CHAPTER 2

SOLUTIONS TO EXERCISES—SET B

EXERCISE 2-1B

1. False. An account is an accounting record of a specific asset, liability,

or owner’s equity item.

2. True.

EXERCISE 2-2B

Account Debited

Account Credited

Transaction

(a)

Basic

Type

(b)

Specific

Account

(c)

Effect

(d)

Normal

Balance

(a)

Basic

Type

(b)

Specific

Account

(c)

Effect

(d)

Normal

Balance

Jan. 2

Asset

Cash

Increase

Debit

Owner’s

Equity

Owner’s

Capital

Increase

Credit

3

Owner’s

Equity

Advertising

Expense

Increase

Debit

Asset

Cash

Decrease

Debit

9

Asset

Equipment

Increase

Debit

Asset

Cash

Decrease

Debit

11

Asset

Accounts

Receivable

Increase

Debit

Owner’s

Equity

Service

Revenue

Increase

Credit

Asset

Supplies

Increase

Liability

Accounts

Increase

Credit

Asset

Cash

Increase

Debit

Asset

Accounts

Decrease

Debit

Liability

Accounts

Decrease

Credit

Asset

Cash

Decrease

Debit

Increase

Debit

Asset

Cash

Decrease

Debit

EXERCISE 2-3B

General Journal J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

Jan. 2

Cash ……………………………………………

20,000

Owner’s Capital …………………….

20,000

3

Advertising Expense …………………….

500

Cash …………………………………….

500

9

Equipment …………………………………..

7,000

Cash …………………………………….

Accounts Receivable ……………………

2,300

Service Revenue ……………………

Supplies ………………………………………

700

Accounts Payable …………………

700

Cash ……………………………………………

1,100

Accounts Receivable …………….

Cash …………………………………….

400

1,200

Cash …………………………………….

EXERCISE 2-4B

Oct. 1 Debits increase assets: debit Cash $22,000.

Credits increase owner’s equity: credit Owner’s Capital $22,000.

EXERCISE 2-4B (Continued)

Oct. 6 Debits increase assets: debit Accounts Receivable $5,400.

Credits increase revenues: credit Service Revenue $5,400.

27 Debits decrease liabilities: debit Accounts Payable $1,100.

Credits decrease assets: credit Cash $1,100.

EXERCISE 2-5B

General Journal

Date

Account Titles and Explanation

Ref.

Debits

Credit

Oct. 1

Cash ……………………………………………

22,000

Owner’s Capital ……………………

22,000

2

Rent Expense ………………………………

700

Cash ……………………………………

700

3

Equipment …………………………………..

2,800

Accounts Payable ………………..

2,800

6

Accounts Receivable ……………………

5,400

Service Revenue ………………….

5,400

Utilities Expense ………………………….

Accounts Payable ………………..

EXERCISE 2-6B

(a) 1. Increase the asset Cash, increase the liability Notes Payable.

2. Increase the asset Equipment, decrease the asset Cash.

3. Increase the expense Rent Expense, decrease the asset Cash.

(b) 1. Cash ……………………………………………………….. 15,000

Notes Payable ……………………………………. 15,000

EXERCISE 2-7B

(a) Assets = Liabilities + Owners’ Equity

1. + +

2. + +

3. + +

4. – –

(b) 1. Cash ……………………………………………………….. 6,000

Owner’s Capital …………………………………. 6,000

2. Supplies …………………………..……………………… 1,100

Accounts Payable ………………………………. 1,100

EXERCISE 2-8B

1. False. The general ledger contains all the asset, liability, and owner’s

equity accounts.

2. False The general ledger is sometimes referred to as the ledger.

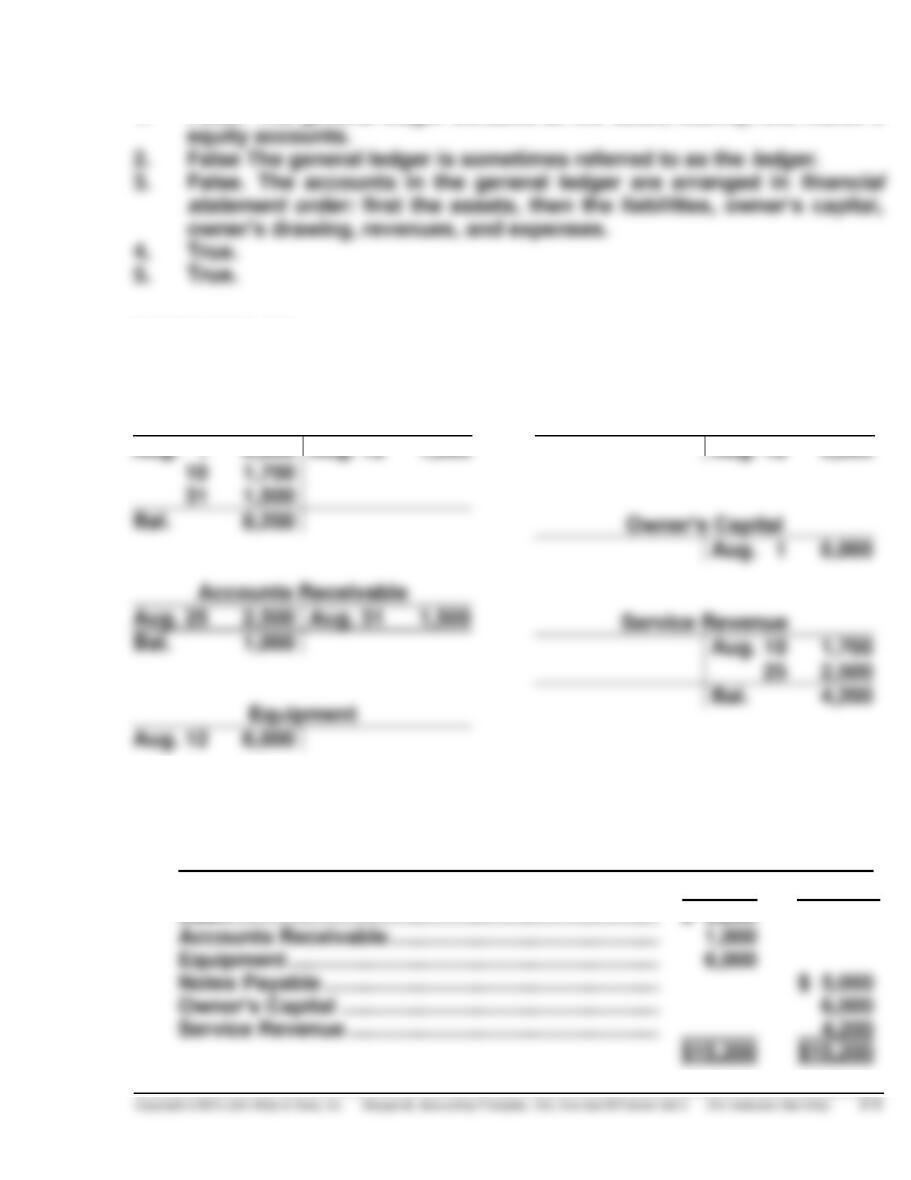

EXERCISE 2-9B

(a)

Cash

Aug. 1 6,000

Aug. 12 1,000

10 1,700

31 1,500

Bal. 8,200

Bal. 1,000

Aug. 12 6,000

Aug. 10 1,700

Bal. 4,200

Notes Payable

Aug. 12 5,000

Owner’s Capital

Aug. 1 6,000

(b) BRET QUANDT, INVESTMENT BROKER

Trial Balance

August 31, 2017

Debit Credit

Cash …………………………..………………………………….. $ 8,200

Accounts Receivable ………………………………………. 1,000

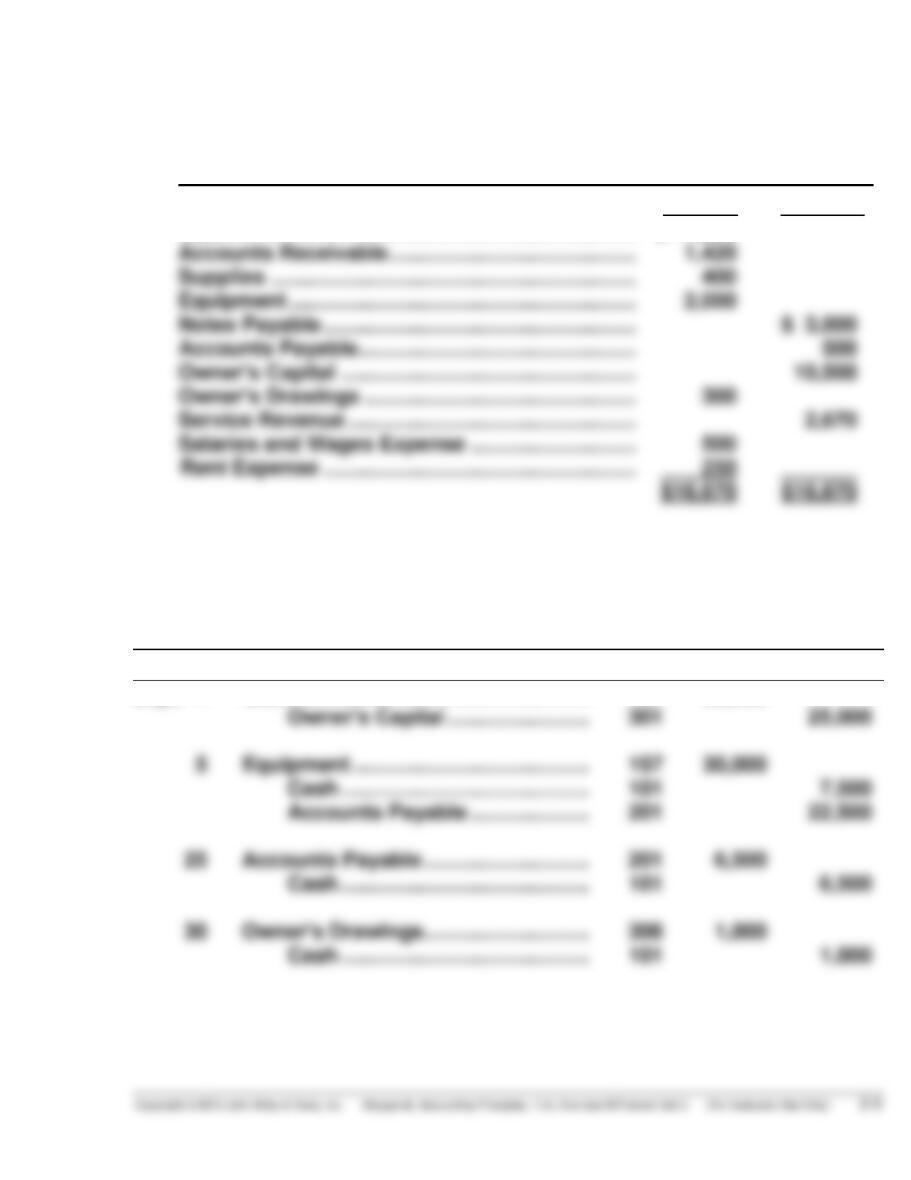

EXERCISE 2-10B

(a) General Journal

Date

Account Titles and Explanation

Ref.

Debit

Credit

Apr. 1

Cash …………………………………………….

Owner’s Capital …………………………

(Owner’s investment of

cash in business)

18,000

18,000

12

Cash …………………………………………….

Service Revenue ……………………….

(Received cash for

services provided)

1,200

1,200

15

25

Accounts Payable ………………………….

Cash …………………………………………

(Paid creditors on account)

1,600

1,600

Cash …………………………………………….

of account)

30

Cash …………………………………………….

Unearned Service Revenue ………..

(Received cash for future

services)

1,400

1,400

EXERCISE 2-10B (Continued)

(b) CARRIE’S GARDENING COMPANY

Trial Balance

April 30, 2017

Debit Credit

Cash …………………………..…………………………………… $19,200

Accounts Receivable ……………………………………….. 2,000

Supplies …………………………………………………………. 1,900

EXERCISE 2-11B

(a) Oct. 1 Cash ……………………………………………………. 8,500

10 Cash ……………………………………………………. 800

Service Revenue ……………………………. 800

(Received cash for services

provided)

20 Cash ……………………………………………………. 450

Accounts Receivable ……………………… 450

(Received cash in payment of

account)

EXERCISE 2-11B (Continued)

(b) NOLASKO CO.

Trial Balance

October 31, 2017

Debit Credit

Cash …………………………..………………………………. $ 11,800

Accounts Receivable …………………………………… 1,420

Supplies …………………………………………………….. 400

Equipment ………………………………………………….. 2,000

EXERCISE 2-12B

(a)

General Journal J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

Sept. 1

Cash ……………………………………………

Owner’s Capital …………………….

101

301

25,000

25,000

5

Equipment …………………………………..

Cash …………………………………….

Accounts Payable …………………

157

101

201

30,000

7,500

22,500

EXERCISE 2-12B (Continued)

(b)

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 1

J1

25,000

25,000

J1

7,500

17,500

J1

6,500

J1

10,000

Equipment No. 157

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 5

J1

30,000

30,000

Accounts Payable No. 201

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 5

J1

22,500

22,500

25

J1

6,500

16,000

Explanation

Ref.

Credit

Balance

Sept. 1

J1

Explanation

Ref.

Debit

Credit

Balance

Sept. 30

J1

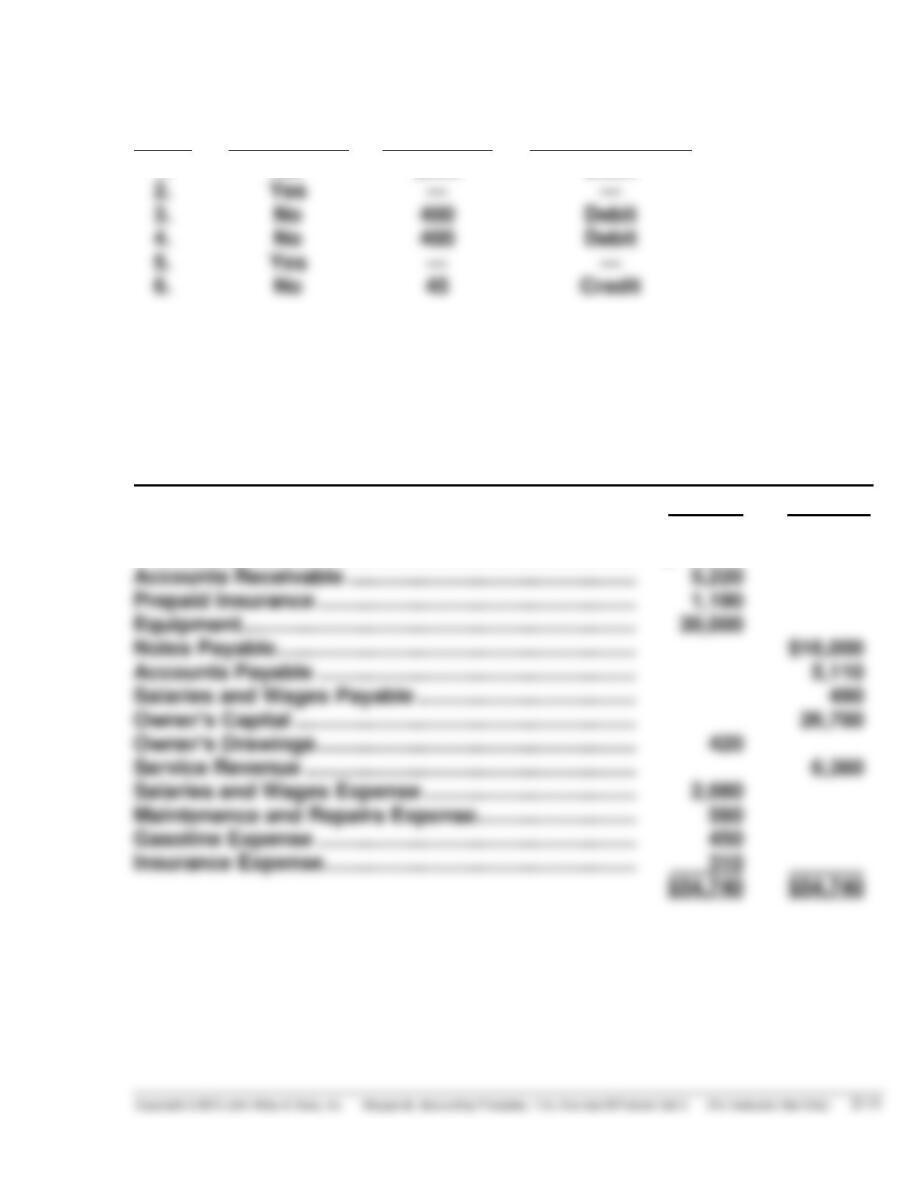

EXERCISE 2-13B

Error

(a)

In Balance

(b)

Difference

(c)

Larger Column

1.

No

$500

Debit

2.

Yes

—

—

3.

No

Debit

4.

5.

Yes

—

—

6.

No

EXERCISE 2-14B

MORAN DELIVERY SERVICE

Trial Balance

July 31, 2017

Debit Credit

Cash ($54,740 – Debit total without Cash

$40,830) …………………………………………………………. $ 13,910

Accounts Receivable …………………………………………. 5,220

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 2-1C

J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

Mar. 1

Cash…………………………………………………

50,000

Owner’s Capital …………………………

50,000

(Owner’s investment of cash

in business)

3

Land …………………………………………………

23,000

Buildings ………………………………………….

9,000

Equipment ………………………………………..

Cash …………………………………………

(Purchased Tee’s Golf Land)

5

Advertising Expense …………………………

1,600

Cash …………………………………………

1,600

(Paid for advertising)

6

Prepaid Insurance …………………………….

1,480

Cash …………………………………………

1,480

(Paid for one-year insurance

policy)

10

Equipment ………………………………………..

2,600

Accounts Payable ……………………..

2,600

(Purchased equipment on

account)

18

Cash…………………………………………………

800

Service Revenue ………………………..

(Received cash for services

provided)

19

Cash…………………………………………………

1,500

Unearned Service Revenue ………..

1,500

(Received cash for future

services)