CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

MAD 16–3 (FIN MAN); MAD 2–3 (MAN)

a. The first item to note is that the cost did not go up due to any increases in the cost of

labor or materials. Rather, the cost of the plaques increased because Job 105 used

more labor and materials per unit than did Job 101. Specifically, Job 101 required

exactly the same number of backboards and brass plates as the number of actual

plaques shipped. However, Job 105 required four more backboards and brass plates

than the number actually shipped (34 versus 30). This is illustrated as follows:

Job 101:

Materials

Walnut plaques:

Brass plates:

Actual units used 40 units

Expected units needed to produce 40 plaques 40 units

Difference 0 units

Labor

Engraving:

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

MAD 16–3 (FIN MAN); MAD 2–3 (MAN) (Concluded)

Job 105:

Materials

Walnut plaques:

Actual units used 34 units

Expected units needed to produce 30 plaques 30 units

Difference 4 units

Labor

Engraving:

Actual labor hours used 17 hours

Expected labor hours to produce 30 plaques

(30 units × 30 min. per unit) ÷ 60 min. per hour 15 hours

Difference 2 hours

Job 105’s 25.5 labor hours are 3.0 more (25.5 hrs. – 22.5 hrs.) than should have

been expected for a job of 30 plaques [(30 × 45 min.) ÷ 60 min. = 22.5 hrs.]. As a

result, the additional hours of labor cost, applied factory overhead, and direct

materials cost cause the unit cost of Job 105 to increase.

b. Apparently, the engraving and assembly work is becoming sloppy. Job 105

required 34 engraved brass plates in order to get 30 with acceptable quality. It is

likely that the engraver is not being careful in correctly spelling the names. The

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

MAD 16–4 (FIN MAN); MAD 2–4 (MAN)

a.

A

B

C

D

E

F

Job. No.

Date

Style

Count

Total Direct

Material Cost

Material Cost

per Unit

[Col. E ÷ Col. D]

Job 102

Jan. 20

Dining tables

20

$ 2,000

$100.00

Job 106

Jan. 20

Coffee tables

100

5,000

50.00

Job 107

Jan. 20

Chairs

50

1,250

25.00

Job 203

Apr. 21

Dining tables

20

2,020

101.00

Job 205

Apr. 21

Coffee tables

100

4,950

49.50

Job 206

Apr. 21

Chairs

52

1,295

24.90

Job 289

July 20

Dining tables

20

2,688

134.40

Job 294

July 20

Coffee tables

140

8,484

60.60

July 20

Chairs

60

1,872

31.20

Job 389

Dining tables

22

3,102

141.00

Job 391

Coffee tables

160

9,600

60.00

Job 392

Chairs

80

2,400

30.00

Job 570

Dec. 11

Dining tables

25

3,690

147.60

Job 573

Dec. 11

Coffee tables

180

11,016

61.20

Job 574

Dec. 11

Chairs

90

2,700

30.00

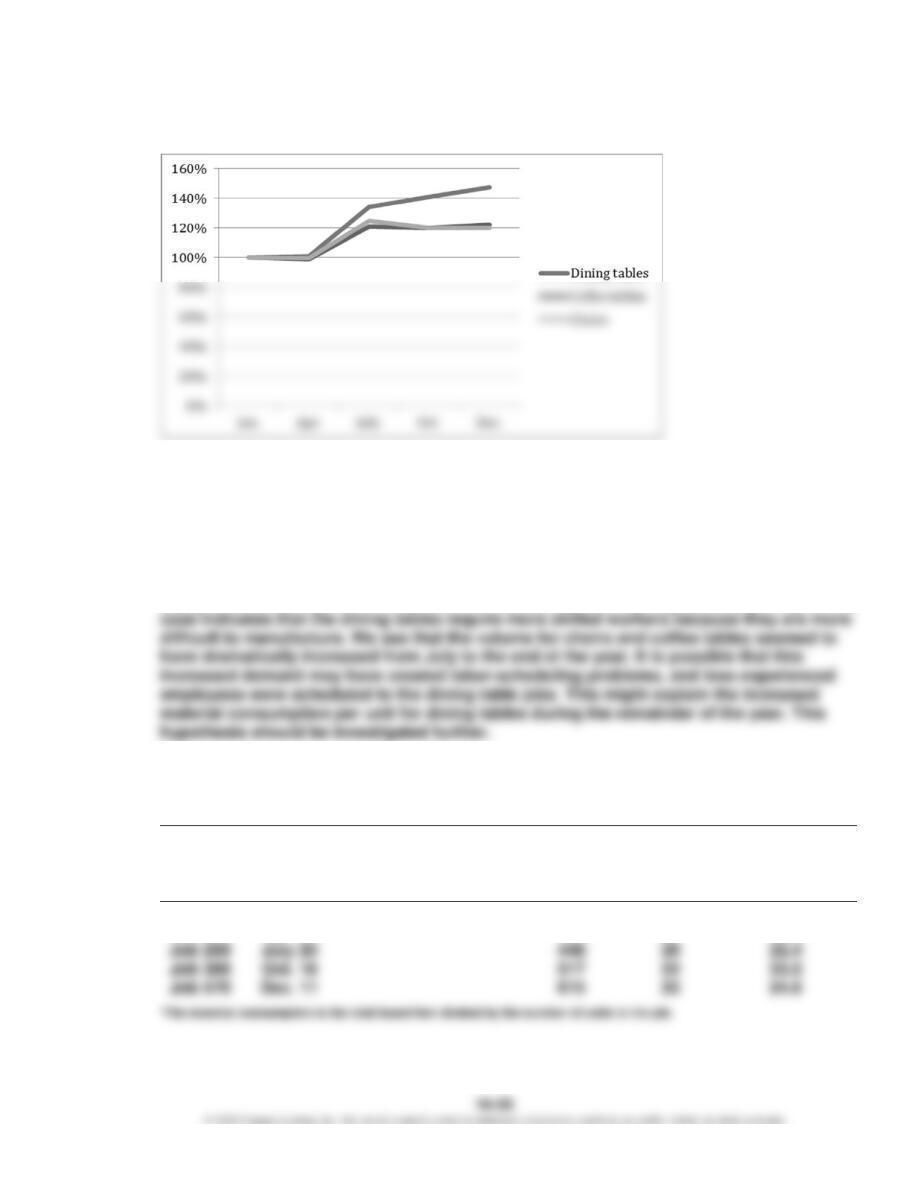

b.

Jan. Apr. July Oct. Dec.

Dining tables 100% 101.0% 134.4% 141.0% 147.6%

Coffee tables 100% 99.0% 121.2% 120.0% 122.4%

Chairs 100% 99.6% 124.8% 120.0% 120.0%

Dining tables:

Jan. $100 ÷ $100

Coffee tables:

Dec. $61.2 ÷ $50

Chairs:

Jan. $25 ÷ $25

Apr. $24.9 ÷ $25

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

MAD 16–4 (FIN MAN); MAD 2–4 (MAN) (Continued)

c.

d. The cost of all styles went up in July relative to the previous months because of the

change in the cost of the lumber from $5 per board foot to $6 per board foot. This may

have been unavoidable and merely a function of market conditions for oak lumber.

Regardless, the cause of the price increase should be investigated.

However, the material cost per unit for dining tables deviated to the high side relative to

the other two styles, beyond the increased cost of lumber. This must be the result of

using more lumber per unit in October and December, than during January and April. The

Note to Instructors: While not asked in the case specifically, the material consumption

pattern for dining tables is as follows:

Dining Tables

Job. No.

Date

Total Board

Feet

Units

Material

Consumption per

Unit (in board

feet)*

Job 102

Jan. 20

400

20

20.0

Job 203

Apr. 21

404

20

20.2

Job 289

July 20

448

20

22.4

Job 389

Oct. 18

517

22

23.5

Job 570

615

25

24.6

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

MAD 16–4 (FIN MAN); MAD 2–4 (MAN) (Concluded)

For comparison, the other two styles are as follows:

Coffee Tables

Job. No.

Date

Total Board

Feet

Units

Material

Consumption

per Unit (in

board feet)*

Job 106

Jan. 20

1,000

100

10.0

Job 205

Apr. 21

990

100

9.9

July 20

Job 391

Oct. 18

1,600

160

10.0

Dec. 11

Chairs

Job. No.

Date

Total Board

Feet

Units

Material

Consumption

per Unit (in

board feet)*

Job 107

250

Job 206

259

Job 392

400

*The material consumption is the total board feet divided by the number of units in the job.

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

TAKE IT FURTHER

TIF 16–1 (FIN MAN); TIF 2–1 (MAN)

No. Tandy’s plan is not ethical. A job order cost accounting system accumulates and

records product costs by jobs. The resulting total and unit product costs can be compared

TIF 16–2 (FIN MAN); TIF 2–2 (MAN)

a. Direct labor cost:

Total actual (applied) overhead, Years 1–5 ……………………… $ 4,200,000

Total direct labor cost, Years 1–5 …………………………………… 21,000,000

Machine cost:

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

TIF 16–2 (FIN MAN); TIF 2–2 (MAN) (Continued)

b.

Year 5

Year 4

Year 3

Direct Labor

Cost

Machine

Hours

Direct Labor

Cost

Machine

Hours

Direct Labor

Cost

Machine

Hours

Year 2

Year 1

Direct Labor

Cost

Machine

Hours

Direct Labor

Cost

Machine

Hours

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

TIF 16–2 (FIN MAN); TIF 2–2 (MAN) (Concluded)

c. The best predetermined overhead rate is machine hours. Although the total overhead

applied for each rate developed in part (a) is the same over the entire five-year period (as

a result of the method by which the predetermined overhead rates were developed), the

TIF 16–3 (FIN MAN); TIF 2–3 (MAN)

Memo

To: Carol Creedence

From: A+ Student

Re: Product CCR Job Cost

The graph of job costs for Product CCR indicates two significant trends in job cost. First,

there appears to be a strong and consistent “Friday effect.” Unit cost increases significantly

The Friday effect could be caused by a reduction in the efficiency of the workforce on

Fridays, as it is the last day of the work week. If this is the case and the trend is not product

The increasing trend in job costs is potentially more complicated. This could be caused by

any number of factors, including increased raw materials cost, decreased quality of raw

materials, or decreased labor efficiency. To evaluate these potential explanations,

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

TIF 16–4 (FIN MAN); TIF 2–4 (MAN)

a. The unit costs are influenced by both the price and quantity of inputs. On the price side,

Input Quantity per Unit

Job 206

Job 228

Steel input

2.10

tons1

2.60

tons2

Foundry labor

8.00

hours3

10.00

hours4

Welding labor

11.00

hours5

14.00

hours6

1 105 tons ÷ 50 units

These numbers were determined by dividing the total input quantities by the number of

units produced to discover the inputs per unit. The inputs for the components were

unchanged between the two jobs.

b. A possible reason for this deterioration in performance is related to the purchasing

manager’s decision to change vendors in order to secure a lower price per ton. The new

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

TIF 16–5 (FIN MAN); TIF 2–5 (MAN)

a. Todd should record the debits for factory wages as a debit to Work in Process. The

factory wages are product costs that must be accumulated in the cost of producing

the product. Eventually, these wage costs will become part of the finished goods

b. Jeff would not be concerned about expensing administrative wages and depreciation

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. b. Baldwin’s annual budgeted overhead is $600,000, computed as follows:

2. b. Total overhead applied to Job 231 is $303, computed as follows:

Tooling overhead per hour: $8,625 ÷ 460 hours = $18.75

Fabricating overhead per hour: $16,120 ÷ 620 hours = $26.00

Job 231 overhead: ($18.75 × 12) + ($26.00 × 3) = $303.00

3. c. The unit costs for Job ICU2 would consist of direct materials, direct labor, and

applied overhead per unit.

4. d. The overhead applied to a job incurring 20 direct labor hours would be $140,

computed as follows: