a.

Liabilities & Owners’ Equity

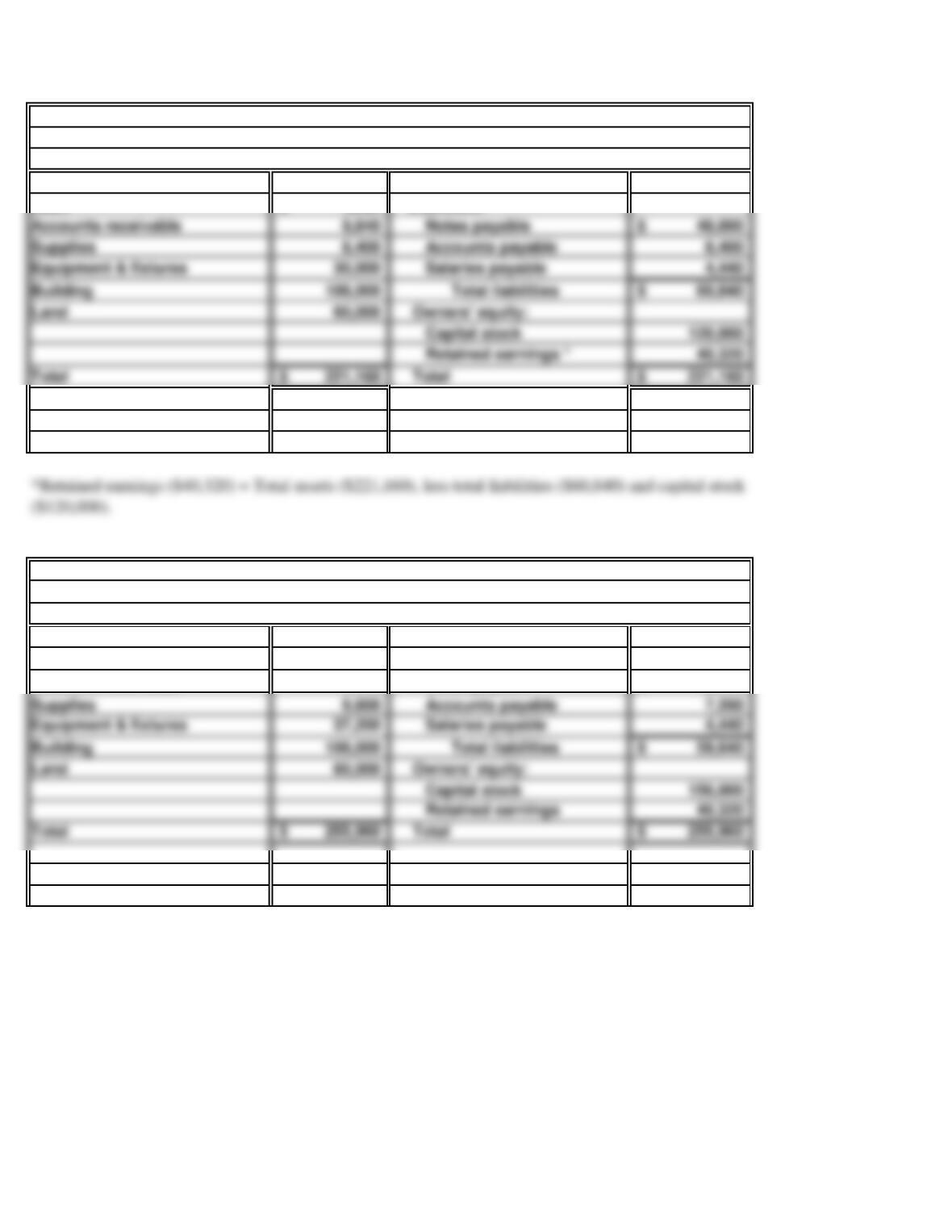

Cash 9,300$ Liabilities:

Accounts receivable 15,000 Notes payable 65,000$

Apple trees 84,000 Accounts payable 8,100

Livestock 5,000 Property taxes payable 4,700

b.

PROBLEM 2.6B

MAPLE VALLEY FARMS

20 Minutes, Medium

The loss of an asset, Barns and sheds, from a tornado would cause a decrease in total assets. When

MAPLE VALLEY FARMS

Balance Sheet

September 30, current year

Assets

a.

Liabilities & Owners’ Equity

Cash 4,920$ Liabilities:

b.

Liabilities & Owners’ Equity

Cash 31,320$ Liabilities:

Accounts receivable 9,840 Notes payable 48,000$

Assets

Balance Sheet

PROBLEM 2.7B

COLLIER BUTCHER SHOP

COLLIER BUTCHER SHOP

35 Minutes, Medium

COLLIER BUTCHER SHOP

Balance Sheet

Assets

July 5, current year

July 1, current year

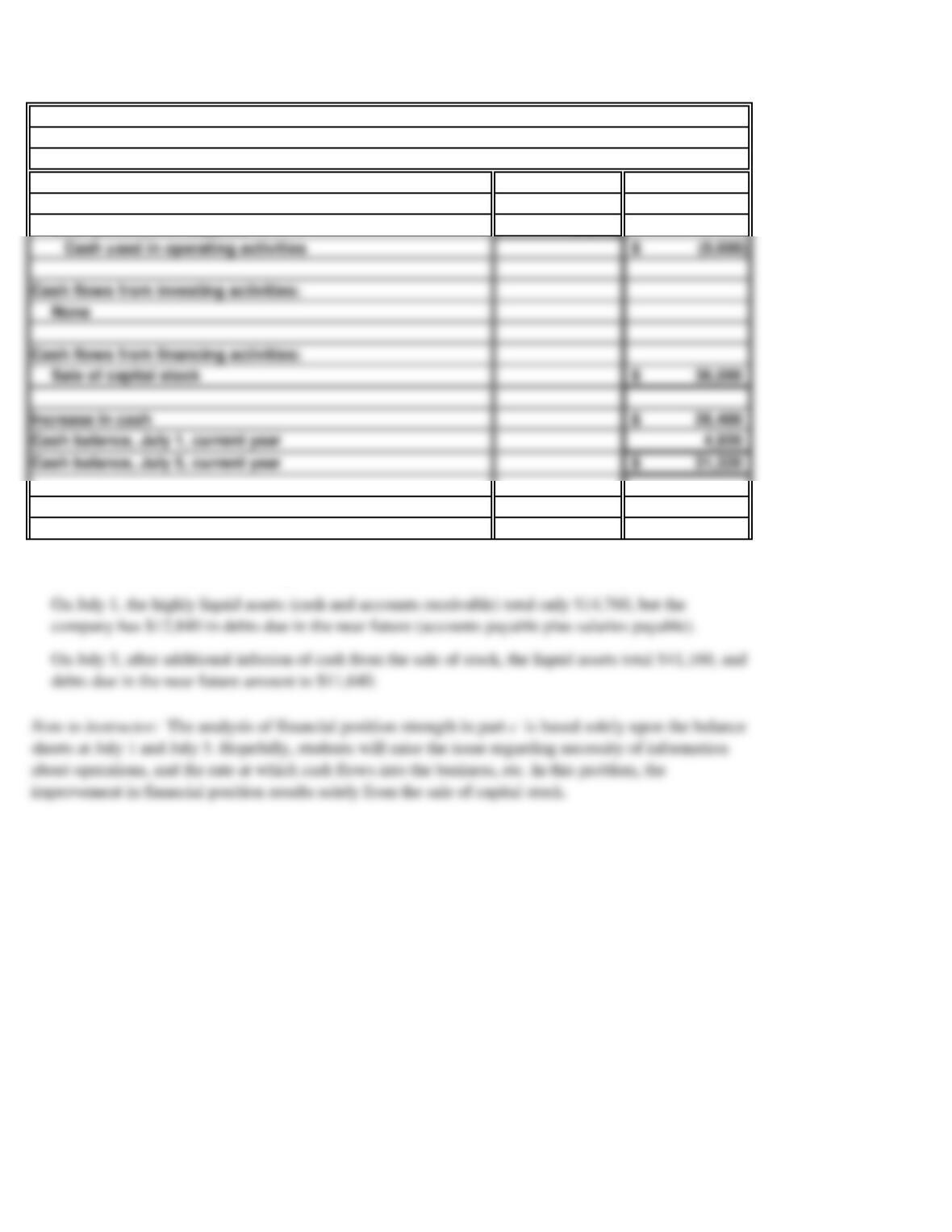

Cash flows from operating activities:

(8,400)$

(1,200)

c.

PROBLEM 2.7B

COLLIER BUTCHERSHOP (concluded)

COLLIER BUTCHER SHOP

Statement of Cash Flows

For the Period July 1-5, current year

Collier Butcher Shop is in a stronger financial position on July 5 than it was on July 1.

Cash payment of accounts payable

Cash purchase of supplies

Cash flows from financing activities:

Cash flows from investing activities:

a.

Liabilities & Owners’ Equity

Cash 6,900$ Liabilities:

Accounts receivable 5,000 Notes payable * 50,000$

b.

Land

Liabilities & Owners’ Equity

Cash 34,000$ Liabilities:

Accounts receivable 5,000 Notes payable 50,000$

8,000$

Balance Sheet

September 30, current year

Assets

PROBLEM 2.8B

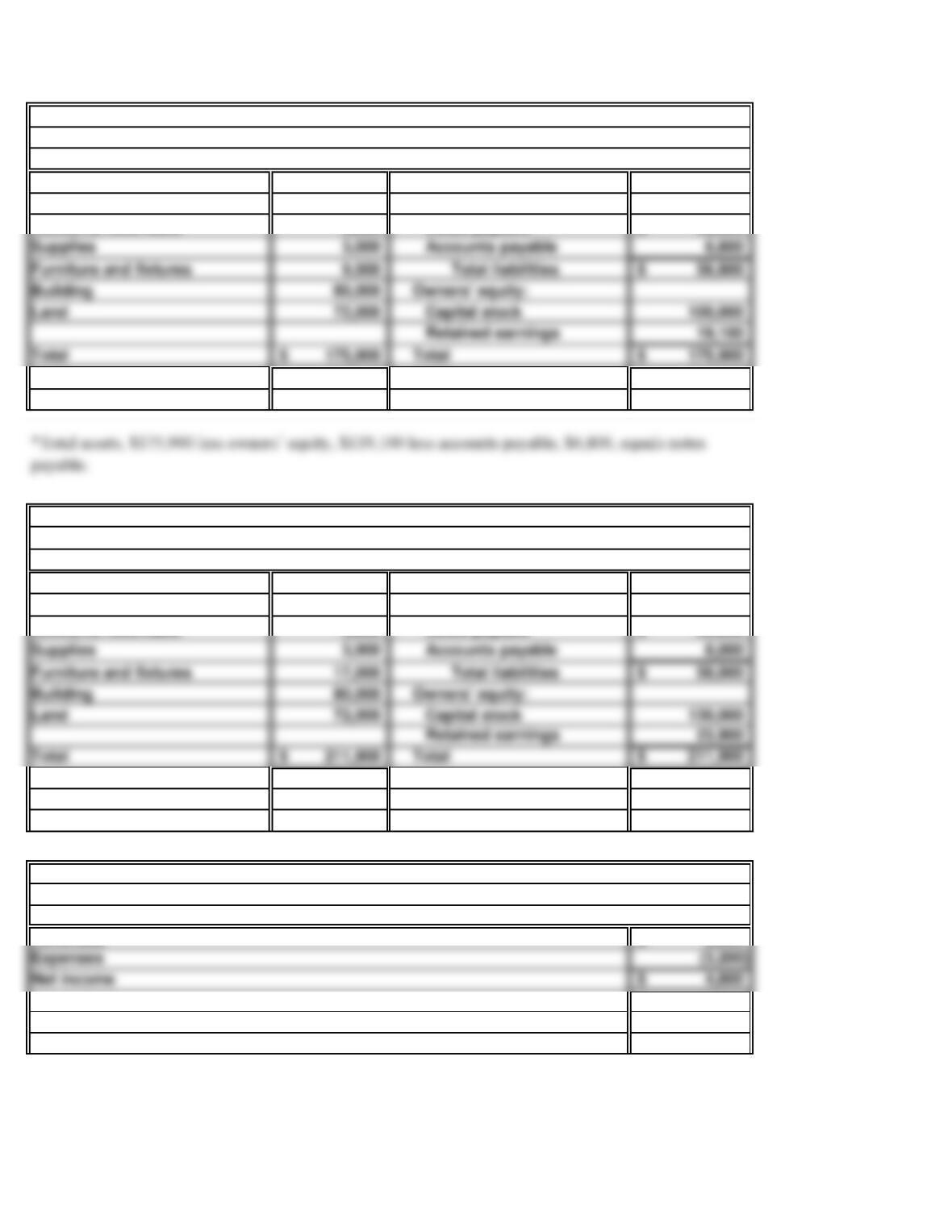

THE SWEET SHOP

40 Minutes, Strong

THE SWEET SHOP

THE SWEET SHOP

Income Statement

For the Period October 1-6, current year

Revenues

Assets

THE SWEET SHOP

October 6, current year

Balance Sheet

Land

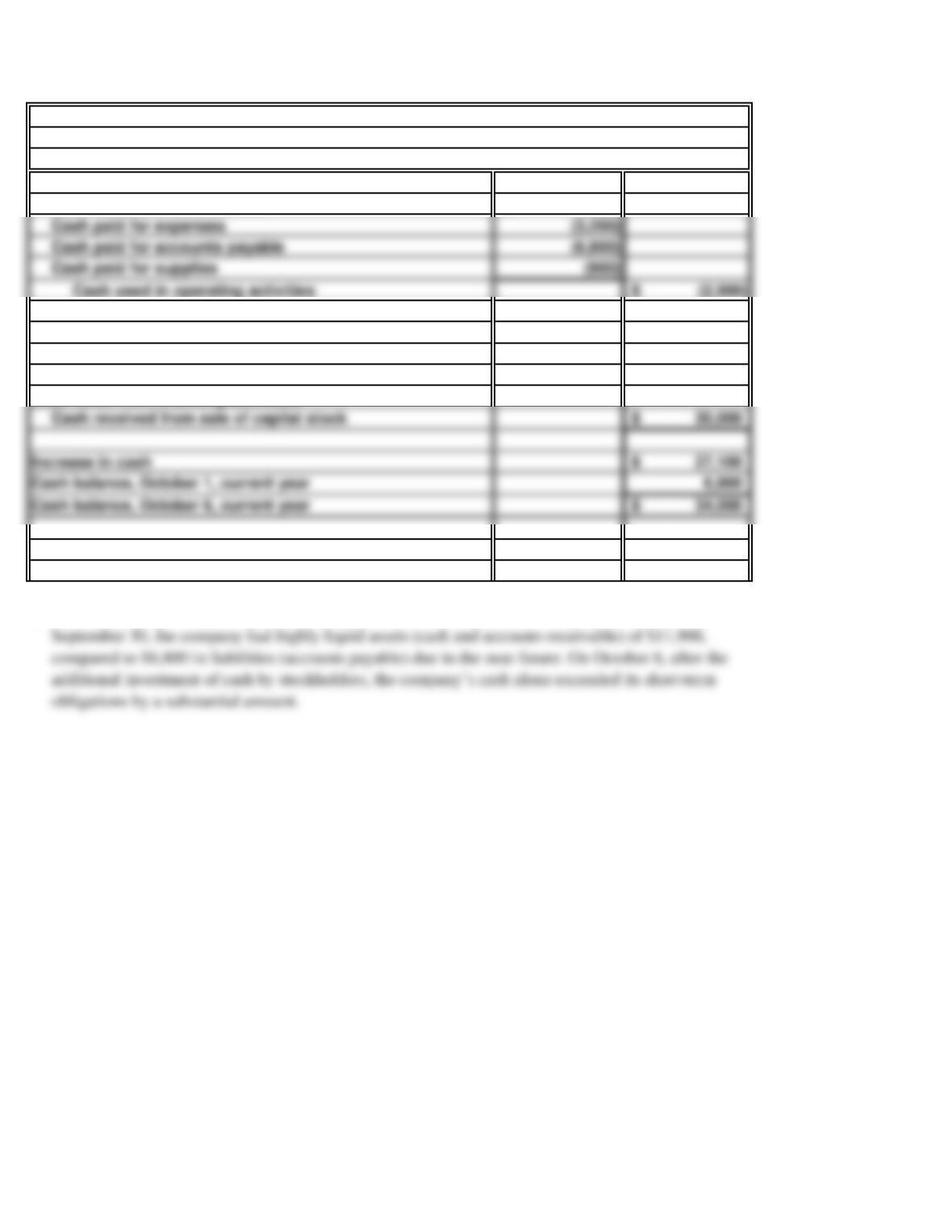

Cash used in operating activities

Cash flows from operating activities:

8,000$

None

c.

PROBLEM 2.8B

THE SWEET SHOP (concluded)

THE SWEET SHOP

The Sweet Shop is in a stronger financial position on October 6 than on September 30. On

Statement of Cash Flows

For the Period October 1-6, current year

Cash received from revenues

Cash flows from financing activities:

Cash flows from investing activities:

a.

Liabilities & Owner’s Equity

Cash 18,400$ Liabilities:

Accounts receivable 10,000 Notes payable 15,000$

b. (1)

(2)

(3)

(4)

(5)

(6)

(7)

As the automobile is not used in the business, it appears to be Jaffe’s personal asset rather than

Only the amount receivable from Dell, Inc. ($10,000) should be included in the company’s

relate to completed transactions and are not yet assets of the business.

The props and costumes should be shown in the balance sheet at their cost, $18,000 , not at just

The cash in Jaffe’s personal savings account is not an asset of the business entity Old Town

Playhouse. Therefore, it should not appear in the balance sheet of the business. The money on

PROBLEM 2.9B

OLD TOWN PLAYHOUSE

35 Minutes, Strong

OLD TOWN PLAYHOUSE

Balance Sheet

September 30, current year

Assets

(8)

(9)

PROBLEM 2.9B

OLD TOWN PLAYHOUSE (concluded)

Owner’s equity is not valued at either the original amount invested or at the estimated market

value of the business. In fact, owner’s equity cannot be valued independently of the values

The amount owed to stagehands for work done through September 30 is the result of completed

a.

Liabilities & Owner’s Equity

Cash 3,200$ Liabilities:

Notes receivable 3,400 Notes payable 72,500$

b. (1)

(2)

(3)

(4)

(5)

(6)

(7)

The proper valuation for the land is its historical cost of $15,000, the amount established by the

PROBLEM 2.10B

STAR SCRIPTS

30 Minutes, Strong

STAR SCRIPTS

Balance Sheet

November 30, current year

Assets

The $25,000 described as “Other assets” is not an asset, because there is no valid legal claim or

The cash in Joe’s personal savings account is not an asset of the business entity Star Scripts and

The years-old IOU does not qualify as a business asset for two reasons. First, it does not belong

The total amount to be included in “Office furniture” for the rug is $10,000, the total cost,

The computer is no longer owned by Star Scripts and therefore cannot be included in the assets.

CONTENT OF A BALANCE SHEET

This case requires students to prepare a hypothetical balance sheet for an entity to be specified by the

instructor. Therefore, we cannot provide a “solution.”

The purpose of the case is to challenge students to think about the types of assets necessary to the

SOLUTIONS TO CRITICAL THINKING CASES

CASE 2.1

30 Minutes, Medium

CASE 2.2

30 Minutes, Strong

This case is intended to acquaint students with using the financial statements and annual report of a

publicly held company of their (or your) choice. As students will select various reports, we cannot

USING FINANCIAL STATEMENTS

a.

b.

CASE 2.3

30 Minutes, Medium

Bankers considering a loan application are particularly interested in the ability of the company

to pay its debts. They want to make loans that will be repaid promptly and in full at the agreed

A banker is also interested in the amount of owners’ equity, since this ownership capital serves

as a protecting buffer between the banker and any losses that may befall the business. Although

Star Corporation has greater owners’ equity than Moon Corporation, the difference is relatively

USING A BALANCE SHEET

As an investor, you would probably be willing to pay a higher price to buy the capital stock of

Star Corporation. Since both companies are newly organized and the cost of assets shown on the

balance sheet approximates fair market value, we can assume in this case that total

a.

b.

John’s preliminary evaluation is focusing too much on the “bottom line” and not looking at the

details of the cash flow information. The most important difference between the cash flows of the

30 Minutes, Medium

USING STATEMENTS OF CASH FLOW

CASE 2.4

Look at the underlying details of financial statements, not just the final figures or bottom line.

c.

One possibility is that Walker Company ran out of financing in Year-3. We do not know the

General recommendations to John should include the following:

1.

2.

3.

4.

ETHICS AND WINDOW DRESSING

CASE 2.5

35 Minutes, Medium

Postponing the cash purchase of WordMaster would indeed leave Omega Software with an

additional $8 million in cash at year-end, which would make the company appear more liquid.

The deliberate omission of liabilities from the balance sheet is unethical and illegal. This action

There is nothing unethical or illegal about renegotiating the due date of a liability. In fact, as

Omega needs to borrow money anyway, extending this obligation to Delta at a 10% interest rate

reasonable in today’s credit market.

The intentional violation of generally accepted accounting principles with the intent to mislead

a.

b.

c.

d.

The Sarbanes-Oxley Act of 2002 directs the PCAOB to establish auditing and related professional

The enforcement authority of the PCAOB is a broad investigative and disciplinary authority over

registered public accounting firms and persons associated with such firms for noncompliance with the

The members of the PCAOB as of March 2016 are:

CASE 2.6

30 Minutes, Easy

The mission of the PCAOB is stated as follows: “The PCAOB is a private-sector non-profit corporation

ETHICS, FRAUD & CORPORATE GOVERNANCE

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

Lewis H. Ferguson

Jay D. Hanson

James R. Doty, chair

b.

170 West Tasman Drive

San Jose, CA 95134

CASE 2.7

25 Minutes, Easy

Cash and Cash Equivalents is the first item in the balance sheet. The end-of-quarter balance appears in the

a.

The business address of Cisco Systems is:

INTERNET

GATHERING FINANCIAL INFORMATION

d.