COMPREHENSIVE PROBLEM 2

2 to 3 hours

Strong

Music-Is-Us, Inc.

A mini-practice set illustrating numerous aspects of the accounting cycle for a

merchandising business organized as a corporation. Students are expected to:

2 to 3 hours, Strong

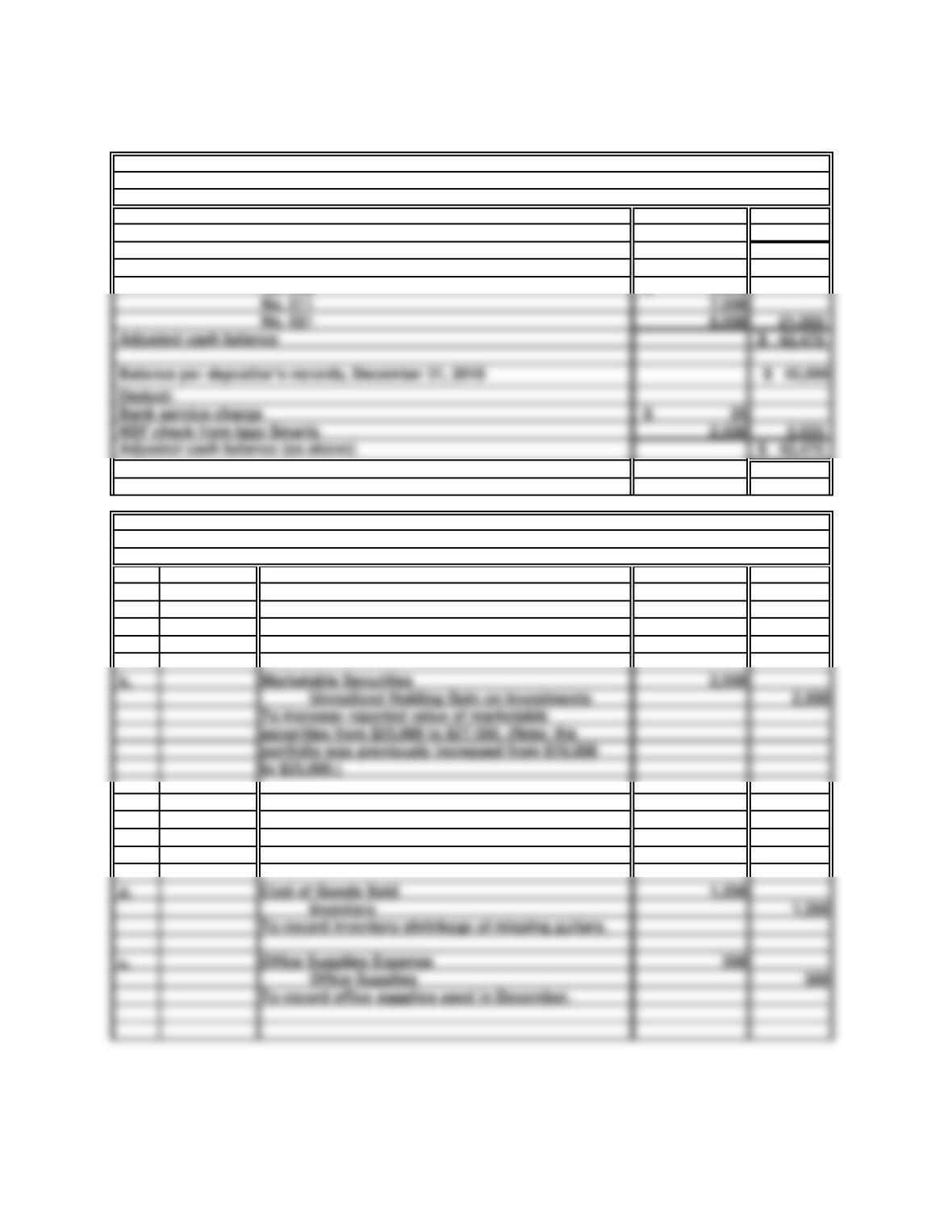

46,975$

16,500

$ 63,475

$ 5,500

a. 25

2,500

Cash 2,525

b. 2,500

Marketable Securities

Unrealized Holding Gain on Investments

securities from $25,000 to $27,500. (Note: the

To increase reported value of marketable

portfolio was previously increased from $19,000

to $25,000.)

c. 3,500

3,500

d. 1,350

e. 300

To record office supplies used in December.

To record inventory shrinkage of missing guitars.

Office Supplies Expense

Cost of Goods Sold

COMPREHENSIVE PROBLEM 2

Balance per bank statement, December 31, 2018

Add: Deposits in transit not recorded by bank

Deduct: Outstanding checks

No. 508

a.

December 31, 2018

MUSIC-IS-US

Bank Reconciliation

the NSF check received from Iggy Bates.

Bank Service Charges

December.

General Journal

Accounts Receivable

To record bank service charges for December and

To record uncollectible accounts expense for

Allowance for Doubtful Accounts

Uncollectible Accounts Expense

7,500

8,000 21,000

$ 25

2,500 2,525

No. 511

No. 521

Adjusted cash balance

Deduct:

Bank service charge

NSF check from Iggy Smarts

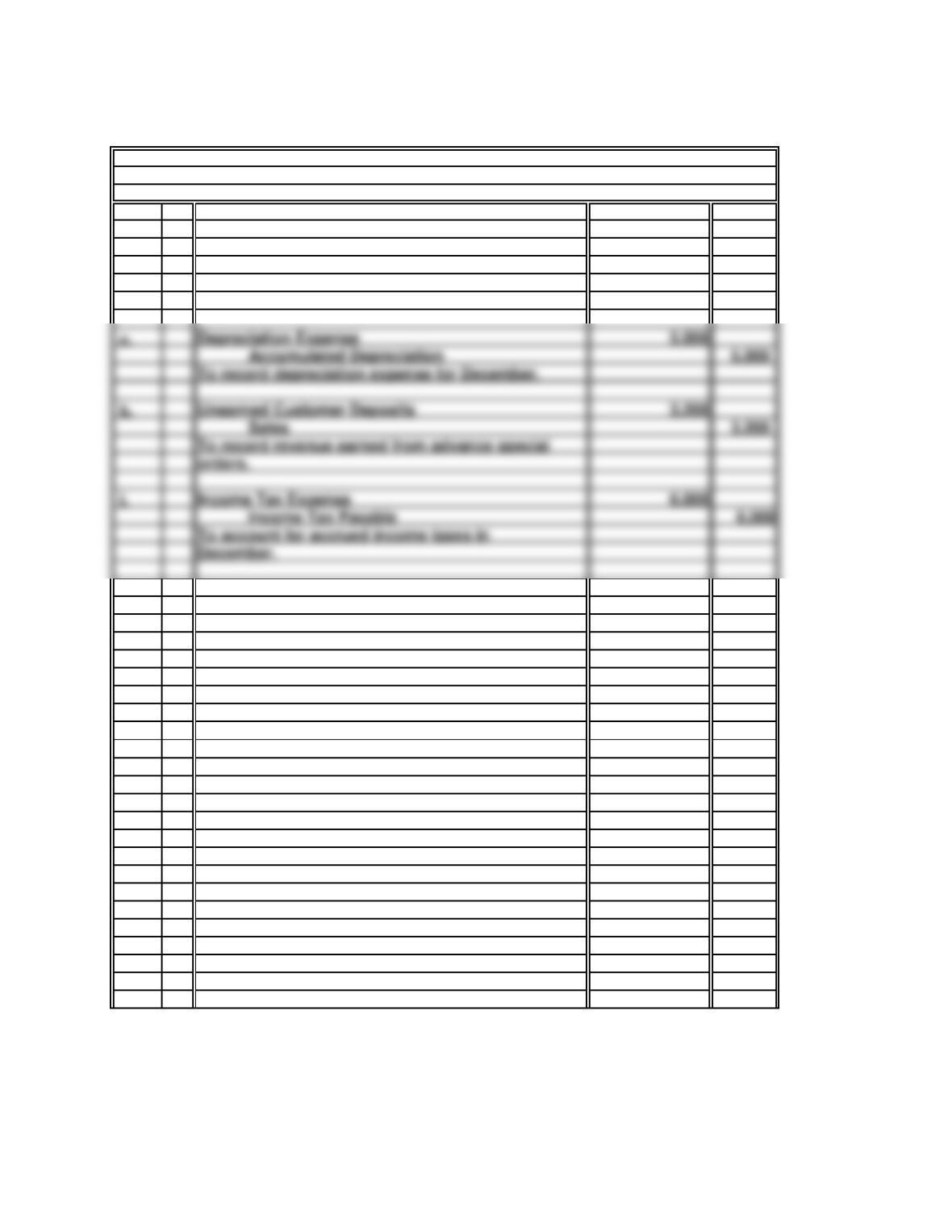

f. 600

Prepaid Insurance 600

COMPREHENSIVE PROBLEM 2

December. (Note: One month of the twelve-month

To record insurance policies expired during

General Journal

Insurance Expense

policy had already been accounted for in

November).

g. 5,000

h. 3,200

i. 6,000

Income Tax Payable 6,000

orders.

Income Tax Expense

December.

To record depreciation expense for December.

Unearned Customer Deposits

To record revenue earned from advance special

To account for accrued income taxes in

Depreciation Expense

Cash $ 42,475

27,500

127,500

8,500$

70,000

4,800

81,000

1,000,000

240,200

8,500

1,603,200

959,350

225

12,500

395,000

700

7,000

3,600

53,000

81,000

$ 3,821,200 $ 3,821,200

Office supplies expense

Insurance expense

Utilities expense

Income tax expense

Uncollectible accounts expense

Depreciation expense

Cost of goods sold

Bank service charges

Salary and wages expense

j.

Unrealized holding gain on investments

Unearned customer deposits

Retained earnings

COMPREHENSIVE PROBLEM 2

Adjusted Trial Balance

As of December 31, 2018

Allowance for doubtful accounts

MUSIC-IS-US

Marketable securities

Accounts receivable

Income taxes payable

Capital stock

Sales

Accounts payable

248,650

900

6,000

1,791,000

805,000

64,800

Office supplies

Prepaid insurance

Building and fixtures

Merchandise inventory

Accumulated depreciation

Land

k.

1,603,200$

959,350

240,200$

Add: Net income (from income statement)

Ending Retained earnings, December 31, 2018

COMPREHENSIVE PROBLEM 2

MUSIC-IS-US (continued)

MUSIC-IS-US

Statement of Retained Earnings

Retained earnings, January 1, 2018

For the Year Ending December 31, 2018

MUSIC-IS-US

Income Statement

For the Year Ended December 31, 2018

Sales

Cost of goods sold

Income before income tax

Net income

Insurance expense

Utilities expense

Depreciation expense

Income taxes expense

Bank service charges

Uncollectible accounts expense

Salary and wages expense

Office supplies expense

Gross profit

k. (continued)

42,475$

27,500

444,525$

1,791,000$

Total assets

Total plant and equipment

Less: Accumulated depreciation

Land

70,000$

4,800

Long-term liabilities:

Income taxes payable

Total current liabilities

1,000,000$

331,025

Total Liabilities and Stockholders’ Equity

Total stockholders’ equity

Unrealized holding gain on investments

COMPREHENSIVE PROBLEM 2

Building and fixtures

MUSIC-IS-US

Balance Sheet

As of December 31, 2018

Current assets:

Marketable securities

Cash

Total current assets

Plant and equipment:

Stockholders’ Equity

Capital stock

Liabilities

Current liabilities:

Accounts payable

Unearned customer deposits

Total liabilities

Retained earnings (from statement of retained earnings)

$ 127,500

6,000

Office supplies

Prepaid insurance

Merchandise inventory

Accounts receivable

Less: Allowance for doubtful accounts

l. Step 1:

m. Step 1:

$959,350 ÷ $248,650* = 3.9 times

365 ÷ 3.9 = 94 days

Compute inventory days (365 ÷ inventory turnover)

27 days

Add: inventory days (from part m above)

Operating cycle

o.

n.

Compute inventory turnover (cost of goods sold ÷ average merchandise

Compute accounts receivable turnover (sales ÷ average accounts receivable)

$1,603,200 ÷ $119,000* = 13.5 times

From a short-term creditor’s perspective, the company appears relatively solvent. It

collects its accounts receivable in less than 30 days, and its uncollectible accounts

Accounts receivable days (from part l above)

Compute accounts receivable days (365 ÷ accounts receivable turnover)

365 ÷ 13.5 = 27 days