Student Name:

Class:

Part a.

7,800$

48,300

43,800

12,300$

Correct!

Instructor

McGraw-Hill/Irwin

Exercise 02-41

Beginning direct materials inventory

MONROE FABRICATORS

Transferred Out

Transferred In

Ending direct materials inventory

Part b.

81,450$

Ending work-in-process inventory

Cost of goods sold

Direct labor

Manufacturing overhead

Total manufacturing cost

Total Manufacturing cost

Beginning work-in-process inventory

Cost of goods manufactured

Gross margin

7,800$

a. ?

8,100

11,400

5,700

Work-in-process inventory, December 31

Given Data E02-41:

MONROE FABRICATORS

Direct materials inventory, January 1

Work-in-process inventory, January 1

Direct materials inventory, December 31

Finished goods inventory, January 1

Sales revenue

Manufacturing overhead

Direct materials used

Direct labor

Gross margin

Cost of goods sold

Total manufacturing cost

Cost of goods manufactured during the year

Purchases of direct materials

Finished goods inventory, December 31

Student Name:

Class:

270$

165

60

495$ «- Correct!

MADRID CORPORATION

Instructor

McGraw-Hill/Irwin

Exercise 02-46

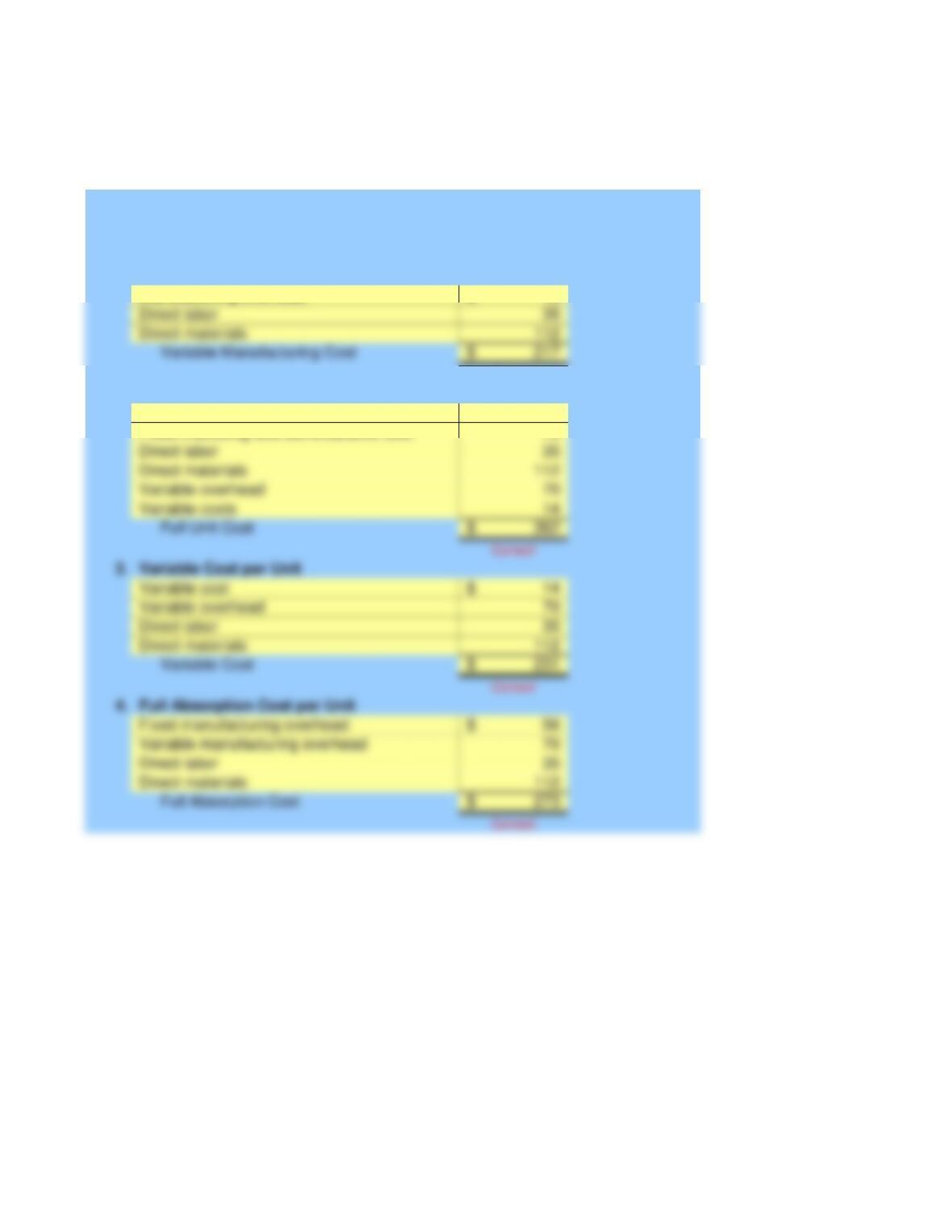

Direct Materials

Direct Labor

Variable Manufacturing Overhead

Variable Manufacturing Costs

Fixed Manufacturing overhead:

Full-absorption Cost

Fixed Marketing and Administrative Cost

Full Cost of Making and Selling Product

Variable Marketing and Administrative Cost

Unit Variable Cost

900$

Given Data E02-46:

Information provided by accounting system:

Fixed costs (for the month)

Sales price (per unit)

MADRID CORPORATION

Units produced and sold (for the month)

Direct labor

Manufacturing overhead

Direct materials

Marketing and administrative

Variable costs (per unit)

Manufacturing overhead

Marketing and administrative

Student Name:

Class:

a.

9,000$

120,000

Correct!

c.

4,500$

e.

Manufacturing Overhead

Direct Labor

Direct materials

Manufacturing Overhead

Total Manufacturing Costs Computation

Direct Labor

Total Conversion Cost Computation

Ending Finished Goods Inventory

Beginning Finished Goods Inventory

Cost of Goods Manufactured

Cost of Goods Manufactured Calculation

Cost of Goods Sold Calculation

Ending Work-in-Process

Total Manufacturing Costs

Beginning Work-in-Process

Problem 02-54

McGraw-Hill/Irwin

Instructor

CHELSEA, INC.

Total Prime Cost Computation

Plus Purchases

Beginning Inventory

Minus Ending Inventory

Direct Labor

Direct materials

9,000$

7,500

Given Data P02-54:

Information provided by accounting records:

CHELSEA, INC.

Direct materials inventory, May 1

Direct materials inventory, May 31

Manufacturing overhead, May

Direct materials purchased during May

Direct labor costs, May

Work-in-process inventory, May 1

Work-in-process inventory, May 31

Finished goods inventory, May 1

Finished goods inventory, May 31

Student Name:

Class:

a.

Computations

1.

70$

Correct!

2.

56$

3.

14$

4.

56$

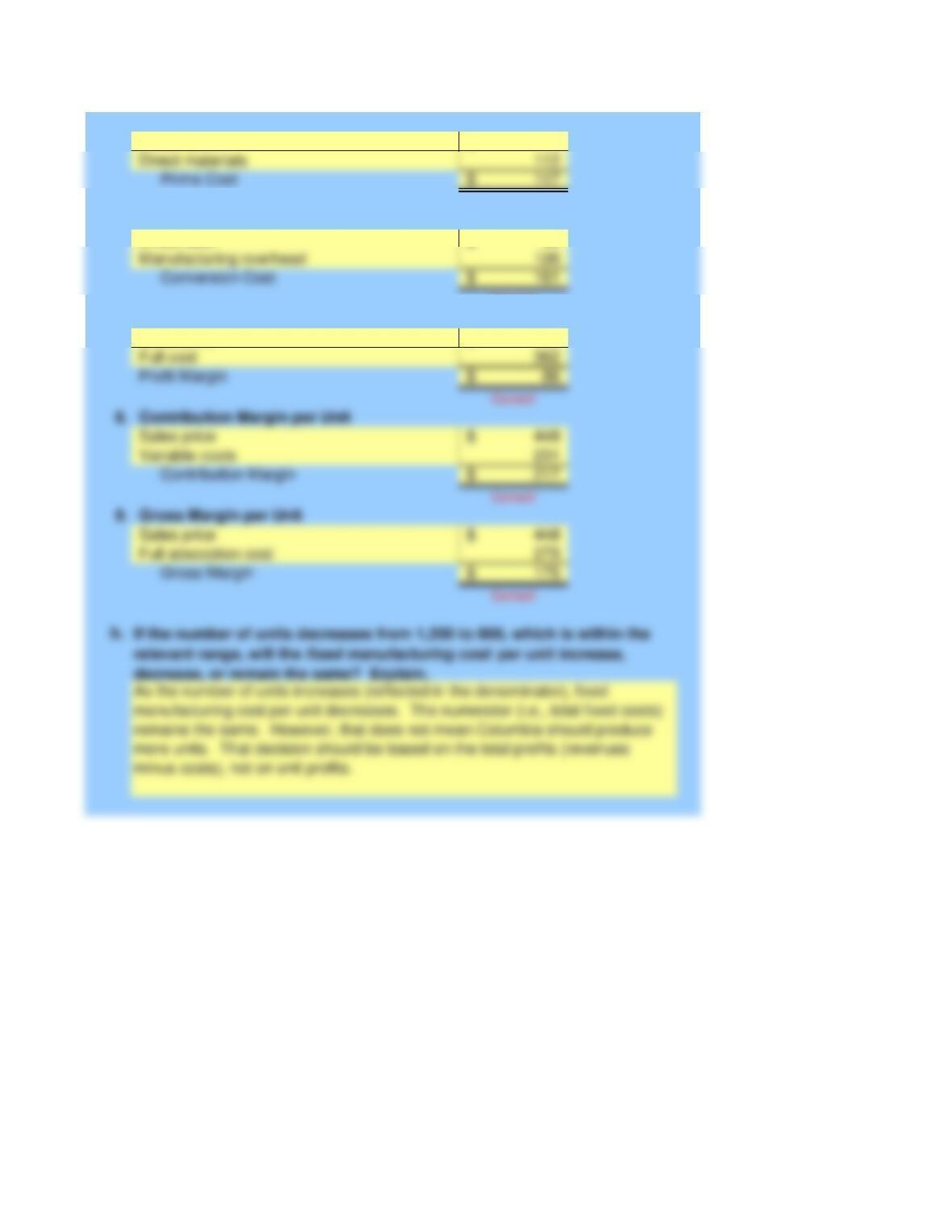

Direct materials

Direct labor

Variable manufacturing overhead

Direct labor

Variable overhead

Variable cost

Variable Cost per Unit

Fixed manufacturing overhead

Full Absorption Cost per Unit

Direct materials

Direct labor

Variable costs

Variable overhead

Direct materials

75

Problem 02-56

McGraw-Hill/Irwin

Instructor

COLUMBIA PRODUCTS

Variable Manufacturing Cost

Manufacturing overhead

Fixed marketing and administrative cost

Fixed manufacturing

Full Unit Cost

Direct materials

Direct labor

5.

35$

Correct!

6.

35$

Manufacturing overhead

Correct!

7.

448$

8.

448$

9.

448$

Full absorption cost

Sales price

Gross Margin per Unit

Variable costs

Sales price

Contribution Margin per Unit

Full cost

Profit Margin per Unit

Direct labor

Sales price

Conversion Cost per Unit

Direct labor

Prime Cost per Unit

Direct materials

448$

Manufacturing costs:

Information provided by accounting system:

Given Data P02-56:

COLUMBIA PRODUCTS

Sales price (per unit)

Variable overhead (per unit)

Fixed costs (for the month)

Variable costs (per unit)

Direct labor (per unit)

Direct materials (per unit)

Marketing and administrative costs:

Fixed overhead (for the month)

Student Name:

Class:

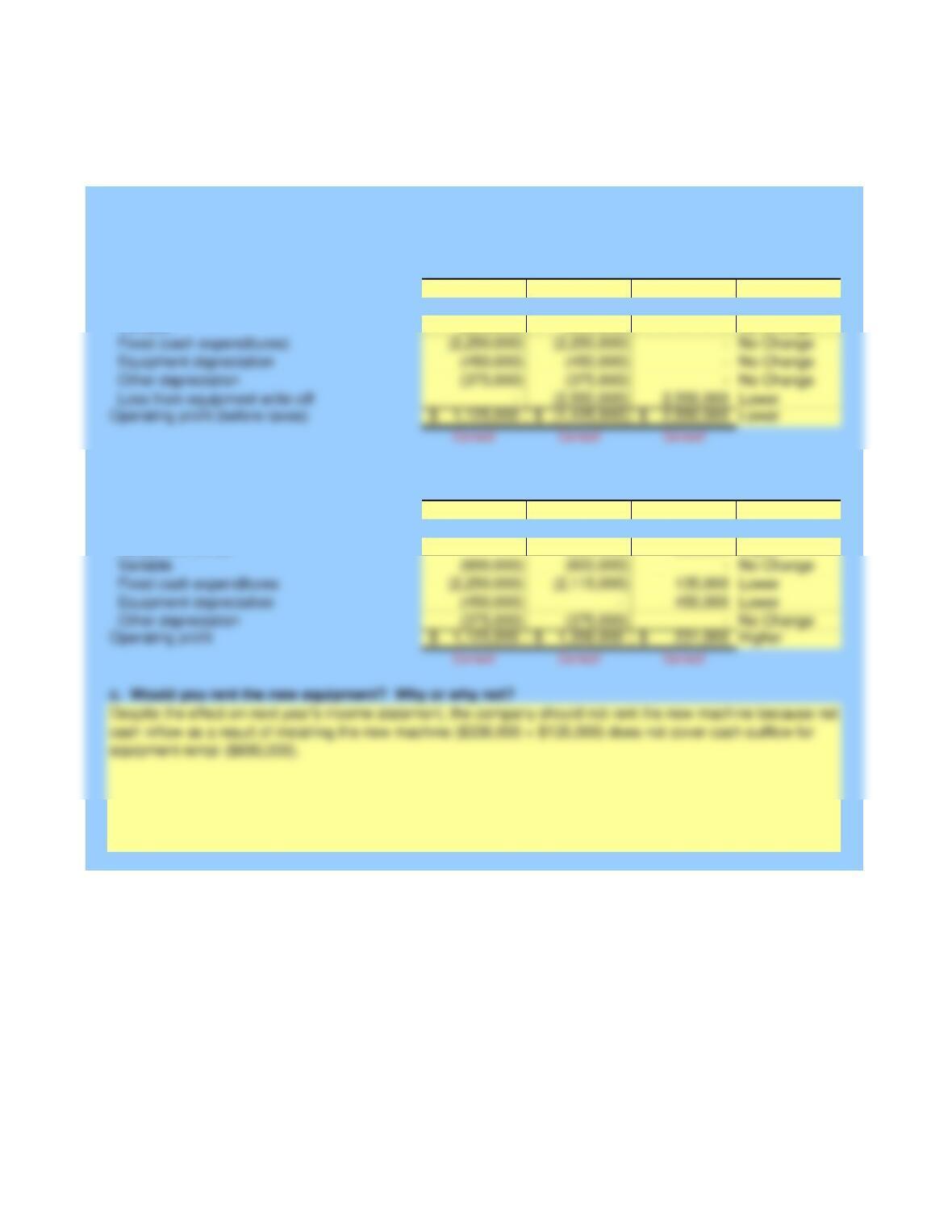

Baseline Rent

(status quo) Equipment Difference Change

4,800,000$ 4,800,000$ –$ No Change

(600,000) (600,000) – No Change

Baseline Rent

(status quo) Equipment Difference

Other depreciation

Equipment depreciation

Fixed cash expenditures

Variable

c. Would you rent the new equipment? Why or why not?

4,800,000$ 5,136,000$ 336,000$ Higher

– (690,000) 690,000 Higher

Instructor

McGraw-Hill/Irwin

Variable

Operating costs:

Sales Revenue

Integrative Case 2-69

a. This year’s income statement

Drive Systems Division (DSD)

Tunes2Go

Equipment rental

Operating costs:

Sales Revenue

b. Next year’s income statement

Loss from equipment write-off

Other depreciation

Equipment depreciation

Fixed (cash expenditures)

3,000,000$

690,000$

7%

No salvage value

Given Data IC2-69:

Tunes2Go

Percentage increase in DSD’s annual revenue

Annual rental charge for new testing machine

Cost of existing automated testing equipment

Drive Systems Division (DSD)

4,800,000$

Sales revenue

Percentage decrease in fixed cash expenditures

Variable operating costs

Fixed operating costs

Equipment depreciation

Other depreciation