CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN)

JOB ORDER COSTING

DISCUSSION QUESTIONS

1. a. Job order cost system and process cost system.

b. The job order cost system provides a separate record of each quantity of product that passes

through the factory.

c. Process cost systems accumulate costs for each department or process within a factory.

4. a. Purchase invoice or receiving report

b. Materials requisition

5. A job cost sheet is the subsidiary ledger to the work in process control account. The cost of materials,

labor, and overhead are listed on each separate job cost sheet for each job. A summary of all the job

cost sheets during an accounting period is the basis for journal entries to the control accounts.

8. a. The predetermined factory overhead rate is determined by dividing the estimated total factory

overhead costs for the forthcoming year by an estimated activity base, one that reflects the

consumption or use of factory overhead costs.

b. Direct labor cost, direct labor hours, and machine hours.

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

DISCUSSION QUESTIONS (Continued)

10. Job order cost accumulation would be most appropriate for professional service firms that provide

extended, project-type services for clients. Examples would be architectural, consulting, advertising,

or legal services. Job cost sheets would accumulate all direct costs of servicing the client. Such costs

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

BASIC EXERCISES

BE 16–1 (FIN MAN); BE 2–1 (MAN)

May

7

Materials

80,000

Accounts Payable

80,000

May

67,400

BE 16–2 (FIN MAN); BE 2–2 (MAN)

Work in Process*

142,000

Wages Payable

142,000

BE 16–3 (FIN MAN); BE 2–3 (MAN)

Factory Overhead

29,200

Materials

8,800

Accumulated Depreciation—Factory

9,000

BE 16–4 (FIN MAN); BE 2–4 (MAN)

a. $7.75 per direct labor hour = $620,000 ÷ 80,000 direct labor hours

c.

Work in Process

42,625

Factory Overhead

42,625

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

BE 16–5 (FIN MAN); BE 2–5 (MAN)

a.

Job 200

Job 305

Direct materials ………………………………………………………………….

$ 60,000

$ 7,400

Direct labor ………………………………………………………………………..

70,000

72,000

Factory overhead ………………………………………………………………..

19,375

23,250

Total costs …………………………………………………………………..

$102,650

Job 200

$62.50 = $149,375 ÷ 2,390 units

Job 305

$50.00 = $102,650 ÷ 2,053 units

BE 16–6 (FIN MAN); BE 2–6 (MAN)

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

EXERCISES

Ex. 16–1 (FIN MAN); Ex. 2–1 (MAN)

a. Materials requisitioned for use (both direct and indirect)

Ex. 16–2 (FIN MAN); Ex. 2–2 (MAN)

a. Cost of goods sold:

Sales ……………………………………………………………………………. $12,375,000

b. Direct materials cost:

Materials purchased ……………………………………………………… $4,125,000

c. Direct labor cost:

Total manufacturing costs for the period ……………………….. $ 7,880,000

Less: Direct materials cost …………………………………………. $3,655,000

Factory overhead* …………………………………………….. 1,400,000 (5,055,000)

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–3 (FIN MAN); Ex. 2–3 (MAN)

a.

RECEIVED

ISSUED

BALANCE

Receiving

Report

Number

Quantity

Unit Price

Materials

Requisition

Number

Quantity

Amount

Date

Quantity

Unit

Price

Amount

May 1

285

$30.00

$8,550

40

130

$32

May 4

285

$30.00

8,550

4,160

44

110

May 21

$32.00

1,600

110

$38.00

4,180

2,280

* May 10 issuance

285 at $30.00

$ 8,550

80 at $32.00

2,560

$11,110

50 at $38.00

$ 3,500

b. Ending inventory balance:

60 at $38.00 ………………………………………………………………………………. $2,280

c.

Work in Process ($11,110 + $3,500)

14,610

Materials

14,610

Ex. 16–4 (FIN MAN); Ex. 2–4 (MAN)

Factory Overhead

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–5 (FIN MAN); Ex. 2–5 (MAN)

a.

Materials*

1,770,000

Accounts Payable

1,770,000

* $820,000 + $315,000 + $555,000 + $80,000

b.

Work in Process*

1,664,000

Factory Overhead

Materials

1,747,600

c.

Fabric

Polyester

Filling

Lumber

Glue

Balance, April 1 …………………………….

$ 58,300

$ 30,000

$ 58,800

$ 9,950

April purchases …………………………….

April requisitions …………………………..

(810,000)

(83,600)

Balance, April 30…………………………..

Ex. 16–6 (FIN MAN); Ex. 2–6 (MAN)

Work in Process

85,755

Factory Overhead

8,220

Wages Payable

93,975

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–7 (FIN MAN); Ex. 2–7 (MAN)

a.

Work in Process

Supporting calculations:

Labor Costs (Hourly Rate × Hours)

Hourly

Rate

Job

301

Job

302

Job

303

Direct Labor

(sum of job

costs)

Indirect

Labor

David Clancy ……………….

Jose Cano ……………………

1,092

$3,676

$164

b. The direct labor costs for the completed jobs would become part of the finished goods

inventory. The direct labor costs for Job 303 would remain part of the work in process

inventory.

Ex. 16–8 (FIN MAN); Ex. 2–8 (MAN)

a.

Work in Process

47,792

Factory Overhead

12,500

60,292

b.

Work in Process

37,904

Factory Overhead

37,904

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–9 (FIN MAN); Ex. 2–9 (MAN)

a. Factory 1: $14.80 per machine hour ($18,500,000 ÷ 1,250,000 machine hours)

Factory Overhead

1,554,000

($14.80 × 105,000).

Factory 2:

Work in Process

3,547,500

Factory Overhead

3,547,500

($55.00 × 64,500).

d. Factory 1—$38,200 credit (overapplied) ($1,515,800 – $1,554,000)

Factory 2—$58,800 debit (underapplied) ($3,606,300 – $3,547,500)

Ex. 16–10 (FIN MAN); Ex. 2–10 (MAN)

The estimated shop overhead is determined as follows:

Shop and repair equipment depreciation ……………………………………….. $ 62,500

The engine parts and shop labor are direct to the jobs and are not included in the shop

overhead rate. The advertising and administrative expenses are selling and administrative

expenses that are not included in the shop overhead but are treated as period expenses.

The estimated activity base is determined by dividing the shop direct labor cost by the direct

labor rate, as follows:

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–11 (FIN MAN); Ex. 2–11 (MAN)

a. Estimated annual operating room overhead: $812,000

Estimated operating room activity base, number of operating room hours:

Predetermined surgical overhead rate:

$812,000 $290 per hour

2,800 hours =

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–12 (FIN MAN); Ex. 2–12 (MAN)

a.

Finished Goods*

560,240

Work in Process

560,240

* $182,500 + $78,300 + $232,190 + $67,250

b.

Work in process inventory, January 1 ……………………………….

Direct labor ……………………………………………………………………..

Factory overhead …………………………………………………………….

Total manufacturing costs………………………………………………..

Jobs finished during January …………………………………………..

Work in process inventory, January 31 ……………………………..

$ 85,800

Ex. 16–13 (FIN MAN); Ex. 2–13 (MAN)

a.

Work in Process

55,500

Factory Overhead

4,500

Materials

60,000

Work in Process

106,800

Factory Overhead

8,200

Wages Payable

115,000

c.

Work in Process

26,700

Factory Overhead

26,700*

Predetermined overhead rate:

Job 301: $7,750 ÷ $31,000 = 25% or

Job 302: $10,550 ÷ $42,200 = 25%

Finished Goods*

122,750

Work in Process

122,750

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–14 (FIN MAN); Ex. 2–14 (MAN)

a.

Rushmore Biking Inc.

Income Statement

For the Month Ended February 28

Revenues

$ 910,000

Cost of goods sold

(550,000)

Gross profit

$ 360,000

Total selling and administrative expenses

(275,000)

Operating income

$ 85,000

b. Materials inventory:

Work in process inventory:

Materials used in production ………………………………………………………….. $ 434,500

Finished goods inventory:

Transferred to finished goods…………………………………………………………. $ 578,000

Less: Cost of goods sold ……………………………………………………………….. (550,000)

Finished goods inventory, February 28 ……………………………………………. $ 28,000

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

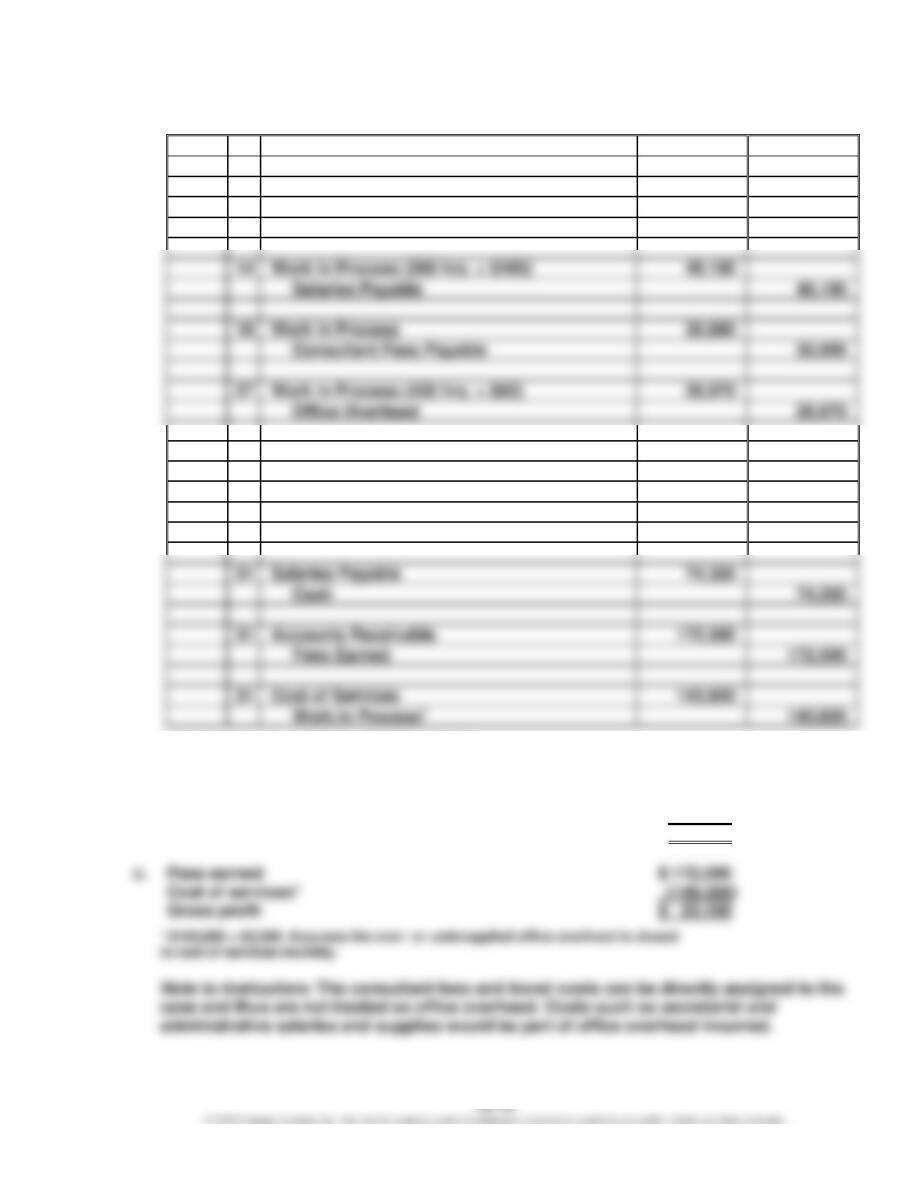

Ex. 16–15 (FIN MAN); Ex. 2–15 (MAN)

a.

July

3

Work in Process (175 hrs. × $150)

26,250

Salaries Payable

26,250

10

Work in Process

12,500

Cash

12,500

14

Work in Process (260 hrs. × $185)

48,100

48,100

18

Work in Process

30,000

30,000

27

Work in Process (435 hrs. × $62)

26,970

Office Overhead

26,970

31

Office Overhead

28,500

Cash

28,500

31

Office Overhead

4,000

Supplies

4,000

31

Salaries Payable

74,350

74,350

31

Accounts Receivable

31

Cost of Services

Work in Process*

* $26,250 + $12,500 + $48,100 + $30,000 + $26,970

b.

Office overhead incurred ($28,500 + $4,000)

$ 32,500

Office overhead applied

(26,970)

Underapplied overhead

$ 5,530

Fees earned

Cost of services*

Gross profit

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Ex. 16–16 (FIN MAN); Ex. 2–16 (MAN)

a.

Work in Process

1,068,000

Salaries Payable

1,068,000

Work in Process

2,130,000

Accounts Payable

2,130,000

Work in Process (65% × $2,130,000)

1,384,500

Agency Overhead

1,384,500

d.

Cost of Services

2,827,750

Work in Process

2,827,750

Cost of completed jobs, $2,827,750:

Vault

Bank

Take Off

Airlines

August 1 balance ………………………………………………..

$ 270,000

$ 80,000

625,000

Total costs ………………………………………………………….

$1,631,500

$1,196,250

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

PROBLEMS

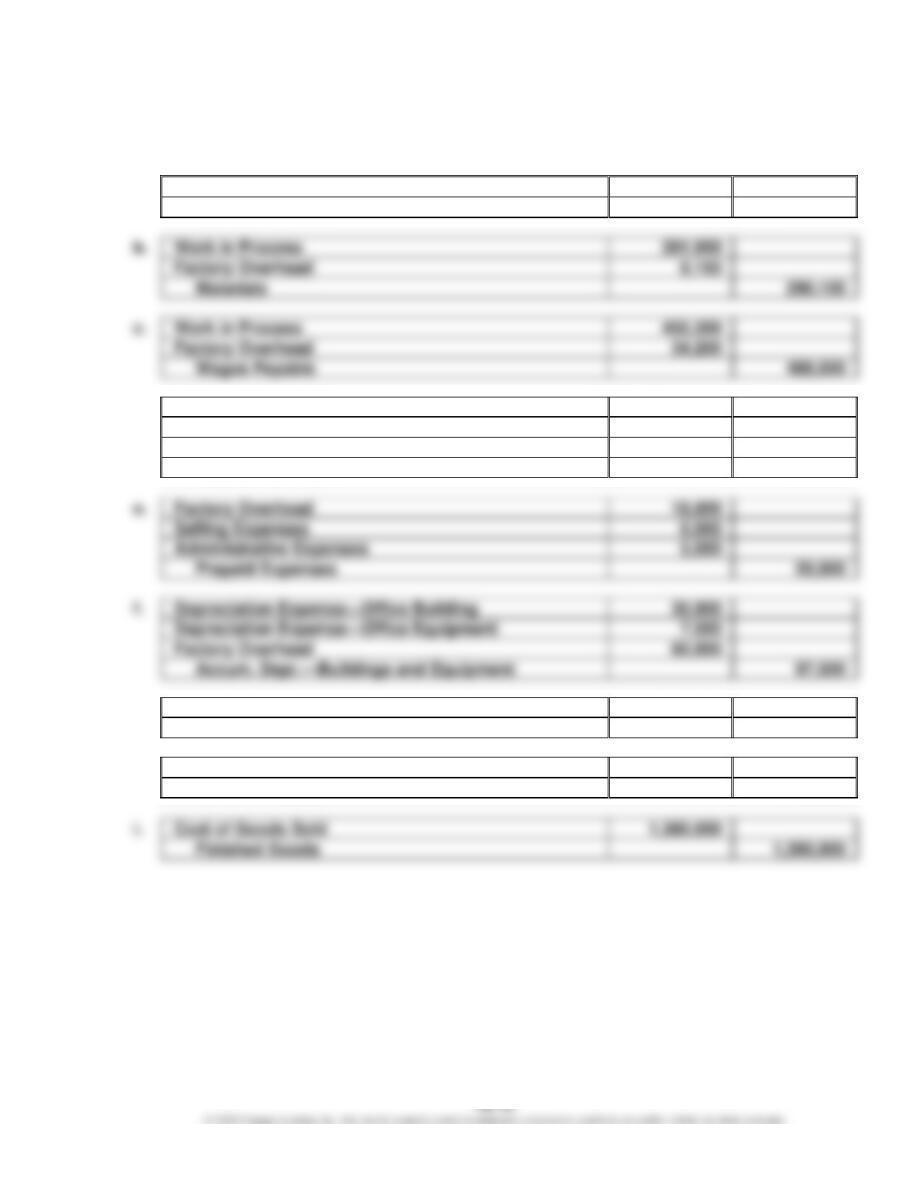

Prob. 16–1A (FIN MAN); Prob. 2–1A (MAN)

a.

Materials

315,500

Accounts Payable

315,500

b.

Work in Process

281,950

Factory Overhead

Materials

290,100

c.

Work in Process

455,300

Factory Overhead

Wages Payable

489,500

d.

Factory Overhead

600,000

Selling Expenses

150,000

Administrative Expenses

100,000

Accounts Payable

850,000

e.

Factory Overhead

Selling Expenses

Administrative Expenses

Prepaid Expenses

Depreciation Expense—Office Equipment

Factory Overhead

Accum. Depr.—Buildings and Equipment

g.

Work in Process

711,660

Factory Overhead

711,660

h.

Finished Goods

1,425,000

Work in Process

1,425,000

i.

Cost of Goods Sold

1,380,000

Finished Goods

1,380,000

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

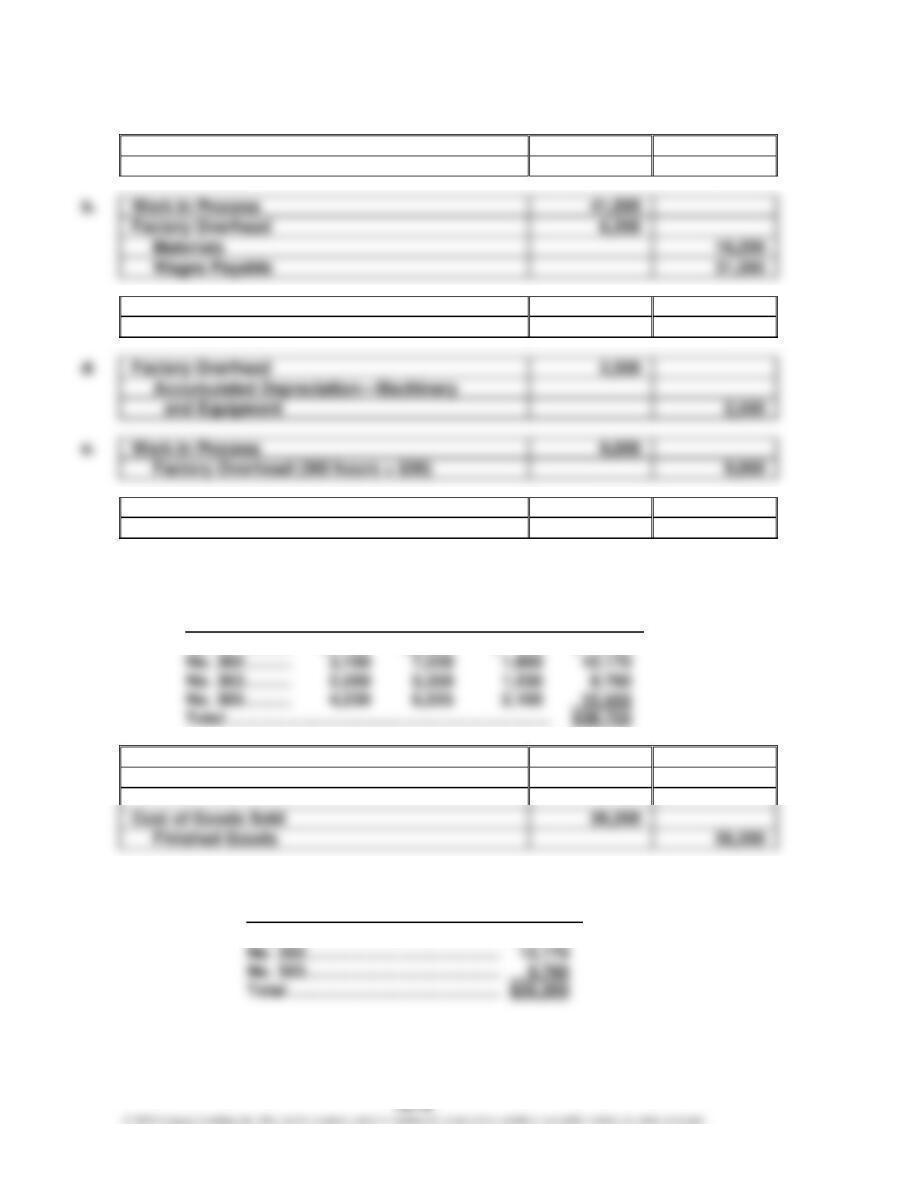

Prob. 16–2A (FIN MAN); Prob. 2–2A (MAN)

1.

a.

Materials

45,000

Accounts Payable

45,000

Work in Process

41,595

Factory Overhead

Materials

16,200

Wages Payable

31,595

c.

Factory Overhead

1,800

Accounts Payable

1,800

d.

Factory Overhead

2,500

Accumulated Depreciation—Machinery

2,500

e.

Work in Process

9,000

Factory Overhead (300 hours × $30)

9,000

f.

Finished Goods

38,755

Work in Process

38,755

Computation of cost of jobs finished:

Job

Direct

Materials

Direct

Labor

Factory

Overhead

Total

No. 301 ……….

$1,850

$2,500

$ 900

$ 5,250

No. 302 ……….

No. 303 ……….

No. 305 ……….

12,555

Total …………………………………………………………….

$38,755

g.

Accounts Receivable

38,050

Sales

38,050

Cost of Goods Sold

26,200

Finished Goods

26,200

Computation of cost of jobs sold:

Job

No. 301 ………………………………………………..

$ 5,250

No. 302 ………………………………………………..

No. 303 ………………………………………………..

8,780

Total ……………………………………………………

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Prob. 16–2A (FIN MAN); Prob. 2–2A (MAN) (Concluded)

2.

Work in Process

Finished Goods

(b)

41,595

(f)

38,755

(f)

38,755

(g)

26,200

(e)

9,000

_________

__________

__________

Bal.

11,840

Bal.

12,555

3. Schedule of unfinished jobs:

No. 304

$ 6,090

No. 306

Balance of Work in

4. Schedule of completed jobs:

Finished Goods, March 31

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

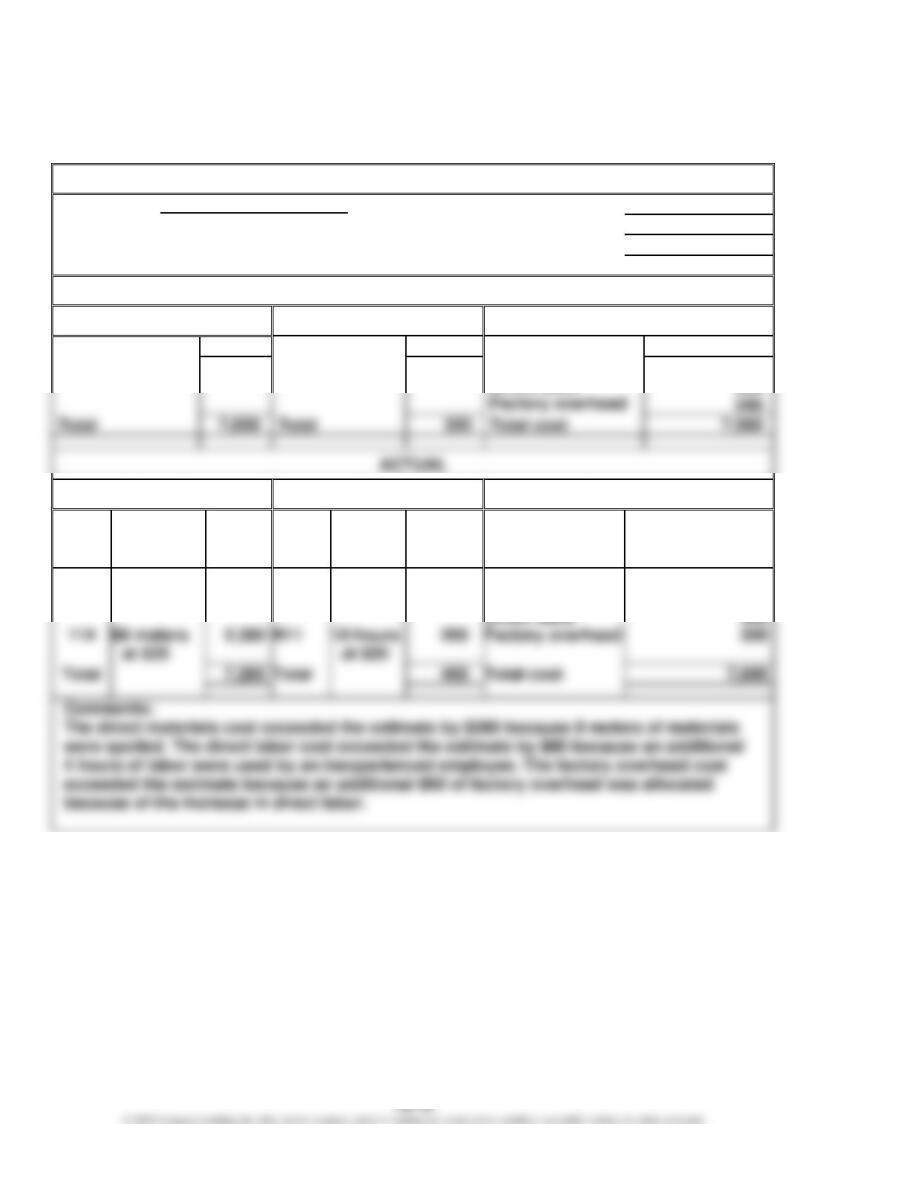

Prob. 16–3A (FIN MAN); Prob. 2–3A (MAN)

1. and 2.

JOB COST SHEET

Customer Jackson Consulting Date

Date wanted

Date completed

Job. No.

October 1

October 10

October 10

ESTIMATE

Direct Materials

Direct Labor

Summary

200 meters at $35

Amount

16 hours at $20

Amount

Direct materials

Total

Total

Total cost

Amount

7,000

320

7,000

Direct Materials

Direct Labor

Summary

Mat.

Req.

No.

Description

Amount

Time

Ticket

No.

Descrip-

tion

Amount

Item

Amount

112

140 meters

at $35

4,900

H10

10 hours

at $20

200

Direct materials

7,280

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

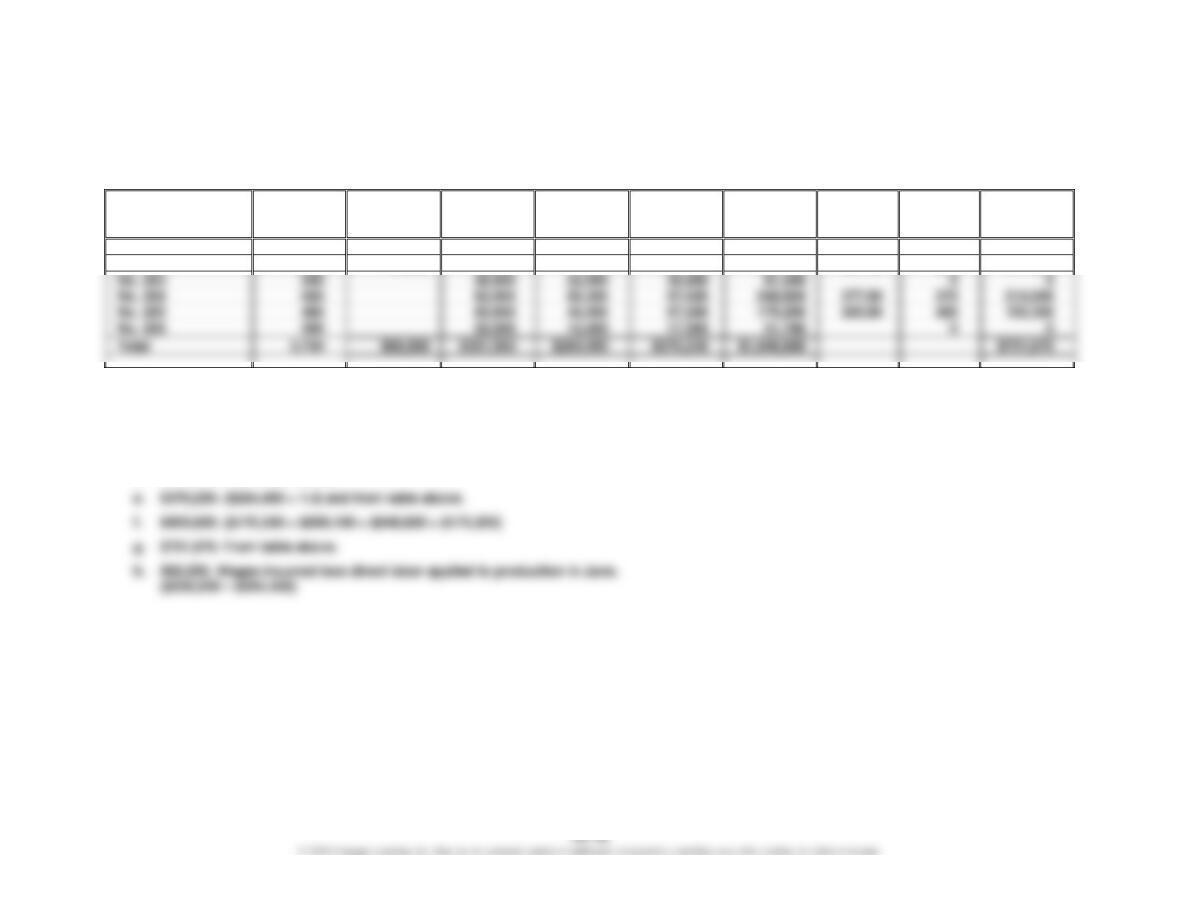

Prob. 16–4A (FIN MAN); Prob. 2–4A (MAN)

1. Supporting calculations:

Job. No.

Quantity

June 1

Work in

Process

Direct

Materials

Direct

Labor

Factory

Overhead

Total Cost

Unit

Cost

Units

Sold

Cost of

Goods

Sold

No. 201

550

$16,500

$ 55,000

$ 41,250

$ 57,750

$ 170,500

$310.00

440

$136,400

No. 202

1,100

44,000

93,500

71,500

100,100

309,100

281.00

880

247,280

No. 204

660

82,500

69,300

97,020

248,820

377.00

570

214,890

No. 205

480

60,000

48,000

67,200

175,200

365.00

420

153,300

No. 206

380

22,000

12,400

17,360

51,760

a. $395,500. Materials applied to production in June + indirect materials.

($351,500 + $44,000)

b. $60,500. From table above and problem.

c. $351,500. From table above.

d. $264,450. From table above.

CHAPTER 16 (FIN MAN); CHAPTER 2 (MAN) Job Order Costing

Prob. 16–4A (FIN MAN); Prob. 2–4A (MAN) (Concluded)

2. June 30 balances:

Materials …………………….. $ 17,000 ($82,500 + $330,000 – $395,500)

$237,500 – $370,230)

* $60,500 + $351,500 + $264,450 + $370,230 – $903,620 = $143,060

**

Job. No.

Units in

Inventory

Unit

Cost

Total

Cost