1. An account is a form designed to record changes in a particular asset, liability, owner’s equity,

revenue, or expense. A ledger is a group of related accounts.

2. The terms debit and credit may signify either an increase or a decrease, depending upon the nature

of the account. For example, debits signify an increase in asset and expense accounts but a decrease

in liability, owner’s capital, and revenue accounts.

3. a. Assuming no errors have occurred, the credit balance in the cash account resulted from drawing

checks for $1,850 in excess of the amount of cash on deposit.

b. The $1,850 credit balance in the cash account as of December 31 is a liability owed to the bank.

It is usually referred to as an “overdraft” and should be classified on the balance sheet as a

liability.

4. a. The revenue was earned in October.

b. (1) Debit Accounts Receivable and credit Fees Earned or another appropriately titled revenue

account in October.

(2) Debit Cash and credit Accounts Receivable in November.

5. No. Errors may have been made that had the same erroneous effect on both debits and credits, such

as failure to record and/or post a transaction, recording the same transaction more than once, and

p

osting a transaction correctly but to the wrong account.

6. The listing of $9,800 is a transposition; the listing of $100 is a slide.

7. a. No. Because the same error occurred on both the debit side and the credit side of the trial

b

alance, the trial balance would not be out of balance.

b. Yes. The trial balance would not balance. The error would cause the debit total of the trial

b

alance to exceed the credit total by $90.

8. a. The equality of the trial balance would not be affected.

b. On the income statement, total operating expenses (salary expense) would be overstated by

$7,500, and net income would be understated by $7,500. On the statement of owner’s equity,

the beginning and ending capital would be correct. However, net income and withdrawals

would be understated by $7,500. These understatements offset one another, and thus, ending

owner’s equity is correct. The balance sheet is not affected by the error.

9. a. The equality of the trial balance would not be affected.

b. On the income statement, revenues (fees earned) would be overstated by $300,000, and net

income would be overstated by $300,000. On the statement of owner’s equity, the beginning

capital would be correct. However, net income and ending capital would be overstated by

$300,000. The balance sheet total assets is correct. However, liabilities (notes payable) is

understated by $300,000, and owner’s equity is overstated by $300,000. The understatement

of liabilities is offset by the overstatement of owner’s equity, and thus, total liabilities and

owner’s equity is correct.

10. a. From the viewpoint of Surety Storage, the balance of the checking account represents an asset.

b. From the viewpoint of Ada Savings Bank, the balance of the checking account represents a

liability.

CHAPTER 2

ANALYZING TRANSACTIONS

DISCUSSION QUESTIONS

2-1

CHAPTER 2 Analyzing Transactions

PE 2–1A

1. Debit and credit entries, normal debit balance

2. Credit entries only, normal credit balance

3. Debit and credit entries, normal credit balance

PE 2–1B

1. Debit and credit entries, normal credit balance

2. Debit and credit entries, normal debit balance

3. Debit entries only, normal debit balance

PE 2–2A

Oct. 27 Office Equipment 32,750

PE 2–2B

Sept. 30 Office Supplies 2,500

Cash 800

Accounts Payable 1,700

PRACTICE EXERCISES

2-2

CHAPTER 2 Analyzing Transactions

PE 2–3A

Mar. 16 Accounts Receivable 9,450

PE 2–3B

Aug. 13 Cash 9,000

PE 2–4A

Dec. 23 Steve Buckley, Drawing 20,000

PE 2–4B

June 30 Dawn Pierce, Drawing 11,500

PE 2–5A

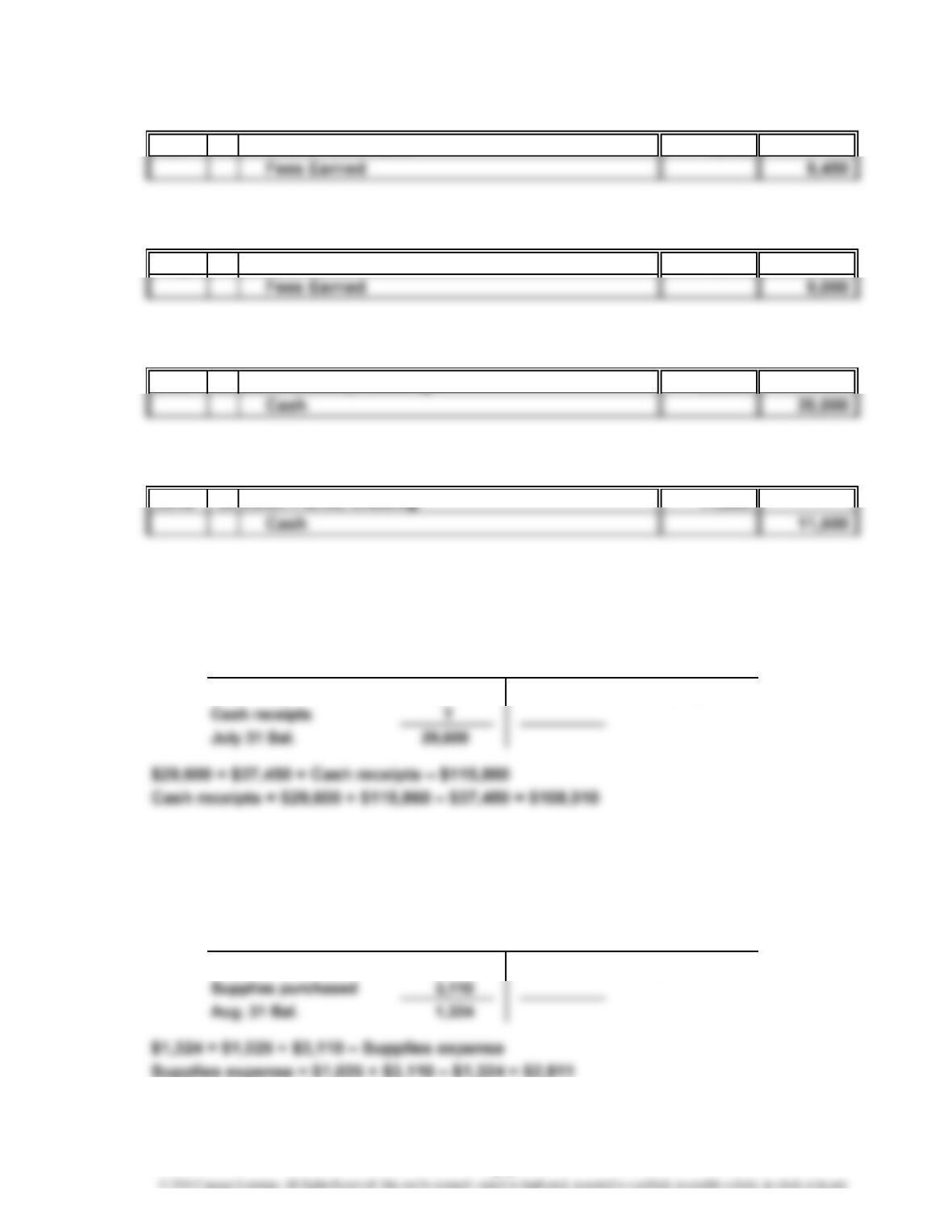

Using the following T account, solve for the amount of cash receipts (indicated

by ? below).

July 1 Bal. 37,450 115,860 Cash payments

PE 2–5B

Using the following T account, solve for the amount of supplies expense

(indicated by ? below).

Aug. 1 Bal. 1,025 ? Supplies expense

Cash

Supplies

2-3

PE 2–6A

a. The totals are unequal. The debit total is higher by $900 ($5,400 – $4,500).

PE 2–6B

a. The totals are equal because both the debit and credit entries were journalized

PE 2–7A

a. Rent Expense 4,650

Miscellaneous Expense 4,650

b. Accounts Payable 3,700

Accounts Receivable 3,700

2-4

CHAPTER 2 Analyzing Transactions

PE 2–7B

a. Cash 8,400

b. Supplies 2,500

Office Equipment 2,500

Supplies 2,500

Accounts Payable 2,500

PE 2–8A

2016 2015 Amount Percent

Fees earned $680,000 $850,000 $(170,000) –20.0%

PE 2–8B

2016 2015 Amount Percent

Fees earned $1,416,000 $1,200,000 $216,000 18.0%

Fuller Company

Income Statements

For Years Ended December 31

Increase/(Decrease)

Increase/(Decrease)

Paragon Company

Income Statements

For Years Ended December 31

2-5

CHAPTER 2 Analyzing Transactions

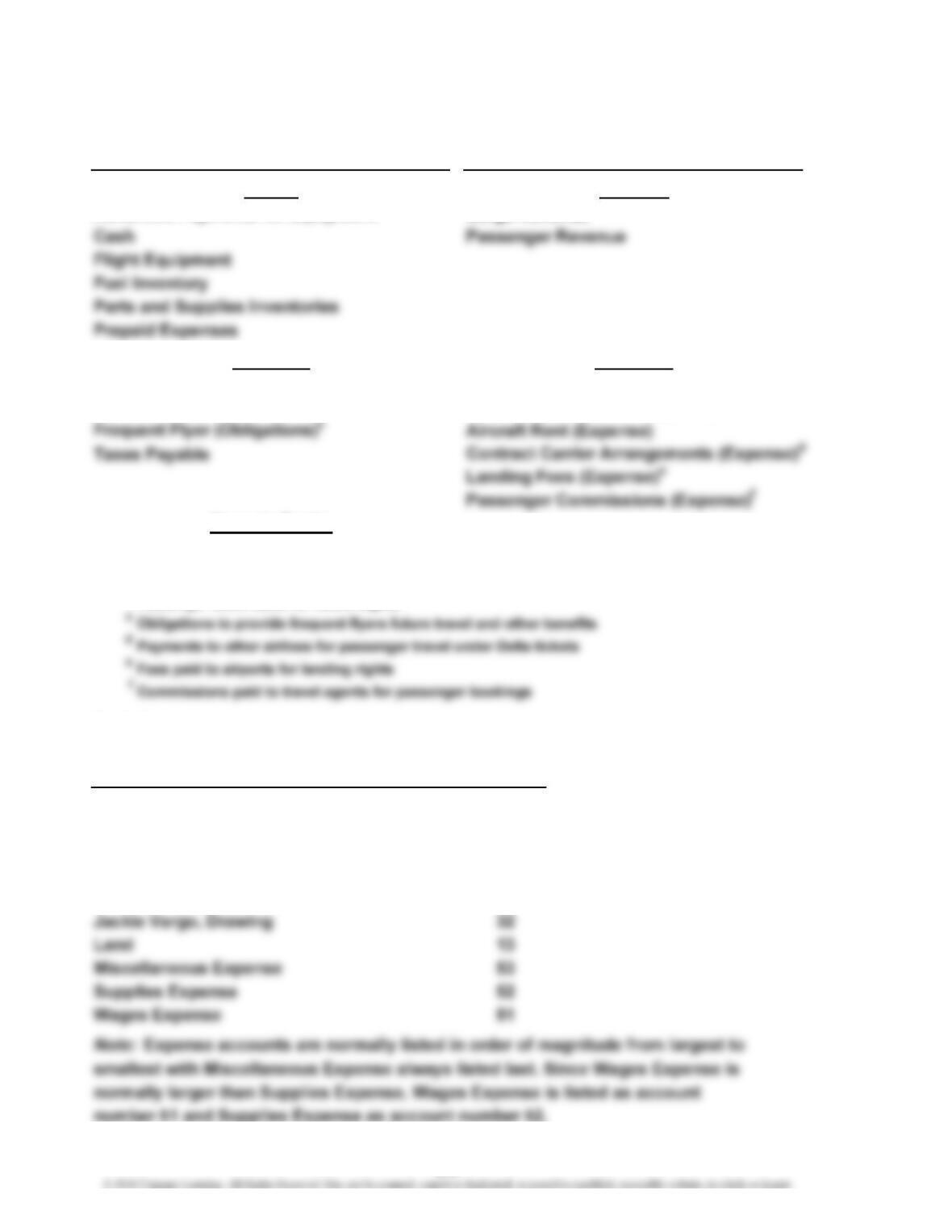

Ex. 2–1

Advanced Payments for EquipmentaCargo Revenue

Accounts Payable Aircraft Fuel (Expense)

Air Traffic LiabilitybAircraft Maintenance (Expense)

None

aAdvance payments (deposits) on aircraft to be delivered in the future

bPassenger ticket sales for future flights

Ex. 2–2

Account

Number

Accounts Payable 21

Accounts Receivable 12

Cash 11

Fees Earned 41

Jackie Vargo, Capital 31

Expenses

Liabilities

Owner’s Equity

Account

EXERCISES

Assets Revenue

Balance Sheet Accounts Income Statement Accounts

2-6

CHAPTER 2 Analyzing Transactions

Ex. 2–3

11 Cash 41 Fees Earned

59 Miscellaneous Expense

31 Ivy Bishop, Capital

32 Ivy Bishop, Drawing

Note: The order of some of the accounts within the major classifications is

Ex. 2–4

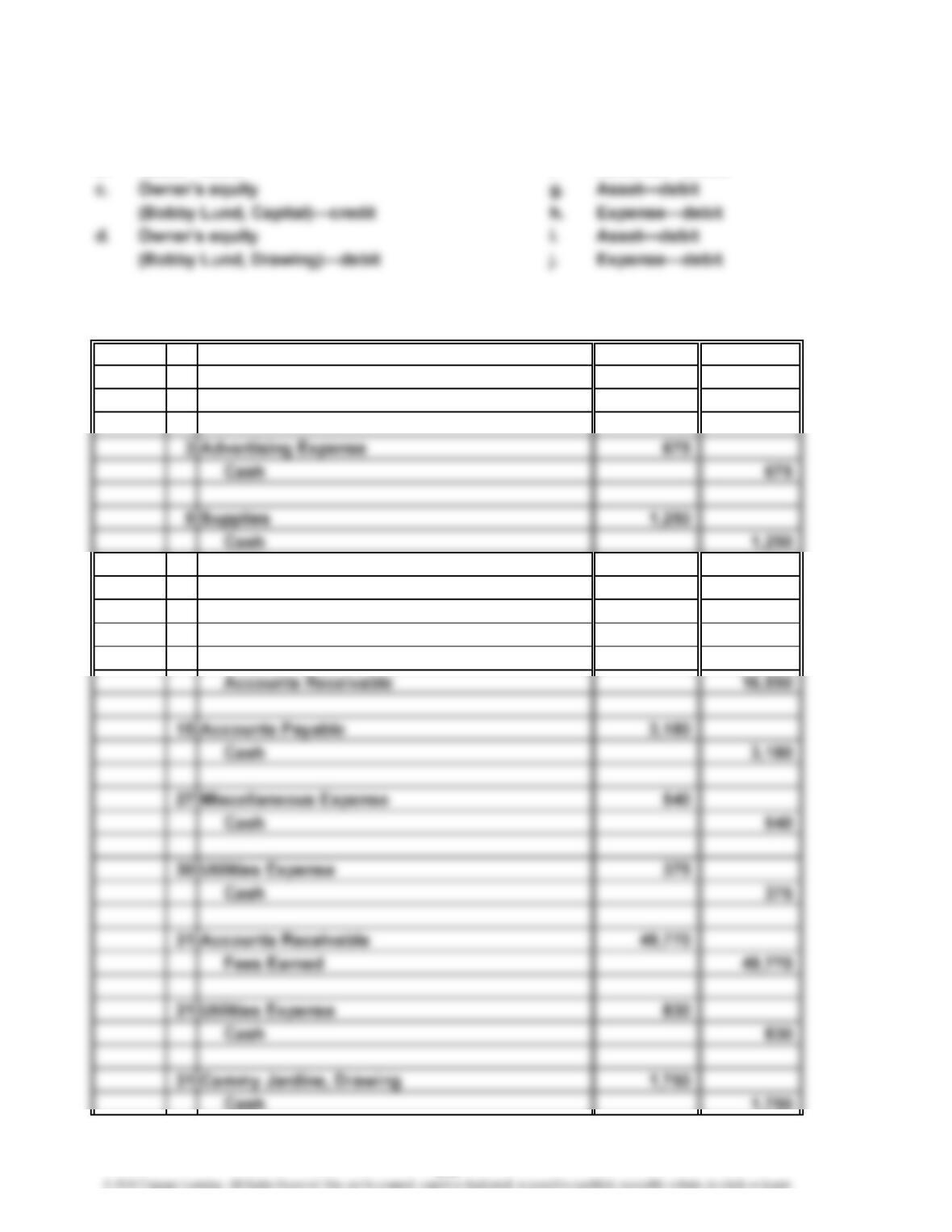

a. debit g. debit

b. credit h. credit

Ex. 2–5

2. debit and credit entries (c)

4. credit entries only (b)

6. debit entries only (a)

2. Liabilities

3. Owner’s Equity

1. Assets 4. Revenue

Balance Sheet Accounts Income Statement Accounts

2-7

CHAPTER 2 Analyzing Transactions

Ex. 2–6

a. Liability—credit e. Asset—debit

b. Asset—debit f. Revenue—credit

Ex. 2–7

2016

March 1 Rent Expense 2,500

Cash 2,500

6 Office Equipment 9,500

Accounts Payable 9,500

10 Cash 16,550

2-8

CHAPTER 2 Analyzing Transactions

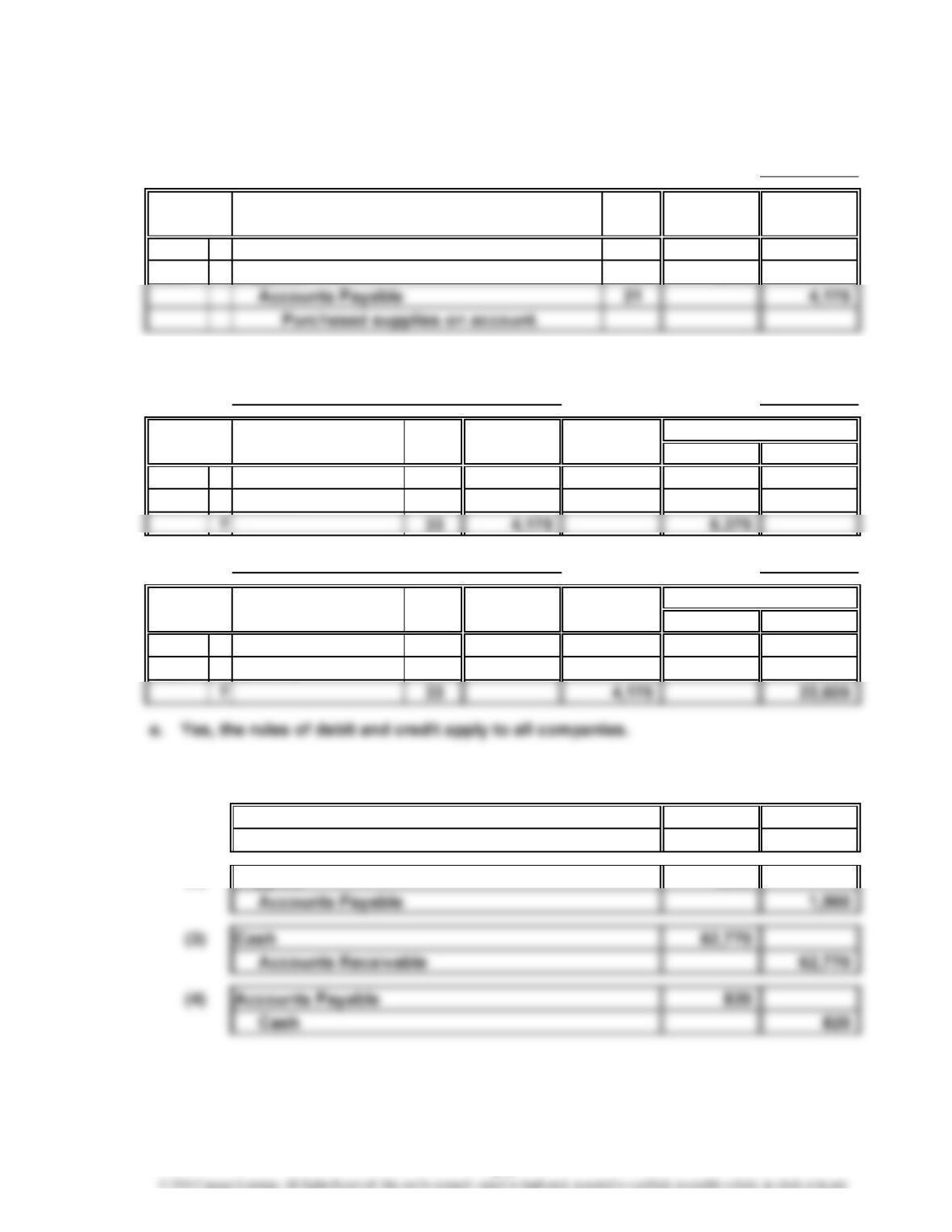

Ex. 2–8

a.

Page 33

Post.

Ref. Debit Credit

2016

Jan. 7 Supplies 15 4,175

b., c., d.

Account No. 15

Post.

Ref. Debit Debit Credit

2016

Jan. 1 Balance 2,200

Account No. 21

Post.

Ref. Debit Debit Credit

2016

Jan. 1 Balance 18,430

Ex. 2–9

a. (1) Accounts Receivable 73,900

Fees Earned 73,900

(2) Supplies 1,960

Balance

Credit

Balance

JOURNAL

Account:

Account: Supplies

Accounts Payable

Date

Date Description

Date Item

Item

Credit

2-9

CHAPTER 2 Analyzing Transactions

Ex. 2–9 (Concluded)

b.

(3) 62,770 (4) 820 (4) 820 (2) 1,960

c. No, an error may not have necessarily occurred. A credit balance

in Accounts Receivable could occur if a customer overpaid his or

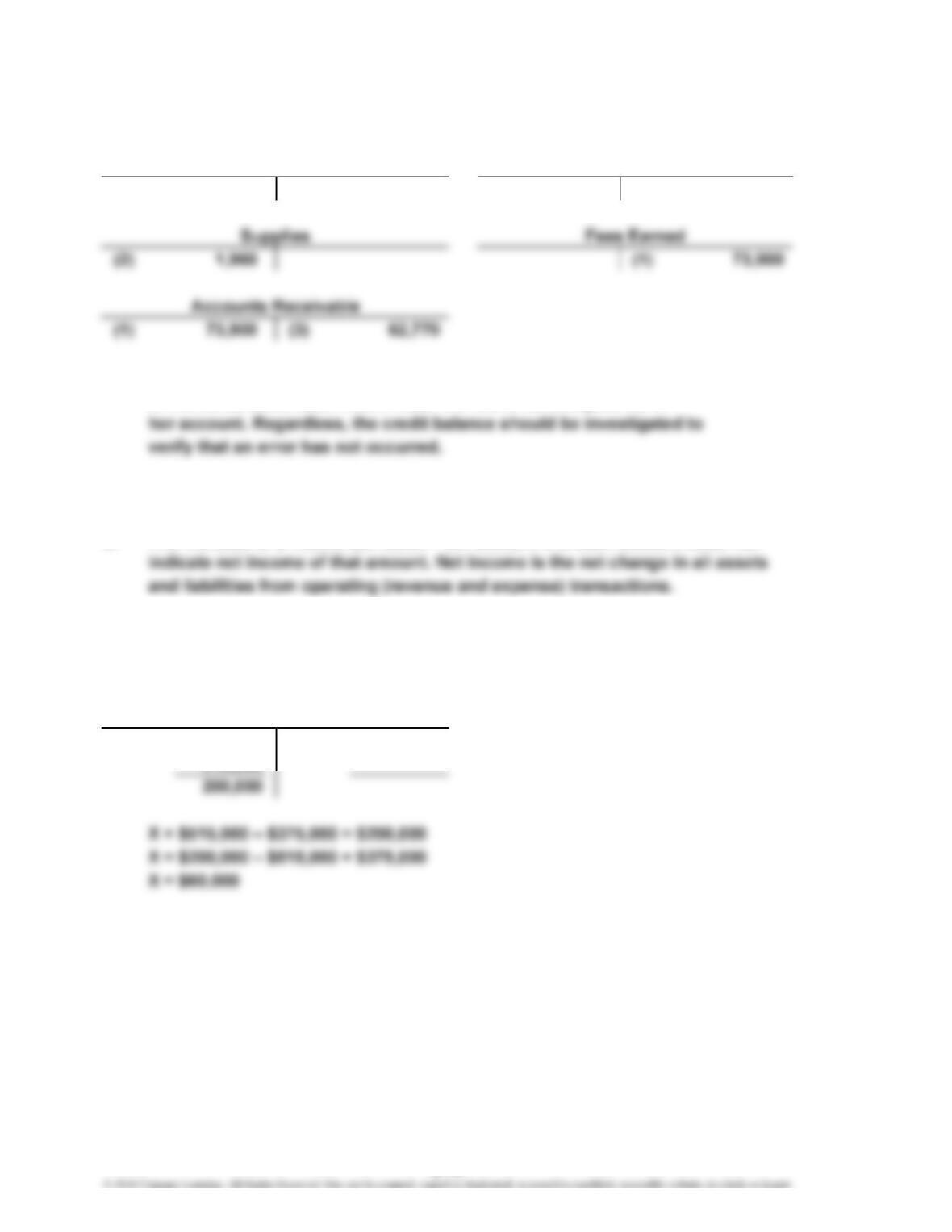

Ex. 2–10

a. The increase of $140,000 ($515,000 – $375,000) in the cash account does not

b. $60,000 ($200,000 – $140,000)

or

X 375,000

515,000

Cash

Cash Accounts Payable

2-10

CHAPTER 2 Analyzing Transactions

Ex. 2–11

a.

Feb. 1 X

186,500 201,400

b.

Oct. 1 115,800 449,600

X

c.

Apr. 1 46,220 X

248,600

Ex. 2–12

a. Debit (negative) balance of $16,000 ($314,000 – $10,000 – $320,000). This

Cash

Accounts Payable

Accounts Receivable

2-11

CHAPTER 2 Analyzing Transactions

Ex. 2–13

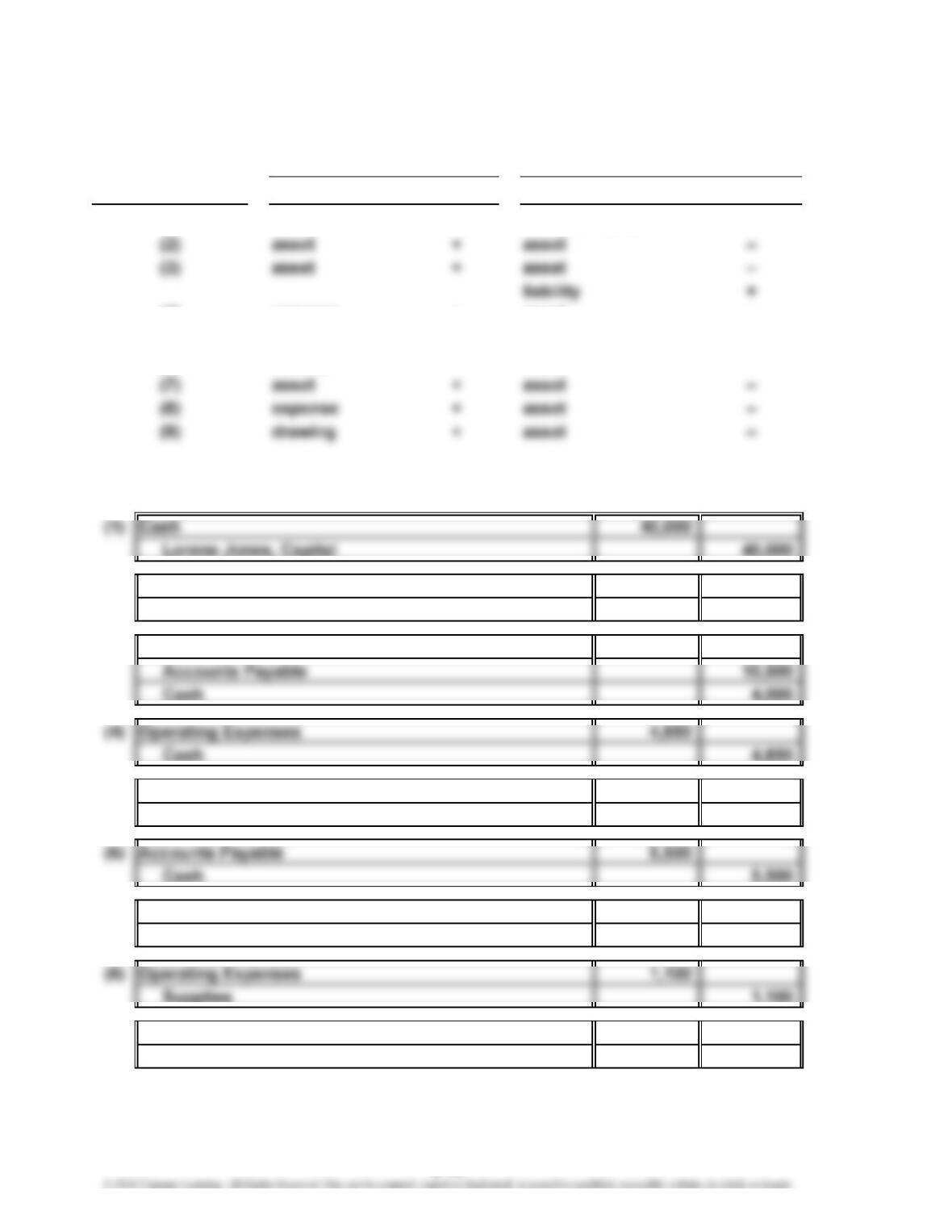

a. and b.

Effect Type Effect

asset + owner’s equity +

expense + asset –

asset + revenue +

liability – asset –

Ex. 2–14

(2) Supplies 2,500

Cash 2,500

(3) Equipment 14,500

(5) Accounts Receivable 13,800

Service Revenue 13,800

(7) Cash 8,700

Accounts Receivable 8,700

(9) Lorene Jones, Drawing 3,000

Cash 3,000

(4)

(5)

(6)

Account Debited Account Credited

Type

(1)

Transaction

2-12

CHAPTER 2 Analyzing Transactions

Ex. 2–15

a.

Debit Credit

Balances Balances

Cash 28,850

Accounts Receivable 5,100

WYOMING TOURS CO.

Unadjusted Trial Balance

June 30, 2016

2-13

CHAPTER 2 Analyzing Transactions

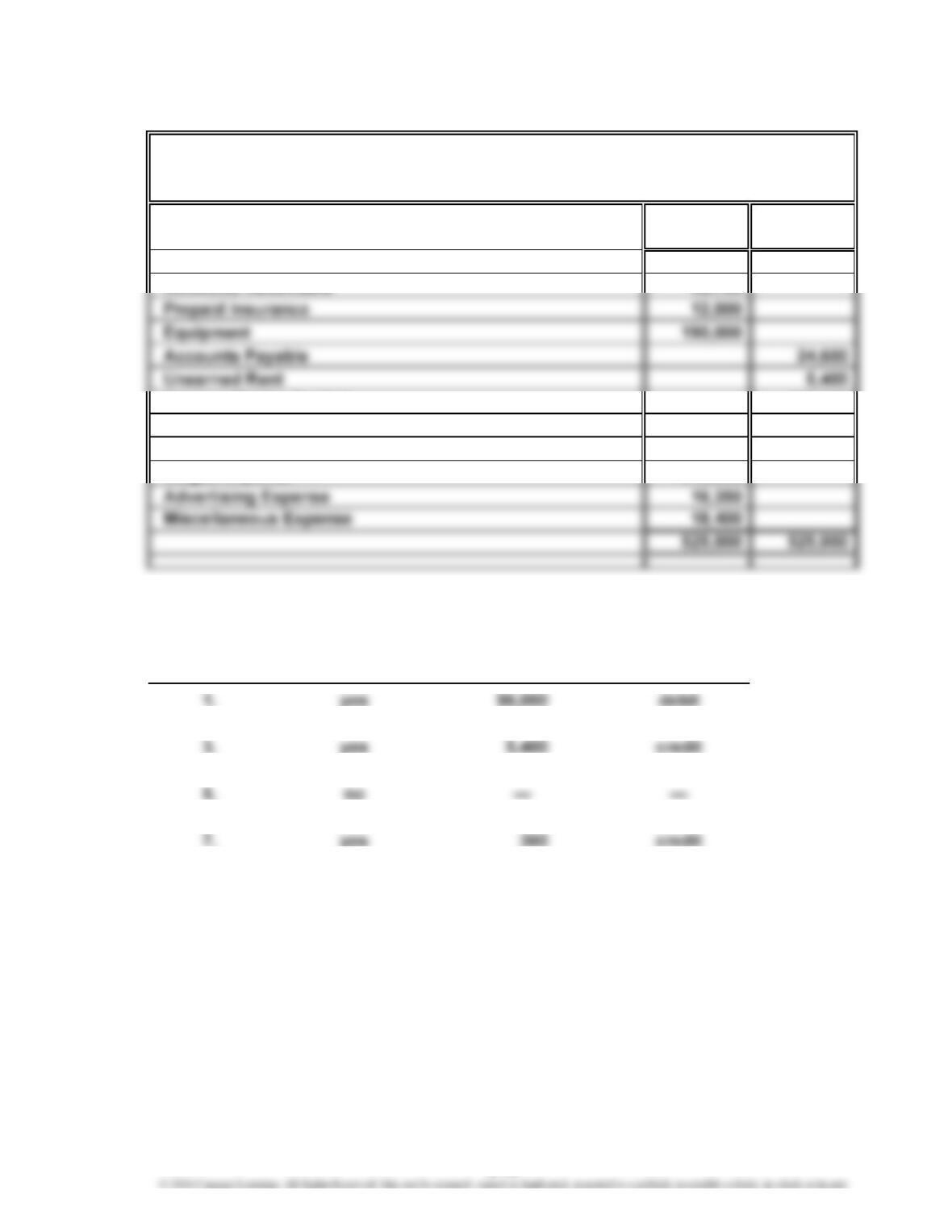

Ex. 2–16

Debit Credit

Balances Balances

Cash 33,320

Accounts Payable 42,770

Unearned Rent 12,000

Notes Payable 50,000

Elaine Wells, Capital 75,000

Elaine Wells, Drawing 24,000

Fees Earned 745,230

Wages Expense 580,700

Rent Expense 48,000

Ex. 2–17

Inequality of trial balance totals would be caused by errors described in (c) and

(e). For (c), the debit total would exceed the credit total by $9,900 ($4,950 + $4,950).

For (e), the credit total would exceed the debit total by $17,100 ($19,000 – $1,900).

HICKORY FURNITURE COMPANY

Unadjusted Trial Balance

December 31, 2016

2-14

CHAPTER 2 Analyzing Transactions

Ex. 2–18

Debit Credit

Balances Balances

Cash 15,500

Accounts Receivable 46,750

Carmen Meeks, Capital 110,000

Carmen Meeks, Drawing 13,000

Service Revenue 385,000

Wages Expense 213,000

Ex. 2–19

(a) (b)

Error Out of Balance Difference

2. no —

4. yes 480

6. yes 90

(c)

Larger Total

RANGER CO.

Unadjusted Trial Balance

August 31, 2016

debit

—

credit

2-15

CHAPTER 2 Analyzing Transactions

Ex. 2–20

1. The Debit column total is added incorrectly. The sum is $890,700 rather than

$1,189,300.

3. The Accounts Receivable balance should be in the Debit column.

5. The Samuel Parson, Drawing, balance should be in the Debit column.

6. The Advertising Expense balance should be in the Debit column.

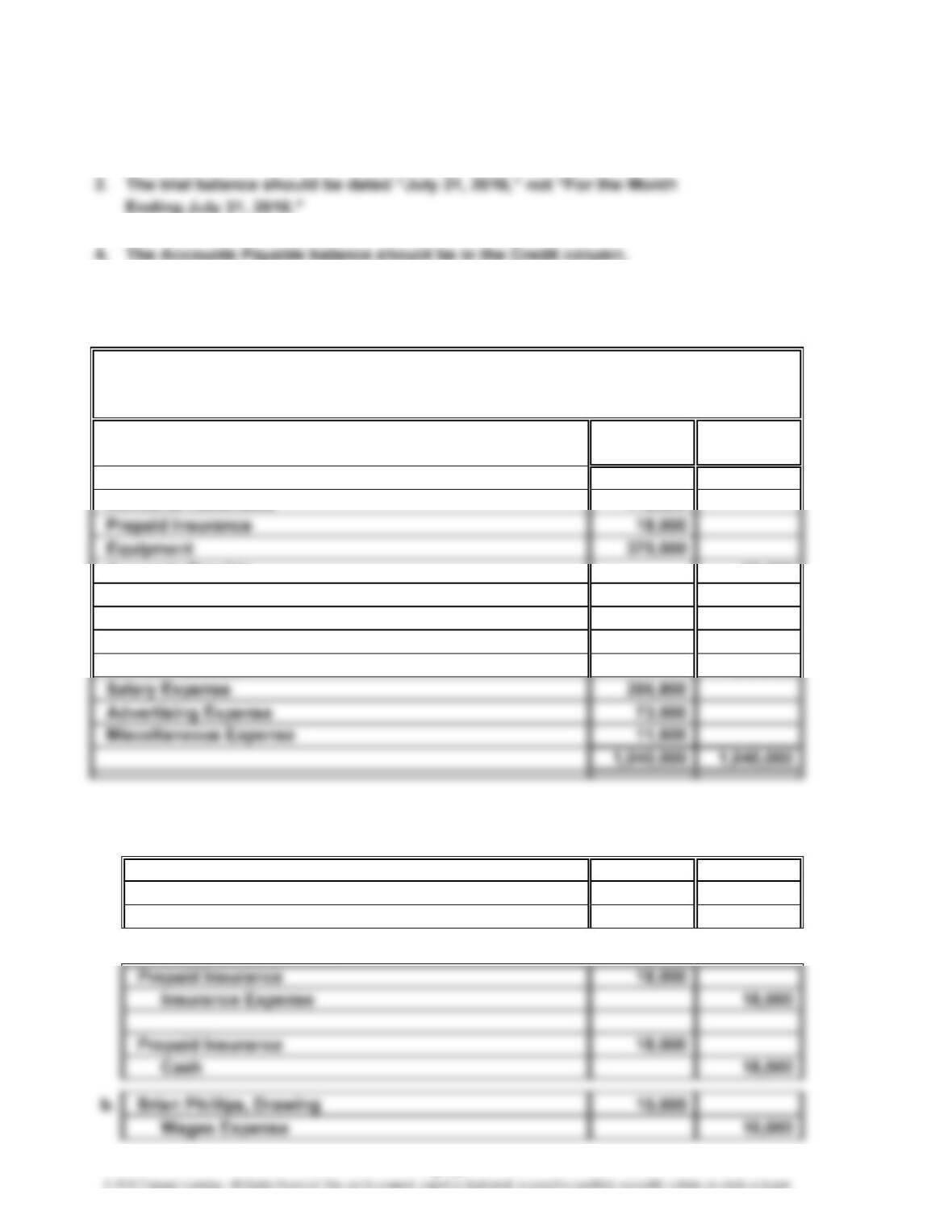

A corrected trial balance would be as follows:

Debit Credit

Balances Balances

Cash 36,000

Accounts Receivable 112,600

Accounts Payable 53,300

Salaries Payable 7,500

Samuel Parson, Capital 297,200

Samuel Parson, Drawing 17,000

Service Revenue 682,000

Ex. 2–21

a. The correction could be made with one or two entries as shown below.

Prepaid Insurance 36,000

Insurance Expense 18,000

Cash 18,000

or (reverses original entry)

MASCOT CO.

Unadjusted Trial Balance

July 31, 2016

2-16

CHAPTER 2 Analyzing Transactions

Ex. 2–22

a. Cash 17,600

Fees Earned 8,800

Accounts Receivable 8,800

Ex. 2–23

a. 1. Revenue:

2. Operating expenses:

3. Operating income:

b. During the recent year, revenue increased by 3.7%, while operating expenses

2-17

CHAPTER 2 Analyzing Transactions

Ex. 2–24

a. 1. Revenue:

$25,101 million increase ($446,950 – $421,849)

2. Operating expenses:

$24,085 million increase ($420,392 – $396,307)

3. Operating income:

b. During the recent year, revenue increased by 6.0%, while operating expenses

from the prior year.

c. Because of the size differences between Target and Walmart (Walmart has

more than 6 times the revenue), it is best to compare the two companies on the

2-18

CHAPTER 2 Analyzing Transactions

Prob. 2–1A

1. and 2.

(a) 18,000 (b) 1,950 (d) 4,500

(g) 13,650 (c) 5,700

(e) 1,875

(l) 21,900 (a) 18,000

(f) 3,600 (m) 4,100

(c) 28,500 (k) 3,750

PROBLEMS

Notes Payable

Professional FeesSupplies

Prepaid Insurance Salary Expense

Automobiles Blueprint Expense

Cash Equipment

Accounts Receivable Kimberly Manis, Capital

2-19

CHAPTER 2 Analyzing Transactions

Prob. 2–1A (Concluded)

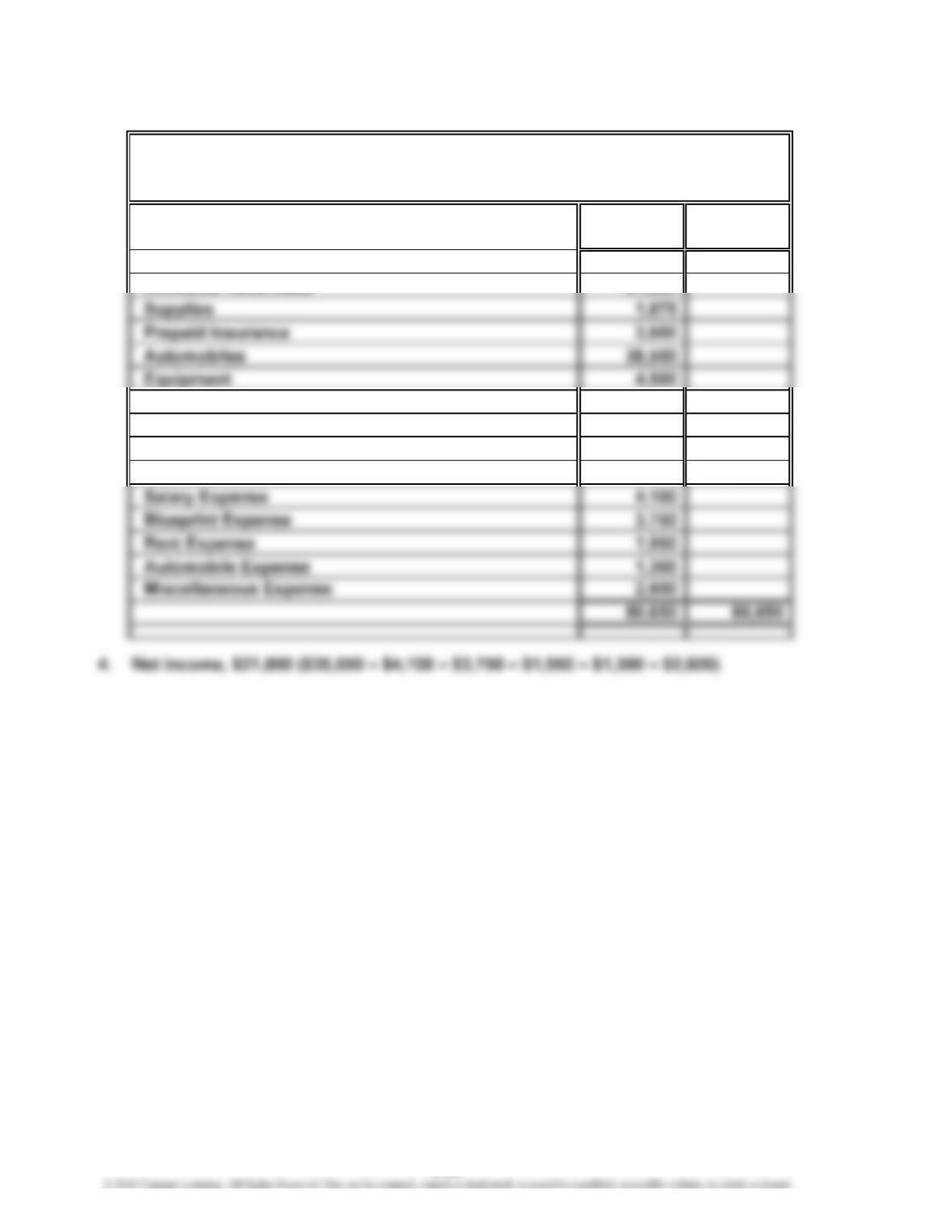

3.

Debit Credit

Balances Balances

Cash 6,575

Accounts Receivable 21,900

Notes Payable 21,850

Accounts Payable 5,250

Kimberly Manis, Capital 18,000

Professional Fees 35,550

KIMBERLY MANIS, ARCHITECT

Unadjusted Trial Balance

January 31, 2016

2-20