Problem 2-8B (LO 2-4, 2-5, 2-6)

Requirement 1

Entries are numbered for posting.

(1)

Nov. 1

Debit

Credit

Cash

13,000

Common Stock

13,000

(Issue common stock)

(2)

Nov. 2

Equipment

3,500

Notes Payable

3,500

(Purchase equipment with note payable)

(3)

Nov. 4

Supplies

Accounts Payable

(Purchase supplies on account)

(4)

Nov. 10

Accounts Receivable

Service Revenue

9,000

(Provide services on account)

(5)

Nov. 15

Accounts Payable

Cash

(Pay cash on account)

(6)

Nov. 20

Salaries Expense

Cash

3,000

(Pay current salaries)

(7)

Nov. 22

Cash

Service Revenue

11,000

(Provide services for cash)

(8)

Nov. 24

Notes Payable

Cash

(Pay note payable)

(9)

Nov. 26

Cash

Accounts receivable

7,000

Chapter 2 – The Accounting Cycle: During the Period

Problem 2-8B (continued)

(10)

Nov. 28

Utilities Expense

1,100

(11)

Nov. 30

Rent Expense

5,000

Problem 2-8B (continued)

Requirements 2 and 3

Cash

Accounts Receivable

Supplies

Bal. 3,200

(1) 13,000

1,100 (5)

3,000 (6)

Bal. 600

(4) 9,000

7,000 (9)

Bal. 700

(3) 1,000

Equipment

Accounts Payable

Notes Payable

Bal. 9,400

2,000 Bal.

(8) 1,400

4,000 Bal.

Common Stock

Retained Earnings

Service Revenue

7,000 Bal.

900 Bal.

9,000 (4)

Salaries Expense

Utilities Expense

Rent Expense

Chapter 2 – The Accounting Cycle: During the Period

Problem 2-8B (continued)

Requirement 4

Buckeye Incorporated

Trial Balance

November 30

Accounts

Debit

Credit

Cash

$22,600

Accounts Receivable

2,600

Supplies

1,700

Equipment

Accounts Payable

Notes Payable

Common Stock

Retained Earnings

Service Revenue

Salaries Expense

Utilities Expense

1,100

Rent Expense

Problem 2-9B (LO 2-4, 2-5, 2-6)

Requirement 1

Entries are numbered for posting.

(1)

December 1-31

Debit

Credit

Cash

27,400

Service Revenue

27,400

(Provide services for cash)

(2)

December 4

Supplies

2,900

Accounts Payable

2,900

(Purchase supplies on account)

(3)

December 8

Advertising Expense

Cash

(4)

December 9

Accounts Payable

Cash

2,900

(Pay cash on account)

(5)

December 12

Cash

Common Stock

5,000

(Issue shares of common stock)

(6)

December 16

Accounts Payable

Cash

6,300

(Pay cash on account)

(7)

December 19

Equipment

Cash

7,700

(Purchase equipment)

(8)

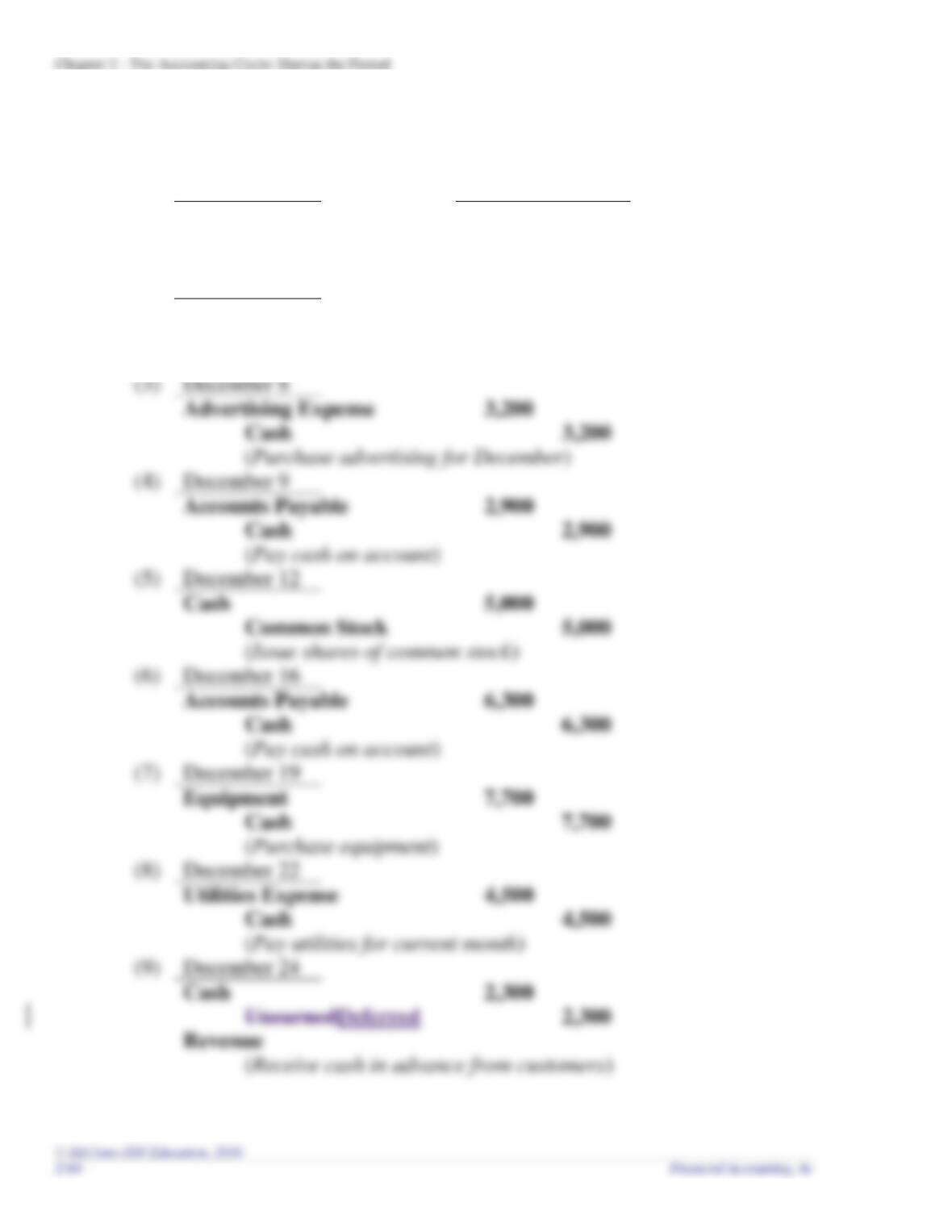

December 22

Utilities Expense

Cash

4,500

(Pay utilities for current month)

(9)

December 24

Cash

Revenue

Problem 2-9B (continued)

December 27

(10)

December 30

Cash

(11)

December 31

Dividends

3,000

Cash

Problem 2-9B (continued)

Requirements 2 and 3

Cash

Supplies

Prepaid Rent

4,400

Bal. 19,400

(1) 27,400

3,200 (3)

2,900 (4)

Bal. 1,500

(2) 2,900

Bal. 7,200

Equipment

Buildings

Accounts Payable

Bal. 83,700

Bal. 240,000

(4) 2,900

9,800 Bal.

UnearnedDeferred

Revenue

Common Stock

Retained Earnings

2,000 Bal.

125,000 Bal.

75,500 Bal.

Dividends

Service Revenue

Salaries Expense

(10) 7,000

Bal. 9,000

264,000 Bal.

Bal. 65,000

Advertising Expense

Utilities Expense

Bal. 18,200

Bal. 32,300

Problem 2-9B (continued)

Requirement 4

Thunder Cat Services

Trial Balance

December 31

Accounts

Debit

Credit

Cash

$ 19,500

Supplies

4,400

Prepaid Rent

7,200

Equipment

Buildings

Accounts Payable

$ 3,500

Common Stock

Retained Earnings

Dividends

Service Revenue

Salaries Expense

Advertising Expense

Chapter 2 – The Accounting Cycle: During the Period

ADDITIONAL PERSPECTIVES

Additional Perspective 2-1

Requirement 1

Entries are numbered for posting.

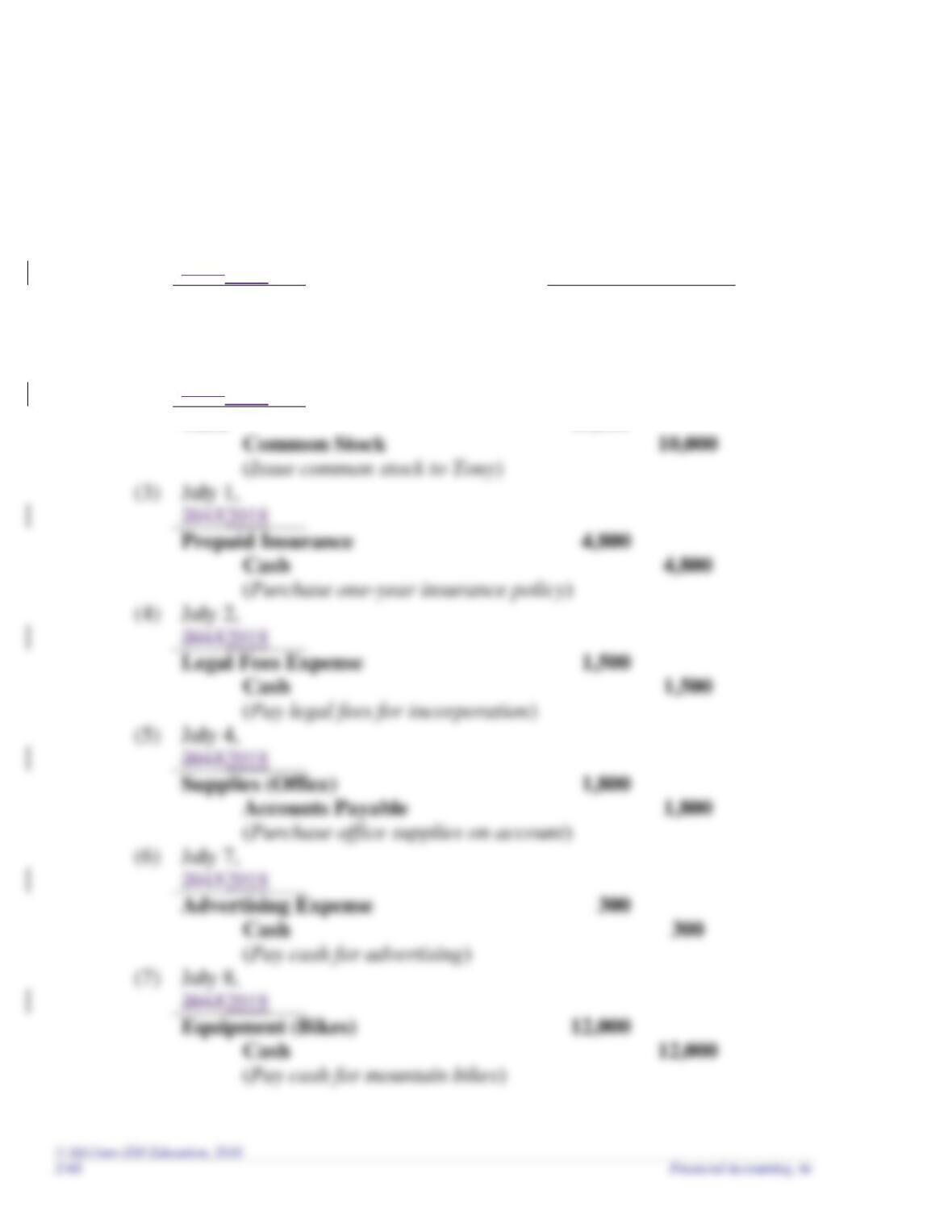

(1)

July 1,

20152018

Debit

Credit

Cash

10,000

Common Stock

10,000

(Issue common stock to Suzie)

(2)

July 1,

20152018

Cash

10,000

Common Stock

10,000

(Issue common stock to Tony)

20152018

Prepaid Insurance

Cash

(Purchase one-year insurance policy)

20152018

Legal Fees Expense

Cash

(5)

July 4,

20152018

Supplies (Office)

(Purchase office supplies on account)

(6)

July 7,

20152018

Cash

(Pay cash for advertising)

(7)

July 8,

20152018

Equipment (Bikes)

Cash

12,000

(Pay cash for mountain bikes)

Chapter 2 – The Accounting Cycle: During the Period

(8)

July 15,

20152018

Chapter 2 – The Accounting Cycle: During the Period

Additional Perspective 2-1 (continued)

Requirement 1 (concluded)

(9)

July 22,

20152018

Chapter 2 – The Accounting Cycle: During the Period

Additional Perspective P2-1 (continued)

Requirement 2

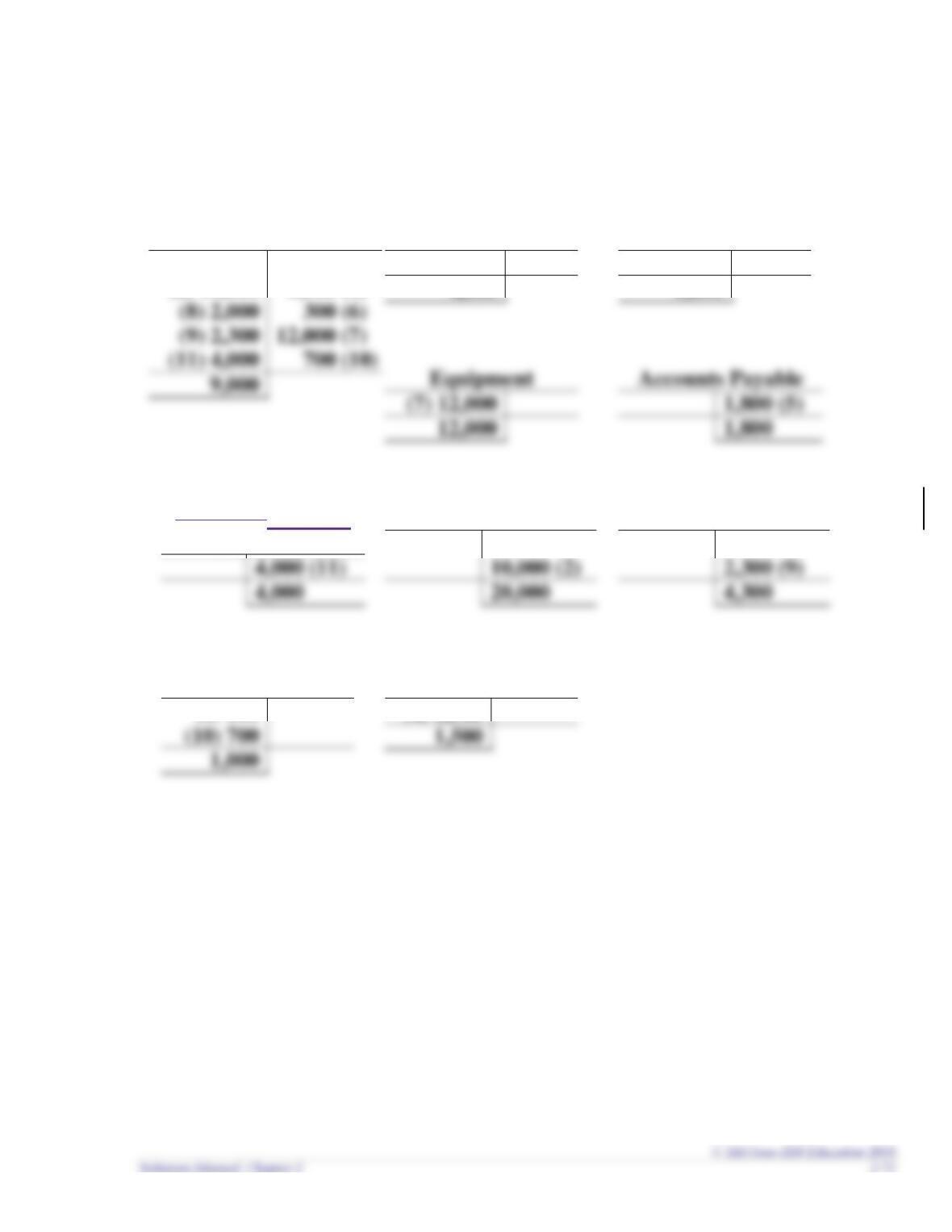

Cash

(1) 10,000

(2) 10,000

4,800 (3)

1,500 (4)

Prepaid Insurance

(3) 4,800

4,800

Supplies

(5) 1,800

1,800

UnearnedDeferred

Revenue

Common Stock

10,000 (1)

Service Revenue

2,000 (8)

Legal Fees Expense

(4) 1,500

Advertising Expense

(6) 300

Chapter 2 – The Accounting Cycle: During the Period

Additional Perspective 2-1 (concluded)

Requirement 3

Great Adventures, Inc.

Trial Balance

July 31, 20152018

Accounts

Debit

Credit

Cash

$ 9,000

Prepaid Insurance

4,800

Supplies

1,800

Equipment

Accounts Payable

Common Stock

Service Revenue

Advertising Expense

1,000

Legal Fees expense

1,500

Chapter 2 – The Accounting Cycle: During the Period

Additional Perspective 2-2

Requirement 1

Percentage change in total assets = ($1,756,0531,696,908 − $1,950,8021,694,164) /

$1,950,8021,694,164 = -9.90.168%

Requirement 2

Percentage change in net income = ($232,10880,322 − $151,70582,983) /

$151,70582,983 = -53.003.207%

Chapter 2 – The Accounting Cycle: During the Period

2-74 Financial Accounting, 4e

Additional Perspective 2-3

Requirement 1

Percentage change in total assets = ($477,974542,993 − $531,539546,293) /

$531,539546,293 = –10.080.60%

Requirement 3

Based on the statement of stockholders’ equity, The Buckle did issue a small amount

of common stock in the most recent year.

Requirement 4

The terms “debit” and “credit” are not shown in the balance sheet. Asset accounts,

Chapter 2 – The Accounting Cycle: During the Period

Additional Perspective 2-4

American EagleBuckle has a higher decline in terms of total assets, but greater growth

in net sales and net income. One reason for American Eagle’sBuckle’s growth could

Chapter 2 – The Accounting Cycle: During the Period

2-76 Financial Accounting, 4e

Additional Perspective 2-5

What is the issue?

Larry should understand that if he reports the additional $75,000 of revenue, the

Who are the parties affected?

Robert, the company’s president, benefits from false reporting by maintaining the

company’s profitable appearance. The incentives could be income bonus plans, a

What factors should Larry consider in making his decision?

Chapter 2 – The Accounting Cycle: During the Period

Additional Perspective 2-6

(Note to instructor: Answers are based on items in Apple’s September 297, 20124

annual report. Dollar amounts are in millions)

Requirement 1

Accounts receivable = $10,93017,460. The accounts receivable account represents the

amount owed to Apple by its customers.

Requirement 2

Requirement 5

Assets ($176,064231,839) = Liabilities ($57,854120,292) + Stockholders’ equity

($118,210111,547)

Chapter 2 – The Accounting Cycle: During the Period

Additional Perspective 2-7

For transaction (a):

Step 1. Analyze customer invoice.

Step 2. Determine assets increase and stockholders’ equity increases (and

For transaction (b):

Step 1. Analyze employee paycheck.

For transaction (c):

Step 1. Analyze purchase receipt for equipment.