Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 2

SOLUTIONS TO EXERCISES—SET B

EXERCISE 2-1B

CL

Accounts payable

CA

Inventory

CA

Accounts receivable

LTI

Investments

EXERCISE 2-2B

CA

Prepaid rent

IA

Patents

PPE

Equipment

LTL

Bonds payable

EXERCISE 2-3B

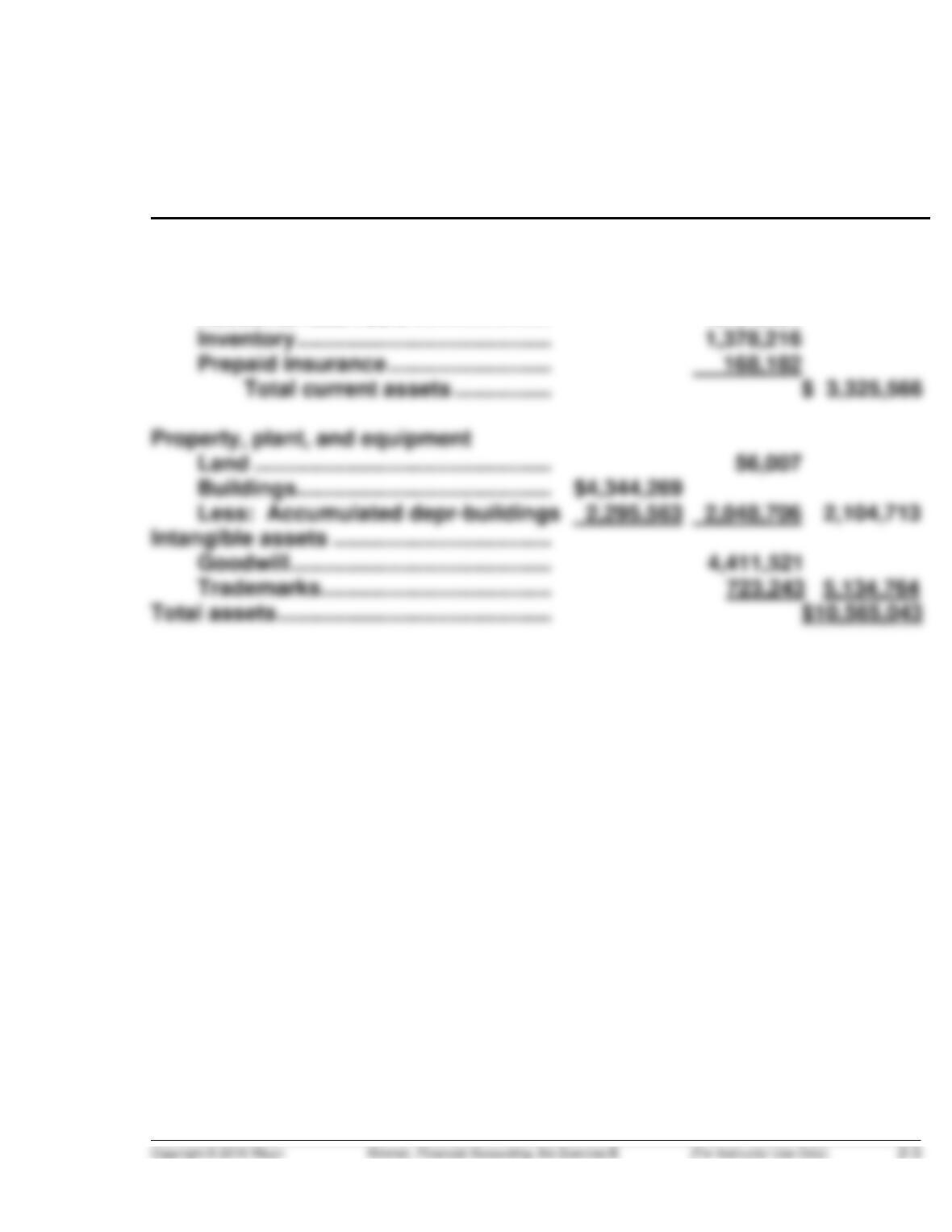

BOEING COMPANY

Partial Balance Sheet

December 31, 2014

(in millions)

Assets

Current assets

Cash ....................................................................... $ 7,042

Debt investments .................................................. 2,266

Accounts receivable ............................................. 5,740

EXERCISE 2-4B

H. J. HEINZ COMPANY

Partial Balance Sheet

April 30, 2014

(in thousands)

Assets

Current assets

Cash ................................................. $ 617,687

Accounts receivable ....................... 1,161,481

EXERCISE 2-5B

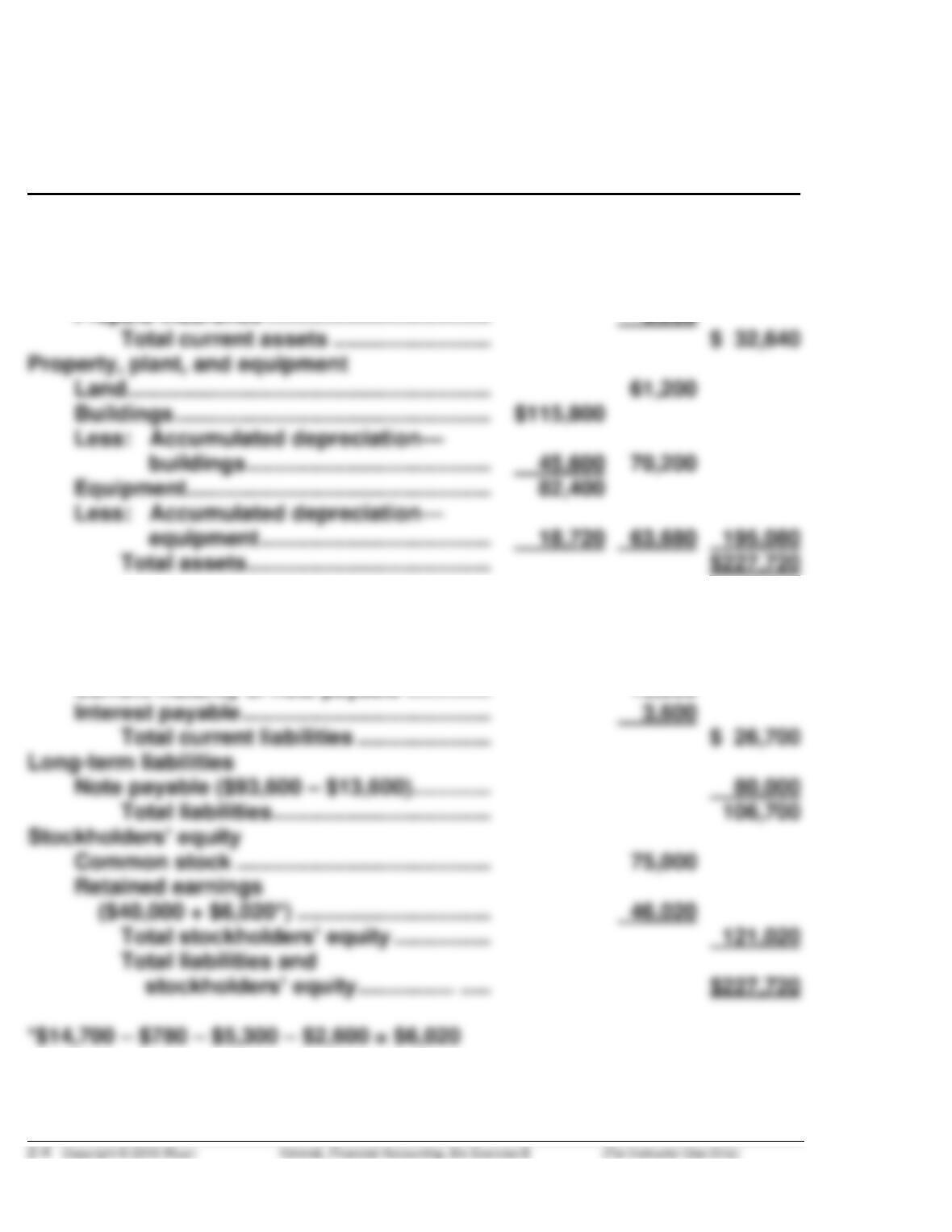

TROTTER COMPANY

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ........................................................... $18,840

Accounts receivable ................................. 10,600

Prepaid insurance ..................................... 3,200

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ..................................... $ 9,500

Current maturity of note payable .............. 13,600

EXERCISE 2-6B

TEXAS INSTRUMENTS, INC.

Balance Sheet

December 31, 2014

(in millions)

Assets

Current assets

Cash ........................................................................... $ 1,328

Debt investments ...................................................... 1,596

Total current assets .......................................... $ 6,918

Long-term investments

Stock investments .................................................... 267

Property, plant, and equipment

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ..................................................... $1,368

Income taxes payable ............................................... 657

EXERCISE 2-7B

(a) Earnings (loss) per share =

Net income Preferred dividends

Average common shares outstanding

—

(b) Using net loss as a basis to evaluate profitability, Callaway Company’s

(c) To determine earnings (loss) per share, dividends on preferred stock

EXERCISE 2-8B

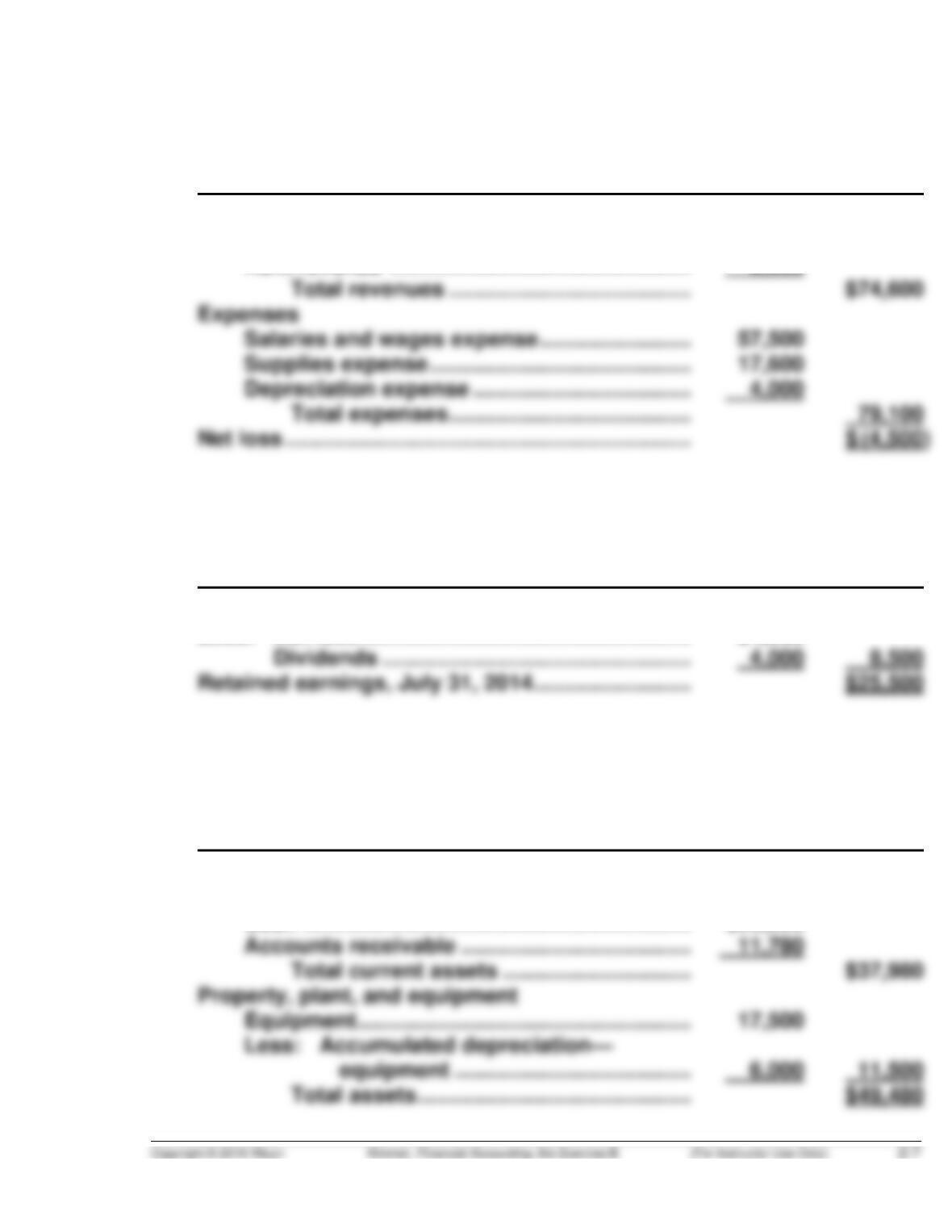

(a) WI-HAUL CORPORATION

Income Statement

For the Year Ended July 31, 2014

Revenues

Service revenue .............................................. $66,100

Rent revenue .................................................. 8,500

WI-HAUL CORPORATION

Retained Earnings Statement

For the Year Ended July 31, 2014

Retained earnings, August 1, 2013 ...................... $34,000

Less: Net loss ...................................................... $4,500

(b) WI-HAUL CORPORATION

Balance Sheet

July 31, 2014

Assets

Current assets

Cash ................................................................ $26,200

EXERCISE 2-8B (Continued)

(b) WI-HAUL CORPORATION

Balance Sheet (Continued)

July 31, 2014

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ................................................ $ 4,100

Salaries and wages payable ............................... 2,080

Total current liabilities ................................... $ 6,180

Long-term liabilities

(c)

$37,980

Current ratio = = 6.1:1

$6,180

(d) The current ratio would not change because equipment is not a

current asset and a 5-year note payable is a long-term liability rather

than a current liability.

The debt to assets ratio would increase from 16.1% to 40.3%*.

Looking solely at the debt to assets ratio, I would favor making the

sale because Wi-Haul’s debt to assets ratio of 16.1% is very low.

Looking at additional financial data, I would note that Wi-Haul

EXERCISE 2-9B

(a)

Beginning of Year

End of Year

Working capital

$2,742 – $1,433 = $1,309

$3,361 – $1,635 = $1,726

(b) Nordstrom’s liquidity increased during the year. Its current ratio in-

creased from 1.91:1 to 2.06:1. Also, Nordstrom’s working capital

increased by $417,000,000.

EXERCISE 2-10B

(a)

Current ratio =$60,000

$30,000 = 2.0: 1

(c) Liquidity measures indicate a company’s ability to pay current obliga-

tions as they become due. Satisfaction of current obligations usually

requires the use of current assets.

EXERCISE 2-10B (Continued)

Payment of current obligations frequently requires cash. Neither

working capital nor the current ratio indicate the composition of

current assets. If a company’s current assets are largely comprised of

items such as inventory and prepaid expenses it may have difficulty

(d) The CFO’s decision to use $18,000 of cash to pay off accounts

payable is not in itself unethical. However doing so just to improve the

EXERCISE 2-11B

2014

2013

(a)

Current ratio

$1,020,834

$376,178

= 2.71:1

$1,189,108

$464,618

= 2.56:1

(c)

Debt to assets ratio

$527,216

$1,867,680

= 28.2%

$562,246

$1,979,558

= 28.4%

(e) Using the debt to assets ratio and free cash flow as measures of

solvency produces negative results for American Eagle Outfitters. Its

EXERCISE 2-11B (Continued)

(f) In both 2014 and 2013 American Eagle Outfitters cash provided by

operating activities was greater than the cash used for capital

EXERCISE 2-12B

(a) 2 Going concern assumption

(b) 6 Economic entity assumption

EXERCISE 2-13B

1. Incorrect. The historical cost principle requires that assets be recorded

and reported at their cost.

3. Incorrect. The economic entity assumption requires that the activities