Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-1

CHAPTER 2

ANALYZING AND RECORDING TRANSACTIONS

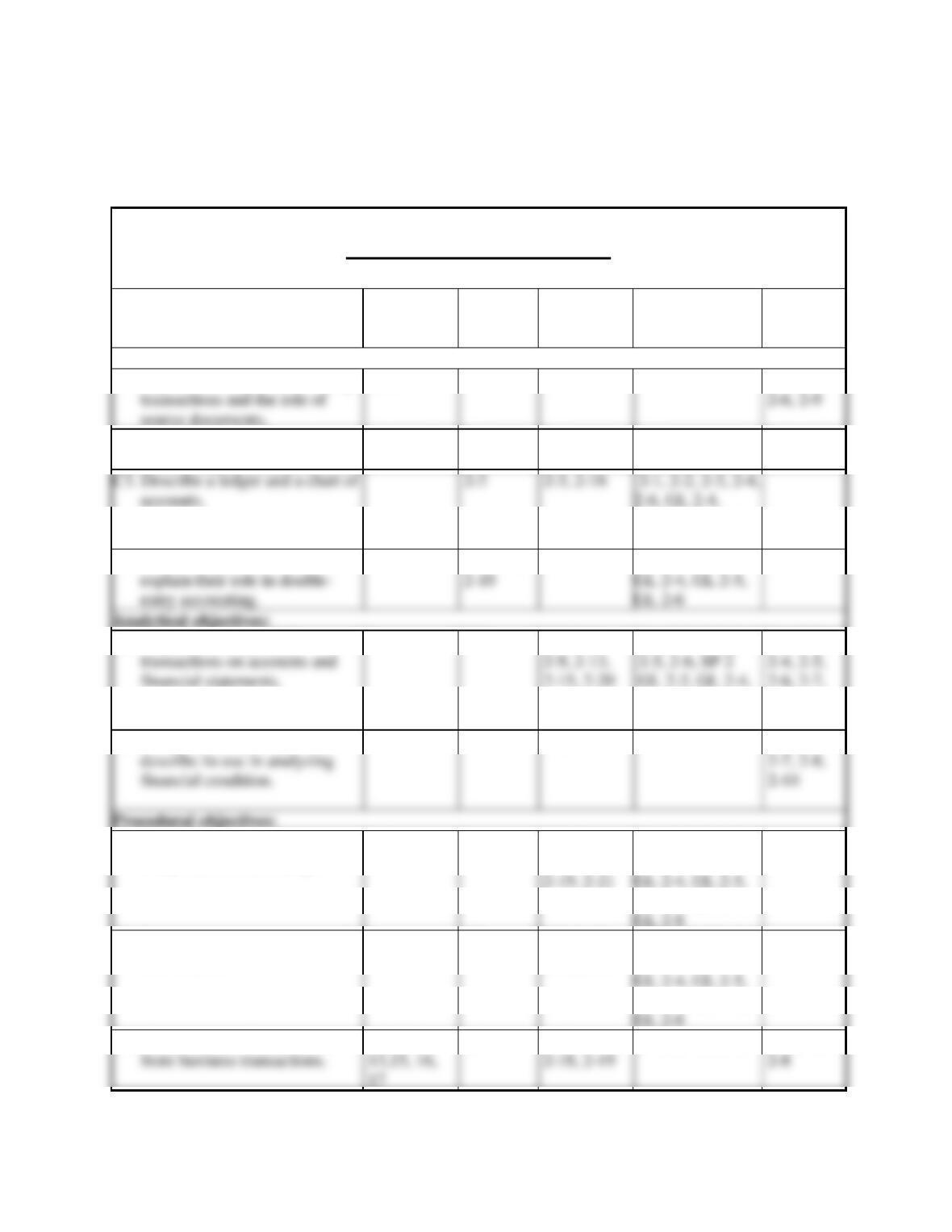

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Explain the steps in processing

3, 6, 9

2-1

2-1

2-6

2-3, 2-4,

C2. Describe an account and its use

in recording transactions.

1 ,2, 14

2-2

2-2

2-5

2-4, 2-6

2-3

2-3, 2-16

2-1, 2-2, 2-3, 2-4,

GL 2-5, GL 2-6,

GL 2-7

2-10

GL 2-4, GL 2-5,

GL 2-6

C4. Define debits and credits and

7

2-4, 2-5,

2-4

2-1, 2-2, 2-3,

2-6

transactions on accounts and

2-9, 2-13,

2-15, 2-20

2-5, 2-6, SP 2

GL 2-2, GL 2-4,

2-4, 2-5,

2-6, 2-7,

A1. Analyze the impact of

.

2-7

2-5, 2-6,

2-1, 2-2, 2-3, 2-4,

GL 2-5, GL 2-6,

GL 2-7, GL 2-8

2-1, 2-2,

2-8

A2. Compute the debt ratio and

2-22

2-5

2-1, 2-2,

2-19, 2-21

GL 2-4, GL 2-5,

P1. Record transactions in a journal

and post entries to a ledger.

4, 5

2-6

2-7, 2-11,

2-12, 2-14

GL 2-8

2-1, 2-2, 2-3, 2-4,

SP 2, GL2-3,

GL 2-6, GL 2-7,

P2. Prepare and explain the use of a

trial balance.

8

2-8

2-8, 2-10,

2-20, 2-21

GL 2-4, GL 2-5,

GL 2-8

2-1, 2-2, 2-3, 2-4,

2-5, SP 2,

GL 2-6, GL 2-7,

17

P3. Prepare financial statements

10, 11, 12,

2-9

2-16, 2-17,

2-5, ES-1, ES-2

2-4, 2-7,

source documents.

2-6, 2-9

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-2

*See additional information on next page that pertains to these quick studies, exercises and problems.

SP refers to the Serial Problem

GL refers to the General Ledger Problems

ES refers to Excel Simulations

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-3

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

by an intuitive question and provide at-a-glance information regarding how an instructor’s class is performing.

Connect Insight is available through Connect titles.

General Ledger

Excel Simulations

Assignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas

and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me

tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student.

Synopsis of Chapter Revisions

NEW opener—Soko and entrepreneurial assignment.

Simplified discussion on analyzing and recording process.

Streamlined discussion of classified vs. unclassified balance sheet.

Enhanced explanation of computing equity.

Enhanced Exhibit 2.4 to identify account categories.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-4

Chapter Outline

Notes

I. System of Accounts

A. Identify transaction from source document which identifies and

describes transactions and events entering the accounting process.

B. Analyze transaction using the accounting equation.

II. The Account and its Analysis

A. An account is a record of increases and decreases in a specific asset,

liability, equity, revenue, or expense.

B. Account categories include:

Payable, Unearned Revenues, and Accrued Liabilities.

1. Assets—resources owned or controlled by a company that have

future economic benefit. Examples include Cash, Accounts

2. Liabilities—claims (by creditors) against assets, which means

they are obligations to transfer assets or provide products or

services to others. Examples include Accounts Payable, Note

3. Equity—owner’s claim on company’s assets is called equity or

owner’s equity. Examples include Owner’s Capital, Owner’s

Withdrawals (decreases in equity). Revenues (results from

providing goods or services; i.e. Sales, Fees Earned) increases

equity. Expenses (results from assets or services used in

operation; i.e. Supplies Expense) decreases equity.

III. Double-Entry Accounting

B. The chart of accounts is a list of all accounts in the ledger with their

A. The general ledger or ledger (referred to as the books) is a collection

Chapter Outline

Notes

C. A T-account represents a ledger account and is used to understand the

effects of one or more transactions. Has shape like the letter T with

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-5

account title on top.

IV. Debits and Credits

A. The left side of an account is called the debit side. A debit is an entry

on the left side of an account.

B. The right side of an account is called the credit side. A credit is an

entry on the right side of an account.

V. Double-Entry System—requires that each transaction affect, and be

recorded in, at least two accounts. The total debits must equal total credits

for each transaction.

A. The assignment of balance sides (debit or credit) follows the

accounting equation.

balances.

1. Assets are on the left side of the equation; therefore, the left, or

debit, side is the normal balance for assets.

3. Withdrawals, revenues, and expenses really are changes in equity,

but it is necessary to set up temporary accounts for each of these

items to accumulate data for statements. Withdrawals and

B. Three important rules for recording transactions in a double-entry

accounting system are:

1. Increases to assets are debits to the asset accounts. Decreases to

assets are credits to the asset accounts.

3. Increases to equity are credits to the equity accounts. Decreases

to equity are debits to the equity accounts.

total debits the account has a credit balance. When two sides are

equal the account has a zero balance.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-6

Chapter Outline

Notes

VI. Journalizing and Posting Transactions

A. Four steps in processing transactions are as follows:

Journalizing—The process of recording each transaction in a journal.

2. Analyze using the accounting equation. Apply double entry

accounting to determine account to be debited and credited.

3. Record journal entry—recorded chronologically (A journal

gives us a complete record of each transaction in one place.)

4. Posting Journal Entries to Ledger—transfer (or post) each

entry from journal to ledger.

a. Debits are posted as debit, and credits as credits to the

accounts identified in the journal entry.

Note: To see an illustration of analyzing, journalizing and posting of 16

basic transactions refer to the textbook.

VII. Trial Balance

A. A trial balance is a list of accounts and their balances (either debit

or credit) at a point in time. Account balances are reported in their

appropriate debit or credit columns of the trial balance.

B. The trial balance tests for the equality of the debit and credit

account balances as required by double-entry accounting.

C. Preparing a Trial Balance: three steps to prepare a trial balance are

as follows:

2. Compute the total debit balances and the total credit balances.

3. Verify (prove) total debit balances equal total credit balances.

D. Searching for Errors: when a trial balance does not balance, an

error has occurred and must be corrected. Follow these steps:

the trial balance as a credit (or debit).

2. Verify that account balances are accurately entered from

ledger.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-7

Chapter Outline

Notes

4. Re-compute each account balance in the ledger.

6. Verify that the original journal entry has equal debits and

credits.

(Note: Any errors must be located and corrected before preparing

The next chapter will address adjustments).

E. Presentation Issues

1. Dollar signs are not used in journals and ledgers but do appear

2. Usual practice on statements is to put dollar signs before the

first and last number in each column.

4. Companies commonly round in reports to the nearest dollar, or

even higher levels.

5. Double rule the final total(s) on the financial statements.

VIII. Decision Analysis—Debt Ratio

A. Companies finance their assets with either liabilities or equity.

B. A company that finances a relatively large portion of its assets

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-8

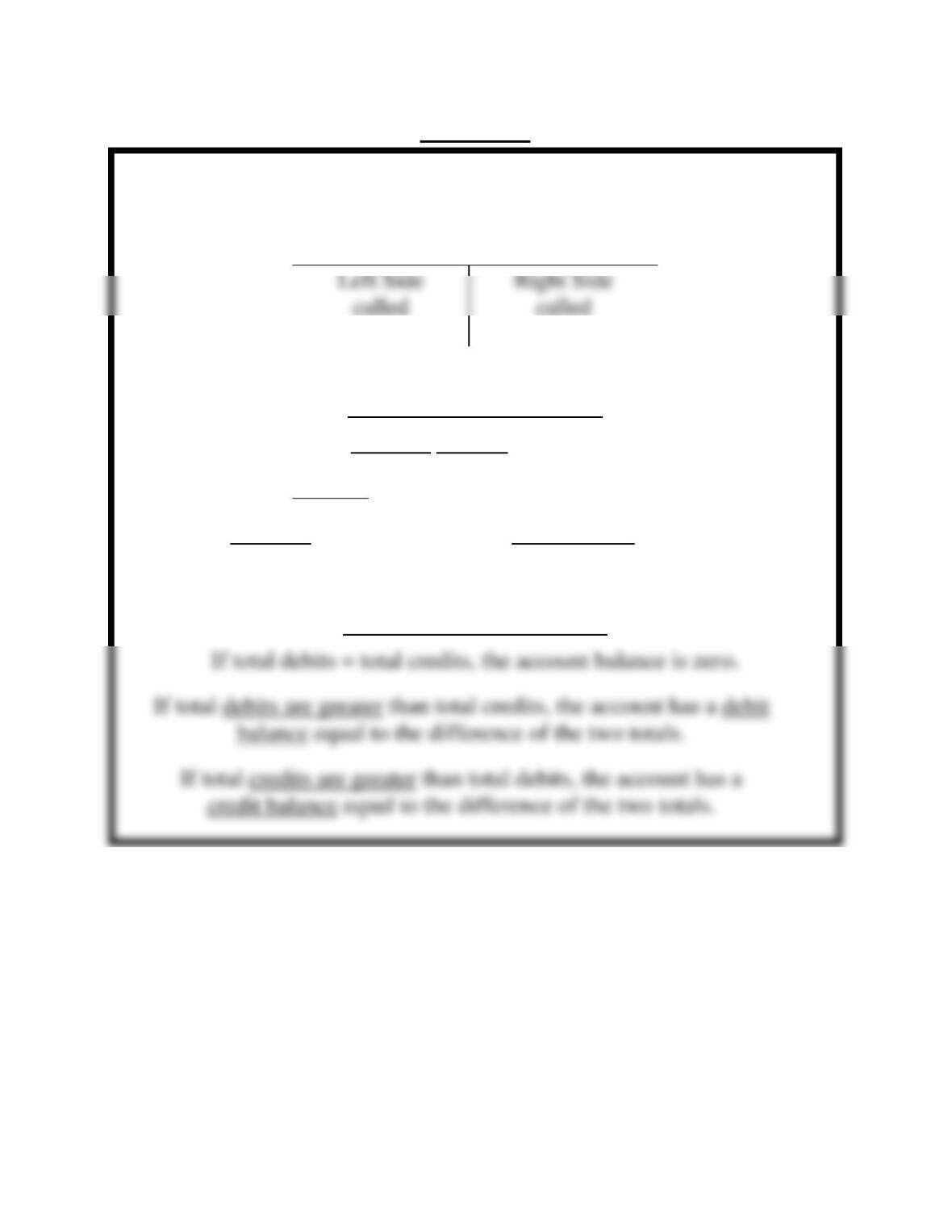

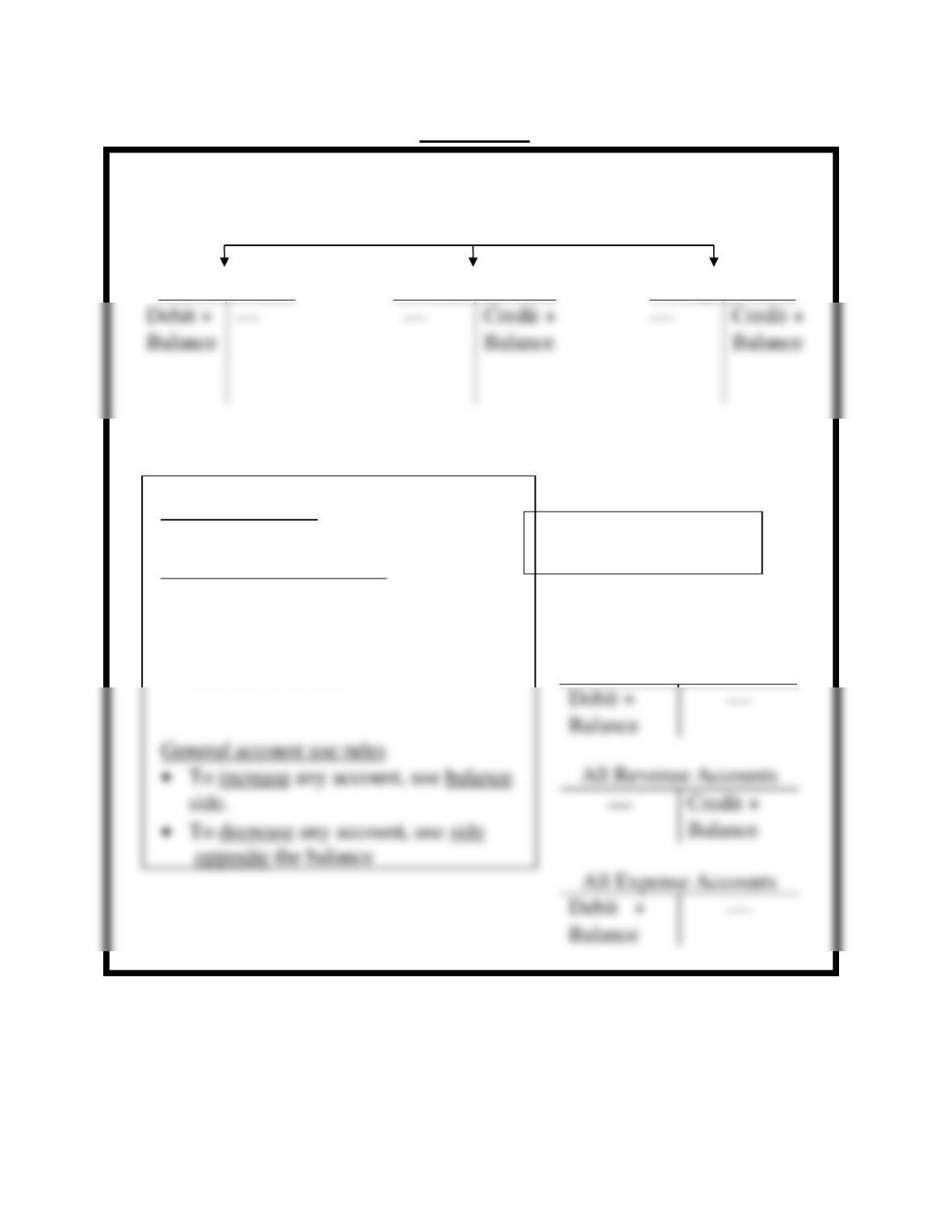

VISUAL #2-1

THREE PARTS OF AN ACCOUNT

(1) ACCOUNT TITLE

(2) DEBIT

(3) CREDIT

Rules for using accounts

Accounts are assigned balance sides (Debit or Credit).

To increase any account, use the balance side.

To decrease any account, use the side opposite the balance.

Finding account balances

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-9

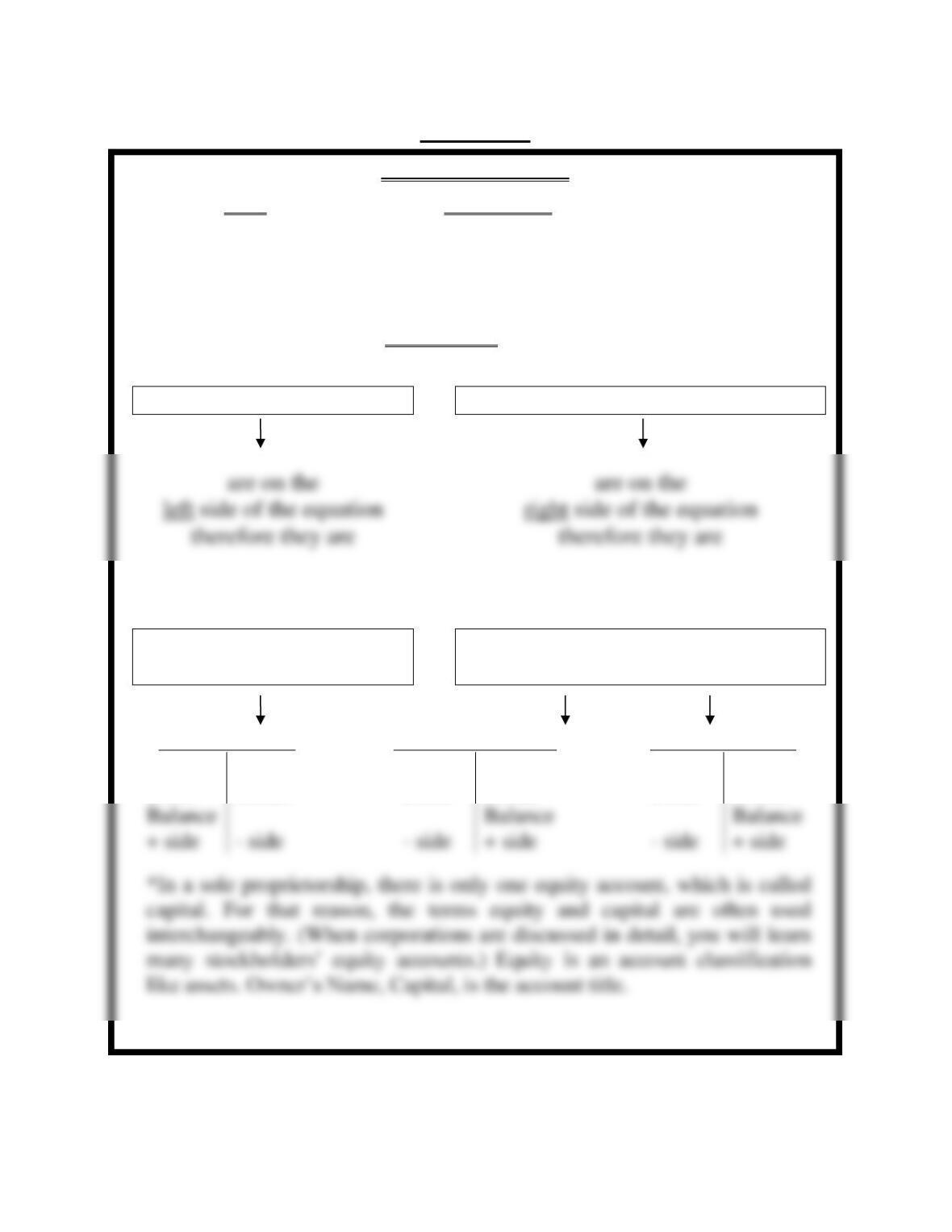

VISUAL #2-2

REAL ACCOUNTS

ALL ACCOUNTS ARE ASSIGNED BALANCE SIDES

BALANCE SIDES FOR ASSETS, LIABILITIES, AND

EQUITY ACCOUNTS ARE ASSIGNED BASED ON

SIDE OF EQUATION THEY ARE ON.

ASSETS

=

LIABILITIES + EQUITY

ASSIGNED LEFT SIDE

BALANCE

ASSIGNED RIGHT SIDE

BALANCE

DEBIT BALANCE

CREDIT BALANCE

All Asset Accts

All Liability Accts

All Equity Accts

Normal

Normal

Normal

Debit

Credit

Debit

Credit

Debit

Credit

+ side

– side

– side

+ side

– side

+ side

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-10

VISUAL #2-3

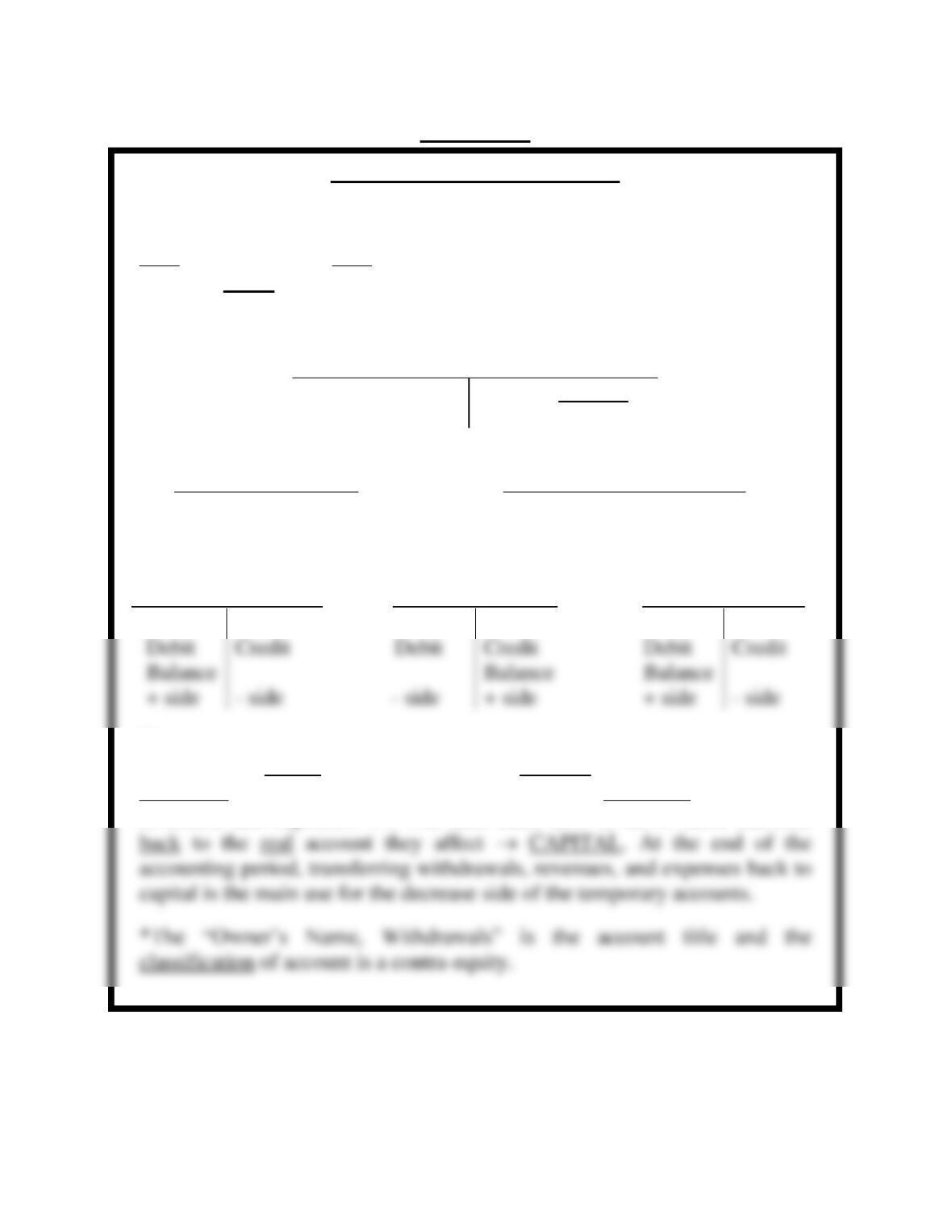

TEMPORARY ACCOUNTS

Temporary accounts are established to facilitate efficient accumulation of

data for statements. Temporary accounts are established for withdrawals,

each revenue, and each expense. Temporary accounts are assigned

balances based on how they affect equity.

(Equity Account)

Owner’s Name, Capital

Debit

Credit Balance

– side

+ side

Temporary Accounts Effect on equity? E or E

Owner, Withdrawals* E = Dr

Revenues E = Cr

Expenses E = Dr

All Withdrawal Accts

All Revenue Accts

All Expense Accts

Normal

Normal

Normal

Note:

Transactions during the period always increase the balances of these

temporary accounts since the transaction represent additional withdrawals,

revenues, and expenses. We will later learn how to move these amounts

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-11

VISUAL #2-4

USING ACCOUNTS – SUMMARY

Real Accounts

All Asset Accts

All Liability Accts

All Equity Accts

RULE REVIEW

Temporary Accounts

Transaction analysis rules

• Each transaction affects at least 2

accounts.

• Each transaction must have equal

debits and credits.

All Withdrawal

Accounts

Balance

General account use rules

opposite the balance

Balance

Balance

Balance

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-12

Chapter 2 Alternate Demonstration Problem

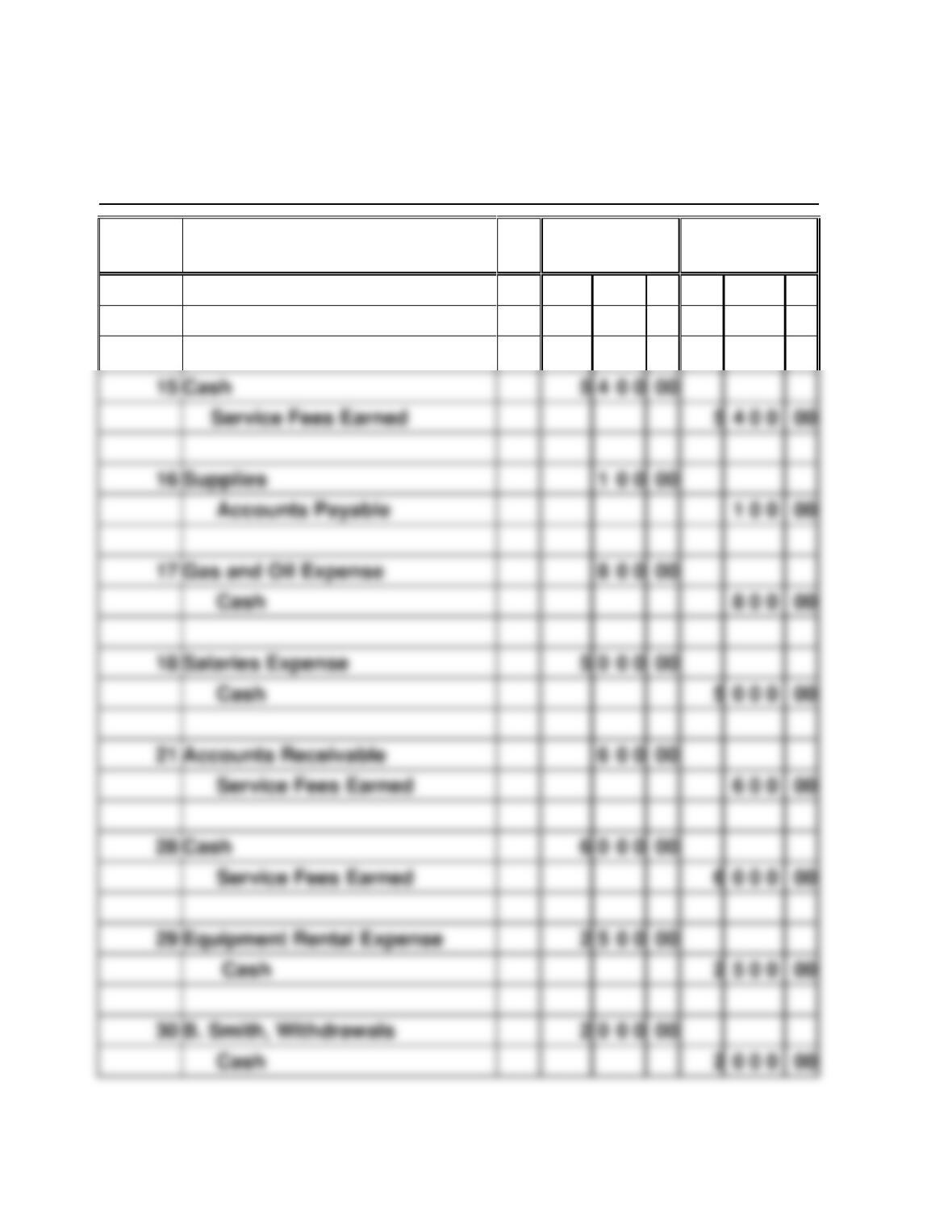

Record the following transactions of Speedy Computer Service, owned by

Bill Smith, for the month of March 2017.

March 1. Bill Smith invested $3,000 cash in his business.

15. Bill provided services and received cash amounting to $5,400

from customers.

17. Paid for gas and oil, $800.

21. Provided service on credit, $600.

29. Paid for truck and equipment rental, $2,500.

Required:

1. Record the above transactions in general journal form.

3. prepare an income statement from trial balance

5. Prepare a balance sheet using the trial balance totals and the

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-13

Chapter 2 Solution: Alternate Demonstration Problem

GENERAL JOURNAL

DATE

ACCOUNT TITLES AND

EXPLANATION

P.R.

DEBIT

CREDIT

March 1

Cash

3

0

0

0

00

Bill Smith, Capital

3

0 0 0

00

15

Cash

5

4

0

0

00

Service Fees Earned

5

4 0 0

00

Accounts Payable

1 0 0

00

17

Gas and Oil Expense

8

0

0

00

Cash

8 0 0

00

18

Salaries Expense

5

0

0

0

00

Cash

5

0 0 0

00

21

Accounts Receivable

6

0

0

00

Service Fees Earned

6 0 0

00

28

Cash

6

0

0

0

00

29

Equipment Rental Expense

2

5

0

0

00

Cash

2

5 0 0

00

30

2

0

0

0

00

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

2-14

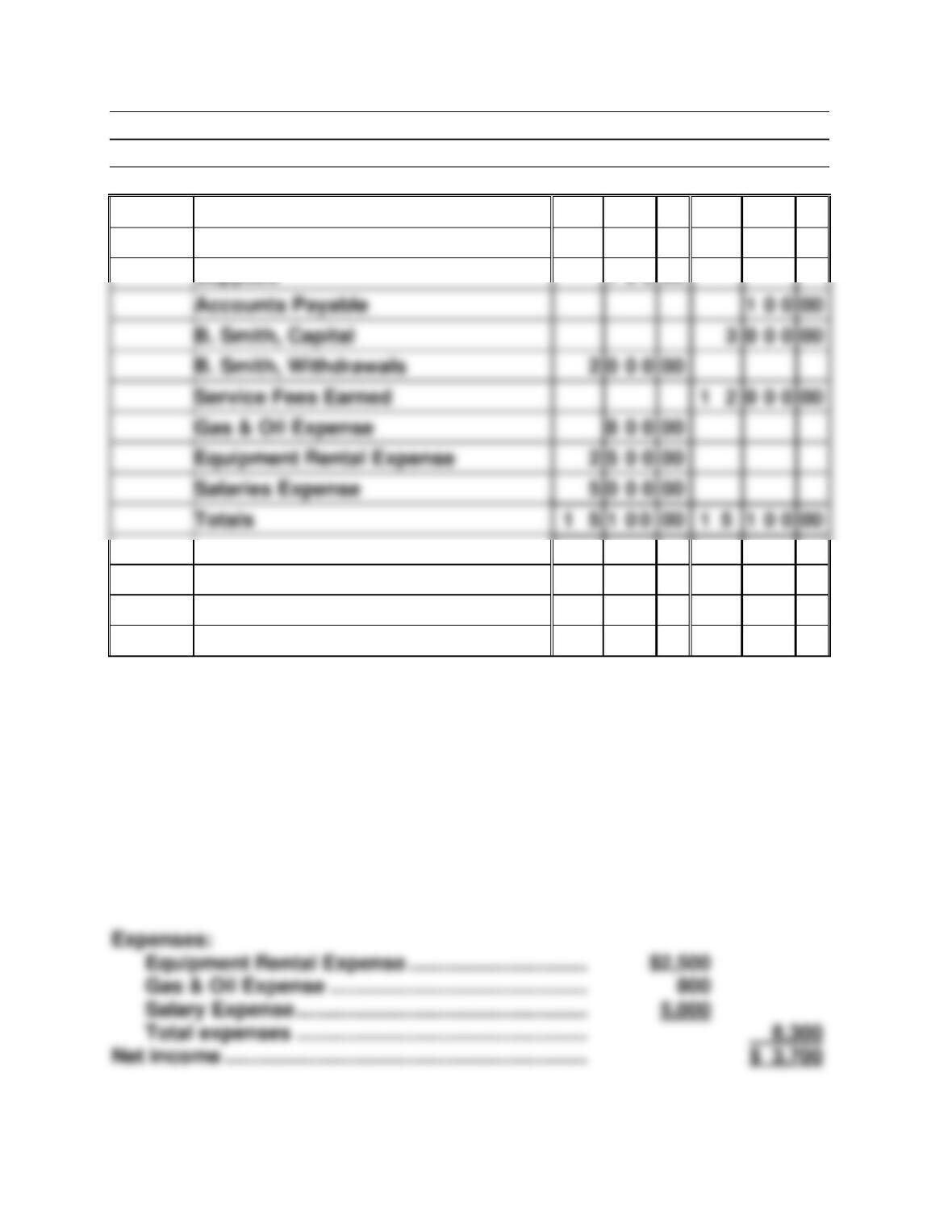

Speedy Computer Service

Trial Balance

March 31, 2017

Cash

4

1

0

0

00

Accounts Receivable

6

0

0

00

Supplies

1

0

0

00

3.

Speedy Computer Service

Income Statement

For the month ended March 31, 2017

Fees Earned ………………………………………………………

$12,000

Expenses:

Equipment Rental Expense …………………………..

Salary Expense …………………………………………….

Total expenses …………………………………………….

Accounts Payable

1

0

0

00

0

0

0

00

2

0

0

0

00

Service Fees Earned

1

0

0

0

00

Gas & Oil Expense

8

0

0

00

Equipment Rental Expense

2

5

0

0

00

Salaries Expense

5

0

0

0

00

Totals

1

5

1

0

0

00

1

5

1

0

0

00

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

4.

Speedy Computer Service

Statement of Owner’s Equity

For the month ended March 31, 2017

Add: Investments

Total

Beginning Capital

$0

5.

Speedy Computer Service

Balance Sheet

March 31, 2017

Assets

Liabilities and Owner’s Equity

Accounts payable ………..

Accts Receivable ………….

Supplies ………………………

Total Assets …………………

6. First, note that the cash investment ($2,000) and cash withdrawal

($2,000) affect the cash balance but do not affect the amount of net