CHAPTER 2

A Further Look at Financial Statements

Learning Objectives

1. Identify the sections of a classified balance sheet.

2. Identify tools for analyzing financial statements and ratios for computing a company’s profitability.

3. Explain the relationship between a retained earnings statement and a statement of

stockholders’ equity.

4. Identify and compute ratios for analyzing a company’s liquidity and solvency using a

balance sheet.

5. Use the statement of cash flows to evaluate solvency.

6. Explain the meaning of generally accepted accounting principles.

7. Discuss financial reporting concepts.

Summary of Questions by Learning Objectives and Bloom’s Taxonomy

Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT

Questions

1. 1 K 6. 2, 4, 5 C 10. 4, 5 K 14. 7 C 18. 7 C

Brief Exercises

1. 1 K 4. 3 K 7. 6 K 9. 7 K 11. 7 K

Do It! Review Exercises

1. 1 AP 2. 1 AP 3. 4, 5 K 4. 7 K

Exercises

1. 1 AP 4. 1 AP 7. 2 AP 10. 4 AP 12. 7 K

Problems: Set A

1. 1 AP 3. 1, 3 AP 5. 2, 4,

7. 2, 4,

8. 6, 7 E

Problems: Set B

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A Prepare a classified balance sheet. Simple 10–20

2A Prepare financial statements. Moderate 20–30

8A Comment on the objectives and qualitative characteristics

of financial reporting.

Simple 10–20

1B Prepare a classified balance sheet. Simple 10–20

2B Prepare financial statements. Moderate 20–30

3B Prepare financial statements. Moderate 20–30

ANSWERS TO QUESTIONS

1. A company’s operating cycle is the average time that is required to go from cash to cash in prod-

ucing revenue.

2. Current assets are assets that a company expects to convert to cash or use up within one year of

the balance sheet date or the company’s operating cycle, whichever is longer. Current assets are

listed in the order in which they are expected to be converted into cash.

7. (a) Liquidity ratios: Working capital and current ratio.

(b) Solvency ratios: Debt to assets and free cash flow.

(c) Profitability ratio: Earnings per share.

Questions Chapter 2 (Continued)

10. (a) The increase in earnings per share is good news because it means that profitability has improved.

(b) An increase in the current ratio signals good news because the company improved its ability

11. (a) The debt to assets ratio and free cash flow indicate the company’s ability to repay the face

value of the debt at maturity and make periodic interest payments.

12. (a) Generally accepted accounting principles (GAAP) are a set of rules and practices, having

substantial support, that are recognized as a general guide for financial reporting purposes.

14. Jantz is correct. Consistency means using the same accounting principles and accounting

methods from period to period within a company. Without consistency in the application of

accounting principles, it is difficult to determine whether a company is better off, worse off, or the

same from period to period.

Questions Chapter 2 (Continued)

18. Accounting relies primarily on two measurement principles. Fair value is sometimes used when

market price information is readily available. However, in many situations reliable market price

information is not available. In these instances, accounting relies on historical cost as its basis.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 2-1

CL Accounts payable CL Income taxes payable

BRIEF EXERCISE 2-2

MORALES COMPANY

Partial Balance Sheet

Current assets

Cash ……………………………………………………………………………… $10,400

BRIEF EXERCISE 2-3

—

BRIEF EXERCISE 2-4

ICS (a) Issued new shares of common stock

DRE (b) Paid a cash dividend

BRIEF EXERCISE 2-5

Working capital = Current assets – Current liabilities

Current assets ($102,500,000

BRIEF EXERCISE 2-6

(a) Current ratio $262, 787

$293, 625 = 0.89:1

BRIEF EXERCISE 2-7

BRIEF EXERCISE 2-8

(a) Predictive value.

BRIEF EXERCISE 2-9

(a) Relevant.

BRIEF EXERCISE 2-10

(a) 1. Predictive value.

BRIEF EXERCISE 2-11

(c)

SOLUTIONS TO DO IT! REVIEW EXERCISES

DO IT! 2-1

LONYEAR CORPORATION

Balance Sheet (partial)

December 31, 2014

Assets

Current assets

Cash …………………………………………………………. $ 13,000

Accounts receivable ………………………………….. 22,000

DO IT! 2-2

IA Trademarks CA Inventory

DO IT! 2-3

(a) 2014 2013

(b) 2014 2013

C

urrent ratio $54,000 = 2.45:1 $36,000 = 1.20:1

$22,000 $30,000

(c)

Free cash flow 2014: $90,000 – $6,000 – $3,000 – $27,000 = $54,000

DO IT! 2-4

1. Monetary unit assumption

2. Faithful representation

SOLUTIONS TO EXERCISES

EXERCISE 2-1

CL Accounts payable CA Inventory

EXERCISE 2-2

CA Prepaid advertising IA Patents

EXERCISE 2-3

THE BOEING COMPANY

Partial Balance Sheet

December 31, 2014

(in millions)

Assets

Current assets

Cash …………………………………………………………….. $ 9,215

Debt investments ………………………………………….. 2,008

Long-term investments

Notes receivable ……………………………………………. 5,466

EXERCISE 2-4

H. J. HEINZ COMPANY

Partial Balance Sheet

April 30, 2014

(in thousands)

Assets

Current assets

Cash …………………………………………… $ 373,145

Accounts receivable ……………………. 1,171,797

EXERCISE 2-5

DONOVAN COMPANY

Balance Sheet

December 31, 2014

Assets

Current assets

Cash …………………………………………….. $11,840

Accounts receivable ……………………… 12,600

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………. $ 9,500

Current maturity of note payable …….. 13,600

Stockholders’ equity

Common stock ……………………………… 60,000

Retained earnings

EXERCISE 2-6

TEXAS INSTRUMENTS, INC.

Balance Sheet

December 31, 2014

(in millions)

Assets

Current assets

Cash ……………………………………………………………….. $ 1,182

Debt investments ……………………………………………… 1,743

Long-term investments

Property, plant, and equipment

Equipment ………………………………………………………. 6,705

Intangible assets

Patents …………………………………………………………….. 2,210

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………………………….. $1,459

Income taxes payable ……………………………………….. 128

Total current liabilities ……………………………….. $ 1,587

Long-term liabilities

EXERCISE 2-7

(a) Earnings per share = Net income Preferred dividends

Average common shares outstanding

—

(b) Using net income (loss) as a basis to evaluate profitability, Callaway

(c) To determine earnings per share, dividends on preferred stock are

EXERCISE 2-8

(a) BARFIELD CORPORATION

Income Statement

For the Year Ended July 31, 2014

Revenues

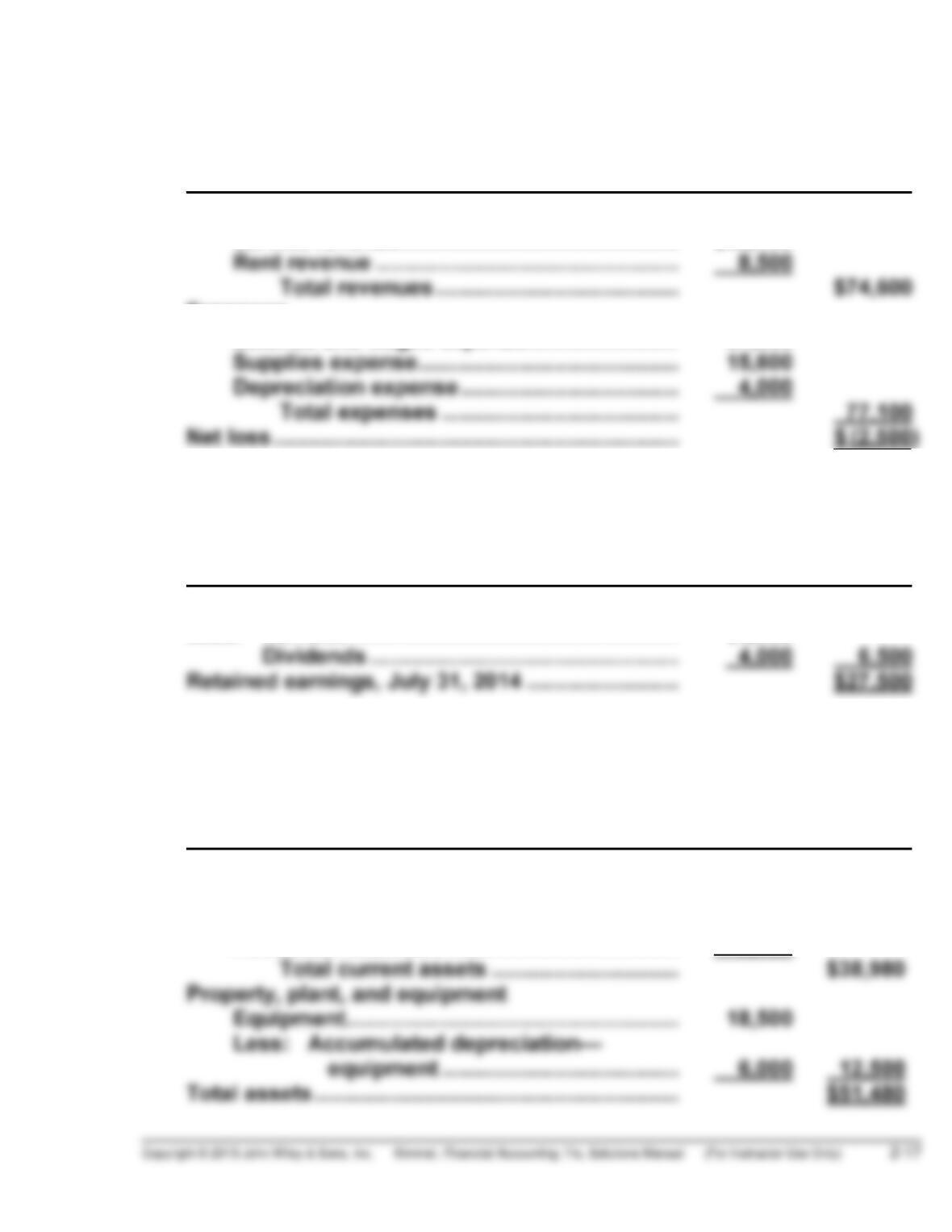

Service revenue………………………………………. $66,100

Expenses

Salaries and wages expense ……………………. 57,500

BARFIELD CORPORATION

Retained Earnings Statement

For the Year Ended July 31, 2014

Retained earnings, August 1, 2013 …………………. $34,000

Less: Net loss ……………………………………………… $2,500

(b) BARFIELD CORPORATION

Balance Sheet

July 31, 2014

Assets

Current assets

Cash ………………………………………………………. $29,200

Accounts receivable ……………………………….. 9,780

EXERCISE 2-8 (Continued)

(b) BARFIELD CORPORATION

Balance Sheet (Continued)

July 31, 2014

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ……………………………………… $ 4,100

Salaries and wages payable ………………………. 2,080

(c) Current ratio = $38, 980

$6,180 =6.3:1

(d) The current ratio would not change because equipment is not a current

asset and a 5-year note payable is a long-term liability rather than a

current liability.

The debt to assets ratio would increase from 15.5% to 39.1%*.

Looking solely at the debt to assets ratio, I would favor making the sale

because Barfield’s debt to assets ratio of 15.5% is very low. Looking at

EXERCISE 2-9

(a) Beginning of Year End of Year

(b) Nordstrom’s liquidity decreased slightly during the year. Its current

(c) Nordstrom’s current ratio at both the beginning and the end of the

recent year exceeds Best Buy’s current ratio for 2011 (and 2010).

EXERCISE 2-10

(a) Current ratio = $60,000

$30,000 =2.0:1

(b) Current ratio = $40, 000*

$10,000** =4.0:1

(c) Liquidity measures indicate a company’s ability to pay current obliga-

tions as they become due. Satisfaction of current obligations usually

EXERCISE 2-10 (Continued)

Payment of current obligations frequently requires cash. Neither work-

ing capital nor the current ratio indicate the composition of current

(d) The CFO’s decision to use $20,000 of cash to pay off accounts payable is

not in itself unethical. However, doing so just to improve the year-end

EXERCISE 2-11

2014 2013

(a) Current ratio $925,359 $1,020,834

2.30 : 1 2.71: 1

$401,763 $376,178

==

(e) Using the debt to assets ratio and free cash flow as measures of

solvency produces deteriorating results for American Eagle Outfitters.