CHAPTER 2 Analyzing Transactions

Prob. 2-4B (Concluded)

5. (a) The unadjusted trial balance in (4) still balances because the debits equaled

the credits in the original journal entry.

(b) The correcting entry for $9,000 ($10,000 – $1,000) would be as follows:

Page 19

Post.

Ref. Debit Credit

(c) Slide

Date

JOURNAL

Description

CHAPTER 2 Analyzing Transactions

Prob. 2-5B

1.

Debit Credit

Balances Balances

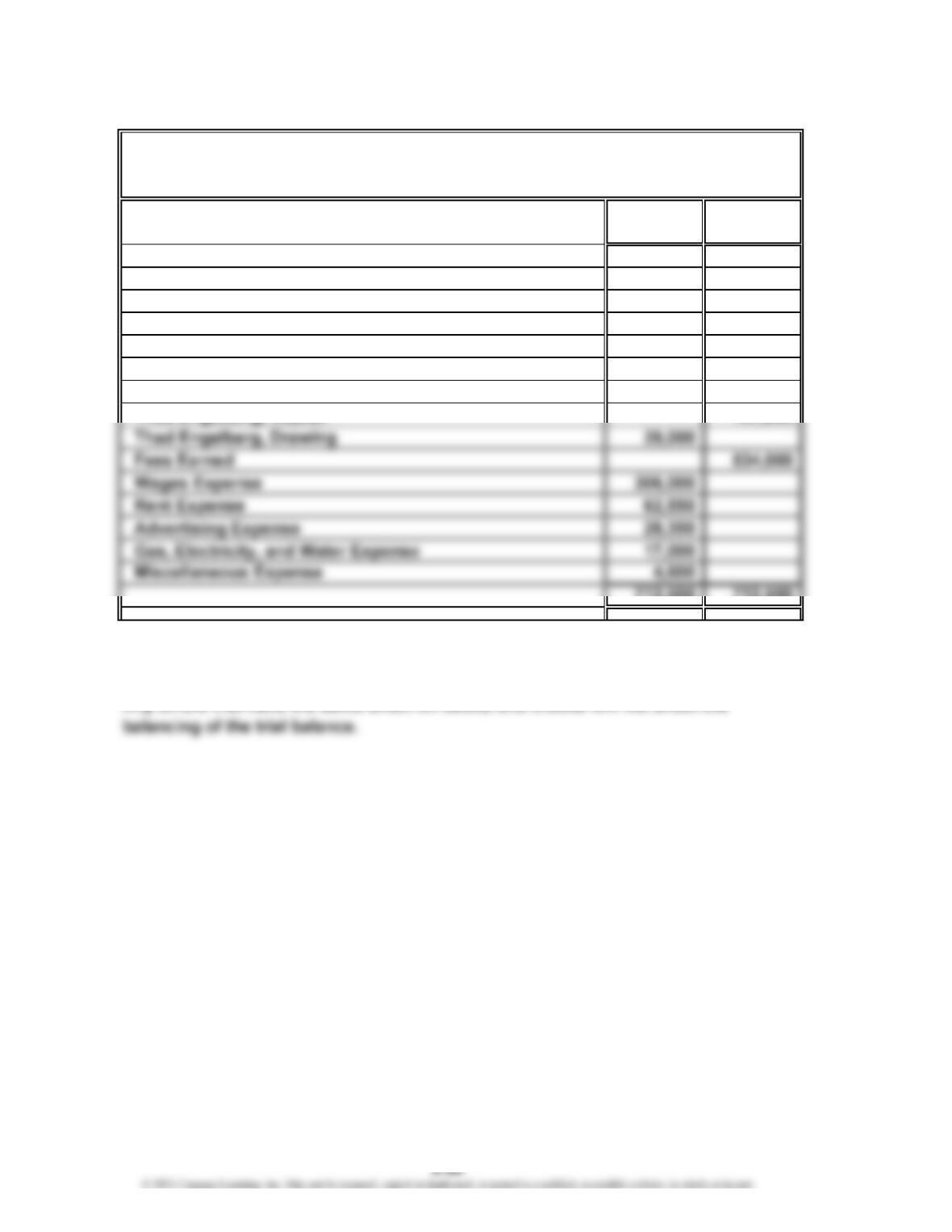

Cash* 20,250

Accounts Receivable 56,400

Supplies 6,750

Prepaid Insurance 9,600

Equipment 162,000

Notes Payable 54,000

Accounts Payable 16,650

712,500 712,500

*$25,550 – $8,000 (a) + $2,700 (b)

2. No. The trial balance indicates only that the debits and credits are equal.

Tech Support Services

Unadjusted Trial Balance

January 31, 20Y8

CHAPTER 2 Analyzing Transactions

2. and 3.

Page 1

Post.

Ref. Debit Credit

20Y9

July 1 Cash 11 5,000

Peyton Smith, Capital 31 5,000

2 Cash 11 1,000

Accounts Receivable 12 1,000

3 Cash 11 7,200

Unearned Revenue 23 7,200

5 Office Equipment 17 7,500

Accounts Payable 21 7,500

8 Advertising Expense 55 200

Cash 11 200

11 Cash 11 1,000

Fees Earned 41 1,000

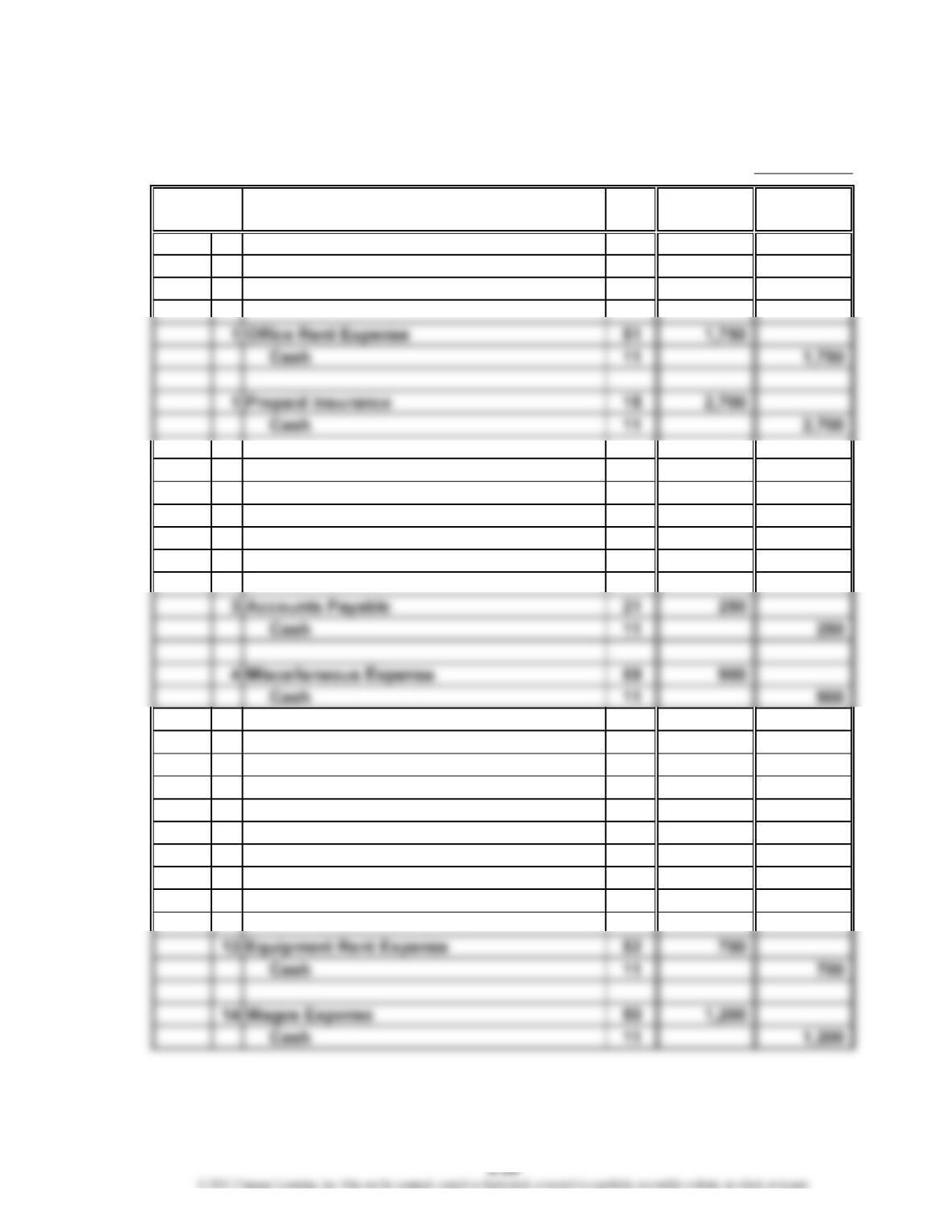

Date

CONTINUING PROBLEM

JOURNAL

Description

CHAPTER 2 Analyzing Transactions

Continuing Problem (Continued)

2. and 3.

Page 2

Post.

Ref. Debit Credit

20Y9

July 16 Cash 11 2,000

Fees Earned 41 2,000

22 Advertising Expense 55 800

Cash 11 800

23 Cash 11 750

Accounts Receivable 12 1,750

Fees Earned 41 2,500

29 Miscellaneous Expense 59 540

Cash 11 540

30 Cash 11 500

Accounts Receivable 12 1,000

Fees Earned 41 1,500

31 Cash 11 3,000

Fees Earned 41 3,000

Date

JOURNAL

Description

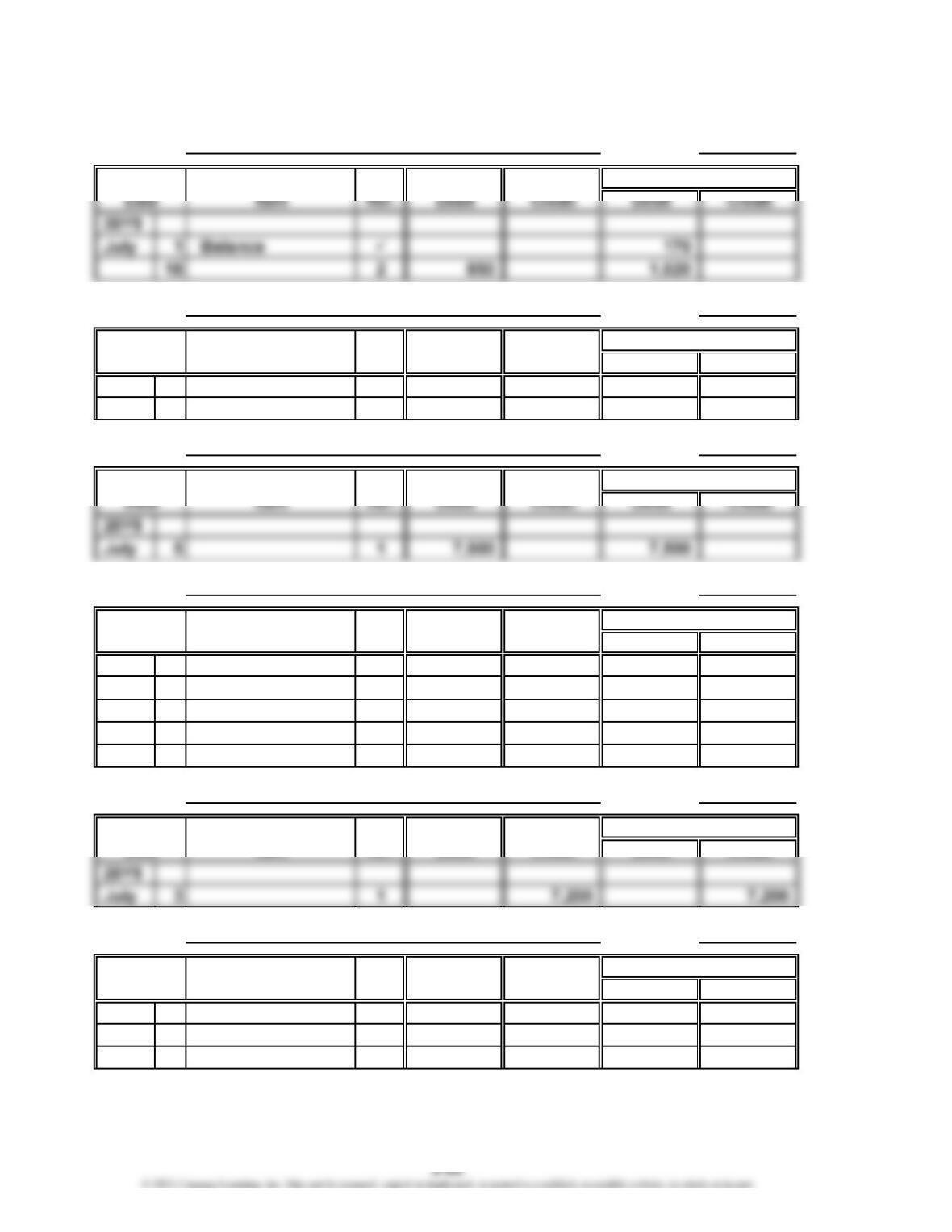

CHAPTER 2 Analyzing Transactions

Continuing Problem (Continued)

1. and 3.

Account No. 11

Post.

Item Ref. Debit Credit Debit Credit

3 1 250 12,420

4 1 900 11,520

8 1 200 11,320

11 1 1,000 12,320

31 2 3,000 12,595

31 2 1,400 11,195

31 2 1,250 9,945

Account No. 12

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 1,000

2 1 1,000 — —

Date

Date

Balance

Cash

Account:

Account: Accounts Receivable

Balance

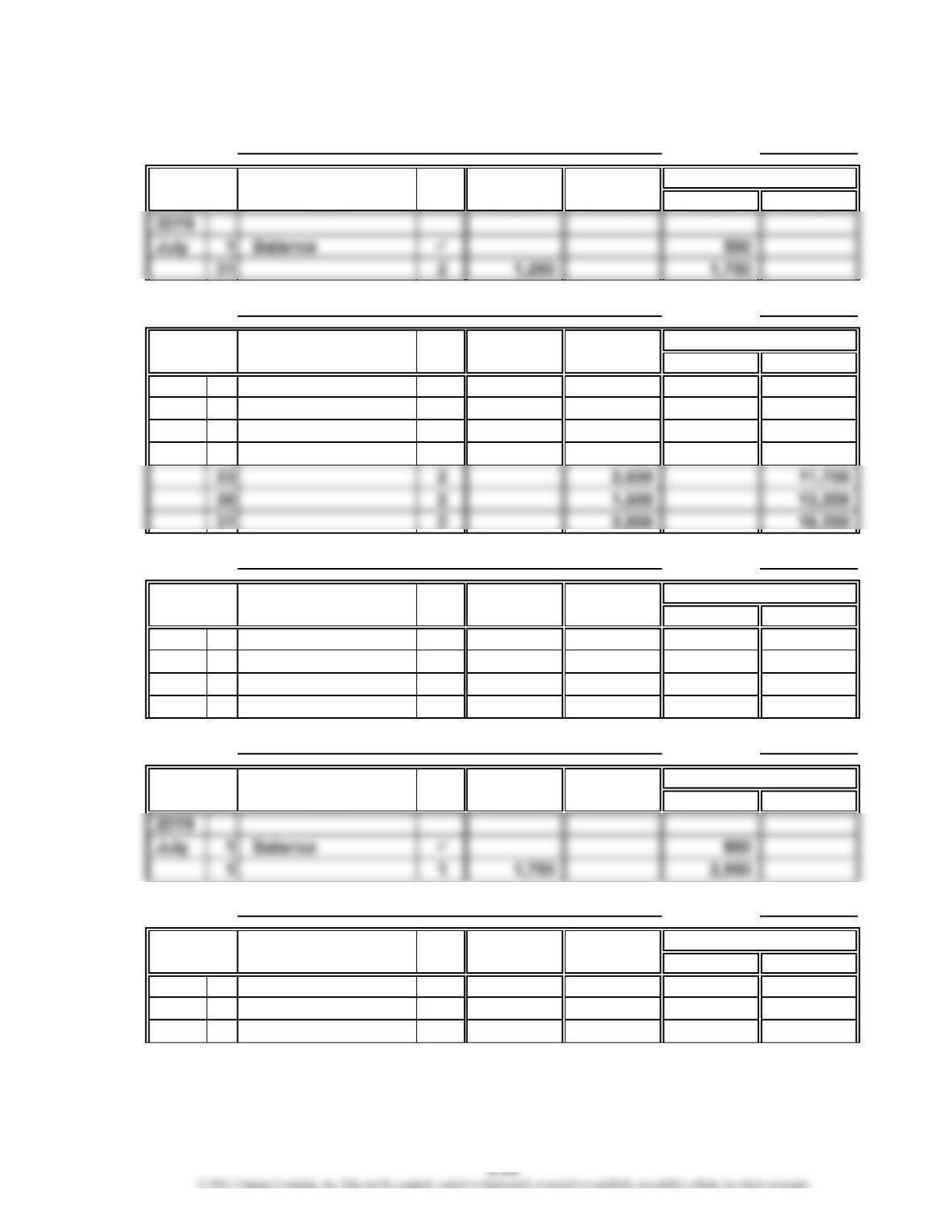

CHAPTER 2 Analyzing Transactions

Continuing Problem (Continued)

Account No. 14

Post.

Account No. 15

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 1 2,700 2,700

Account No. 17

Post.

Account No. 21

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 250

3 1 250 — —

5 1 7,500 7,500

18 2 850 8,350

Account No. 23

Post.

Account No. 31

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 4,000

1 1 5,000 9,000

Balance

Date

Account: Office Equipment

Account: Unearned Revenue

Account: Accounts Payable

Balance

Date

Balance

Account: Peyton Smith, Capital

Supplies

Account:

Account: Prepaid Insurance

Balance

Balance

Balance

Date

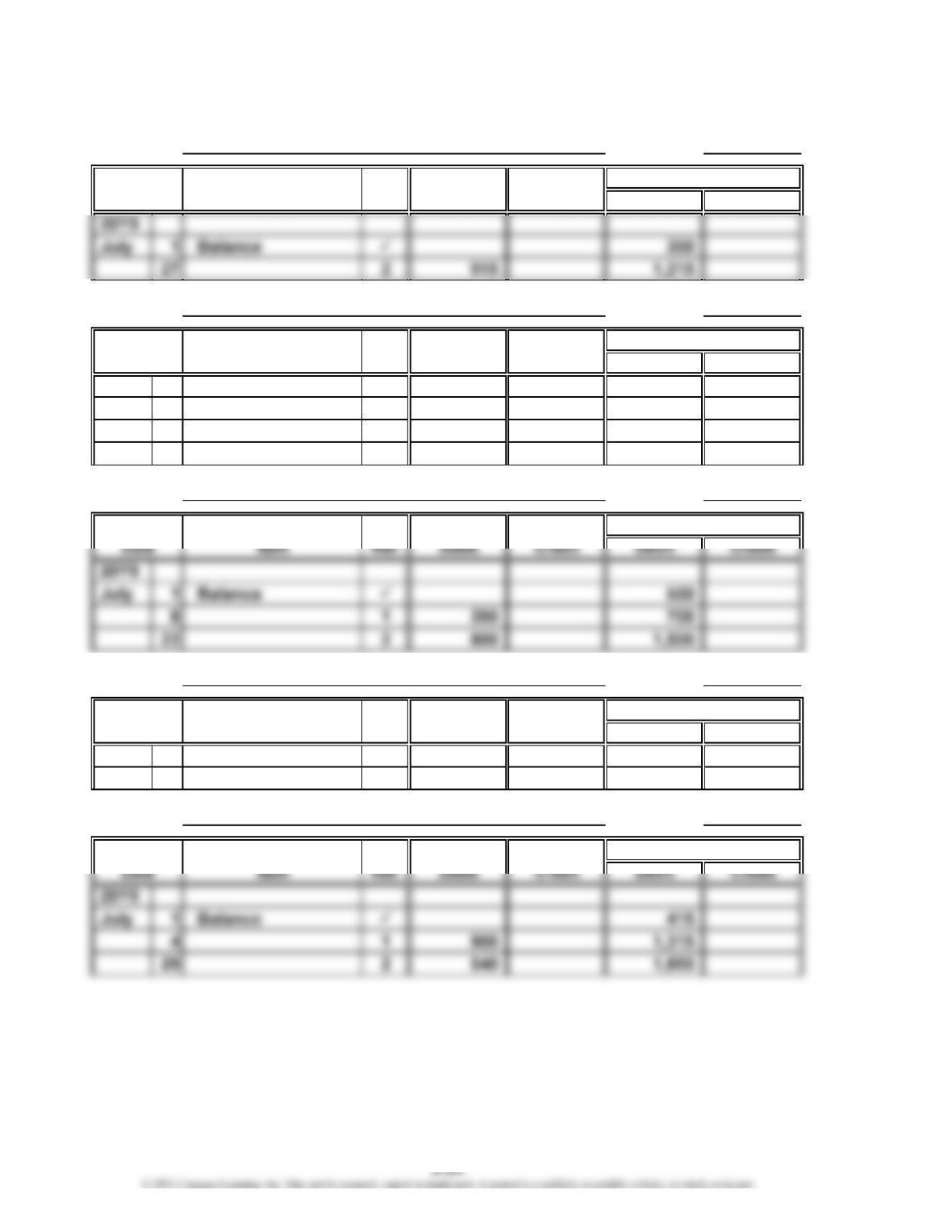

CHAPTER 2 Analyzing Transactions

Continuing Problem (Continued)

Account No. 32

Post.

Item Ref. Debit Credit Debit Credit

Account No. 41

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 6,200

11 1 1,000 7,200

16 2 2,000 9,200

Account No. 50

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 400

14 1 1,200 1,600

28 2 1,200 2,800

Account No. 51

Post.

Item Ref. Debit Credit Debit Credit

Account No. 52

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 675

13 1 700 1,375

Date

Balance

Peyton Smith, Drawing

Account:

Balance

Date

Account: Fees Earned

Balance

Date

Balance

Date

Account: Equipment Rent Expense

Account: Wages Expense

Balance

Date

Account: Office Rent Expense

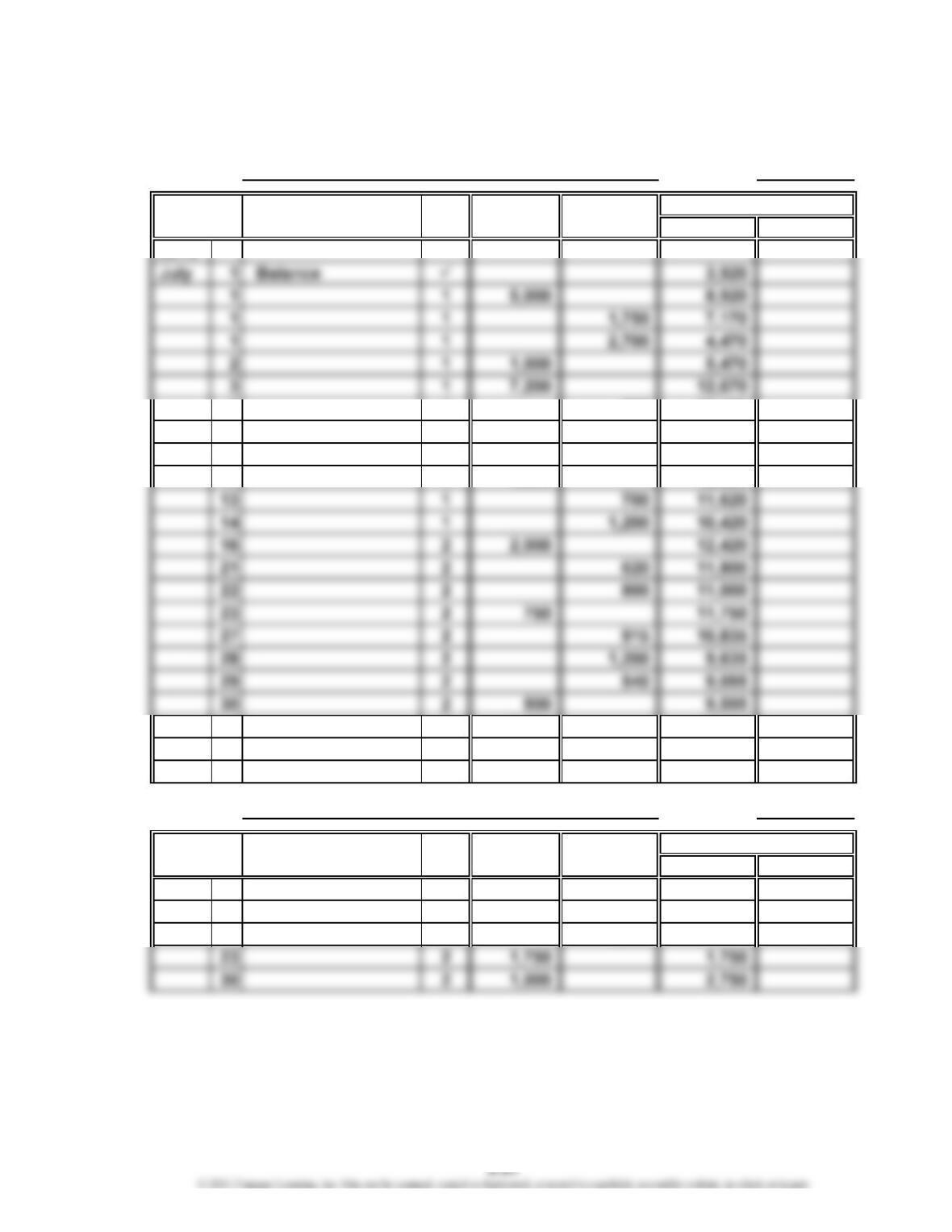

CHAPTER 2 Analyzing Transactions

Continuing Problem (Continued)

Account No. 53

Post.

Item Ref. Debit Credit Debit Credit

Account No. 54

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 1,590

21 2 620 2,210

31 2 1,400 3,610

Account No. 55

Post.

Account No. 56

Post.

Item Ref. Debit Credit Debit Credit

20Y9

July 1 Balance 180

Account No. 59

Post.

Account: Supplies Expense

Balance

Date

Account: Miscellaneous Expense

Balance

Account: Utilities Expense

Balance

Date

Balance

Date

Balance

Music Expense

Account:

Account: Advertising Expense

CHAPTER 2 Analyzing Transactions

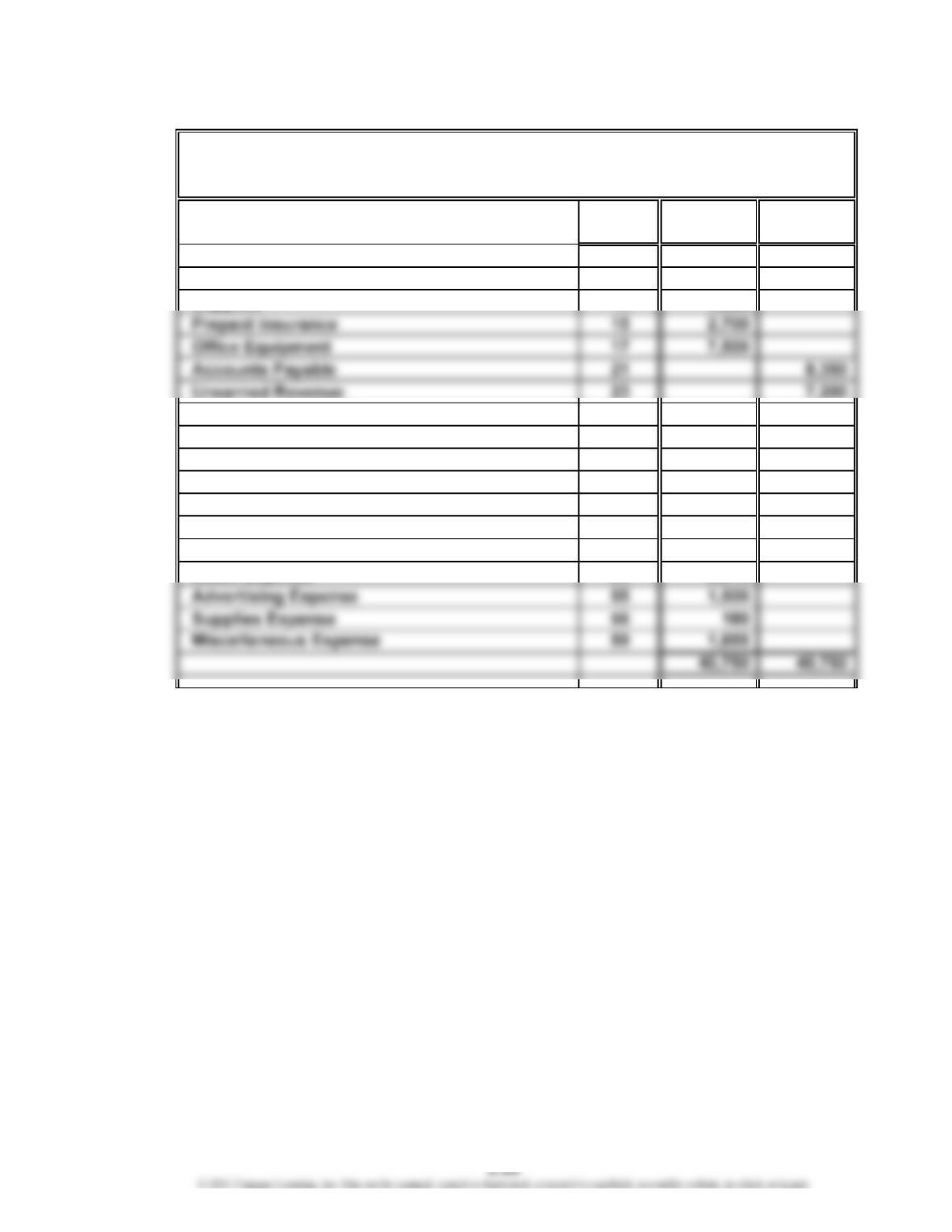

Continuing Problem (Concluded)

4.

Account Debit Credit

No. Balances Balances

Cash 11 9,945

Accounts Receivable 12 2,750

Peyton Smith, Capital 31 9,000

Peyton Smith, Drawing 32 1,750

Fees Earned 41 16,200

Wages Expense 50 2,800

Office Rent Expense 51 2,550

Equipment Rent Expense 52 1,375

Utilities Expense 53 1,215

PS Music

Unadjusted Trial Balance

July 31, 20Y9

CHAPTER 2 Analyzing Transactions

CP 2-1

1. No. For financial accounting information to be useful, it must accurately reflect

an entity’s business transactions and economic activity. For this to happen,

each account must reflect the increases or decreases that result from each

2. The users of the financial information who rely on this information will be

affected, as the information will not be a faithful representation of the entity’s

economic activity.

CP 2-2

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31,

2018, follows:

1. $22,536 million

2. $12,724 million ($6,040 + $3,468 + $3,216)

3. $9,812 million ($22,536 million on total assets – $12,724 million total liabilities)

CP 2-3

1. The rules of debit and credit must be memorized. Dot is correct in that the rules

of debit and credit could be reversed as long as everyone accepted and abided

by the rules. However, the important point is that everyone accepts the rules as

the way in which transactions should be recorded. This generates uniformity

across the accounting profession and reduces errors and confusion. Because the

current rules of debit and credit have been used for centuries, Dot should adapt

to the current rules of debit and credit, rather than devise her own.

CASES & PROJECTS

CHAPTER 2 Analyzing Transactions

CP 2-3 (Concluded)

assets is a debit would also be removed. The accounting equation would still

hold, but the control over recording transactions would be weakened.

(debit) means “left” and credere (credit) means “right.”

2. The accounting system may be designed to capture information about the

buying habits of various customers or vendors, such as the quantity

normally ordered, average amount ordered, and number of returns. Thus, in

CP 2-4

Note to Instructors: The purpose of this activity is to familiarize students with the job

opportunities available in accounting and allow them to demonstrate their ability to

communicate the role of accounting in the context of a specific position that requires

knowledge of accounting. An example of an advertisement for such a position is

shown below. Individual student answers will vary depending on the specific scenario

they select.

ABOUT THE COMPANY

Our client is looking to add a Financial Analyst. With a large and growing finance team,

there is significant opportunity for growth and advancement within the department.

opportunities for growth.

RESPONSIBILITIES OF THE FINANCIAL ANALYST

The Financial Analyst will:

•Conduct special studies to analyze complex financial actions and prepare

recommendations for policy, procedure, control, or action.

•Analyze financial information to determine present and future financial performance.

•Evaluate complex profit plans, operating records, and financial statements.

CHAPTER 2 Analyzing Transactions

CP 2-5

The following general journal entry should be used to record the receipt of tuition

payments received in advance of classes:

Cash…………………………………………………………………

…

XXX

Unearned Tuition Deposits…………………………………… XXX

Cash is an asset account, and Unearned Tuition Deposits is a liability account. As

CP 2-6

The journal is called the book of original entry. It provides a time-ordered history

of the transactions that have occurred for the firm. This time-ordered history is

very important because it allows one to trace ledger account balances back to

the original transactions that created those balances. This is called an “audit

trail.” If the firm recorded transactions by posting to ledgers directly, it would be

nearly impossible to reconstruct actual transactions. The debits and credits

would all be separated and accumulated into the ledger balances. Once the

CP 2-7

a. Although the titles and numbers of accounts may differ, depending on how

expenses are classified, the following accounts would be adequate for

recording transaction data for Eagle Caddy Service:

11 Cash 41 Fees Earned

12 Accounts Receivable

13 Supplies

b.

Fees earned $11,400

Expenses:

Rent expense $3,500

Supplies expense 1,925

Wages expense 850

Note to Instructors: Students may have prepared slightly different income

statements, depending upon the titles of the major expense classifications

chosen. Regardless of the classification of expenses, however, the total

sales, total expenses, and net income should be as presented above.

T accounts are not required for the preparation of the income statement of

Eagle Caddy Service. The following presentation illustrates one solution using

Balance Sheet Accounts Income Statement Accounts

1. Assets 4. Revenue

Income Statement

For the Month Ended June 30, 20Y9

5. Expenses

Eagle Caddy Service

CHAPTER 2 Analyzing Transactions

CP 2-7 (Continued)

11 41

20Y9 20Y9 20Y9

June 1 2,000 June 1 500 June 15 5,400

15 5,400 2 750 25 1,800

30 4,200 3 600 30 4,200

12 52

20Y9 20Y9 20Y9

June 25 1,800 June 30 1,500 June 30 1,925

Bal. 300

13 53

20Y9 20Y9 20Y9

June 2 750 June 30 1,925 June 30 850

7 1,000

22 850

Bal. 675

21 54

Utilities Expense

Cash Fees Earned

Supplies ExpenseAccounts Receivable

Supplies

Accounts Payable

Wages Expense

CHAPTER 2 Analyzing Transactions

CP 2-7 (Concluded)

c. $6,265, computed in the following manner:

Cash receipts:

Initial investment…………………………………………………

…

$2,000

Cash sales ($5,400 + $4,200)……………………………………

…

9,600

Collections on accounts…………………………………………

…

1,500

Total cash receipts during June……………………………

…

$13,100

Cash disbursements:

Rent expense ($500 + $3,000)…………………………………… $3,500

Supplies purchased for cash……………………………………

…

750

Wages expense……………………………………………………

…

850

Payment for supplies on account……………………………… 1,000