CHAPTER 2

LEARNING OBJECTIVES

1. DESCRIBE HOW ACCOUNTS, DEBITS, AND CREDITS

ARE USED TO RECORD BUSINESS TRANSACTIONS.

2. INDICATE HOW A JOURNAL IS USED IN THE

RECORDING PROCESS.

CHAPTER REVIEW

The Account

1. (L.O. 1) An account is an individual accounting record of increases and decreases in a specific

asset, liability, or owner’s equity item.

Debits and Credits

3. The terms debit and credit mean left and right, respectively.

a. The act of entering an amount on the left side of an account is called debiting the account

4. In a double-entry system, equal debits and credits are made in the accounts for each transaction.

Thus, the total debits will always equal the total credits.

5. The effects of debits and credits on assets and liabilities and the normal balances are:

Accounts Debits Credits Normal Balance

Assets Increase Decrease Debit

6. Accounts are kept for each of the four subdivisions of owner’s equity: capital, drawings, revenues,

and expenses.

7. The effects of debits and credits on the owner’s equity accounts and the normal balances are:

Accounts Debits Credits Normal Balance

Owner’s Capital Decrease Increase Credit

Owner’s Drawings Increase Decrease Debit

8. The expanded accounting equation is:

The Journal

9. (L.O. 2) The basic steps in the recording process are:

a. Analyze each transaction for its effect on the accounts.

10. Transactions are initially recorded in a journal.

a. A journal is referred to as a book of original entry.

b. A general journal is the most basic form of journal.

11. The journal makes several significant contributions to the recording process:

a. It discloses in one place the complete effect of a transaction.

The Ledger

13. (L.O. 3) The ledger is the entire group of accounts maintained by a company. It keeps in one

place all the information about changes in account balances and it is a source of useful data for

management.

14. The standard form of a ledger account has three columns and the balance in the account is

determined after each transaction.

15. Posting is the procedure of transferring journal entries to the ledger accounts. The following steps

are used in posting:

a. In the ledger, enter in the appropriate columns of the account(s) debited the date, journal

The Chart of Accounts

16. A chart of accounts is a listing of the accounts and the account numbers which identify their

The Basic Steps

17. The basic steps in the recording process are illustrated as follows:

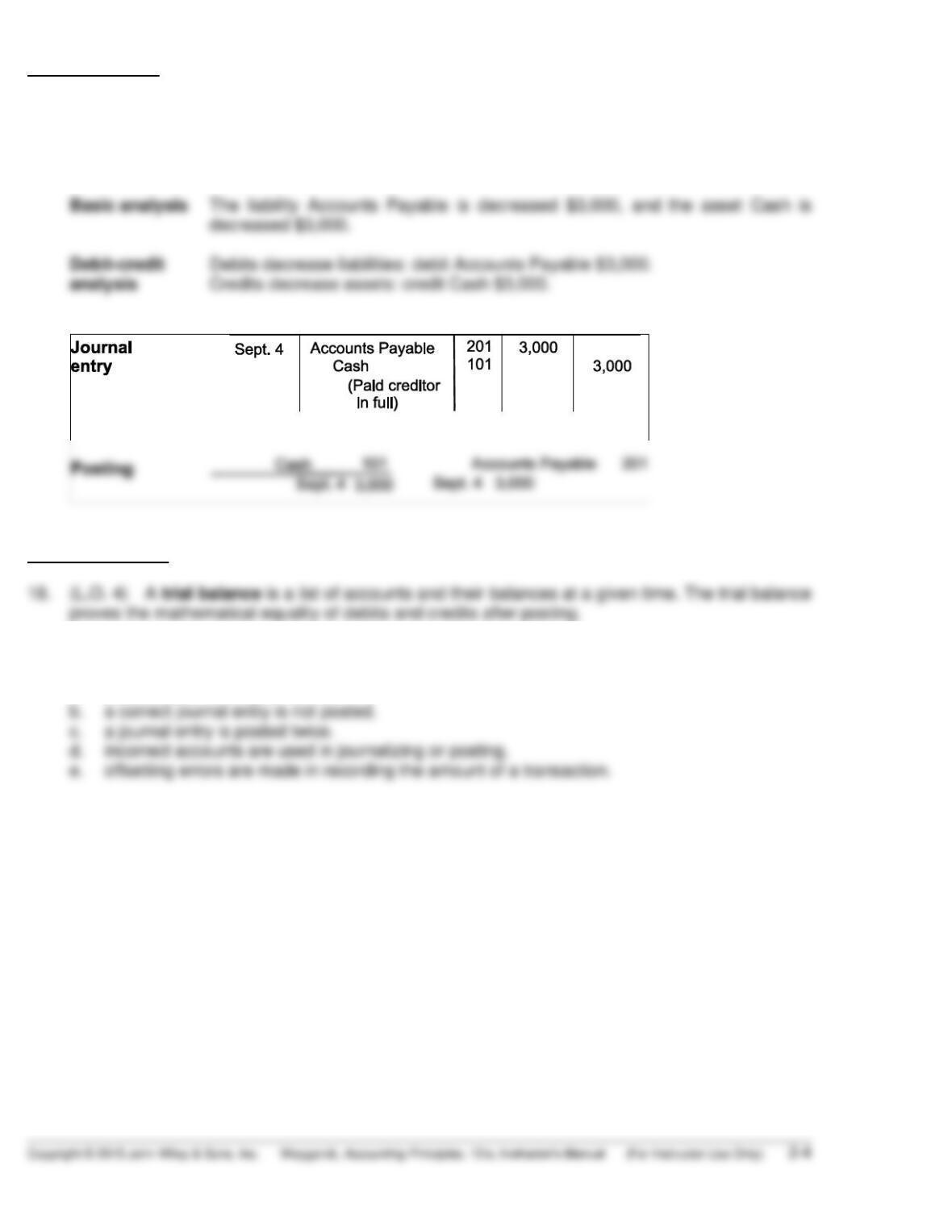

Transaction On September 4, Fesmire Inc. pays $3,000 cash to a creditor in full payment of

the balance due.

The Trial Balance

18. (L.O. 4) A trial balance is a list of accounts and their balances at a given time. The trial balance

proves the mathematical equality of debits and credits after posting.

19. A trial balance does not prove that the company has recorded all transactions or that the ledger is

correct because the trial balance may balance even when

a. a transaction is not journalized.

LECTURE OUTLINE

A. The Account.

An account is an individual accounting record of increases and decreases in

a specific asset, liability, or owner’s equity item.

An account consists of three parts:

B. Debits and Credits.

The terms debit and credit are directional signals: Debit indicates left, and credit

indicates right.

C. Steps in the Recording Process.

There are three basic steps in the recording process:

3. Transfer the journal information to the appropriate accounts in the ledger.

D. The General Journal/Journalizing.

Entering transaction data in the general journal is called journalizing.

The general journal:

1. Discloses in one place the complete effects of a transaction.

E. The Ledger.

The ledger is the entire group of accounts maintained by a company. A gen-

eral ledger contains all the assets, liabilities, and owner’s equity accounts.

1. The ledger provides the balance in each of the accounts as well as

keeps track of changes in these balances.

F. Posting/Chart of Accounts.

1. Posting is transferring journal entries to the ledger accounts.

2. Posting involves the following steps:

a. In the ledger, in the appropriate columns of the account(s) debited,

enter the date, journal page, and debit amount shown in the journal.

b. In the reference column of the journal, write the account number to

which the debit amount was posted.

c. In the ledger, in the appropriate columns of the account(s) credited,

enter the date, journal page, and credit amount shown in the journal.

G. Trial Balance.

A trial balance is a list of accounts and their balances at a given time.

INVESTOR INSIGHT

Bank regulators fined Bank One Corporation (Now Chase) $1.8 million because

they felt the reliability of the bank’s accounting system caused it to violate

regulatory requirements. The financial records of Waste Management Inc. were

in such disarray that 10,000 employees were receiving pay slips that were in

error.

In order for these companies to prepare and issue financial statements, their

accounting equations must have been in balance at year-end. How could these

errors or misstatements have occurred?

Answer: A company’s accounting equation (its books) can be in balance yet its

financial statements have errors or misstatements because of the

IFRS

A Look At IFRS

International companies use the same set of procedures and records to keep track of

transaction data. Thus, the material in Chapter 2 dealing with the account, general rules

of debit and credit, and steps in the recording process—the journal, ledger, and chart of

accounts—is the same under both GAAP and IFRS.

KEY POINTS

Following are the key similarities and differences between GAAP and IFRS as related to the

recording process:

• Transaction analysis is the same under IFRS and GAAP.

• Both the IASB and FASB go beyond the basic definitions provided in the textbook for

the key elements of financial statements, that is, assets, liabilities, equity, revenue, and

expenses.

• A trial balance under IFRS follows the same format as shown in the textbook.

LOOKING TO THE FUTURE

The basic recording process shown in this textbook is followed by companies across the globe.

It is unlikely to change in the future. The definitional structure of assets, liabilities, equity,

20 MINUTE QUIZ

Circle the correct answer.

True/False

1. Assets are increased by debits and liabilities are decreased by credits.

True False

2. The owner’s capital account is increased by credits.

True False

3. An account will have a credit balance if the total debit amounts exceed the total credit

amounts.

True False

4. The ledger is the entire group of accounts maintained by a company.

True False

5. The basic steps in the recording process are (1) to analyze each transaction, (2) to enter

the transaction in a journal, and (3) to transfer the journal entry to the appropriate ledger

accounts.

True False

6. Transferring journal entries to the ledger accounts is called posting and should be per-

formed in chronological order.

True False

7. Assets = liabilities + owner’s capital – drawings + revenues – expenses is a correct form

of the expanded basic accounting equation.

True False

8. In posting, one should enter “J2” in the Post. Ref. Column on page two of the journal.

True False

9. When the columns of the trial balance equal each other, it proves no errors occurred in

recording and posting.

True False

10. The double-entry system helps ensure the accuracy of the recorded amounts and helps to

detect errors.

True False

Multiple Choice

1. Transactions are initially recorded in the

a. general ledger.

b. general journal.

c. trial balance.

d. balance sheet.

2. The right side of an account is referred to as the

a. footing.

b. chart side.

c. debit side.

d. credit side.

3. A purchase of equipment for cash requires a credit to

a. Equipment.

b. Cash.

c. Accounts Payable.

d. Owner’s Capital.

4. The equality of the accounting equation can be proven by preparing a

a. trial balance.

b. journal.

c. general ledger.

d. T-account.

5. Which of the following accounts would be increased with a debit?

a. Rent Payable

b. Owner’s Capital

c. Service Revenue

d. Owner’s Drawings

ANSWERS TO QUIZ

True/False

1. False 6. True

2. True 7. True

Multiple Choice

1. b.