Chapter 02 – The Accounting Cycle: During the Period

Chapter 2

The Accounting Cycle: During the Period

INSTRUCTOR’S MANUAL

Learning Objectives

LO2-1 Identify the basic steps in measuring external transactions.

LO2-2 Analyze the impact of external transactions on the accounting equation.

LO2-3 Assess whether the impact of external transactions results in a debit or credit to

an account balance.

LO2-4 Record transactions in a journal using debits and credits.

LO2-5 Post transactions to the general ledger.

LO2-6 Prepare a trial balance.

Chapter 02 – The Accounting Cycle: During the Period

Teaching Suggestions

Chapter 2 builds on the financial statements of Eagle Golf Academy presented in Chapter 1.

Part A provides 10 external transactions. Students first learn the impact that each transaction

has on the accounting equation and that the equation remains in balance after each transaction.

The first five transactions involve only the basic accounting equation (A = L + SE). The final

five transactions involve issues with the expanded accounting equation—revenue recognition,

expense recognition, and dividends. Illustration 2-3 is a useful tool to show students the

relationship between the basic accounting equation and the expanded accounting equation.

Part B introduces debits and credits and how to record transactions in a journal. The same 10

transactions in Part A are covered again in Part B using debits and credits. Debits and credits are

taught as the language of accounting (or terminology used to indicate an increase or decrease in

accounts). A journal entry is the sentence form of the accounting language. It’s important for

students to see debit and credit as accounting terms used to describe economic events.

Illustration 2-6 is the corollary to Illustration 2-3 and shows students how debits and credits are

used in the expanded accounting equation. Illustration 2-7 provides a simple memorization tool

to help students with debits and credits (DEALOR).

The chapter ends with a full summary of the transactions recorded in the journal (Illustration

2-11), the posting to the general ledger (Illustration 2-12), and the preparation of the trial balance

(Illustration 2-13).

At the end of this document, instructors will find a detailed illustration of the posting of

Eagle Golf Academy’s 10 transactions to the Cash general ledger account. The 10 transactions

correspond to those in Illustration 2-11, and the Cash account corresponds to the one shown in

Illustration 2-12. Students can see how each debit to the Cash account in a journal entry is posted

to the debit side of the general ledger account, increasing the balance. Similarly, credits to the

Cash account are posted to the credit side of the general ledger account, reducing the balance.

Chapter 02 – The Accounting Cycle: During the Period

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO2-1

Understand the difference between external and

internal transactions

5

2

LO2-1

List steps to measure external transactions

5

3

LO2-2

Explain the dual effect of transactions

5

4

LO2-2

Describe the impact of transactions on the

accounting equation

5

5

LO2-2

Explain the dual effect of transactions

5

6

LO2-3

Identify normal accounting balances

5

7

LO2-3

Understand the effects of debits and credits on

account balances

5

8

LO2-3

Determine whether a debit or credit increases an

account balance

5

9

LO2-3

Determine whether a debit or credit decreases an

account balance

5

10

LO2-3

Explain the relation between retained earnings and

its revenue and expense components

5

11

LO2-4

Describe a journal and a journal entry

5

12

LO2-4

Understand the proper format for recording

transactions

5

13

LO2-4

Explain why debits equal credits

5

14

LO2-4

Record transactions

5

15

LO2-4

Describe recorded transactions

5

16

LO2-5

Explain a T-account

5

17

LO2-5

Post transactions

5

18

LO2-5

Describe a general ledger

5

19

LO2-6

Describe a trial balance

5

20

LO2-6

Understand total debits and total credits in a trial

balance

5

Chapter 02 – The Accounting Cycle: During the Period

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE2-1

LO2-1

List steps in the measurement process

5

BE2-2

LO2-2

Balance the accounting equation

5

BE2-3

LO2-2

Balance the accounting equation

10

BE2-4

LO2-2

Analyze the impact of transactions on the

accounting equation

10

BE2-5

LO2-3

Understand the effect of debits and credits on

accounts

10

BE2-6

LO2-3

Understand the effect of debits and credits on

accounts

10

BE2-7

LO2-4

Record transactions

10

BE2-8

LO2-4

Record transactions

10

BE2-9

LO2-5

Analyze T-accounts

10

BE2-10

LO2-2, 2-3,

2-4, 2-5

Analyze the impact of transactions on the

accounting equation, record transactions, and post

10

BE2-11

LO2-6

Prepare a trial balance

10

BE2-12

LO2-6

Correct a trial balance

10

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E2-1

LO2-1

Identify terms associated with the measurement

process

5

E2-2

LO2-2

Analyze the impact of transactions on the

accounting equation

5

E2-3

LO2-2

Analyze the impact of transactions on the

accounting equation

10

E2-4

LO2-2

Analyze the impact of transactions on the

accounting equation

5

E2-5

LO2-2

Understand the components of retained earnings

10

E2-6

LO2-3

Indicate the debit or credit balance of accounts

10

E2-7

LO2-3

Associate debits and credits with external

transactions

5

E2-8

LO2-4

Record transactions

10

E2-9

LO2-4

Identify transactions

5

E2-10

LO2-4

Record transactions

15

E2-11

LO2-4

Record transactions

15

E2-12

LO2-4

Correct recorded transactions

15

E2-13

LO2-4

Correct recorded transactions

15

E2-14

LO2-5

Post transactions to Cash T-account

10

E2-15

LO2-5

Post transactions to T-accounts

15

E2-16

LO2-5

Identify transactions

10

E2-17

LO2-6

Prepare a trial balance

10

E2-18

LO2-6

Prepare a trial balance

10

E2-19

LO2-4, 2-5, 2-6

Record transactions, post to T-accounts, and prepare

a trial balance

30

E2-20

LO2-4, 2-5, 2-6

Record transactions, post to T-accounts, and prepare

a trial balance

30

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P2-1A

LO2-2

Analyze the impact of transactions on the

accounting equation

10

P2-2A

LO2-2

Analyze the impact of transactions on the

accounting equation

15

P2-3A

LO2-3

Identify the type of account and its normal debit or

credit balance

15

P2-4A

LO2-4

Record transactions

20

P2-5A

LO2-2, 2-4

Analyze the impact of transactions on the

accounting equation and record transactions

30

P2-6A

LO2-6

Prepare a trial balance

20

P2-7A

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

45

P2-8A

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

50

P2-9A

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

60

P2-1B

LO2-2

Analyze the impact of transactions on the

accounting equation

10

P2-2B

LO2-2

Analyze the impact of transactions on the

accounting equation

15

P2-3B

LO2-3

Identify the type of account and its normal debit or

credit balance

15

P2-4B

LO2-4

Record transactions

20

P2-5B

LO2-2, 2-4

Analyze the impact of transactions on the

accounting equation and record transactions

30

P2-6B

LO2-6

Prepare a trial balance

20

P2-7B

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

45

P2-8B

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

50

P2-9B

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

60

Chapter 02 – The Accounting Cycle: During the Period

Additional

Perspectives

Topic

Time

(Min.)

AP2-1

Continuing Problem: Great Adventures

45

AP2-2

Financial Analysis: American Eagle Outfitters, Inc.

15

AP2-3

Financial Analysis: The Buckle, Inc.

15

AP2-4

Comparative Analysis: American Eagle Outfitters, Inc. vs. The

Buckle, Inc.

15

AP2-5

Ethics

20

AP2-6

Internet Research

30

AP2-7

Written Communication

25

Chapter 02 – The Accounting Cycle: During the Period

Chapter Quiz Questions

The following multiple-choice questions are 10 unique quiz questions that correspond to the 10

questions at the end of each chapter. Each question covers the same learning objective but with a

little different twist. The correct answer is highlighted in bold for each item.

LO2-1

1. Which of the following does not represent an external business transaction?

LO2-1

2. Which step in the process of measuring external transactions involves assessing the equality

LO2-2

3. Which of the following transactions causes an increase in total liabilities?

a. Paying maintenance expenses for the current month.

LO2-2

4. Which of the following transactions causes a decrease in stockholders’ equity?

LO2-2

5. Which of the following is possible for a particular business transaction?

LO2-3

6. A debit is used to decrease which of the following accounts?

Chapter 02 – The Accounting Cycle: During the Period

LO2-3

7. A credit is used to decrease which of the following accounts?

a. Service Revenue.

LO2-4

8. Purchasing office supplies on account for $100 is recorded as:

a. Supplies

100

Accounts Payable

100

LO2-5

9. Transferring the debit and credit information from a journal to individual accounts in the

general ledger is referred to as:

LO2-6

10. Which of the following is true about a trial balance?

Chapter 02 – The Accounting Cycle: During the Period

Alternate Let’s Review

Problem #1

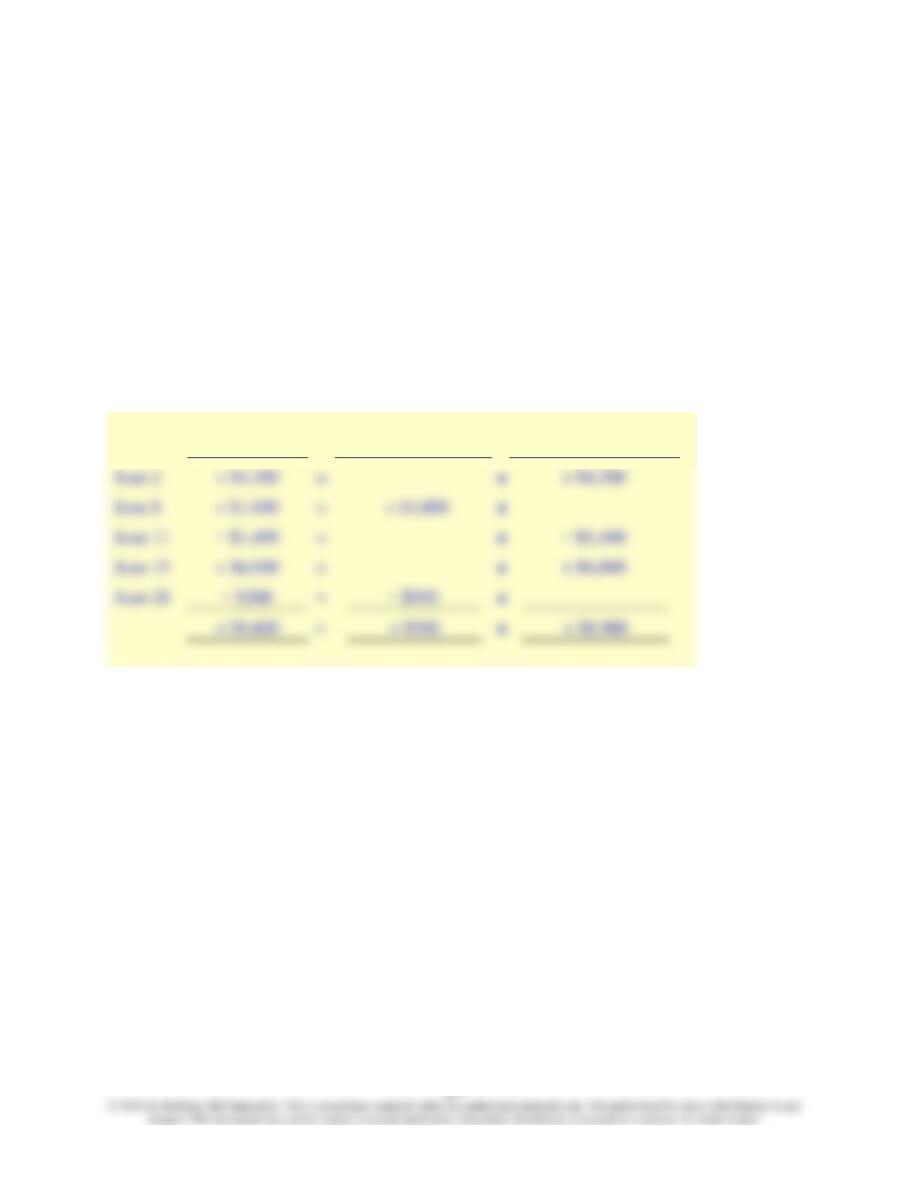

A company has the following transactions during June:

June 2 Provide services to customers for cash, $4,300

June 8 Purchase office supplies on account, $1,000

June 11 Pay workers’ salaries for the current period, $1,400

June 15 Issue additional shares of common stock, $6,000

June 28 Pay one-half of the amount owed for supplies purchased on June 8, $500

Required:

Indicate how each transaction affects the accounting equation.

Solution:

Assets

=

=

Liabilities

+

+

Stockholders’ Equity

Chapter 02 – The Accounting Cycle: During the Period

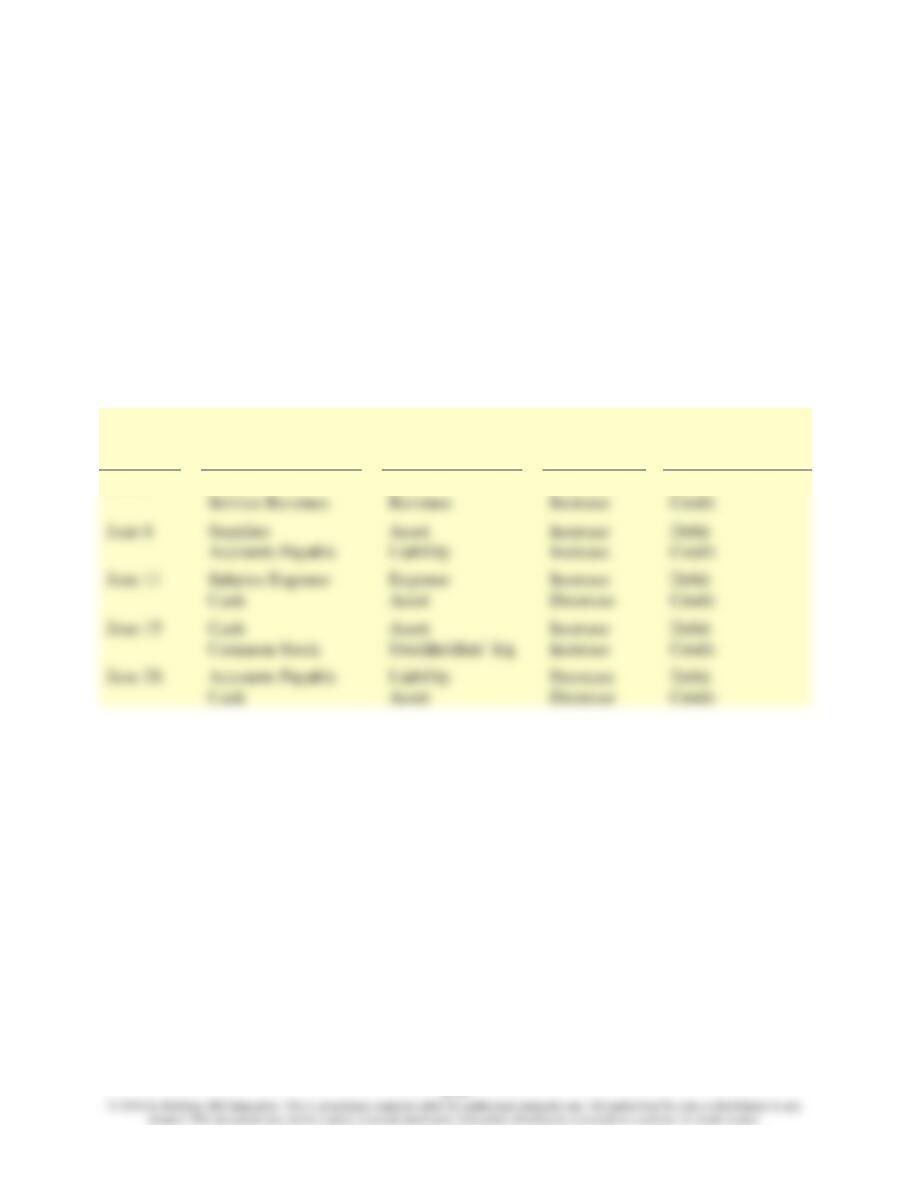

Problem #2

A company has the following transactions during June:

June 2 Provide services to customers for cash, $4,300

June 8 Purchase office supplies on account, $1,000

June 11 Pay workers’ salaries for the current period, $1,400

June 15 Issue additional shares of common stock, $6,000

June 28 Pay one-half of the amount owed for supplies purchased on June 8, $500

Required:

For each transaction, identify (1) the two accounts involved, (2) the type of account, (3) whether

the transaction increases or decreases the account balance, and (4) whether the increase or

decrease would be recorded with a debit or credit.

Solution:

Date

(1)

Accounts Involved

(2)

Account Type

(3)

Increase or

Decrease

(4)

Debit or Credit

June 2

Cash

Asset

Increase

Debit

June 8

Supplies

Asset

Increase

Debit

June 11

Salaries Expense

Expense

Increase

Debit

June 15

Cash

Asset

Increase

Debit

June 28

Accounts Payable

Liability

Decrease

Debit

Cash

Asset

Decrease

Credit

Chapter 02 – The Accounting Cycle: During the Period

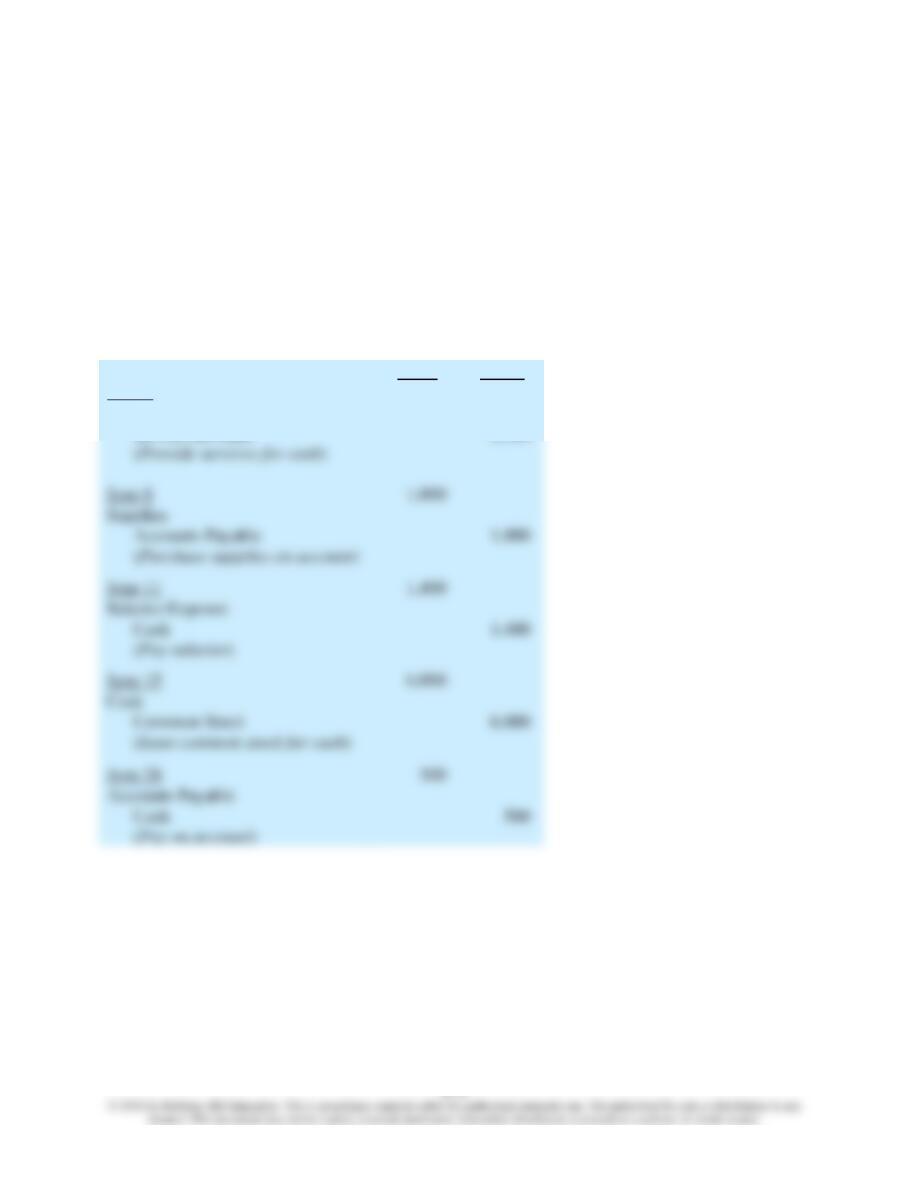

Problem #3

A company has the following transactions during June:

June 2 Provide services to customers for cash, $4,300

June 8 Purchase office supplies on account, $1,000

June 11 Pay workers’ salaries for the current period, $1,400

June 15 Issue additional shares of common stock, $6,000

June 28 Pay one-half of the amount owed for supplies purchased on June 8, $500

Required:

Record each transaction.

Solution:

Debit

Credit

June 2

Cash

4,300

June 8

Supplies

June 11

Salaries Expense

June 15

Cash

June 28

Accounts Payable

Service Revenue

4,300

Chapter 02 – The Accounting Cycle: During the Period

Key Points by Learning Objective

LO2-1 Identify the basic steps in measuring external transactions.

External transactions are transactions between the company and separate economic entities.

Internal transactions do not include an exchange with a separate economic entity.

LO2-2 Analyze the impact of external transactions on the accounting equation.

After each transaction, the accounting equation must always remain in balance. In other words,

assets always must equal liabilities plus stockholders’ equity.

LO2-3 Assess whether the impact of external transactions results in a debit or credit to an

account balance.

For the basic accounting equation (Assets = Liabilities + Stockholders’ Equity), assets (left side)

LO2-4 Record transactions in a journal using debits and credits.

LO2-5 Post transactions to the general ledger.

LO2-6 Prepare a trial balance.

Chapter 02 – The Accounting Cycle: During the Period

Common Mistakes

Common Mistake

Common Mistake

Don’t let the account name fool you. Even though the term revenue appears in the account title

Common Mistake

Common Mistake

Common Mistake

Common Mistake

Students sometimes hear the phrase “assets are the debit accounts” and believe it indicates that

assets can only be debited. This is incorrect! Assets, or any account, can be either debited or

Chapter 02 – The Accounting Cycle: During the Period

Common Mistake

Just because the debits and credits are equal in a trial balance does not necessarily mean that all

Chapter 02 – The Accounting Cycle: During the Period

Decision Points

Question

Accounting Information

Analysis

How much profit has

Retained earnings

The balance of retained earnings

Question

Accounting Information

Analysis

How does the

Journal entries

The effects of external transactions

Chapter 02 – The Accounting Cycle: During the Period

Career Corner

Career Corner

The accuracy of account balances is essential for providing useful information to decision

makers, such as investors and creditors. That’s why the Securities and Exchange Commission

Chapter 02 – The Accounting Cycle: During the Period

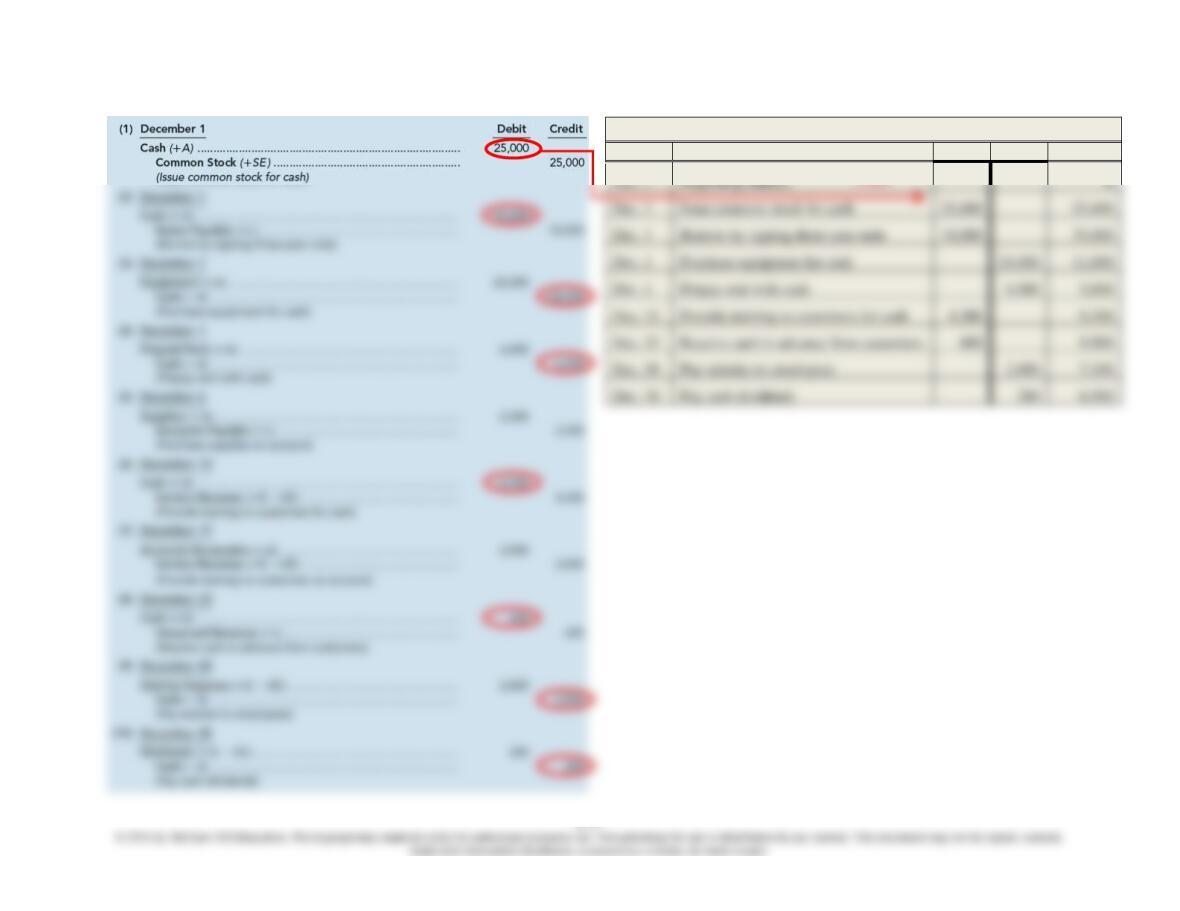

Posting Transactions of Eagle Golf Academy to the Cash General Ledger Account (Learning Objective 2-5)

Illustration 2-11, page 77

Cash account from Illustration 2-12, page 78

Dec. 1

Beginning balance

Dec. 1

Issue common stock for cash

25,000

Dec. 1

Borrow by signing three-year note

10,000

Dec. 1

Purchase equipment for cash

Dec. 1

Prepay rent with cash

Dec. 12

Provide training to customers for cash

Dec. 23

Receive cash in advance from customers

Dec. 28

Pay salaries to employees

Dec. 30

Pay cash dividends

Account: Cash

Date

Description

Debit

Credit

Balance

Post