2-1

CHAPTER 2

OVERVIEW OF BUSINESS PROCESSES

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

2.1 Table 2-1 lists some of the documents used in the revenue, expenditure, and human

resources cycle. What kinds of input or output documents or forms would you find in

the production (also referred to as the conversion cycle?

Students will not know the names of the documents but they should be able to identify the

tasks about which information needs to be gathered. Here are some of those tasks

• Requests for items to be produced

2.2 With respect to the data processing cycle, explain the phrase “garbage in, garbage

out.” How can you prevent this from happening?

When garbage, defined as errors, and allowed into a system that error is processed and the

resultant data stored. The stored data at some point will become output. Thus, the phrase

Ch. 2: Overview of Business Processes

2-2

2.3 What kinds of documents are most likely to be turnaround documents? Do an

internet search to find the answer and to find example turnaround documents.

Documents that are commonly used as turnaround documents include the following:

• Utility bills

• Meter cards for collecting readings from gas meters, photocopiers, water meters etc

2.4 The data processing cycle in Figure 2-1 is an example of a basic process found

throughout nature. Relate the basic input/process/store/output model to the functions

of the human body.

There are a number of ways to relate the input/process/store/output model to the human

Accounting Information Systems

2-3

body. Here are a few of them

• Brain. We read, see, hear, and feel things. We process that input in order to understand

2.5 Some individuals argue that accountants should focus on producing financial

statements and leave the design and production of managerial reports to information

systems specialists. What are the advantages and disadvantages of following this

advice? To what extent should accountants be involved in producing reports that

include more than just financial measures of performance? Why?

There are no advantages to accountants focusing only on financial information. Both the

accountant and the organization would suffer if this occurred. Moreover, it would be very

Ch. 2: Overview of Business Processes

2-4

SUGGESTED ANSWERS TO THE PROBLEMS

2.1 The chart of accounts must be tailored to an organization’s specific needs. Discuss

how the chart of accounts for the following organizations would differ from the one

presented for S&S in Table 2-4.

Some of the changes in the chart of accounts for each type of entity include the following:

a. University

• No equity or summary drawing accounts. Instead, have a fund balances section

for each type of fund.

b. Bank

• Loans to customers would be an asset, some current others noncurrent, depending

upon the length of the loan.

• No inventory

• Customer accounts would be liabilities.

Accounting Information Systems

d. Manufacturing Company

• Several types of inventory accounts (raw materials, work-in-process, and finished

goods).

• Additional digits to code revenues and expenses by products and to code

assets/liabilities by divisions.

Ch. 2: Overview of Business Processes

2-6

2.2 Design a chart of accounts for SDC. Explain how you structured the chart of

accounts to meet the company’s needs and operating characteristics. Keep total

account code length to a minimum, while still satisfying all of Mace’s desires.

(Adapted from the CMA Exam)

A six-digit code (represented by letters ABCDEF) is sufficient to meet SDC’s needs:

A This digit identifies the 4 divisions plus the corporate office

Accounting Information Systems

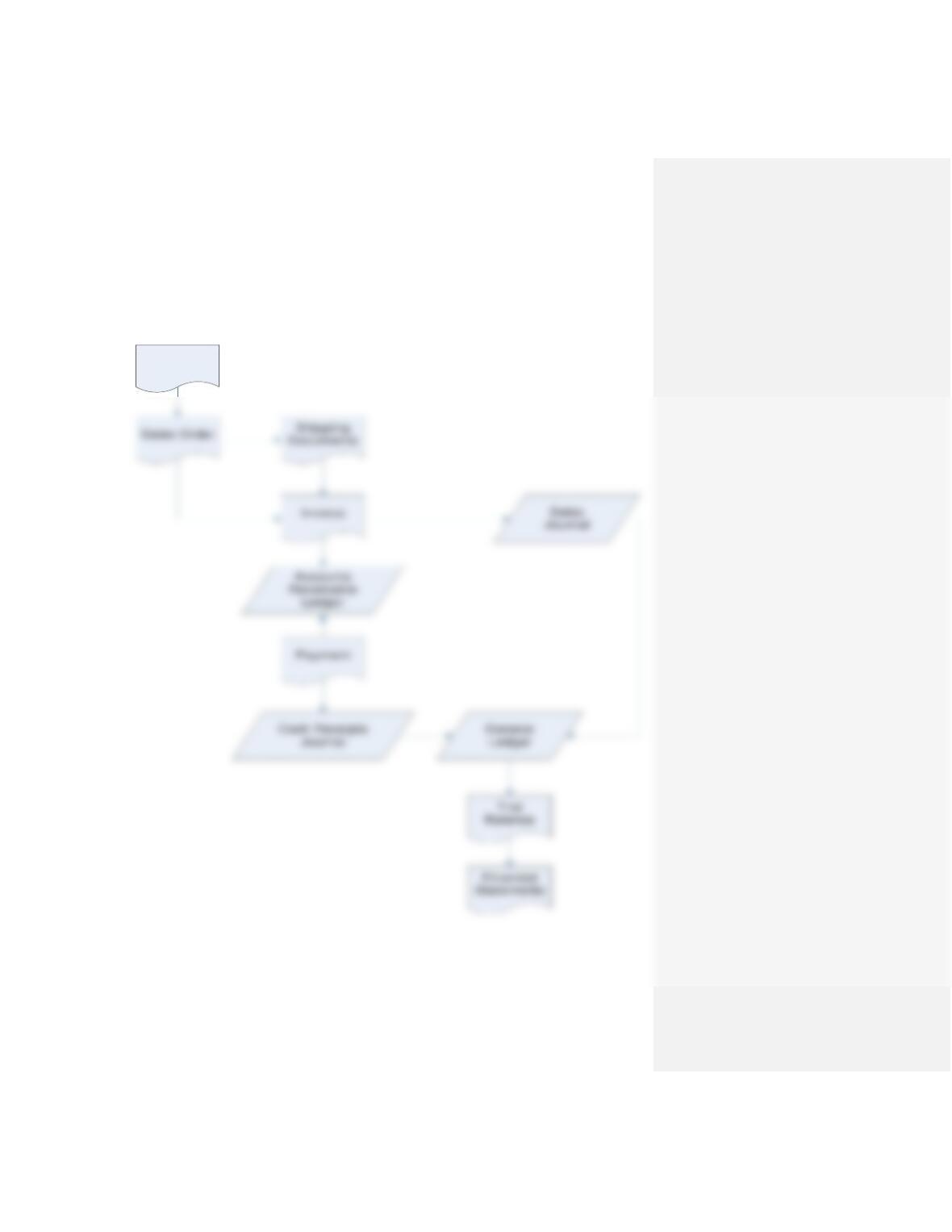

2.3 An audit trail enables a person to trace a source document to its ultimate effect on the

financial statements or work back from amounts in the financial statements to source

documents. Describe in detail the audit trail for the following:

a. The audit trail for inventory purchases includes linking purchase requisitions, purchase

orders, and receiving reports to vendor invoices for payment. All these documents

would be linked to the check or EFT transaction used to pay for an invoice and

Purchase

Requisition

Purchase

Order Receiving

Report Invoice

Ch. 2: Overview of Business Processes

2-8

b. The audit trail for the sale of inventory links the customer order, sales order, and

shipping document to the sales invoice. These documents are linked to the journal

entry recording the sale of that merchandise. The invoice would also be linked to the

cash received from the customer and to the journal entry to record that receipt.

Customer

Order

Accounting Information Systems

2-9

c. The audit trail for employee payroll links records of employee activity (time cards,

time sheets, etc.) to paychecks and to the journal entry to record payment of payroll.

Ch. 2: Overview of Business Processes

2-10

2.4 Your nursery sells various types and sizes of trees, bedding plants, vegetable plants,

and shrubs. It also sells fertilizer and potting soil. Design a coding scheme for your

nursery.

Grading depends upon the instructor’s judgment about the quality of the coding scheme.

2.5 Match the following terms with their definitions

a. 10

b. 23

c. 7

d. 16

Accounting Information Systems

2.6 For each of the following scenarios identify which data processing method (batch or

online, real-time) would be the most appropriate.

Some students will respond that all can and ought to be done with online-real time

processing. While all can certainly be done that way, batch processing does have its

advantages (cheaper, more efficient, etc.). In making the decision between batch and

2.7 After viewing the Web sites, and based on your reading of the chapter, write a 2 page

paper that describes how an ERP can connect and integrate the revenue, expenditure,

human resources/payroll, and financing cycles of a business.

Student solutions will vary depending on the demonstrations they observe. However, the

2.8 Identify whether the following transactions belong in a master file or a transaction

file.

a. Update customer address change – Master file

b. Update unit pricing information – Master file

c. Record daily sales – Transaction file

Ch. 2: Overview of Business Processes

2.9 You were hired to assist Ashton Fleming in designing an accounting system for S&S.

Ashton has developed a list of the journals, ledgers, reports, and documents that he

thinks S&S needs (see Table 2-6). He asks you to complete the following tasks:

a. Specify what data you think should be collected on each of the following four

documents: sales invoice, purchase order, receiving report, employee time card

b. Design a report to manage inventory.

c. Design a report to assist in managing credit sales and cash collections.

d. Visit a local office supply store and identify what types of journals, ledgers,

and blank forms for various documents (sales invoices, purchase orders, etc.)

are available. Describe how easily they could be adapted to meet S&S’s needs.

a. A sample invoice is presented in the Revenue Cycle chapter. A sample purchase

order is presented in the Expenditure Cycle chapter. A sample receiving report also

appears in the Expenditure Cycle chapter. Although student designs will vary, each

document should contain the following data items:

Purchase Order

Ship to address Item numbers ordered

Bill to address Payment terms

Purchasing agent number Shipping instructions

Quantity of parts ordered Supplier name or number

Prices of parts ordered Date of purchase

Taxes, if any Total amount of purchase

Accounting Information Systems

2-13

Inspected by

b. The report to manage inventory should contain the following information:

• Preferred vendor

• Product number

c. The report to manage credit sales and cash collections should include:

• Credit sales per period

• Cash collections per period

Ch. 2: Overview of Business Processes

2-14

SUGGESTED ANSWERS TO THE CASES

2.1 Bar Harbor Blueberry Farm

Data from Case

Date

Supplier

Invoice

Supplier Name

Supplier

Address

Amount

March 7

AJ34

Bud’s Soil Prep, Inc.

PO Box 34

$2,067.85

March 11

14568

Osto Farmers Supply

45 Main

$ 67.50

March 14

893V

Whalers Fertilizer, Inc.

Route 34

$5,000.00

Purchases Journal

Page 1

Date

Supplier

Supplier

Invoice

Account

Number

Post

Ref

Amount

March 7

Bud’s Soil Prep, Inc.

AJ34

23

√

$2,067.85

March 11

Osto Farmers Supply

14568

24

√

$ 67.50

March 14

Whalers Fertilizer, Inc.

893V

36

√

$5,000.00

March 21

Osto Farmers Supply

14699

24

√

$3,450.37

Wholesale

March 31

14,858.60

March 21

14699

Osto Farmers Supply

45 Main

$3,450.37

Wholesale

Accounting Information Systems

2-15

General Ledger

Accounts Payable Account Number:

300

Date

Description

Post Ref

Debit

Credit

Balance

March 1

Balance

Forward

$18,735.55

Purchases Account Number: 605

Date

Description

Post Ref

Debit

Credit

Balance

March 1

Balance

Forward

$54,688.49

March 31

March 31

Ch. 2: Overview of Business Processes

2-16

Account Payable Subsidiary Ledger

Account No: 23

Bud’s Soil Prep, Inc.

PO Box 34

Terms: 2/10,

Net 30

Date

Description

Debit

Credit

Balance

March

1

Balance Forward

0.00

Account No: 24

Osto Farmers Supply

45 Main

Terms: 2/10,

Net 30

Date

Description

Debit

Credit

Balance

1

Mar 11

Seedling Heat Mat

Mar 21

Medium Portable

Greenhouse

March

Balance Forward

0.00

Account No: 36

Whalers Fertilizer,

Inc.

Route 34

Terms: 2/10,

Net 30

Date

Description

Debit

Credit

Balance

Fertilizer

March

Balance Forward

0.00

Account No: 38

IFM Package

Wholesale

587 Longview

Terms: 2/10,

Net 30

Date

Description

Debit

Credit

Balance

March

1

Balance Forward

0.00

Mar 21

Peat Pots

Mar 24

Labels

March

7

Mulch