PROBLEM 2-8B

(a) The primary objective of financial reporting is to provide information

useful for decision making. Since Yocum’s shares appear to be ac-

tively traded, investors must be capable of using the information made

available by Yocum to make decisions about the company.

CCC 2-1 CONTINUING COOKIE CHRONICLE

(a) The balance sheet reports the assets, liabilities, and stockholders’

equity of a company at a specific date. The income statement presents

the revenues and expenses and resulting net income or net loss of a

(b) By looking at the balance sheet and the cash flow statement and

calculating liquidity ratios, we can measure a company’s short term

(c) By looking at the balance sheet and the cash flow statement and

calculating solvency ratios we are able to measure a company’s ability

(d) By looking at the income statement we can determine if Biscuits is

profitable. If revenues earned by Biscuits exceed expenses incurred,

(e) By looking at the balance sheet we can determine if Biscuits has any

debt. By looking at the balance sheet and cash flow statement and

calculating solvency ratios we are able to determine whether a company

CONTINUING COOKIE CHRONICLE (Continued)

(f) By looking at the statement of cash flows we can determine whether

Biscuits has paid any dividends to its shareholders.

(g) Be aware that financial statements of Biscuits provide a historical

perspective of what has already taken place. The financial statements

may prove to be a good indicator of what will happen in the future but

BYP 2-1 FINANCIAL REPORTING PROBLEM

(a) Total current assets were $212,201,000 at December 31, 2011, and

$235,167,000 at December 31, 2010.

(b) Current assets are properly listed in the order of liquidity. As you will

learn in a later chapter, inventories are considered to be less liquid than

BYP 2-2 COMPARATIVE ANALYSIS PROBLEM

(

a

)

($ in thousands) Hershey Company Tootsie Roll

1. Working capital $2,046,558 – $1,173,775 = $872,783 $212,201 – $58,355 = $153,846

2. Current ratio $2,046,558 ÷ $1,173,775 = 1.7:1 $212,201 ÷ $58,355 = 3.6:1

(b) Liquidity

Hershey Company appears much more liquid since it has about $719

million more working capital than Tootsie Roll. But, looking at the current

ratios, we see that Tootsie Roll’s ratio is more than two times as large as

Hershey’s.

Solvency

Based on the debt to assets ratio, Tootsie Roll is more solvent.

Tootsie Roll’s debt to assets ratio is significantly lower than Hershey’s

BYP 2-3 RESEARCH CASE

(a) Many large companies, big accounting firms, and accounting standard

setters tend to favor a switch to IFRS because they believe that global

accounting standards would save companies money by consolidating

(b Many small companies are opposed to switching to IFRS because (1)

(c) It has been suggested that IFRS lacks standards that are specific to

utility companies that U.S. GAAP contains.

(d) Condorsement (a word invented by the SEC) represents a

combination of convergence and endorsement. Under condorsement,

U.S. standard setters would continue to work with international

BYP 2-4 INTERPRETING FINANCIAL STATEMENTS

(a) The percentage decrease in Gap’s total assets during this period is

calculated as:

The average decrease per year can be approximated as:

(b) Gap’s working capital and current ratio decreased (2007), increased

(2008 and 2009) and then decreased (2010) during this period,

indicating a decline, an improvement and then another decline in liquidity.

(c) The debt to assets ratio suggests that Gap’s solvency didn’t change

(d) The earnings per share suggests that Gap’s profitability improved signifi-

cantly from 2006 to 2010, increasing from $0.94 to $1.89. However, based

REAL-WORLD FOCUS

BYP 2-5

BYP 2-6

BYP 2-7 DECISION MAKING ACROSS THE ORGANIZATION

The current ratio increase is a favorable indication as to liquidity, but alone

tells little about the prospects of the client. From this ratio change alone,

it is impossible to know the amount and direction of the changes in individual

accounts, total current assets, and total current liabilities. Also unknown

are the reasons for the changes.

The working capital increase is also a favorable indication as to liquidity,

but again the amount and direction of the changes in individual current

assets and current liabilities cannot be determined from this measure.

as they come due. A decline in the debt to assets ratio is also a positive

sign regarding going-concern potential.

The increase in net income is a favorable indicator for both solvency and

profitability prospects although much depends on the quality of receivables

BYP 2-8 COMMUNICATION ACTIVITY

To: F. P. Fernetti

From: Accounting Major

Subject: Financial Statement Analysis

(a) Ratios can be classified into three types, which measure three different

aspects of a company’s financial health:

1. Liquidity ratios—These measure a company’s ability to pay its

current obligations.

(b) 1. Examples of liquidity measures are:

2. Examples of solvency measures are:

BYP 2-8 (Continued)

3. Example of profitability measure:

(c) There are three bases for comparing a company’s results:

The bases of comparison are:

1. Intracompany—This basis compares an item or financial relation-

ship within a company in the current year with the same item or

relationship in one or more prior years.

BYP 2-9 ETHICS CASE

(a) The stakeholders in this case are: Boeing’s management; CEO, public

relations manager, Boeing’s stockholders, McDonnell Douglas stock-

(c) The periodicity assumption requires that financial results be reported

on specific, pre-determined dates.

(e) Answers will vary. One possibility: Release the information regarding

(f) Investors and analysts should be aware that Boeing’s management will

BYP 2-10 ALL ABOUT YOU

Answers will vary.

BYP 2-11 FASB CODIFICATION ACTIVITY

(a) 1. Current assets is used to designate cash and other assets or

resources commonly identified as those that are reasonably

expected to be realized in cash or sold or consumed during the

normal operating cycle of the business.

(b) Access FASB Codification 210-20-45

A right of set off exists when all of the following conditions are met:

1. Each of two parties owes the other determinable amounts.

BYP 2-12 PEOPLE, PLANET AND PROFIT

(a) The existence of three different forms of certification would most

likely create confusion for coffee purchasers. It would difficult to

(b) The Starbucks certification appears to be the most common in that

area. It has the advantage of having a direct link to the Starbucks

coffee market. Although it does not guarantee that Starbucks will buy

(c) The certifications have multiple objectives including organic farming

as a means to protect bird species, biodiversity and wildlife habitat.

Some included requirements are to improve workers’ living

conditions, such as providing running water in worker housing, child

IFRS CONCEPTS AND APPLICATION

IFRS 2-1

The statement of financial position required under IFRS and the balance

sheet prepared under GAAP usually present the same information regarding

a company’s assets, liabilities, and stockholders’ equity at a point in time.

IFRS does not dictate a specific order but most companies list noncurrent

items before current. Differences in ordering are

Statement of Financial

Position presentation

Balance Sheet

presentation

Noncurrent assets Current assets

IFRS 2-2

IFRS 2-3

IFRS 2-4

RUIZ COMPANY

Partial Statement of Financial Position

Current assets

Prepaid insurance ………………………………………………………….. £ 3,600

Supplies ………………………………………………………………………… 5,200

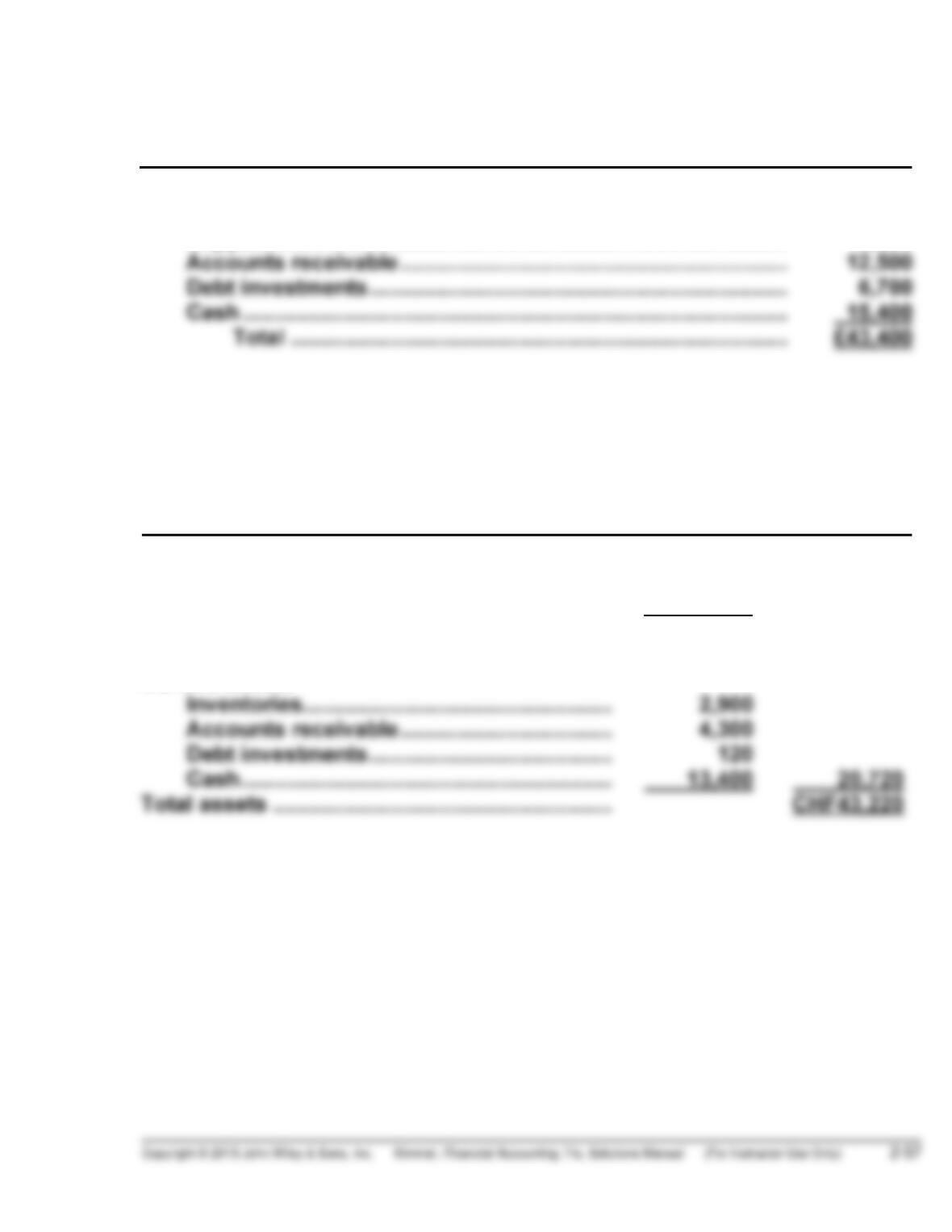

IFRS 2-5

WIDMER COMPANY

Partial Statement of Financial Position

December 31, 2014

Property, plant and equipment

Equipment …………………………………………… CHF21,700

Less: Accumulated depreciation …………. 5,700 CHF16,000

Long-term investments

Share investments ……………………………….. 6,500

Current assets

IFRS 2-6

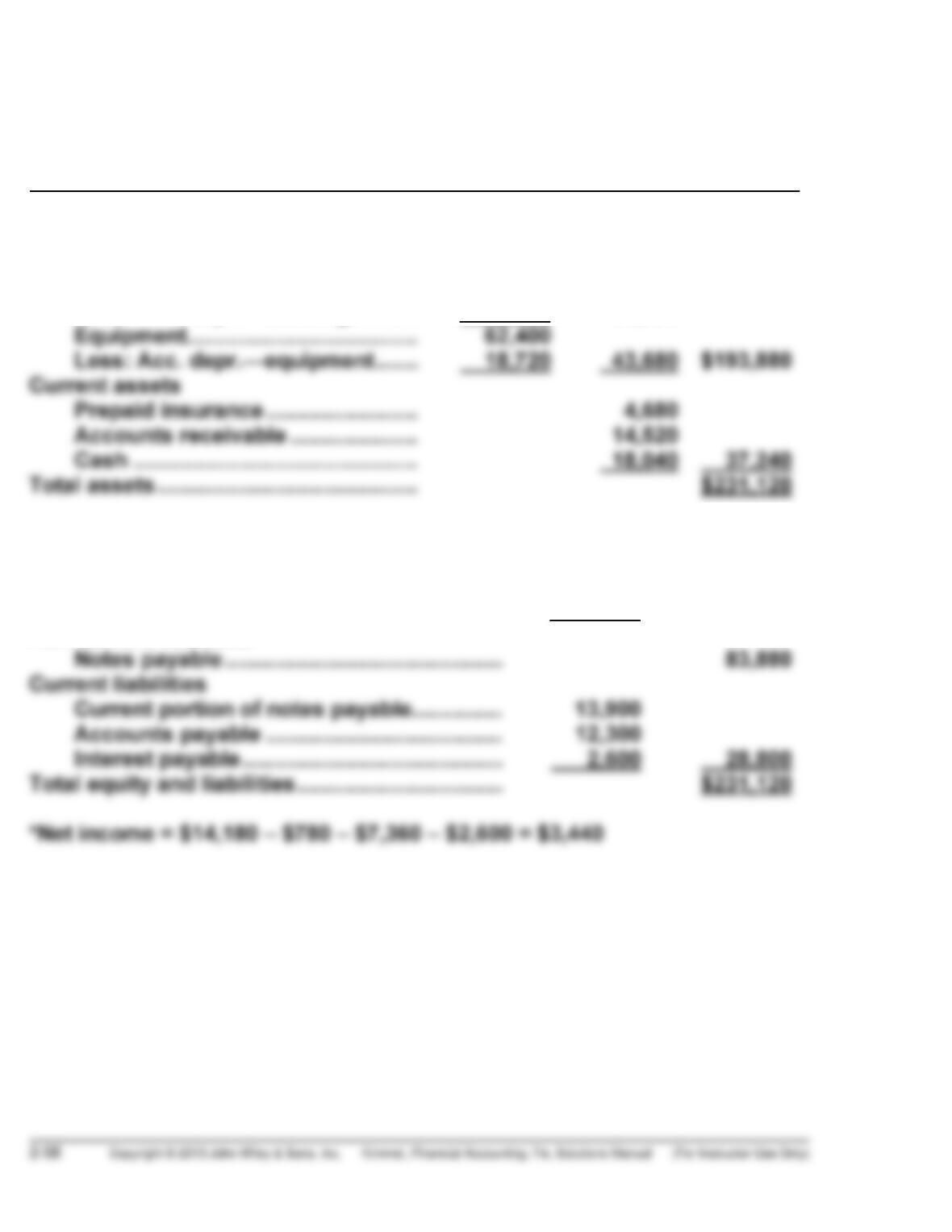

COLE BOWLING ALLEY

Statement of Financial Position

December 31, 2014

Assets

Property, plant, and equipment

Land ………………………………………… $64,000

Buildings …………………………………. $128,800

Less: Acc. depr.—buildings ……… 42,600 86,200

Equity and Liabilities

Equity

Share capital—ordinary ………………………… $100,000

Retained earnings ($15,000 + $3,440*) …… 18,440 $118,440

Non-current liabilities

IFRS 2-7

It is possible to compare liquidity and solvency for companies using

different currencies. The ratios that are used to do so, such as the current

ratio and debt to total assets, indicate relative amounts of assets and

liabilities rather than absolute monetary values.

IFRS 2-8 INTERNATIONAL COMPARATIVE ANALYSIS PROBLEM

Differences in the format of the statement of financial position (balance

sheet) used by Zetar and Tootsie Roll include the following:

Zetar Tootsie Roll

1. Non-current assets listed first Current assets listed first

2. Goodwill listed before property,

plant and equipment

Property, plant, and equipment

listed before goodwill

3. Current assets are shown in

reverse order of liquidity with

Current assets are shown in

order of liquidity with cash being