1. An account is a form designed to record changes in a particular asset, liability, owner’s equity,

revenue, or expense. A ledger is a group of related accounts.

2. The terms debit and credit may signify either an increase or a decrease, depending upon the nature

of the account. For example, debits signify an increase in asset and expense accounts but a decrease

in liability, owner’s equity, and revenue accounts.

5. No. Errors may have been made that had the same erroneous effect on both debits and credits, such

as failing to record and/or post a transaction, recording the same transaction more than once, and

p

osting a transaction correctly but to the wrong account.

6. Recording $9,800 instead of the correct amount of $8,900 is a transposition. Recording $100 instead

of the correct amount of $1,000 is a slide.

7. a. No. Because the same error occurred on both the debit side and the credit side of the trial

b

alance, the trial balance would not be out of balance.

b. Yes. The trial balance would not balance. The error would cause the debit total of the trial

b

alance to exceed the credit total by $90.

9. a. The equality of the trial balance would not be affected.

b. On the income statement, revenues (fees earned) would be overstated by $300,000, and net

income would be overstated by $300,000. On the statement of owner’s equity, the beginning

capital would be correct. However, net income and ending capital would be overstated by

$300,000. The balance sheet total assets is correct. However, liabilities (notes payable) is

understated by $300,000, and owner’s equity is overstated by $300,000. The understatement

of liabilities is offset by the overstatement of owner’s equity, and thus, total liabilities and

owner’s equity is correct.

CHAPTER 2

ANALYZING TRANSACTIONS

DISCUSSION QUESTIONS

CHAPTER 2 Analyzing Transactions

PE 2-1A

1. Debit and credit entries (c), normal debit balance

2. Credit entries only (b), normal credit balance

3. Credit entries only (b), normal credit balance

PE 2-1B

1. Debit and credit entries (c), normal credit balance

2. Debit and credit entries (c), normal debit balance

3. Debit entries only (a), normal debit balance

PE 2-2A

Feb. 19 Office Equipment 14,800

PE 2-2B

Sept. 30 Office Supplies 1,900

Cash 600

PRACTICE EXERCISES

CHAPTER 2 Analyzing Transactions

PE 2-3A

Apr. 30 Accounts Receivable 12,980

Fees Earned 12,980

PE 2-3B

PE 2-4A

Dec. 23 Graeme Schneider, Drawing 27,000

Cash 27,000

PE 2-4B

PE 2-5A

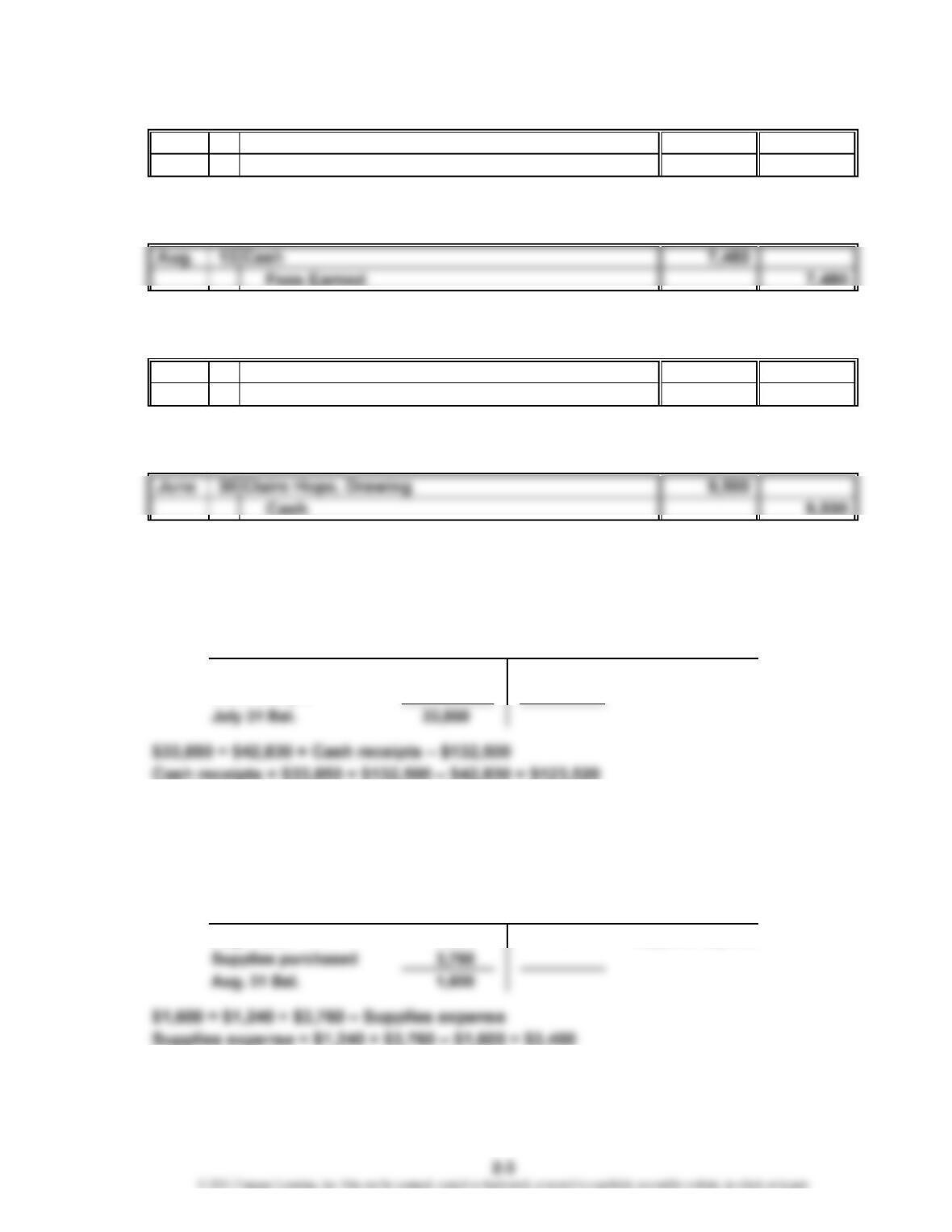

Using the following T account, solve for the amount of cash receipts (indicated

by ? below).

July 1 Bal. 42,830 132,500 Cash payments

Cash receipts ?

PE 2-5B

Using the following T account, solve for the amount of supplies expense

(indicated by ? below).

Aug. 1 Bal. 1,240 ? Supplies expense

Cash

Supplies

CHAPTER 2 Analyzing Transactions

PE 2-6A

a. The trial balance totals are unequal. The debit total is higher by $900 ($9,800 –

$8,900).

b. The trial balance totals are equal because both the debit and credit entries were

PE 2-6B

a. The trial balance totals are equal because both the debit and credit entries were

journalized and posted for $14,200.

b. The trial balance totals are unequal. The credit total is higher by $360 ($1,730 –

$1,370).

CHAPTER 2 Analyzing Transactions

PE 2-7A

a.

Miscellaneous Expense 3,220 Rent Expense 3,220

Rent Expense 3,220 Cash 3,220

b.

Cash 5,080 Cash 5,080

Accounts Payable 5,080 Accounts Receivable 5,080

Accounts Receivable instead of Accounts Payable should have been credited.

Comparison

Made in Error Have Been Made

Journal Entry That Was Journal Entry That Should

Journal Entry That Was Journal Entry That Should

Made in Error Have Been Made

Correcting Journal Entries

CHAPTER 2 Analyzing Transactions

PE 2-7B

a.

Accounts Receivable 10,700 Cash 10,700

Fees Earned 10,700 Fees Earned 10,700

Accounts Receivable 10,700

b.

Office Equipment 4,300 Supplies 4,300

Supplies 4,300 Accounts Payable 4,300

Supplies instead of Office Equipment should have been debited.

Accounts Payable instead of Supplies should have been credited.

The debit and credit amount of $4,300 is correct.

Note: The first entry reverses the incorrect entry, and the second entry is what should have

been recorded initially. These two entries could have been combined into one entry;

however, preparing two entries makes it easier for someone later to understand what

happened and why the entries were necessary.

Journal Entry That Was Journal Entry That Should

Made in Error Have Been Made

Journal Entry That Was Journal Entry That Should

Made in Error Have Been Made

Comparison

CHAPTER 2 Analyzing Transactions

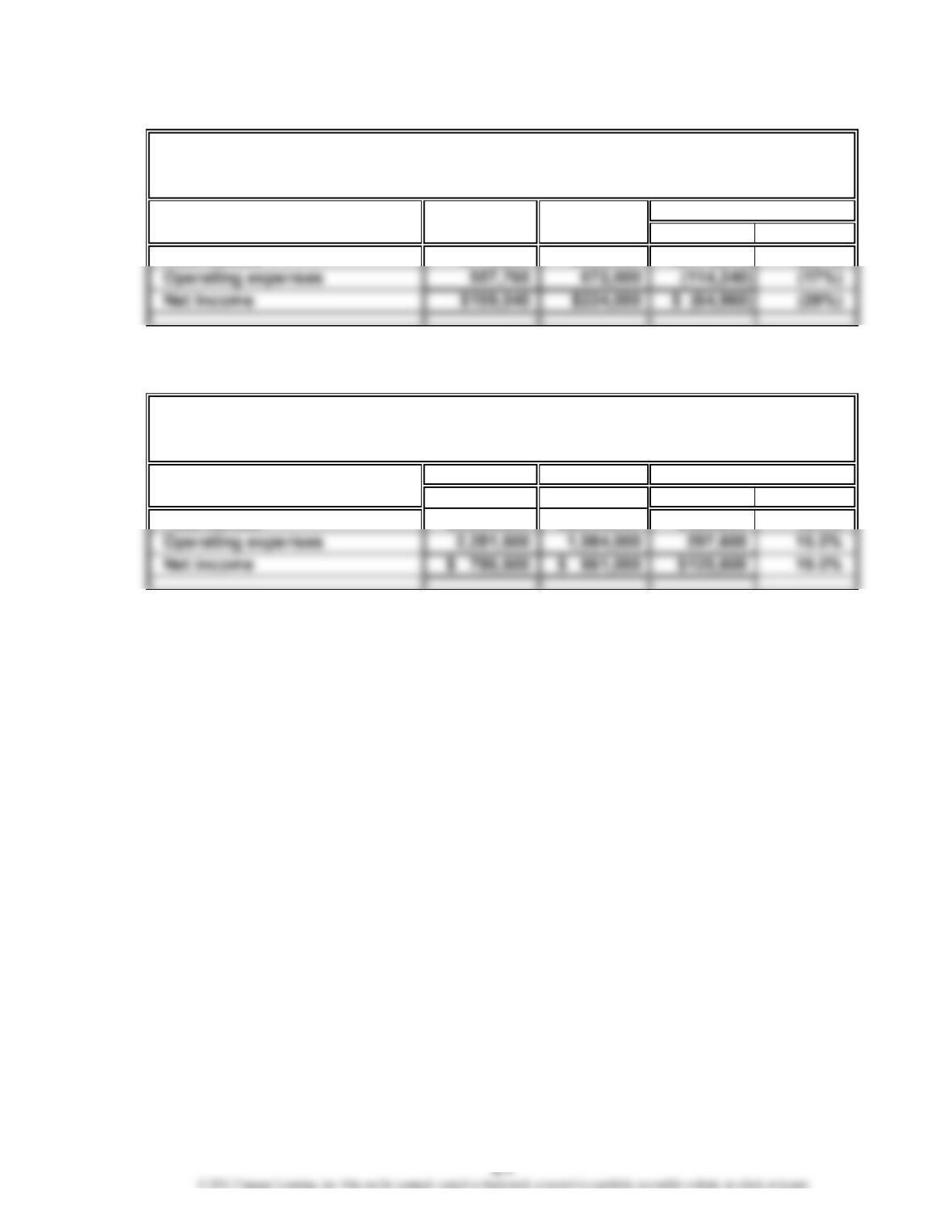

PE 2-8A

20Y1 20Y0 Amount Percent

Fees earned $716,800 $896,000 $(179,200) (20%)

PE 2-8B

20Y1 20Y0

Amount Percent

Vaughn Company

Income Statements

For the Years Ended December 31

Increase/(Decrease)

Increase/(Decrease)

Satterfield Company

Income Statements

For the Years Ended December 31

CHAPTER 2 Analyzing Transactions

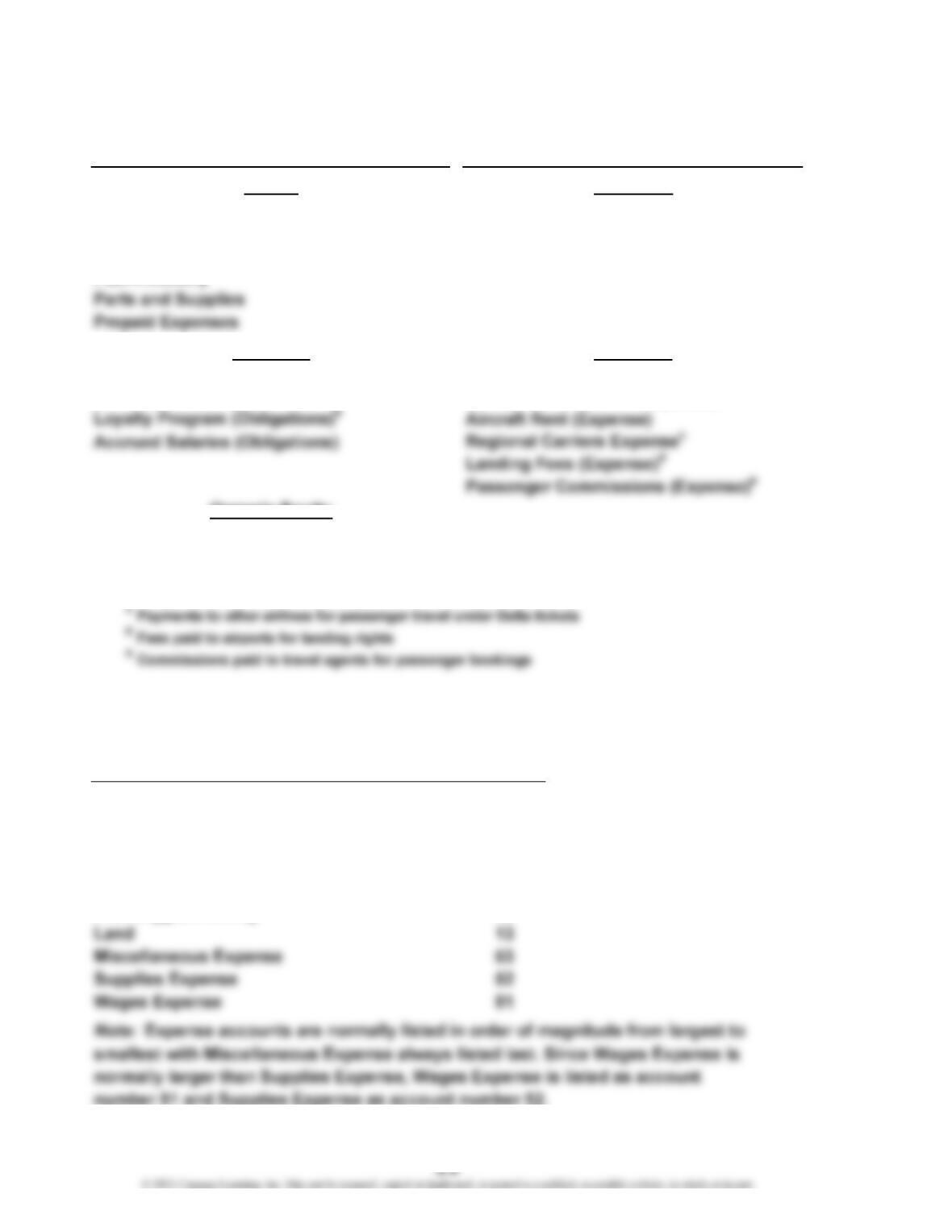

Ex. 2-1

Cash Cargo Revenue

Accounts Receivable Passenger Revenue

Property and Equipment

Accounts Payable Aircraft Fuel (Expense)

Air Traffic LiabilityaAircraft Maintenance (Expense)

b

d

None

aPassenger ticket sales for future flights

b

Obligations to provide frequent flyers future travel and other benefits

d

Ex. 2-2

Account

Number

Accounts Payable 21

Accounts Receivable 12

Cash 11

Fees Earned 41

Fred Biggs, Capital 31

Fred Biggs, Drawing 32

Expenses

Liabilities

Owner’s Equity

Account

EXERCISES

Assets Revenues

Balance Sheet Accounts Income Statement Accounts

CHAPTER 2 Analyzing Transactions

Ex. 2-3

11 Cash 41 Fees Earned

12 Accounts Receivable

53 Supplies Expense

59 Miscellaneous Expense

21 Accounts Payable

22 Unearned Rent

Note: The order of some of the accounts within the major classifications is

somewhat arbitrary, as in accounts 13–14, accounts 21–22, and accounts 51–53.

In a new business, the order of magnitude of balances in such accounts is not

determinable in advance. The magnitude may also vary from period to period.

Ex. 2-4

a. debit g. debit

b. credit h. credit

c. debit i. debit

Ex. 2-5

1. debit and credit entries (c)

2. debit and credit entries (c)

3. debit and credit entries (c)

2. Liabilities

1. Assets 4. Revenue

Balance Sheet Accounts Income Statement Accounts

CHAPTER 2 Analyzing Transactions

Ex. 2-6

a. Liability—credit e. Asset—debit

b. Asset—debit f. Revenue—credit

Ex. 2-7

20Y3

Oct. 1 Rent Expense 4,800

Cash 4,800

6 Office Equipment 10,670

Accounts Payable 10,670

10 Cash 19,730

Accounts Receivable 19,730

15 Accounts Payable 9,480

Cash 9,480

27 Miscellaneous Expense 530

Cash 530

30 Utilities Expense 220

Cash 220

CHAPTER 2 Analyzing Transactions

Ex. 2-8

a.

Page 87

Post.

Ref. Debit Credit

20Y4

b., c., d.

Account No. 15

Post.

Ref. Debit Debit Credit

20Y4

Sept. 1 Balance 2,960

18 87 8,710 11,670

Account No. 21

Post.

e. Yes. The rules of debit and credit apply to all companies.

Ex. 2-9

a. (1) Accounts Receivable 73,900

Fees Earned 73,900

(2) Supplies 1,960

Accounts Payable 1,960

Balance

Credit

Balance

JOURNAL

Account:

Account: Supplies

Accounts Payable

Date

Date Description

Item

CHAPTER 2 Analyzing Transactions

Ex. 2-9 (Concluded)

b.

(3) 62,770 (4) 820 (4) 820 (2) 1,960

c. No. An error may not have necessarily occurred. A credit balance in Accounts

Receivable could occur if a customer overpaid his or her account. Regardless,

the credit balance should be investigated to verify that an error has not occurred.

Ex. 2-10

a. The increase of $140,000 ($515,000 – $375,000) in the cash account does not

indicate net income of that amount. Net income is the excess of revenues

over expenses and is normally not the same as the change in the cash account.

b. $60,000 ($200,000 – $140,000)

or

Cash

Cash Accounts Payable

Supplies Fees Earned

CHAPTER 2 Analyzing Transactions

Ex. 2-11

X = $46,600

b.

Oct. 1 121,100 470,500

X

Oct. 31 136,800

$121,100 + X – $470,500 = $136,800

X = $136,800 + $470,500 – $121,100

X = $486,200

c.

Ex. 2-12

a. Credit balance of $170,000 ($500,000 – $10,000 – $320,000).

b. Yes. The balance sheet prepared at December 31 will balance, with Terrace

Waters, Capital, being reported in the owner’s equity section as $170,000.

Cash

Accounts Receivable

CHAPTER 2 Analyzing Transactions

Ex. 2-13

a. and b.

Effect Type Effect

asset + owner’s equity +

asset + asset –

asset + asset –

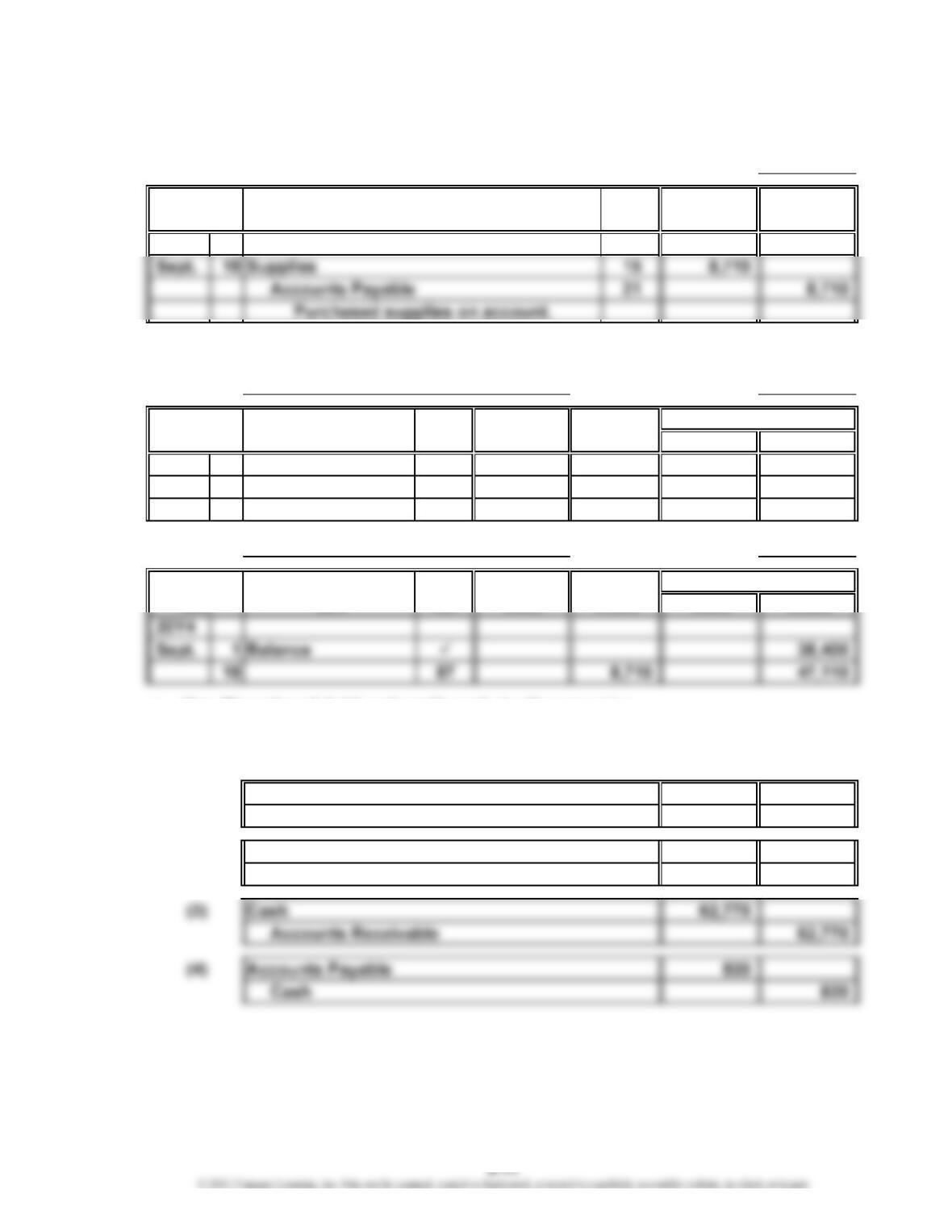

Ex. 2-14

(1) Cash 97,000

Mary Silva, Capital 97,000

Cash 2,070

(4) Operating Expenses 8,120

Cash 8,120

(5) Accounts Receivable 15,910

Fees Earned 15,910

(6) Accounts Payable 3,490

Cash 3,490

(7) Cash 10,540

Accounts Receivable 10,540

(3)

(2)

Account Debited Account Credited

Type

(1)

Transaction

CHAPTER 2 Analyzing Transactions

Ex. 2-15

a.

Debit Credit

Balances Balances

Cash 89,500

Accounts Receivable 5,370

Supplies 310

Equipment 10,350

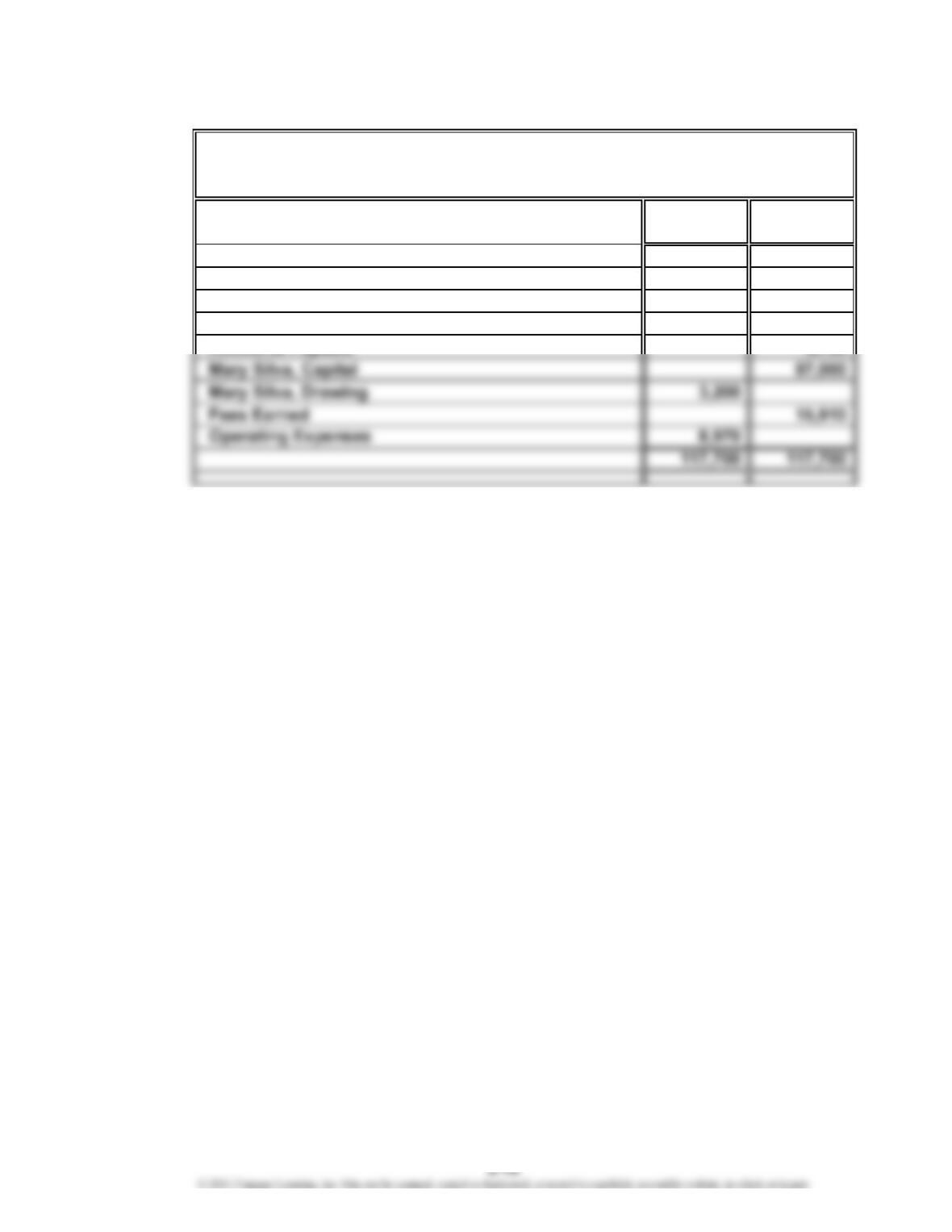

b. Net income, $6,940 ($15,910 – $8,970)

Emerald Tours Co.

Unadjusted Trial Balance

May 31, 20Y5

CHAPTER 2 Analyzing Transactions

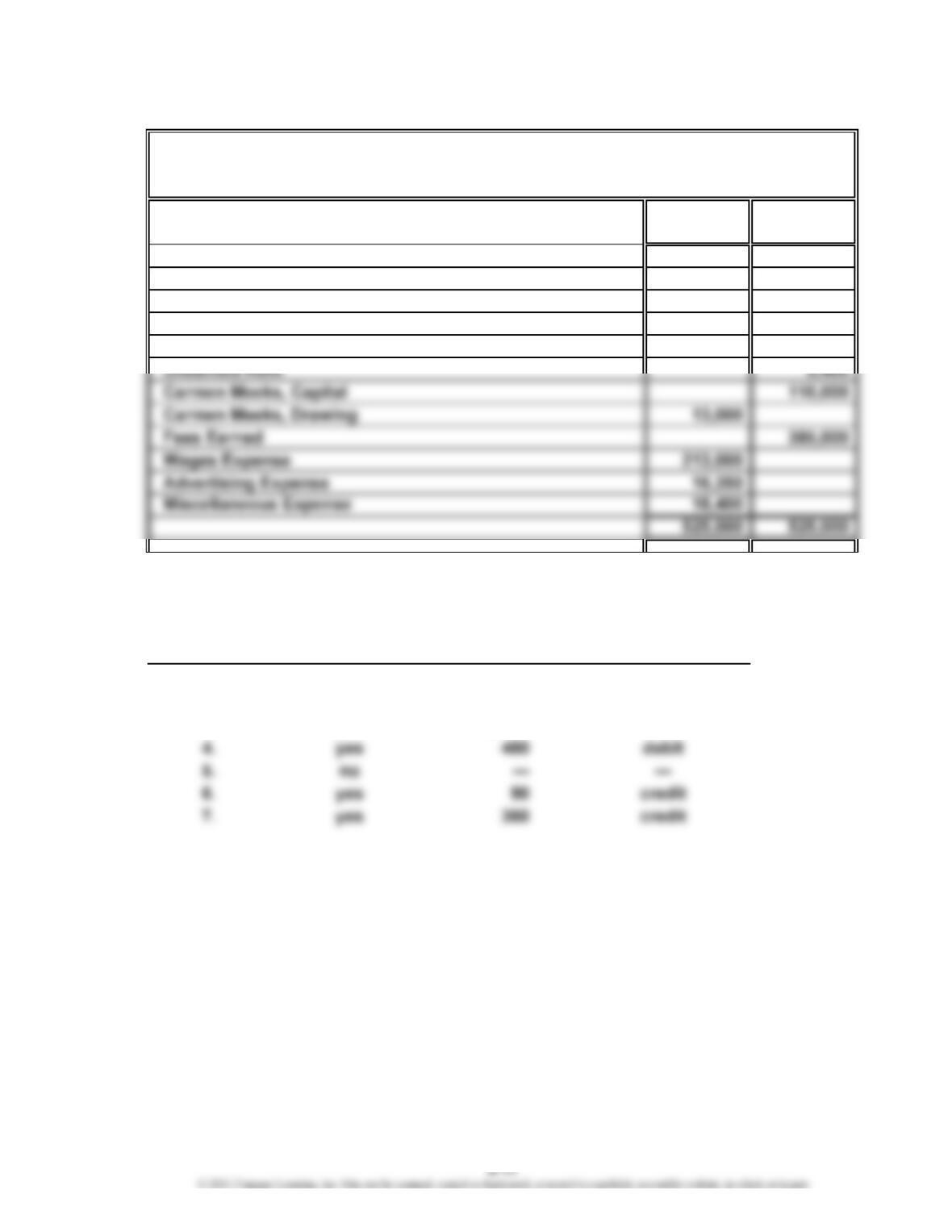

Ex. 2-16

Debit Credit

Unearned Rent 12,000

Notes Payable 50,000

Elaine Wells, Capital 75,000

Elaine Wells, Drawing 24,000

Fees Earned 745,230

925,000 925,000

*

$33,320 = $925,000 – $9,500 – $3,600 – $6,255 – $26,850 – $48,000 – $580,700 – $24,000

– $50,000 – $21,600 – $4,275 – $116,900

Ex. 2-17

Inequality of trial balance totals would be caused by errors described in (c) and

(e). For (c), the debit total would exceed the credit total by $9,900 ($4,950 + $4,950).

For (e), the credit total would exceed the debit total by $17,100 ($19,000 – $1,900).

Hickory Furniture Company

Unadjusted Trial Balance

December 31, 20Y6

CHAPTER 2 Analyzing Transactions

Ex. 2-18

Debit Credit

Balances Balances

Cash 15,500

Accounts Receivable 46,750

Prepaid Insurance 12,000

Equipment 190,000

Accounts Payable 24,600

Ex. 2-19

(a) (b)

Error Out of Balance Difference

1. yes $6,000

2. no —

3. yes 5,400

(c)

Larger Total

Ranger Co.

Unadjusted Trial Balance

August 31, 20Y7

debit

—

credit

CHAPTER 2 Analyzing Transactions

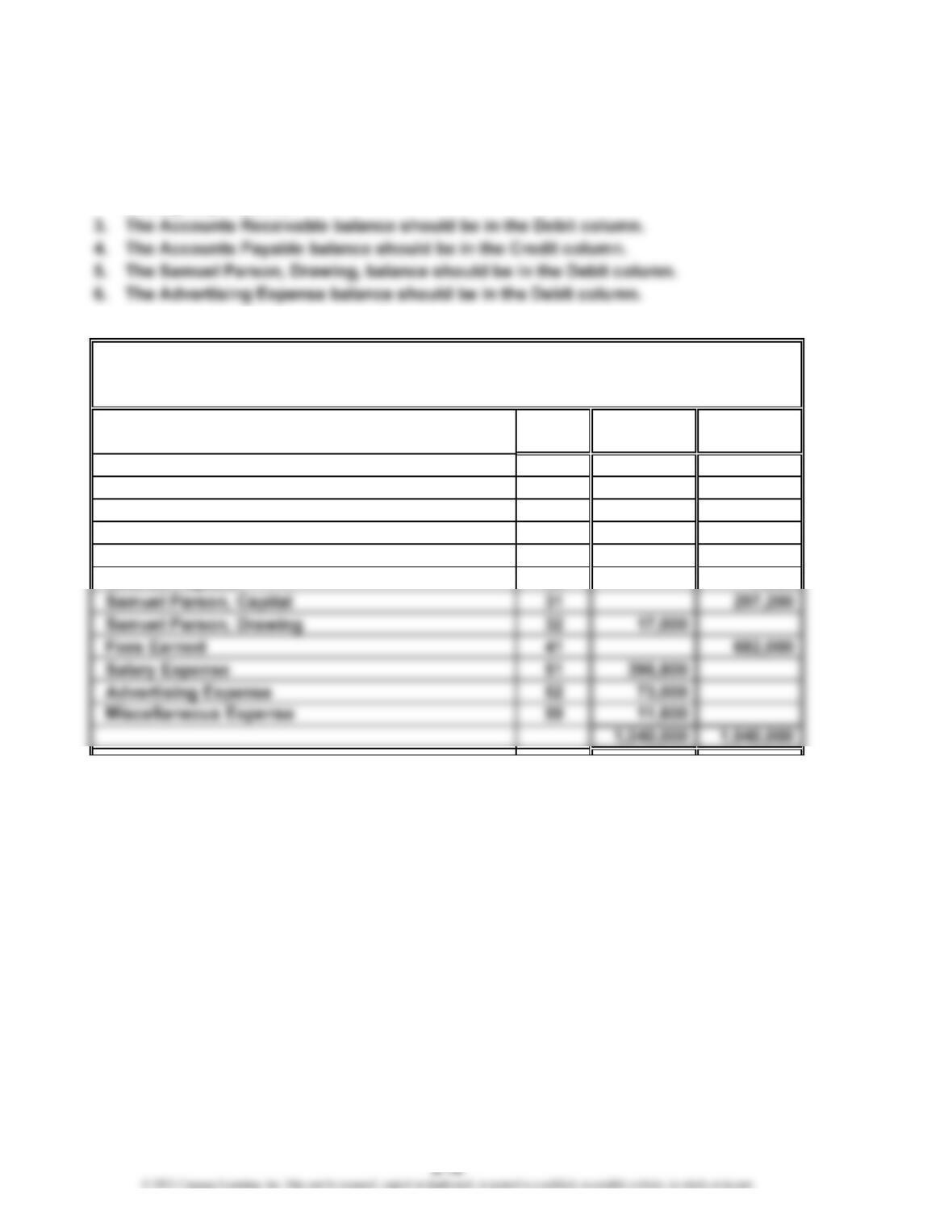

Ex. 2-20

1. The Debit column total is added incorrectly. The sum is $890,700 rather than

$1,189,300.

2. The trial balance should be dated “July 31, 20Y3,” not “For the Month

Ending July 31, 20Y3.”

A corrected trial balance would be as follows:

Account Debit Credit

No. Balances Balances

Cash 11 36,000

Accounts Receivable 12 112,600

Prepaid Insurance 13 18,000

Equipment 14 375,000

Accounts Payable 21 53,300

Salaries Payable 22 7,500

Mascot Co.

Unadjusted Trial Balance

July 31, 20Y3

CHAPTER 2 Analyzing Transactions

Ex. 2-21

a.

Insurance Expense 18,000 Prepaid Insurance 18,000

Prepaid Insurance 18,000 Cash 18,000

Prepaid Insurance 18,000

Insurance Expense 18,000

Prepaid Insurance 18,000

Cash 18,000

b.

Wages Expense 10,000 Brian Phillips, Drawing 10,000

Cash 10,000 Cash 10,000

Brian Phillips, Drawing instead of Wages Expense should have been debited.

Journal Entry That Was Journal Entry That Should

Made in Error Have Been Made

Correcting Journal Entries

Journal Entry That Was Journal Entry That Should

Made in Error Have Been Made

Comparison

CHAPTER 2 Analyzing Transactions

Ex. 2-22

a.

Fees Earned 8,800 Cash 8,800

Cash 8,800 Accounts Receivable 8,800

Cash instead of Fees Earned should have been debited. Accounts Receivable

instead of Cash should have been credited. The debit and credit amount of

Note: The first entry reverses the incorrect entry, and the second entry is what should have

been recorded initially. These two entries could have been combined into one entry;

however, preparing two entries makes it easier for someone later to understand what

happened and why the entries were necessary.

b.

Supplies Expense 1,760 Supplies 1,760

Accounts Payable 1,760 Cash 1,760

Accounts Payable 1,760

Supplies Expense 1,760

Supplies 1,760

Cash 1,760

Note: The first entry reverses the incorrect entry, and the second entry is what should have

been recorded initially. These two entries could have been combined into one entry;

Correcting Journal Entries

Journal Entry That Was Journal Entry That Should

Made in Error Have Been Made

Comparison

Journal Entry That Was Journal Entry That Should

Made in Error Have Been Made

Comparison