allocation is the process of assigning indirect costs to product, services, people,

business units, etc. Cost allocation is necessary when several departments share facilities

or services.

▪ Cost object is any end to which a cost is assigned. Examples include a unit of product

or service, a department, or a customer.

o Cost flow diagram is a diagram or flowchart illustrating the cost allocation process.

▪ Fundamental approach to cost allocation:

• Identify the cost objects

• Determine the cost pools

• Select a cost allocation rule

▪ Cost flow diagrams help managers understand

• How a cost system works

See Demonstration Problem 2

2-9

• Direct cost is any cost that can be directly (unambiguously) related to a cost object at

reasonable cost; indirect cost is any cost that cannot be directly related to a cost object.

LO 2-4 Understand how material, labor, and overhead costs are added to a

product at each stage of the production process.

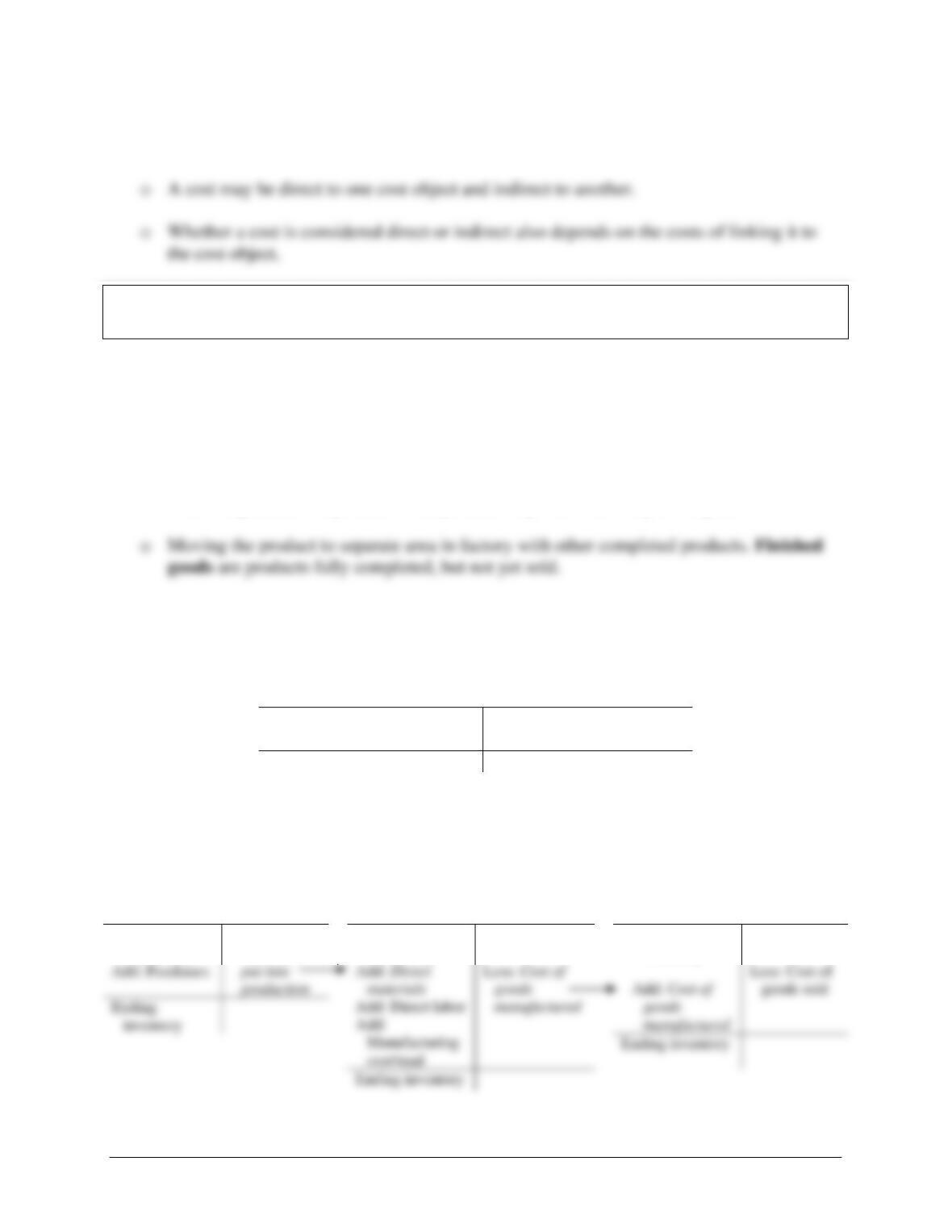

• Any production process involves three basic steps:

o Delivering direct materials to receiving area, inspecting, and then placing in direct

material inventory area (store).

o Transporting direct materials to an assembly line and undergoing the production process.

Work in process is a product in the production process but not yet complete.

• For manufacturing companies, there are three inventory accounts in a cost accounting system.

Each inventory account is likely to have the following structure (in T-account):

Inventory Account

(Direct materials, Work-in-process, or Finished goods)

Beginning inventory

Debit: Additions

Credit: Withdrawals

Ending inventory

o Inventoriable costs are costs added (debited) to inventory accounts.

• The cost flows coincide with the physical flows of goods in and out of their respective storage

areas.

Direct materials inventory

Work-in-process inventory

Finished goods inventory

Beginning

inventory

Ending

Less: Direct

materials

Beginning

inventory

Beginning

inventory

2-10

o The inventory account balances at the end of an accounting period appear on the balance

sheet as part of the current assets.

HOW COSTS FLOW THROUGH THE STATEMENTS

• Income Statements – Exhibit 2.7 illustrates an income statement for a manufacturing firm.

• Cost of Goods Manufactured and Sold Statement – Exhibit 2.8 illustrates a cost of goods

manufactured and sold statement for a manufacturing company.

o A typical cost of goods sold statement for a manufacturing company is more complicated

than that of a merchandising firm and has the following structure:

Cost of Goods Manufactured and Sold Statement

Beginning work-in-process inventory

xx

Manufacturing costs during the year:

Direct materials

Beginning inventory

xx

Add: Purchase of direct materials

xx

Direct materials available

xx

Less ending inventory

(xx)

Direct material put into production

xx

Direct labor

xx

Manufacturing overhead

xx

Total manufacturing costs incurred

xx

Total work in process during the year

xx

Less ending work-in-process inventory

(xx)

Cost of goods manufactured

xx

Beginning finished goods inventory

xx

Finished goods available for sale

xx

Less ending finished goods inventory

(xx)

Cost of goods sold

xx

▪ The three shaded areas deal with direct materials, work-in-process, and

finished goods, respectively.

o The cost of goods manufactured and sold statement is prepared through the internal

reporting system and is for managerial use only.

2-11

o Total manufacturing costs incurred equals the sum of direct material put into production,

direct labor, and manufacturing overhead incurred during the period. Managers in

production and operations give careful attention to these costs.

o The total cost of work in process during the year (i.e., the sum of the beginning work-in–

process inventory and total manufacturing costs incurred) is a measure of the resources

that have gone into production.

o Cost of goods manufactured represents the cost of goods that were finished during the.

Production departments usually have a goal for goods completed each period. Managers

See Demonstration Problem 3

LO 2-5 Define basic cost behaviors, including fixed, variable, semivariable,

and step costs.

COST BEHAVIOR

• Fixed Versus Variable Costs

o Cost behavior deals with the way costs respond to changes in activity levels; a cost driver

is a factor that causes, or “drives,” costs.

o Fixed costs are costs that are unchanged as volume changes within the relevant range of

activity. Examples: much of manufacturing overhead, many nonmanufacturing costs.

2-12

o Variable costs are costs that change in direct proportion with a change in volume within

the relevant range of activity. Examples: for manufacturing companies, direct materials,

and certain manufacturing overhead, direct labor in some cases; for merchandising

businesses, cost of the product, some marketing and administrative costs; for service

organizations, certain types of labor, supplies, copying, and printing costs.

The following graph shows a variable cost relationship between activity (units of

production) and the resulting cost of direct materials used.

o Relevant range refers to the activity levels within which a given total fixed costs or unit

variable cost will be unchanged.

o A semivariable cost is a cost that has both fixed and variable components; also called

mixed cost. Examples: electric utility costs, phone charges.

Cost of Direct Materials

$4,500

Units

1,000

1,500

$3,000

2-13

o Four aspects of cost behavior complicate the task of classifying costs into fixed or

variable categories.

▪ Not all costs are strictly fixed or variable.

LO 2-6 Identify the components of a product’s costs.

COMPONENTS OF PRODUCT COSTS

• Some cost concepts are determined by the rules of financial accounting. Some are more useful

for managerial decision making.

o Full cost is the sum of all fixed and variable costs of manufacturing and selling a unit of

product.

o Full absorption cost is the sum of all variable and fixed manufacturing costs. Full

absorption cost is used to compute a product’s inventory value under GAAP; as such, it

excludes nonmanufacturing costs.

o Exhibit 2.11 illustrates the product cost components for a company.

o On a per-unit basis:

▪ Full absorption cost = Direct materials + Direct labor + Variable manufacturing

overhead + Fixed manufacturing overhead.

2-14

Full absorption cost

o The diagram below demonstrates the relationship among various product cost

components.

Direct materials

Direct labor

• Unit Fixed Costs Can Be Misleading for Decision Making

o Unit fixed costs are valid only at one volume.

o When fixed costs are allocated to each unit, accounting records often make the costs

appear as though they are variable.

o It is easy to interpret unit costs incorrectly and make incorrect decisions.

See Demonstration Problem 4

• Gross margin as reported in the external financial statements is the difference between

revenue and cost of goods sold, or

o Gross margin = Revenue – Cost of goods sold.

Variable manufacturing cost

Variable manufacturing overhead

Fixed manufacturing overhead

Variable marketing and administrative costs

Fixed marketing and administrative costs

2-15

• Contribution margin per unit = Sales price – Variable costs per unit. Contribution margin

is the amount available to cover fixed costs and earn a profit.

o The income statement format that emphasizes contribution margin is referred to as the

contribution margin income statement.

Traditional

Income Statement

Components

Contribution margin

Income Statement

Sales price

Sales price

Less: Full absorption cost

+ Fixed manufacturing costs

Less: Variable cost

Gross margin

Contribution margin

+ Fixed marketing and

Less: Fixed costs

= Variable manufacturing cost

LO 2-7 Understand the distinction between financial and contribution

margin income statements.

HOW TO MAKE COST INFORMATION MORE USEFUL FOR MANAGERS

• Period costs can be determined once product costs are properly defined. Three approaches to

determining product costs are available.

2-16

See Demonstration Problem 5

• Gross Margin versus Contribution Margin Income Statements

o A comparison of the first two income statement formats is shown below.

Gross Margin

Income Statement

Contribution Margin

Income Statement

Sales revenue

Sales revenue

Less: Cost of goods sold

(including variable manufacturing costs

and fixed manufacturing costs)

Less: Variable costs

(including variable manufacturing and

variable marketing and administrative

See Demonstration Problem 6

• Developing Financial Statements for Decision Making

o The cost accounting system is designed to provide managers with relevant information

for decision making. Financial statements may be developed to serve special purposes.

Gross margin

Contribution margin

administrative costs and fixed marketing

marketing and administrative costs)

Operating profit

Operating profit

2-17

o Depending on the business and strategic environment of the firm, it is possible to

construct financial statements around activities related to quality, environmental

compliance, or new product development.

SUMMARY

• Exhibit 2.16 provides a summary of cost terms and definitions.

Matching

A.

Administrative costs

G.

Full absorption cost

B.

Conversion costs

H.

Indirect cost

C.

Cost allocation

I.

Opportunity cost

D.

Cost object

J.

Prime costs

E.

Cost pool

K.

Semivariable cost

F.

Direct cost

L.

Work in process

_____ 1. The foregone benefit from the best (forgone) alternative course of action.

_____ 2. Sum of direct labor and manufacturing overhead.

_____ 3. All variable and fixed manufacturing costs; used to compute a product’s inventory

value under GAAP.

_____ 4. The process of assigning indirect costs to products, services, people, business units,

etc.

_____ 5. Any cost that cannot be directly related to a cost object.

_____ 6. Any end to which a cost is assigned.

_____ 7. Costs required to manage the organization and provide staff support.

_____ 8. Sum of direct materials and direct labor.

_____ 9. Collection of costs to be assigned to the cost objects.

_____ 10. A cost that has both fixed and variable components.

_____ 11. A product in the production process but not yet complete.

_____ 12. Any cost that can be directly (unambiguously) related to a cost object at reasonable

cost.

2-19

Matching Answers

1. I

Multiple Choice Questions

1. Which of the following statements about costs and expenses is correct?

a. A cost is a sacrifice of resources.

b. Cost and expense are the same.

c. All assets will become expenses.

d. There is no guidance as to when costs are to be treated as expenses.

2. A cost of goods sold statement for a retail business:

a. Includes transportation-in costs.

b. Has a cost of goods manufactured section.

c. Covers a period of time.

d. Both a and c.

3. A period cost:

a. Is also known as manufacturing cost.

b. Includes both marketing and administrative costs.

c. Will be expensed when products are sold.

d. Is part of cost of goods sold.

Use the following information to answer questions 4 through 7:

A product is sold for $75 each with unit cost of direct materials $20, direct labor $15, variable

manufacturing overhead $12, and fixed manufacturing overhead $10. The volume produced and

sold is 6,000 units. Variable and fixed marketing and administrative costs are $4 and $3,

respectively.

4. Which of the following statements is correct?

a. Prime cost is $35.

b. Conversion cost is $37.

c. Inventoriable cost is $57.

d. All of the above.

5. What is the amount of cost of goods sold?

a. $342,000

b. $201,500

c. $364,000

d. None of the above.

6. Which of the following statements is correct?

a. Operating profit is $66,000.

b. Gross margin is $108,000.

c. Contribution margin is $144,000.

d. All of the above.

2-21

7. What is the full absorption cost per unit?

a. The same as full cost.

b. The same as inventoriable cost.

c. The full absorption cost per unit is $55.

d. The sum of variable manufacturing cost and variable marketing and administrative cost.

8. Which of the following statements regarding cost behavior within the relevant range is

incorrect?

a. Total fixed cost remains the same.

b. Fixed cost per unit remains constant.

c. Variable cost per unit remains constant.

d. Semivariable cost is also called mixed cost.

9. Unit fixed cost:

a. Is treated as variable cost when allocated to each unit.

b. Can be used for decision making under any circumstances.

c. Is misleading as the total fixed cost does not change.

d. Both a and c.

10. A value income statement:

a. Is developed for managerial decision making.

b. Distinguishes between value-added and nonvalue-added activities.

c. Is governed by GAAP.

d. Both a and b.

11. Which of the following statements is correct?

a. A cost object is any end to which a cost is assigned.

b. A cost pool is the collection of costs to be assigned to the cost objects.

c. A cost flow diagram is a diagram illustrating the cost allocation process.

d. All of the above.

12. The annual operating expense of running a copy center is shared by the three departments

that use its service: Human resource, Accounting, and Legal. Last year, the copy center

incurred $30,000 while HR copied 20,000 pages, Accounting 30,000 pages, and Legal

50,000 pages. What was Accounting department’s share of the copy center cost?

a. $15,000

b. $6,000

c. $9,000

d. $7,500

2-22

Multiple Choice Answers

1. a (LO1)

2-23

Demonstration Problem 1

A developer plans to buy a parcel of land and construct an office building on top of it. He

narrows his search to two possible lots in adjacent states with convenient access to highways.

The expected returns from Lots C and D are $190,000 and $210,000, respectively.

Required:

What is the opportunity cost of funds the developer uses to purchase Lot D?

Demonstration Problem 1 – Solution

2-25

Demonstration Problem 2

Kahn Industry, Inc. has three divisions. The following information was available for last quarter.

Division A

Division B

Division C

Company

Revenues

$200,000

$320,000

$140,000

$660,000

Cost of goods (or services) sold

160,000

240,000

100,000

500,000

Gross margin

$240,000

$ 80,000

$ 40,000

$160,000

Marketing and administrative costs

18,000

20,000

12,000

50,000

Operating profit

$ 22,000

$ 60,000

$ 28,000

$110,000

Interest

10,000

Income taxes (30%)

30,000

Net income

$ 70,000

The CEO of Kahn Industry wanted to allocate the interest cost of $10,000 to the three divisions.

Required:

1. Identify the cost object(s) and the cost pool.

2. Allocate the interest cost based on each division’s (1) revenues, (2) gross margin, and (3)

operating profit.

3. Draw a cost flow diagram assuming the allocation of interest cost is based on revenues.

Demonstration Problem 2 – Solution

Part 1

Part 2

Division A

Division B

Division C

Total

(1) Revenues

$200,000

$320,000

$140,000

$660,000

Allocation rule

Allocation

(2) Gross margin

$160,000

Allocation rule

Allocation

(3) Operating profit

$110,000

Allocation rule

Allocation

Part 3

Cost Pool

Interest cost

$10,000

30.3%

48.5%

21.2%

2-27

Demonstration Problem 3

The account balances are listed below for Eagle Manufacturing Company for the month of

March.

Finished goods inventory, March 31

$29,000

Direct materials purchases

70,000

Indirect labor

21,000

Direct labor

48,000

Work-in-process inventory, March 31

73,000

Factory supervisory salaries

12,000

Direct materials inventory, March 1

12,000

Factory utilities expense

4,000

Direct materials inventory, March 31

21,000

Work-in-process inventory, March 1

54,000

Factory depreciation expense

5,000

Finished goods inventory, March 1

33,000

Required:

Prepare a cost of goods manufactured and sold statement for Eagle Manufacturing Company for

the month ended March 31.

2-28

Demonstration Problem 3 – Solution

Eagle Manufacturing Company

Cost of Goods Manufactured and Sold Statement

For the month of March

Beginning work-in-process inventory

$ 54,000

Manufacturing costs during the year:

Direct materials

Beginning inventory

Add: Purchase of direct materials

Direct materials available

Less ending inventory

Direct material put into production

Direct labor

Manufacturing overhead:

Indirect labor

Factory supervisory salaries

Factory utilities expense

Factory depreciation expense

Total manufacturing overhead

Total manufacturing costs incurred

Total work in process during the year

Less ending work-in-process inventory

Cost of goods manufactured

Beginning finished goods inventory

Finished goods available for sale

Less ending finished goods inventory

Cost of goods sold

2-29

Demonstration Problem 4

Gourmet Industry manufactures pasta machines. The accountant of the company provides the

cost structure for each pasta machine produced as follows:

Variable manufacturing cost

$ 85

Fixed manufacturing cost

(=

Fixed manufacturing cost per year $120,000

Units produced per year 2,000

=

)

60

$145

The regular price for each pasta machine is $200. A regional restaurant chain wants to buy 150

pasta machines for $120 each. Gourmet Industry is also responsible for a one-time shipping cost

of $850. Marketing, administrative, total fixed costs, and regular sales are not affected by the

decision. Gourmet Industry has enough idle capacity to handle the order.

Required:

Determine if Gourmet Industry should accept the special order.

Demonstration Problem 4 – Solution

By accepting the special order, Gourmet Industry will increase its operating profit by $4,400.

2-31

Demonstration Problem 5

The following information is available for each unit of the finished product produced and sold:

Sales price

$60

Variable manufacturing cost

20

Fixed manufacturing cost*

12

Variable marketing and administrative cost

6

Fixed marketing and administrative cost*

4

* The unit fixed manufacturing cost and fixed marketing and administrative costs are based on

an estimated volume of 6,000 units produced and sold.

Required:

Determine full absorption cost, variable cost, full cost, gross margin, contribution margin, and

operating profit per unit.

2-32

Demonstration Problem 5 – Solution

Full absorption cost = $20 + $12 = $32

Variable cost = $20 + $6 = $26

2-33

Demonstration Problem 6

(Continued from Demonstration Problem 5)

The following information is available for each unit of the finished product produced and sold:

Sales price

$60

Variable manufacturing cost

20

Fixed manufacturing cost*

12

Variable marketing and administrative cost

6

Fixed marketing and administrative cost*

4

* The unit fixed manufacturing cost and fixed marketing and administrative costs are based on

an estimated volume of 6,000 units produced and sold.

Required:

Prepare a traditional income statement and contribution margin income statement when 6,000

units are produced and sold.

Demonstration Problem 6 – Solution

Traditional

Income Statement

Contribution Margin

Income Statement