CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Prob. 16–5A (FIN MAN); Prob. 2–5A (MAN)

1.

Ginocera Inc.

Income Statement

For the Year Ended December 31, 20Y8

Sales

$ 17,920,000

Cost of goods sold

(10,864,000)

Gross profit

$ 7,056,000

Selling and administrative expenses:

Selling expenses:

Infomercial campaign

$2,000,000

Shipping expenses

Administrative expenses:

Operating income

Supporting calculations:

Sales: 1,120,000 units × $16 = $17,920,000

Cost of goods sold: 1,120,000 units × $9.70 = $10,864,000

Manufacturing cost per unit:

Direct materials:

Hardened steel blanks ………………………………. $4.00

Wood (for handle) …………………………………….. 1.50

Shipping expenses: 1,120,000 units × $0.20 = $224,000

2. Finished Goods balance, December 31, 20Y8:

(1,200,000 units – 1,120,000 units) × $9.70 = $776,000

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

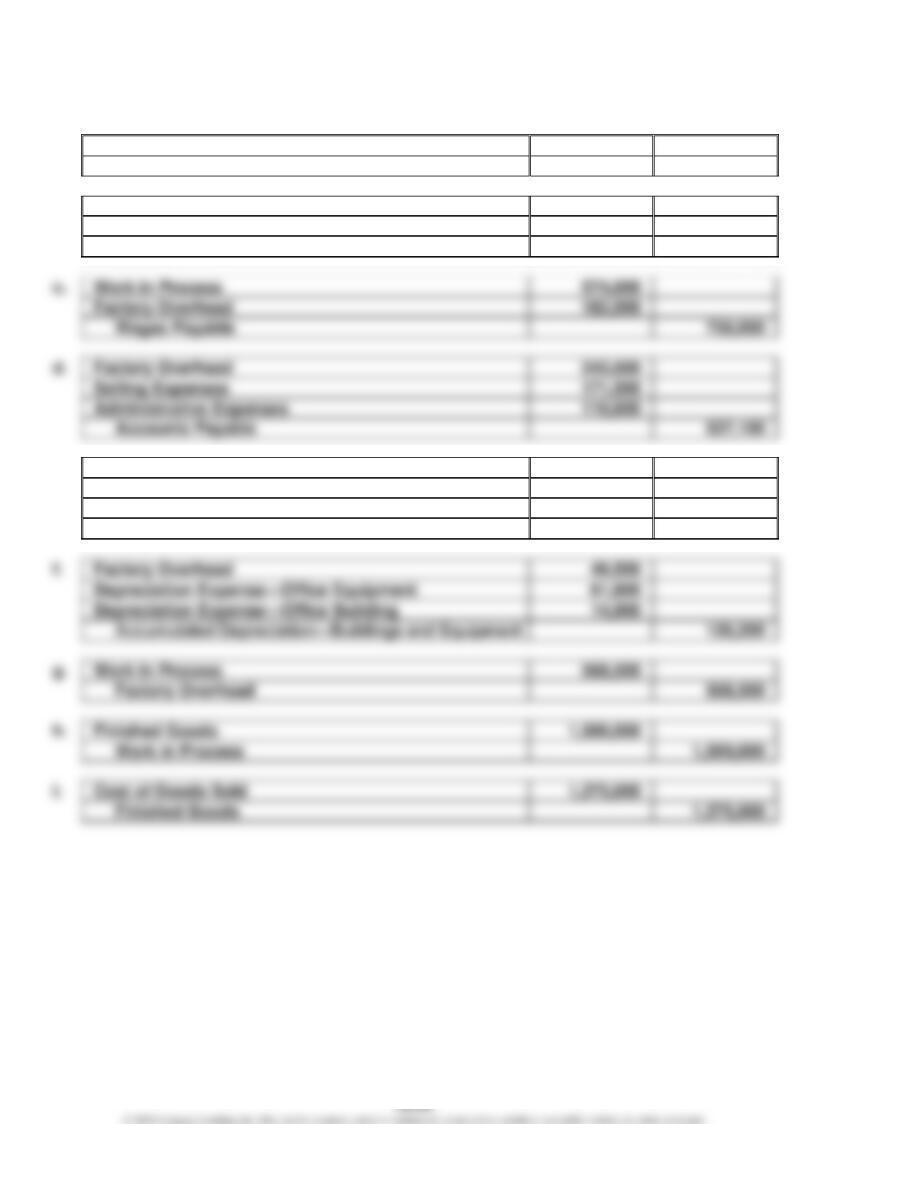

Prob. 16–1B (FIN MAN); Prob. 2–1B (MAN)

a.

Materials

770,000

Accounts Payable

770,000

b.

Work in Process

604,200

Factory Overhead

75,800

Materials

680,000

c.

Work in Process

574,000

Factory Overhead

182,000

Wages Payable

756,000

d.

Factory Overhead

245,000

Selling Expenses

171,500

Administrative Expenses

110,600

Accounts Payable

527,100

e.

Factory Overhead

24,500

Selling Expenses

28,420

Administrative Expenses

16,660

Prepaid Expenses

69,580

f.

Factory Overhead

49,500

Depreciation Expense—Office Equipment

61,800

Depreciation Expense—Office Building

14,900

126,200

Work in Process

568,500

Factory Overhead

568,500

Finished Goods

Work in Process

i.

Cost of Goods Sold

Finished Goods

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

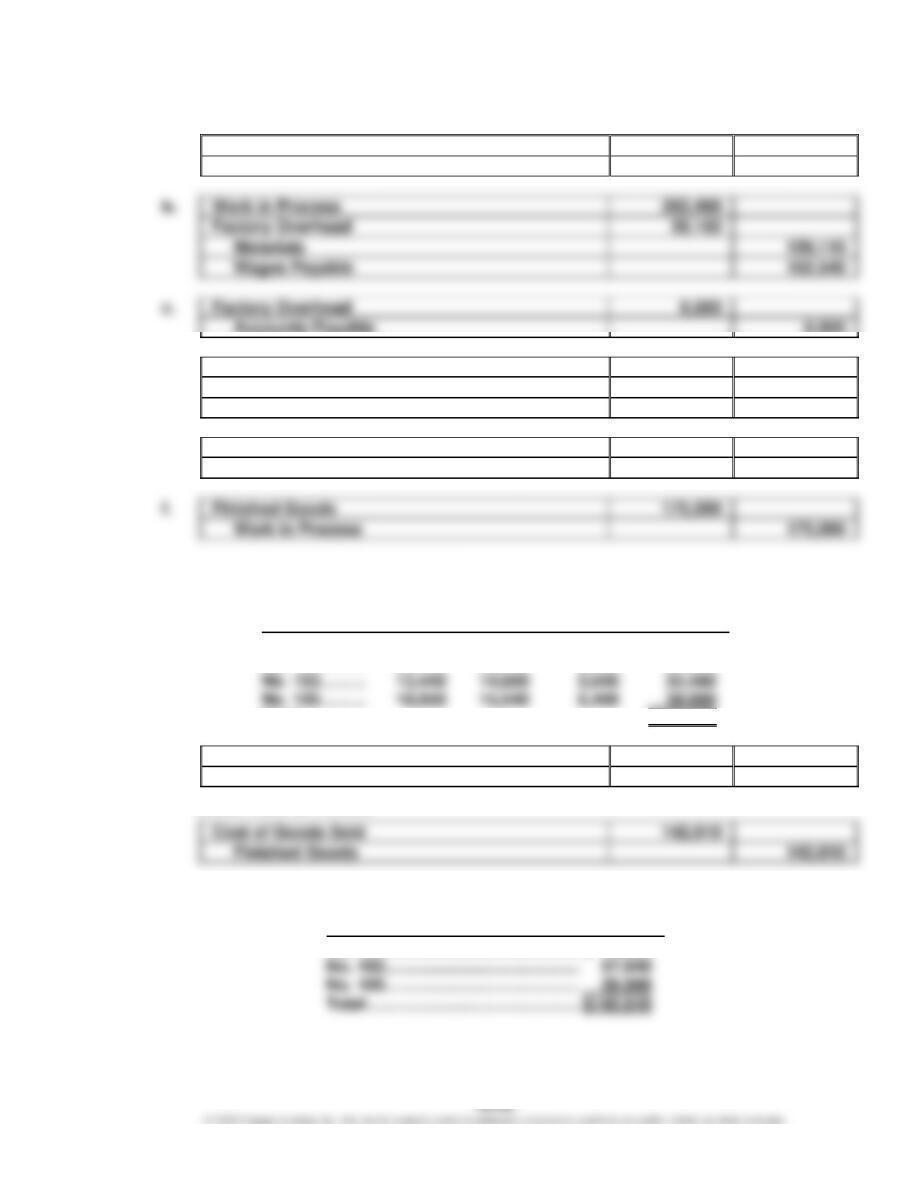

Prob. 16–2B (FIN MAN); Prob. 2–2B (MAN)

1.

a.

Materials

147,000

Accounts Payable

147,000

Work in Process

262,490

Factory Overhead

Materials

139,110

Wages Payable

152,540

c.

Factory Overhead

6,000

Accounts Payable

6,000

d.

Factory Overhead

4,100

Accumulated Depreciation—Machinery

and Equipment

4,100

e.

Work in Process

40,480

Factory Overhead (1,012 hours × $40)

40,480

Finished Goods

175,090

Work in Process

175,090

Computation of cost of jobs finished:

Job

Direct

Materials

Direct

Labor

Factory

Overhead

Total

No. 101……….

$19,320

$19,500

$6,160

$ 44,980

No. 102……….

23,100

28,140

6,400

57,640

No. 103……….

No. 105……….

18,050

15,540

6,400

Total …………………………………………………………….

$175,090

g.

Accounts Receivable

189,100

Sales*

189,100

* $62,900 + $80,700 + $45,500

Cost of Goods Sold

142,610

Finished Goods

142,610

Computation of cost of jobs sold:

Job

No. 101 ………………………………………………..

No. 102 ………………………………………………..

No. 105 ………………………………………………..

Total ……………………………………………………

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Prob. 16–2B (FIN MAN); Prob. 2–2B (MAN) (Concluded)

2.

Work in Process

Finished Goods

(b)

262,490

(f)

175,090

(f)

175,090

(g)

142,610

(e)

40,480

_________

__________

__________

Bal.

127,880

Bal.

32,480

3. Schedule of unfinished jobs:

No. 104

No. 106

Balance of Work in

4. Schedule of completed jobs:

Finished Goods, April 30

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

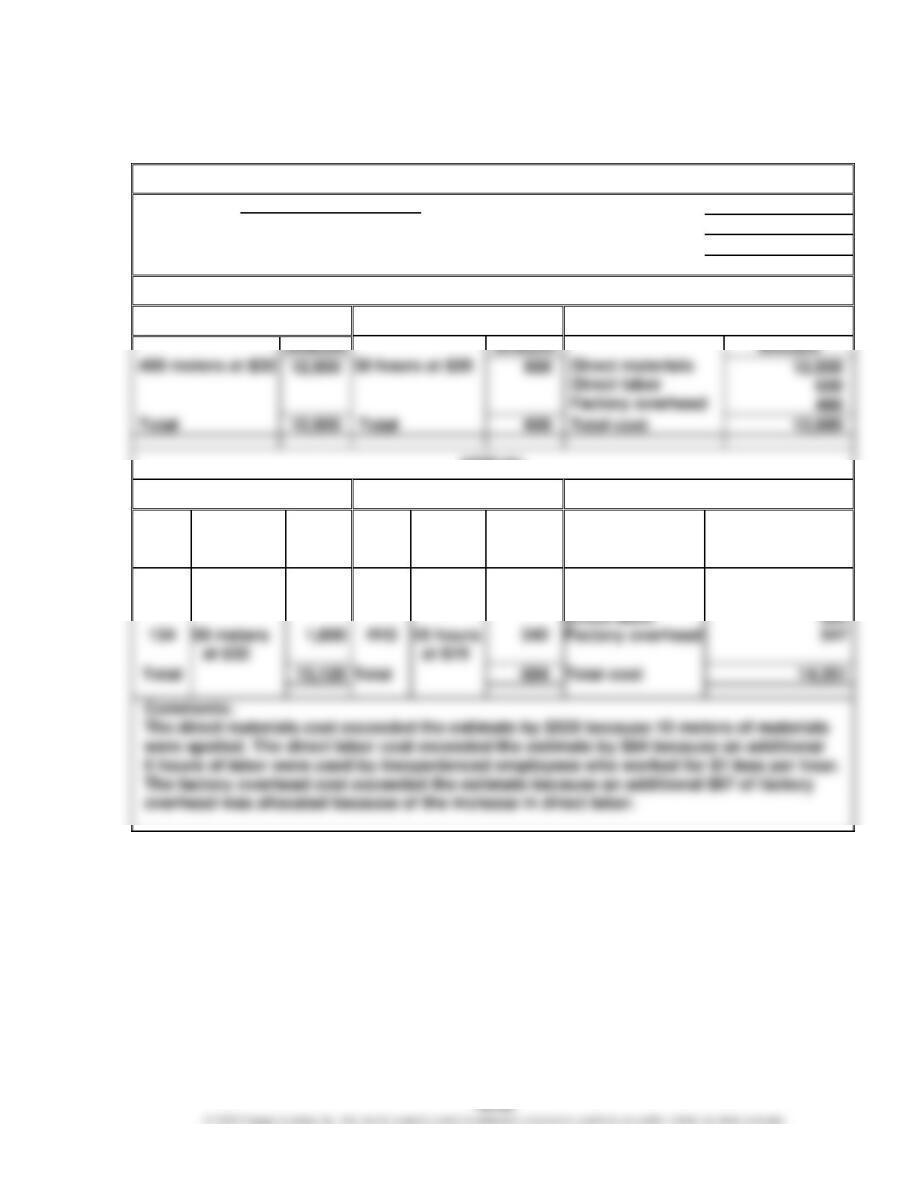

Prob. 16–3B (FIN MAN); Prob. 2–3B (MAN)

1. and 2.

JOB COST SHEET

Customer Lunden Consulting Date

Date wanted

Date completed

Job. No.

May 9

May 15

May 15

ESTIMATE

Direct Materials

Direct Labor

Summary

Amount

Total

Total

Total cost

ACTUAL

Direct Materials

Direct Labor

Summary

Mat.

Req.

No.

Description

Amount

Time

Ticket

No.

Descrip-

tion

Amount

Item

Amount

132

360 meters

at $32

11,520

H9

18 hours

at $19

342

Direct materials

13,120

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

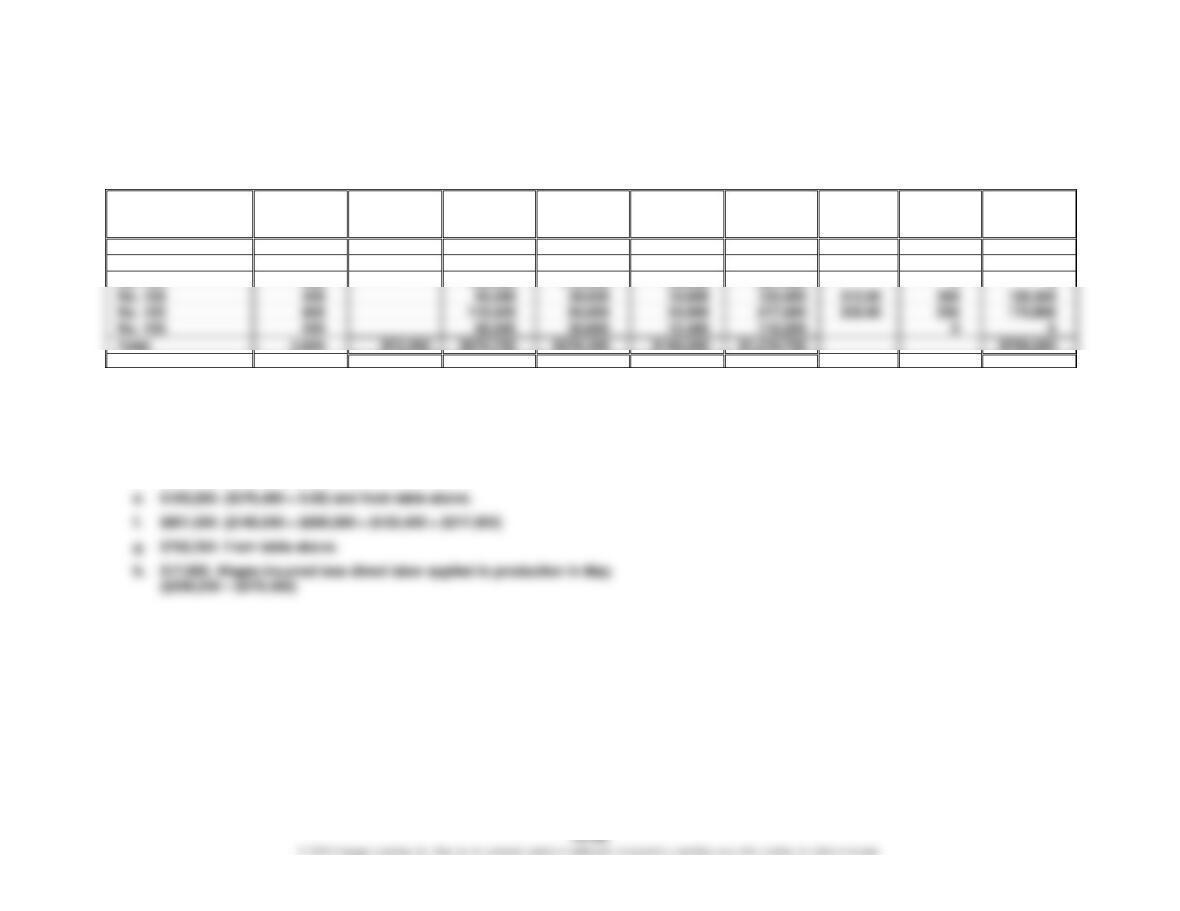

Prob. 16–4B (FIN MAN); Prob. 2–4B (MAN)

1. Supporting calculations:

Job. No.

Quantity

May 1

Work in

Process

Direct

Materials

Direct

Labor

Factory

Overhead

Total Cost

Unit

Cost

Units

Sold

Cost of

Goods

Sold

No. 101

330

$26,400

$ 82,500

$ 59,400

$ 29,700

$ 198,000

$600.00

264

$158,400

No. 102

380

46,000

105,400

72,600

36,300

260,300

685.00

360

246,600

No. 103

55,000

No. 104

400

66,000

39,600

19,800

125,400

384

120,384

No. 105

660

118,800

66,000

33,000

217,800

330.00

530

174,900

No. 106

330

66,000

30,800

15,400

112,200

Total

2,600

$72,400

$570,700

$378,400

$189,200

$1,210,700

$700,284

a. $586,100. Materials applied to production in May + indirect materials.

($570,700 + $15,400)

b. $72,400. From table above and problem.

c. $570,700. From table above.

d. $378,400. From table above.

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Prob. 16–4B (FIN MAN); Prob. 2–4B (MAN) (Concluded)

2. May 31 balances:

Materials ………………………… $ 19,500 ($105,600 + $500,000 – $586,100)

* $72,400 + $570,700 + $378,400 + $189,200 – $801,500 = $409,200

**

Job. No.

Units in

Inventory

Unit

Cost

Total

Cost

No. 101

66

$600.00

$ 39,600

No. 104

16

No. 105

Total

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Prob. 16–5B (FIN MAN); Prob. 2–5B (MAN)

1.

Technology Accessories Inc.

Income Statement

For the Year Ended December 31, 20Y3

Sales

$ 18,400,000

Cost of goods sold

(11,914,000)

Gross profit

$ 6,486,000

Selling expenses:

Operating income

Supporting calculations:

Sales: 460,000 units × $40 = $18,400,000

Cost of goods sold: 460,000 units × $25.90 = $11,914,000

Manufacturing cost per unit:

Direct materials:

Leather ………………………………………………………….. $10.00

* $1,250 ÷ 125 units per hour

Salespersons commissions: $18,400,000 × 20% = $3,680,000

2. Finished Goods balance, December 31, 20Y3:

(500,000 units – 460,000 units) × $25.90 = $1,036,000

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

MAKE A DECISION

MAD 16–1 (FIN MAN); MAD 2–1 (MAN)

a. Divide the total direct labor cost by the count to determine the direct labor cost per unit

for each job:

Total Direct

Labor Cost

Count

Direct Labor

Cost per

Sports Coat

Job 107

$ 63.00

10

$6.30

Job 125

14

7.00

b. The direct labor cost per sports coat increased over the first three jobs, then declined

with the last job. The increase for the first three jobs is not related to a change in the

c. The direct labor hours per sports coat is determined by dividing the total direct labor

hours by the count as follows:

Direct

Labor Hours

Count

Direct Labor

Hours per

Sports Coat

Job 107

4.50

10

0.45

Job 125

7.00

14

0.50

Job 192

3.20

0.40

than Job 107 and a significant improvement over Job 160.

MAD 16–2 (FIN MAN); MAD 2–2 (MAN)

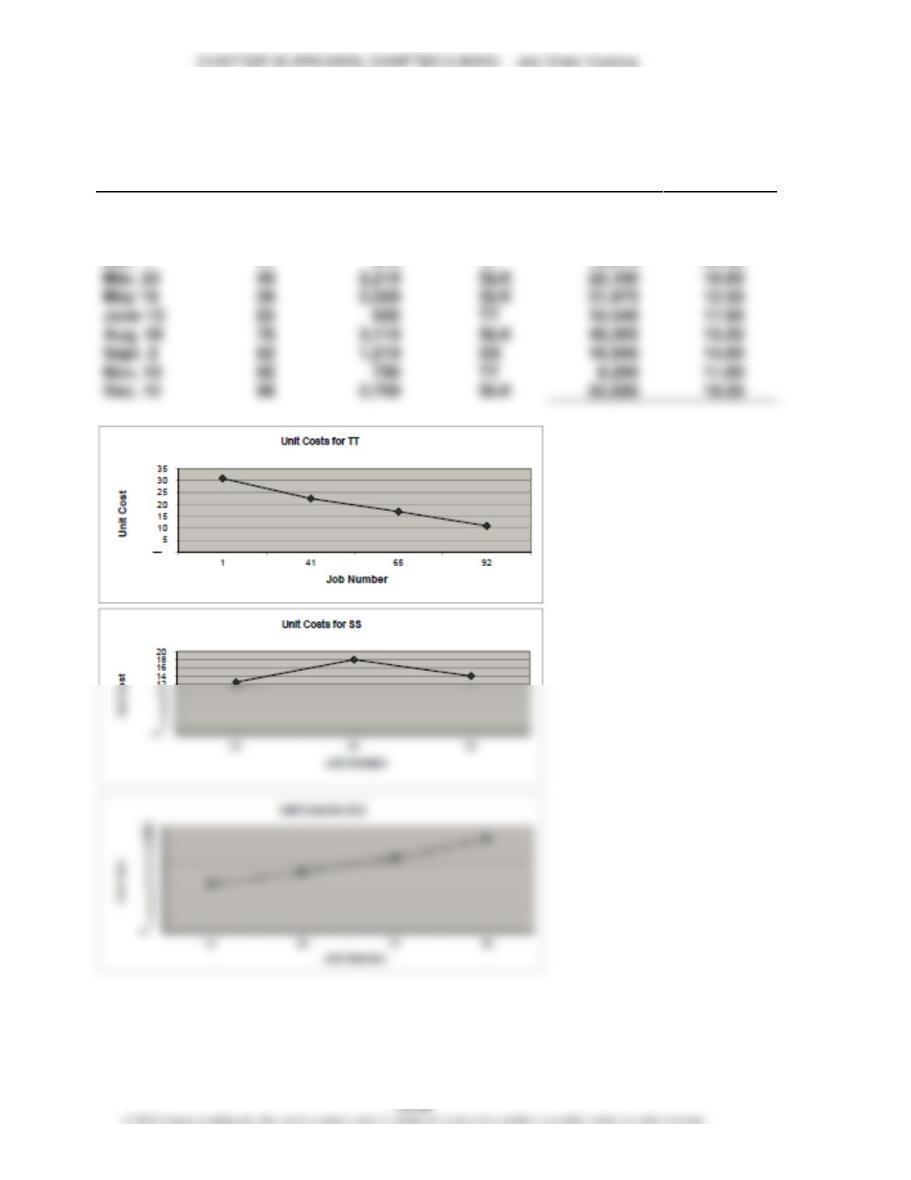

a.

Date

Job. No.

Quantity

Product

Amount

Unit

Cost

Jan. 2

1

520

TT

$16,120

$31.00

Jan. 15

22

1,610

SS

20,125

12.50

Feb. 3

30

1,420

SS

25,560

18.00

Mar. 7

41

15,075

22.50

Mar. 24

49

2,210

22,100

10.00

May 19

58

2,550

31,875

12.50

June 12

65

10,540

17.00

Aug. 18

78

3,110

48,205

15.50

Sept. 2

82

1,210

SS

16,940

14.00

Nov. 14

92

750

TT

8,250

11.00

Dec. 12

98

2,700

52,650

19.50

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

MAD 16–2 (FIN MAN); MAD 2–2 (MAN) (Concluded)

As can be seen, the unit costs behave differently for each product. SLK has

increasing unit costs during the year, SS is steady, and TT has decreasing unit

costs during the year.

b. Management should want to determine why SLK costs are increasing and why TT