CHAPTER 2

SOLUTIONS TO EXERCISES—SET B

EXERCISE 2-1B

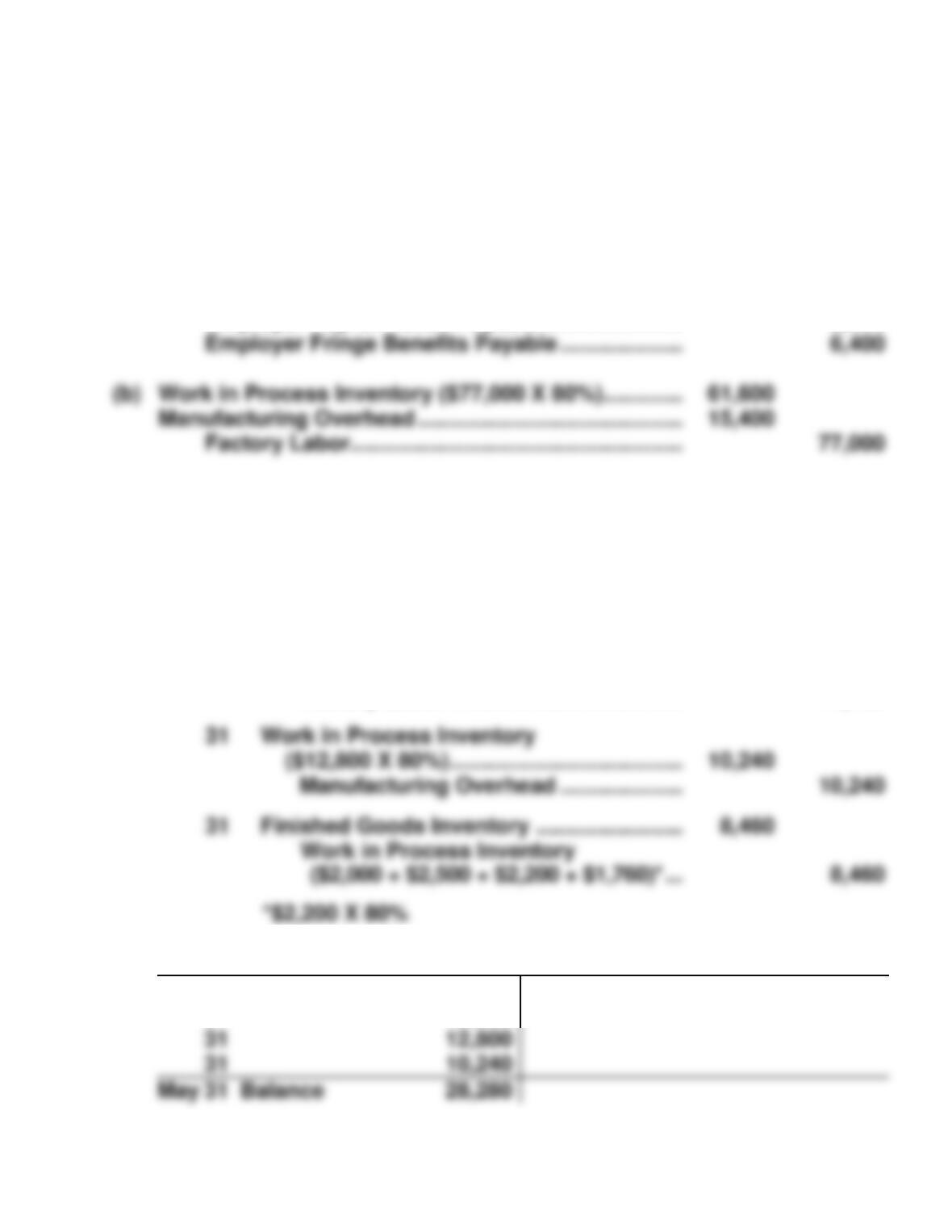

(a) Factory Labor ……………………………………………………. 77,000

Factory Wages Payable ……………………………….. 61,000

Employer Payroll Taxes Payable ………………….. 9,600

EXERCISE 2-2B

(a) May 31 Work in Process Inventory ………………….. 10,500

Manufacturing Overhead …………………….. 1,800

Raw Materials Inventory…………………. 12,300

31 Work in Process Inventory ………………….. 12,800

Manufacturing Overhead …………………….. 1,950

Factory Labor ……………………………….. 14,750

(b)

Work in Process Inventory

May 31 Balance 28,280

May 1 Balance 3,200

31 10,500

May 31 8,460

EXERCISE 2-2B (Continued)

Job Cost Sheets

Job

No.

Beginning Work

in Process

Direct

Material

Direct

Labor

Manufacturing*

Overhead

Total

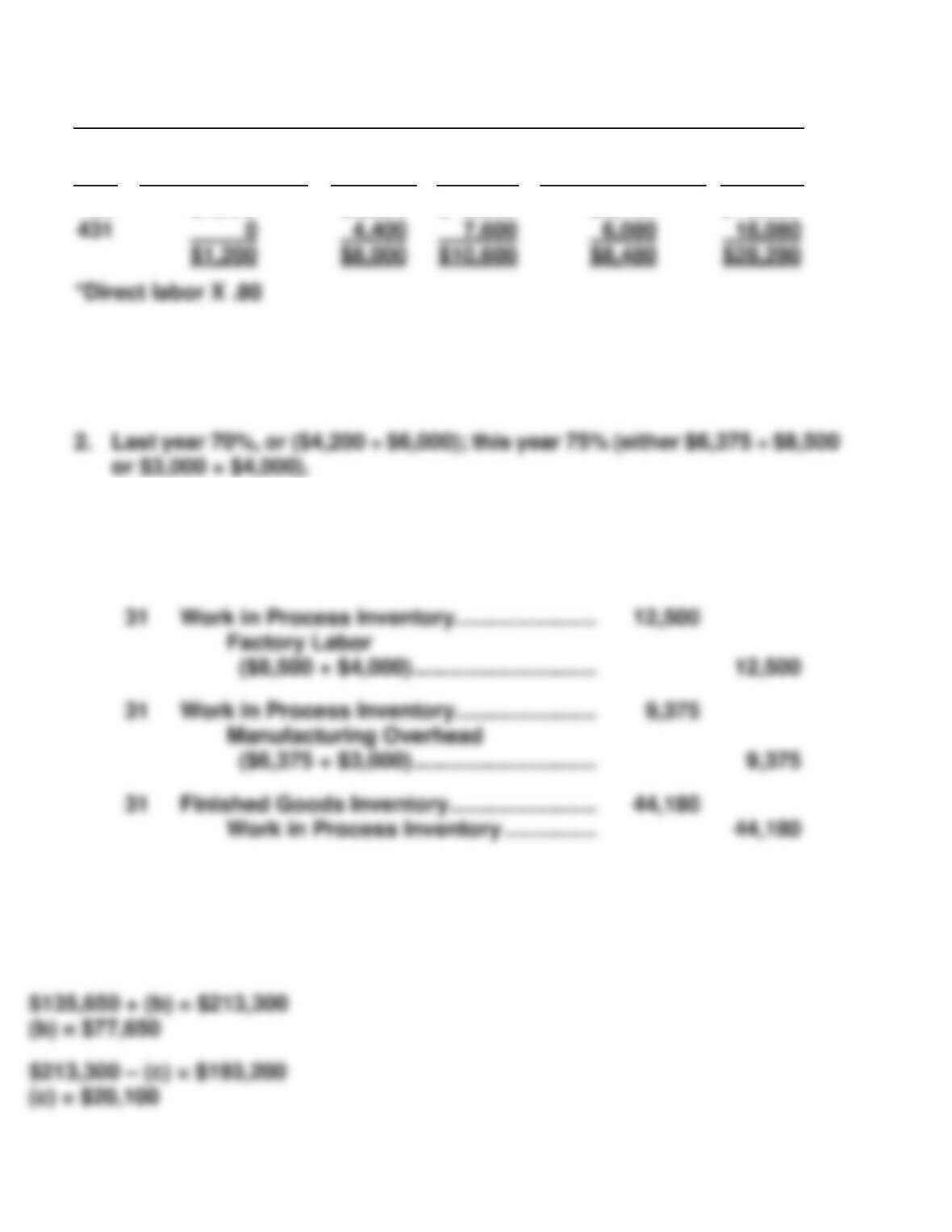

430

$1,200

$3,600

$ 3,000

$2,400

$10,200

EXERCISE 2-3B

(a) 1. $14,305, or ($4,105 + $6,000 + $4,200).

(b) Jan. 31 Work in Process Inventory ………………….. 8,000

Raw Materials Inventory

($6,000 + $2,000) ……………………….. 8,000

EXERCISE 2-4B

(a) + $50,000 + $37,500 = $135,650

(a) = $48,150

EXERCISE 2-4B (Continued)

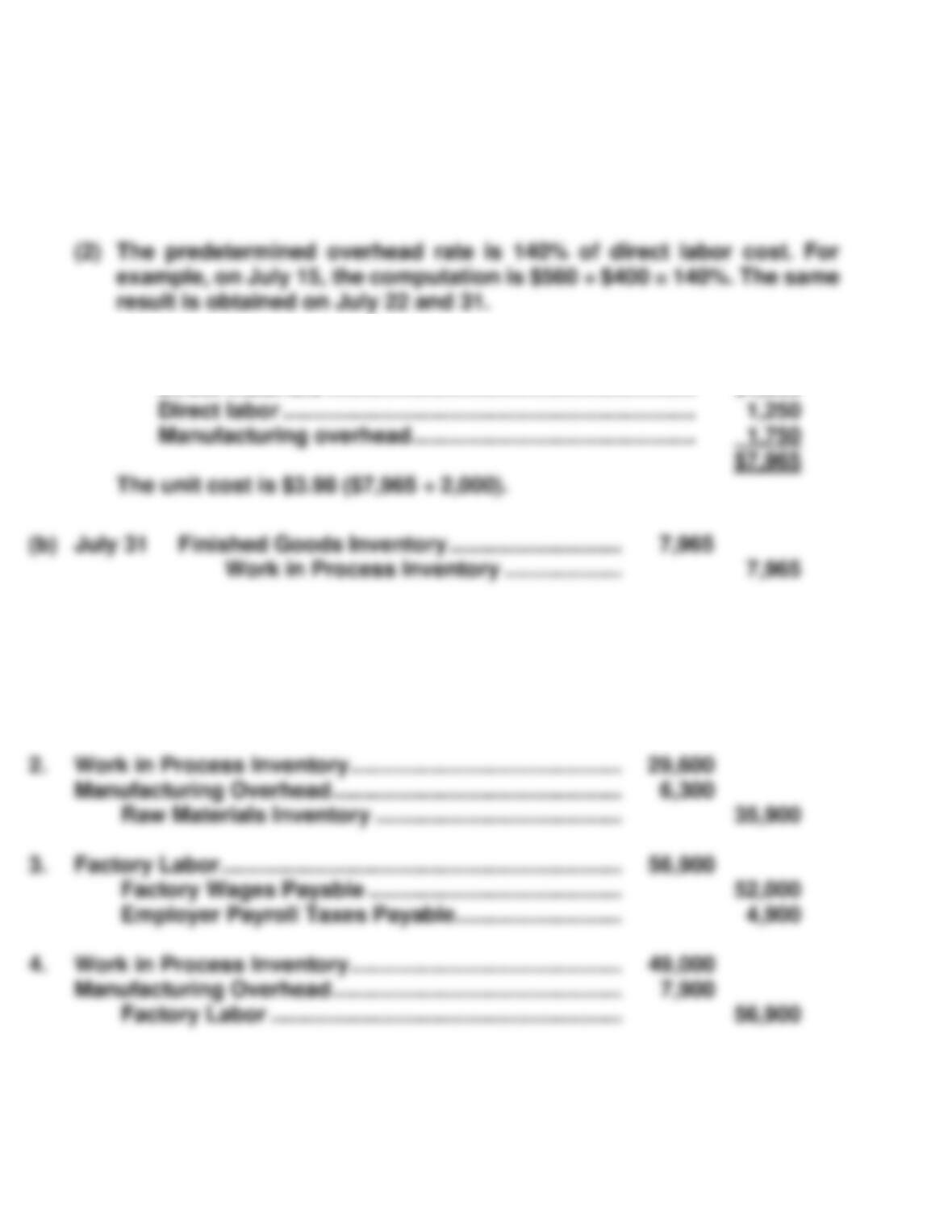

[Note: The instructions indicate that manufacturing overhead is applied on the

basis of direct labor cost, and the rate is the same in all cases. From Case A,

a student should note the overhead rate to be 75%, or ($37,500 ÷ $50,000).]

(d) = .75 X $120,000

(d) = $90,000

[Note: (h) and (i) are solved together.]

(i) = .75(h)

$72,600 + (h) + .75(h) = $212,600

1.75(h) = $140,000

EXERCISE 2-5B

(a) $2.56 per machine hour ($320,000 ÷ 125,000).

EXERCISE 2-6B

(a) (1) The source documents are:

Direct materials—Materials requisition slips.

Direct labor—Time tickets.

Manufacturing overhead—Predetermined overhead rate.

(3) The total cost is:

Direct materials …………………………………………………… $4,965

EXERCISE 2-7B

1. Raw Materials Inventory ………………………………………… 45,235

Accounts Payable ………………………………………….. 45,235

EXERCISE 2-7B (Continued)

5. Manufacturing Overhead ………………………………… 80,500

Accounts Payable ……………………………………. 80,500

6. Work in Process Inventory ($49,000 X 120%) ……. 58,800

Manufacturing Overhead………………………….. 58,800

EXERCISE 2-8B

1. Raw Materials Inventory …………………………………. 213,000

Accounts Payable ……………………………………. 213,000

Factory Labor ………………………………………………… 92,000

Factory Wages Payable ……………………………. 92,000

EXERCISE 2-8B (Continued)

5. Work in Process Inventory ……………………………… 59,150

Manufacturing Overhead

(70% X $84,500) …………………………………… 59,150

Computation of cost of jobs finished:

Job

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Total

A20

$33,240

$18,500

$12,950

$ 64,690

EXERCISE 2-9B

(a) ANDRES MANUFACTURING COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended May 31, 2017

Work in process, May 1 …………………………………. $ 18,800

Direct materials used …………………………………….. $54,200

Direct labor …………………………………………………… 32,000

EXERCISE 2-9B (Continued)

(b) ANDRES MANUFACTURING COMPANY

(Partial) Income Statement

For the Month Ended May 31, 2017

Sales…………………………………………………………. $200,000

Cost of goods sold

Finished goods, May 1 ………………………… $ 12,600

Cost of goods manufactured ……………….. 127,100

(c) In the May 31 balance sheet, the manufacturing inventories will be reported in

EXERCISE 2-10B

(a) Work in Process Inventory

April 30 $11,300 (#10, $7,200 + #11, $4,100)

(b) Finished Goods Inventory

April 30 $1,200 (#12)

(c) Gross Profit

Month

Job

Number

Sales

Cost of

Goods Sold

Gross

Profit

May

12

$ 1,560

$ 1,200

$ 360

EXERCISE 2-11B

(a)

Transaction

Number

Accounts Titles

Debit

Credit

1

Supplies ……………………………………..

1,795

Accounts Payable …………………..

1,795

(b)

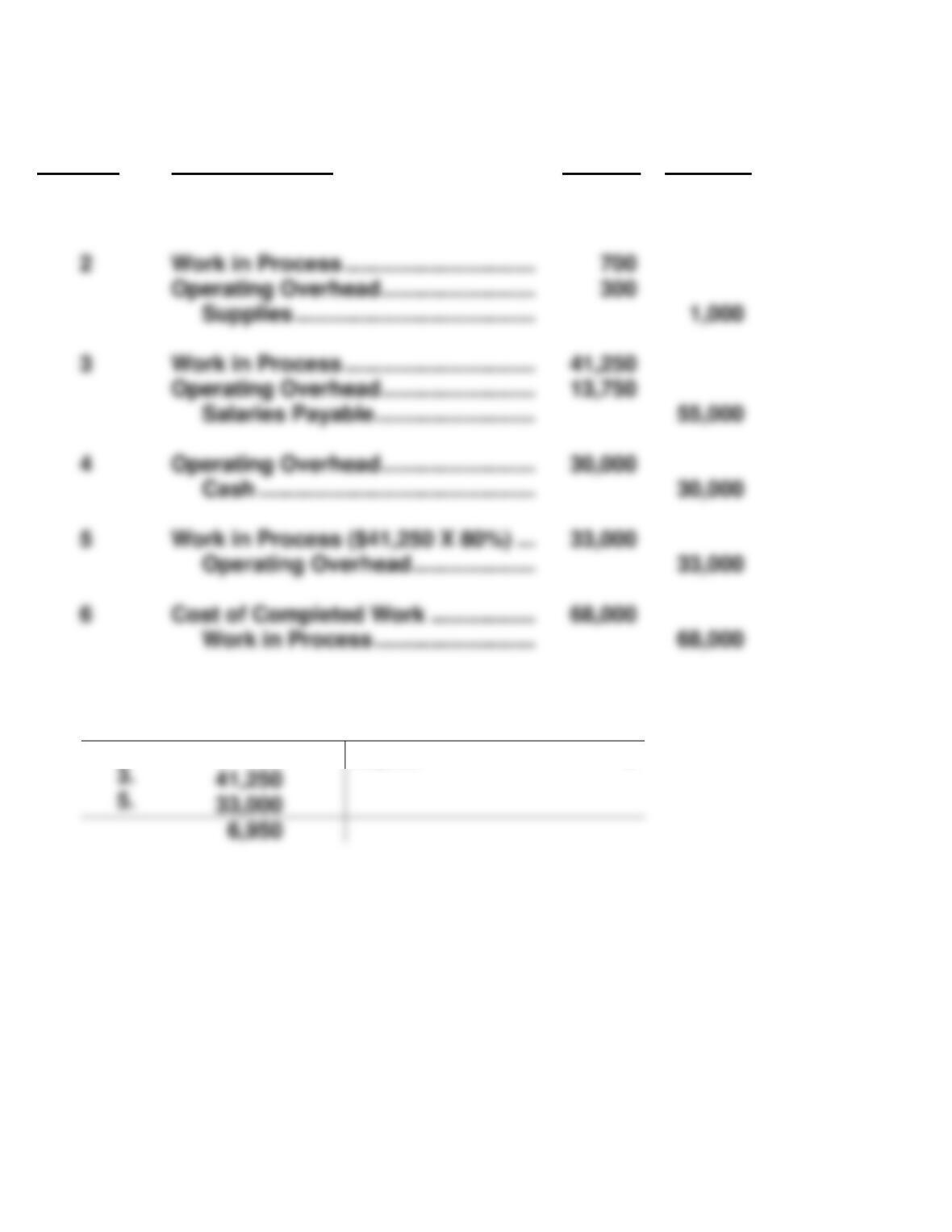

Work in Process

2.

700

68,000

6.

5.

Operating Overhead …………………….

Supplies …………………………………

3

Work in Process ………………………….

Operating Overhead …………………….

4

Operating Overhead …………………….

Cash ………………………………………

5

Work in Process ($41,250 X 80%) …

6

Cost of Completed Work ……………..

Work in Process ……………………..

EXERCISE 2-12B

(a)

Manson

Walker

Barton

Direct materials

$ 650

$ 350

$ 200

(b) The Barton job is the only incomplete job, therefore, $5,375.

(c) Applied overhead

$ 10,500 (CR)

Actual overhead

Balance

$ 500 (CR)

EXERCISE 2-13B

(a) Predetermined overhead rate = Budgeted overhead ÷ Budgeted

decorator hours

(b) Applied overhead

Work in Process (52,000 hrs X $17) …………….

884,000

Operating Overhead ………………………

884,000

(c)

Applied overhead

$ 884,000

Actual overhead

Balance

$ 5,000

overapplied

Auditor labor costs

Applied overhead

Total cost

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 2-1C

(a) $450,000 ÷ 20,000 direct labor hours = $22.50 per direct labor hour

(b) See solution to part (e) for job cost sheets

(c) Raw Materials Inventory ……………………………………. 46,000

Accounts Payable ……………………………………… 46,000

(d) Work in Process Inventory ………………………………… 33,000

Raw Materials Inventory

($5,000 + $15,000 + $13,000) ……………………. 33,000

PROBLEM 2-1C (Continued)

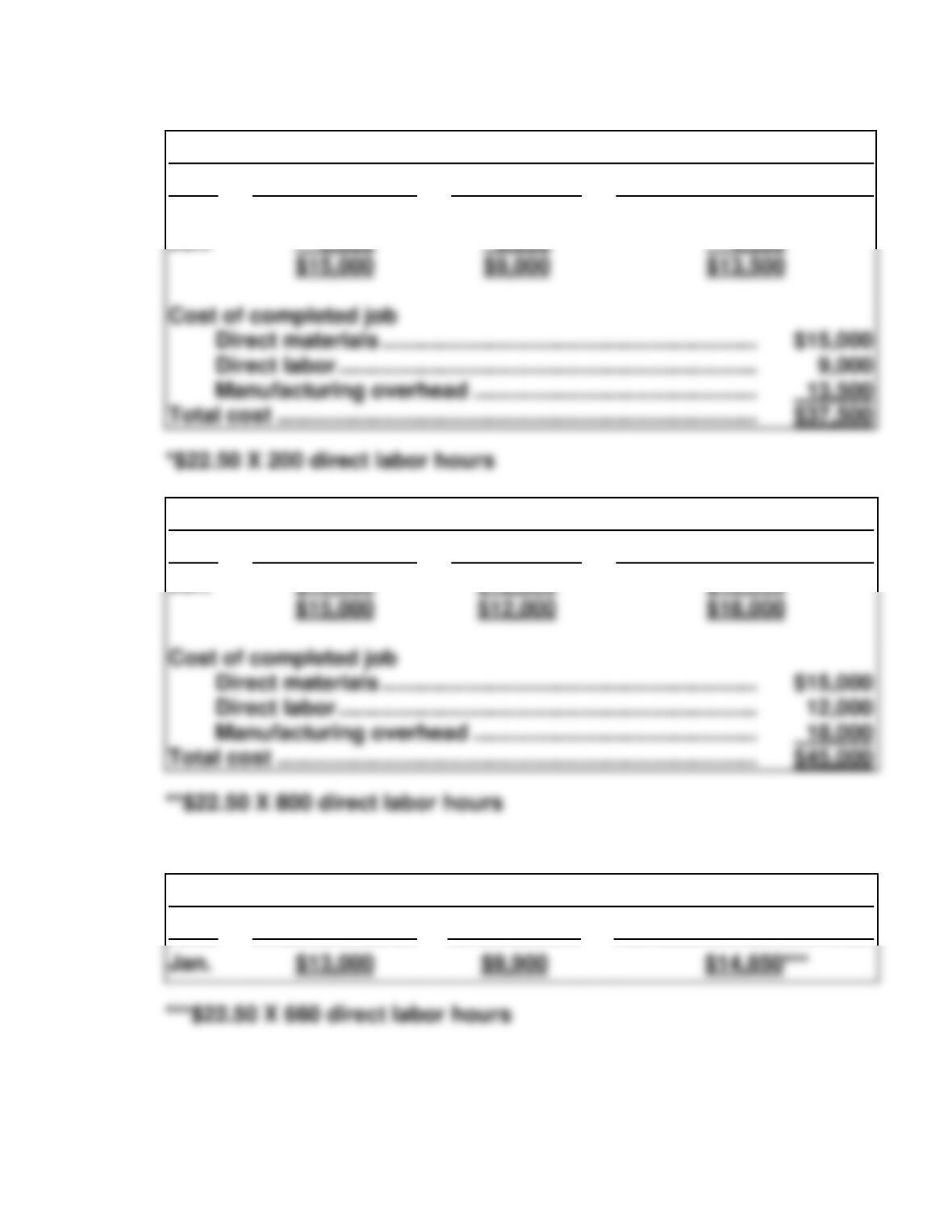

(e) Job Cost Sheets

Job No. 25

Date

Direct Materials

Direct Labor

Manufacturing Overhead

Beg.

Jan.

$10,000

5,000

$6,000

3,000

*$ 9,000*

* 4,500*

Job No. 26

Date

Direct Materials

Direct Labor

Manufacturing Overhead

Jan.

Direct labor ……………………………………………………….…. 12,000

Manufacturing overhead ………………………………………. 18,000

Total cost …………………………………………………………………… $45,000

$15,000

$12,000

**$18,000**

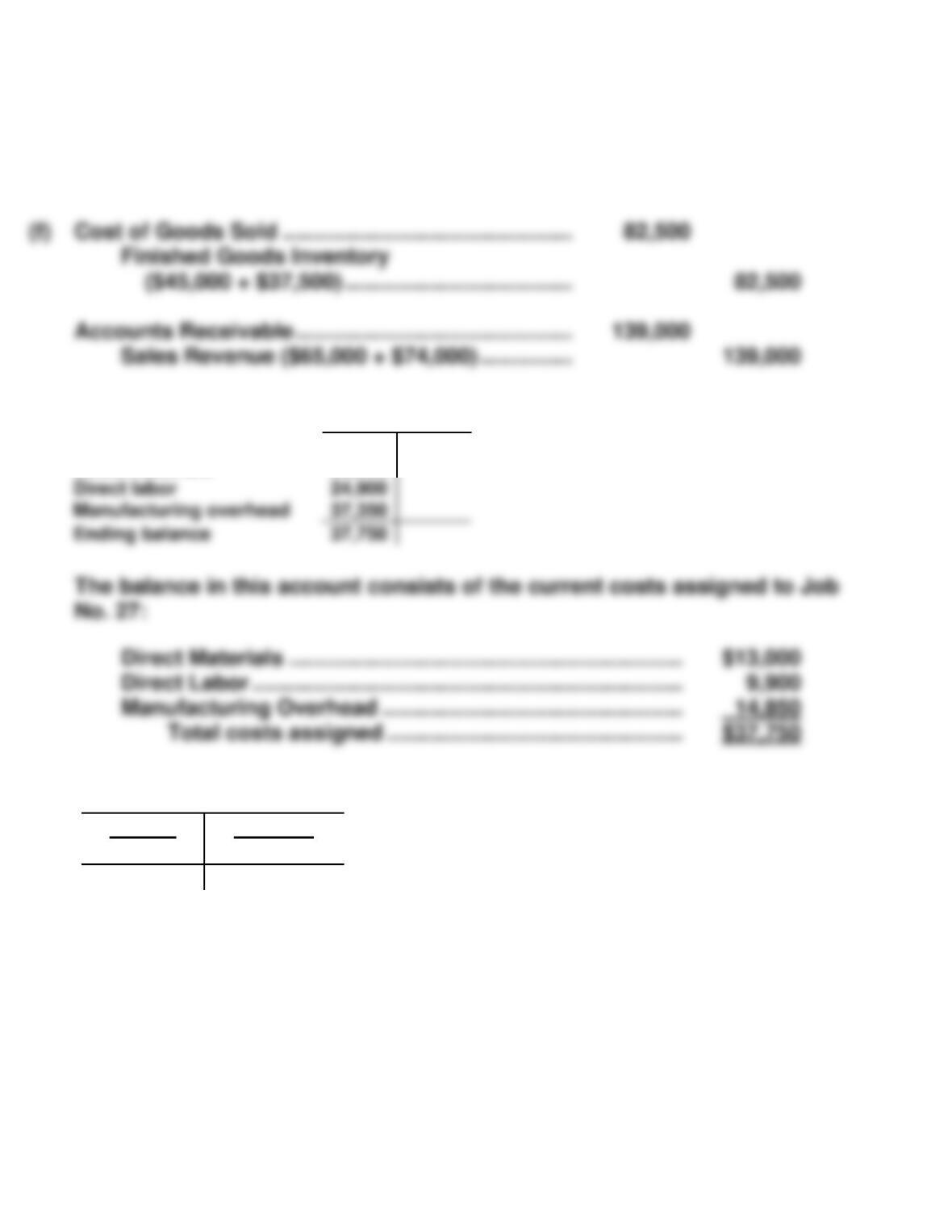

Job No. 27

Date

Direct Materials

Direct Labor

Manufacturing Overhead

Manufacturing overhead ………………………………………. 13,500

Total cost …………………………………………………………………… $37,500

PROBLEM 2-1C (Continued)

Finished Goods Inventory ………………………………. 82,500

Work in Process Inventory

($37,500 + $45,000) ………………………………. 82,500

(g)

Work in Process

Beginning balance

Direct materials

25,000

33,000

82,500

Cost of completed jobs 25 and 26

(h)

Manufacturing Overhead

Actual

40,500

Applied

37,350

3,150

The balance in the Manufacturing Overhead account is underapplied.

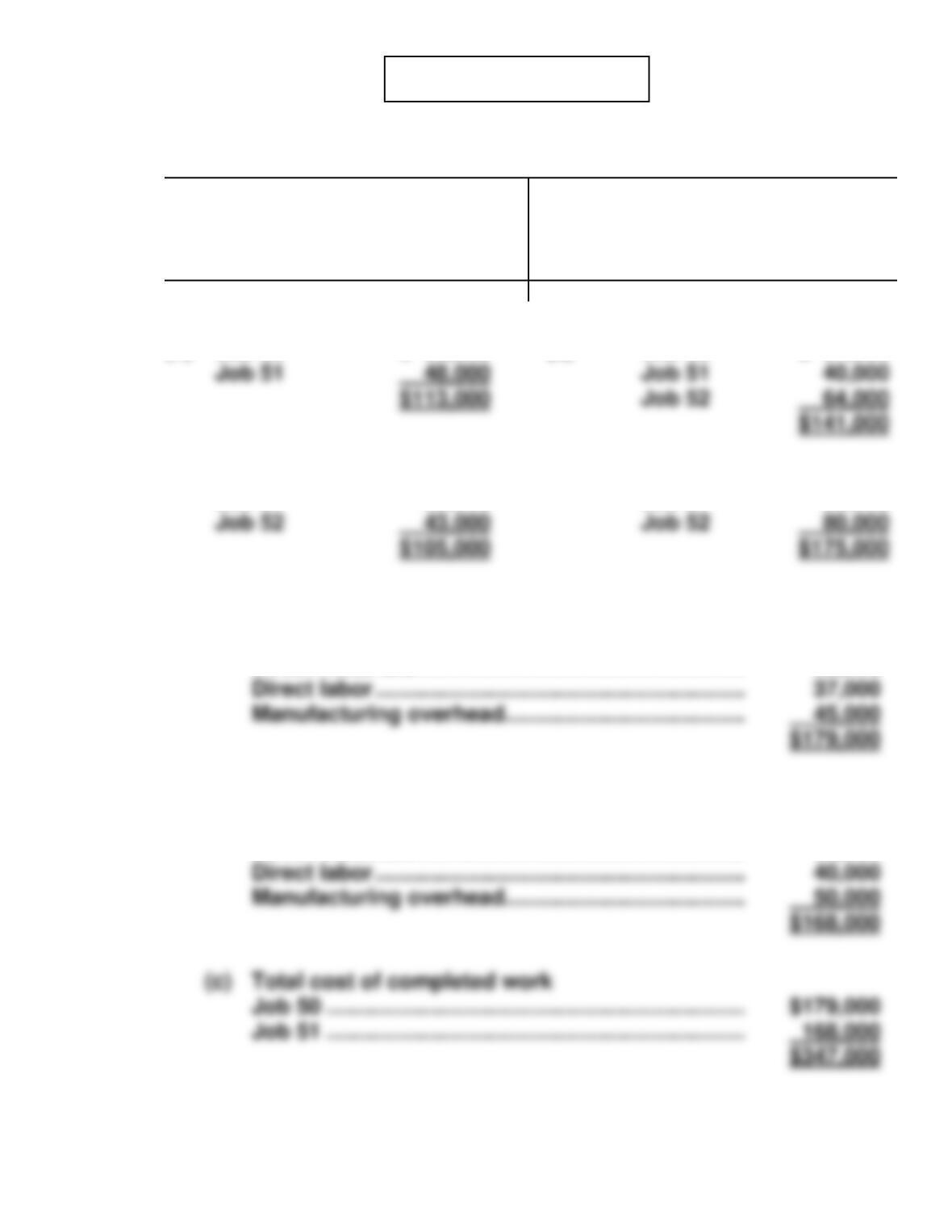

PROBLEM 2-2C

(a)

Work in Process Inventory

1/1 Balance (1) 113,000

Direct materials (2) 105,000

Direct labor (3) 141,000

Manufacturing overhead (4)

175,000

Completed work (5) (c) 347,000

12/31 Balance 187,000

(1)

Job 50

$ 65,000

(3)

Job 50

$ 37,000

(2)

Job 50

Job 51

$ 32,000

30,000

(4)

Job 50

Job 51

$ 45,000

50,000

(5) (a) Job 50

Beginning balance ………………………………………… $ 65,000

Direct materials …………………………………………….. 32,000

(b) Job 51

Beginning balance ………………………………………… $ 48,000

Direct materials …………………………………………….. 30,000

PROBLEM 2-2C (Continued)

Work in process balance ………………………………………… $187,000

Unfinished job No. 52 …………………………………………….. $187,000 (a)

(a) Current year’s cost

Direct materials ……………………… $ 43,000

Direct labor ……………………………. 64,000

(b) Actual overhead costs

Incurred on account ……………………………………….. $121,000

Indirect materials ……………………………………………. 12,000

Applied overhead costs

Job 50 ……………………………………………………………. $ 45,000

Job 51 ……………………………………………………………. 50,000

Actual overhead ……………………………………………………. $170,500

Manufacturing Overhead ……………………………………….. 4,500

Cost of Goods Sold ………………………………………… 4,500

(c) Sales (given) …………………………………………….. $500,000

Cost of goods sold

Add: Job 48 …………………………..………………… $ 87,000

Job 49 …………………………………………….. 65,000

PROBLEM 2-3C

(a)

(i) Raw Materials Inventory ……………………………………. 4,300

Accounts Payable ………………………………………. 4,300

(ii) Work in Process Inventory ………………………………… 5,500

Manufacturing Overhead …………………………………… 1,500

Raw Materials Inventory ……………………………… 7,000

(iii) Finished Goods Inventory …………………………………. 21,540

Work in Process Inventory ………………………….. 21,540

Job

Direct

Materials

Direct

Labor

Manufacturing

Overhead*

Total

Costs

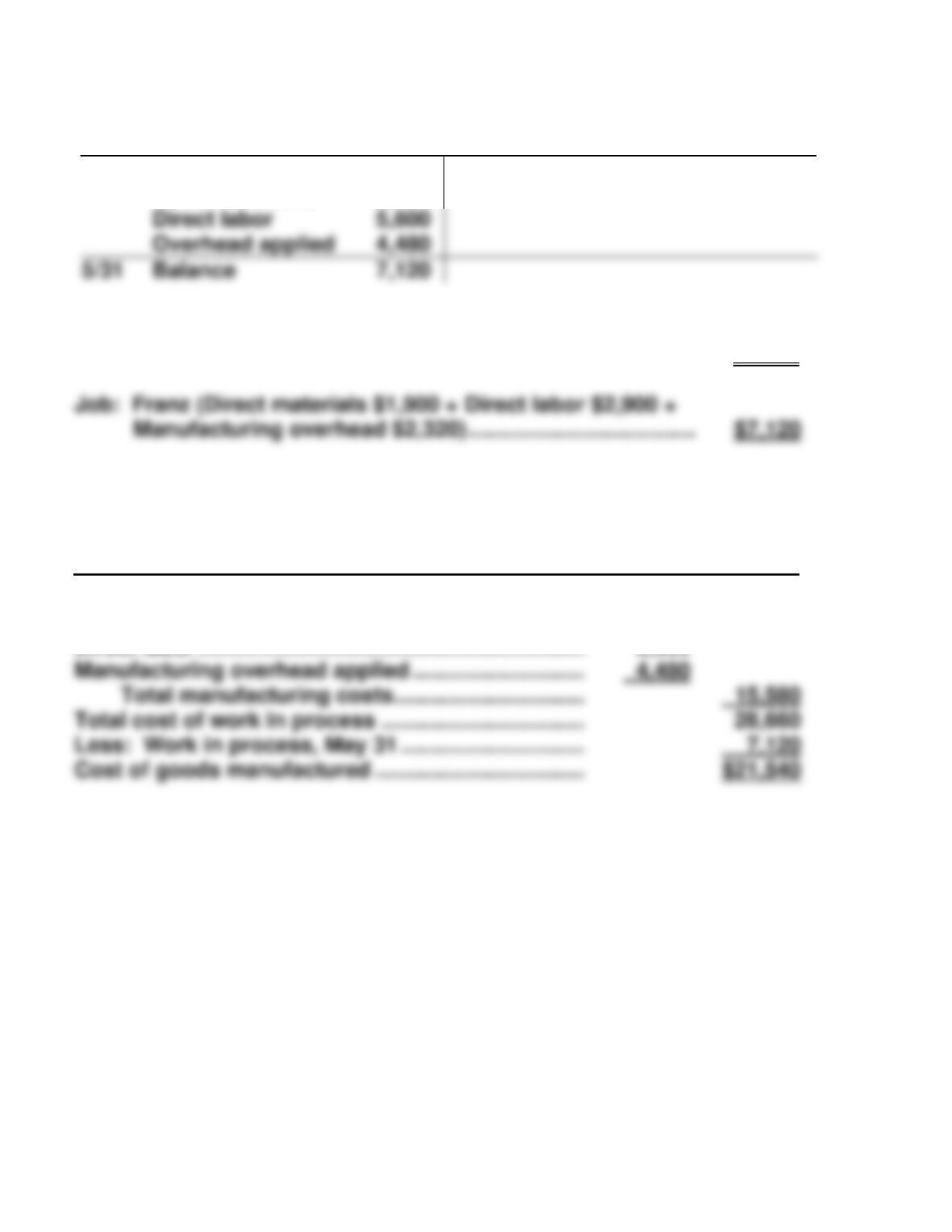

Clark

$3,100

$2,500

$2,000

$ 7,600

*80% of direct labor amount

Cash ………………………………………………………………… 45,000

Sales Revenue (3 X $15,000) ……………………….. 45,000

PROBLEM 2-3C (Continued)

(b)

Work in Process Inventory

5/1 Balance 13,080

Direct materials 5,500

5/31 Completed work 21,540

(c) Work in Process Inventory ……………………………………………….. $7,120

(d) VICTOR RAMOS COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended May 31, 2017

Work in process, May 1 ……………………………………. $13,080

Direct materials used ……………………………………….. $5,500

Direct labor ……………………………………………………… 5,600

Overhead applied 4,480

PROBLEM 2-4C

(a) Department A: $825,000 ÷ $550,000 = 150% of direct labor cost.

(b)

Department

Manufacturing Costs

A

B

C

Total

Direct materials

Direct labor

$ 92,000

52,000

$ 98,000

35,000

$ 64,000

50,400

(c)

Department

Manufacturing Overhead

A

B

C

Under (over) applied

Incurred

$ 76,000

$55,000

$92,000

PROBLEM 2-5C

(a) $89,000 ($78,000 + $11,000).

(b) $20,500 [($17,000 + $92,500) – $89,000 (See (a))].

(h) $153,000 (Given in other data).

(i) $336,700 (Same as (f)).