Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

2–21 Ch. 2—Problems

Problem 2-2, Concluded

(3) Roland Company and Subsidiary Downes Company

Consolidated Balance Sheet

July 1, 2016

Assets

Current assets:

Other assets ......................................................................... $ 80,000*

Inventory (including $20,000 adjustment) ............................ 200,000

$ 280,000

Long-lived assets:

Land (including $50,000 increase) ....................................... $190,000

Liabilities and Stockholders’ Equity

Current liabilities ....................................................................... $ 240,000

Stockholders’ equity:

Common stock (par) ............................................................. $ 54,000

Paid-in capital in excess of par ............................................ 976,000

PROBLEM 2-3

(1) Investment in Entro Corporation ............................................... 400,000

Cash ..................................................................................... 400,000

(2) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ........................................... $400,000 $400,000 N/A

Problem 2-3, Concluded

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Price paid for investment ........... $400,000 $400,000 N/A

Less book value of interest acquired:

Common stock ($5 par) .......... $ 50,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($100,000 fair –

$80,000 book value) ............... $ 20,000 debit D1

Land ($40,500 fair – $40,000

book value) ............................. 500 debit D2

Building ($202,500 fair –

(3) Elimination entries:

Common Stock—Entro ............................................................. 50,000

Paid-In Capital in Excess of Par—Entro ................................... 250,000

2–23 Ch. 2—Problems

PROBLEM 2-4

(1) Investment in Express Corporation ........................................... 320,000

Cash ..................................................................................... 320,000

(2) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ........................................... $405,400** $320,000 $85,400*

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Price paid for investment ........... $405,400 $320,000 $ 85,400

Less book value of interest acquired:

Common stock ($10 par) ........ $ 50,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($100,000 fair –

$80,000 book value) ............... $ 20,000 debit D1

Land ($50,000 fair – $40,000

book value) ............................. 10,000 debit D2

Buildings ($200,000 fair –

Problem 2-4, Concluded

(3) Elimination entries:

Common Stock—Express ($50,000 × 80%) ............................. 40,000

Paid-In Capital in Excess of Par—Express ($250,000 × 80%) . 200,000

Retained Earnings—Express ($70,000 × 80%) ........................ 56,000

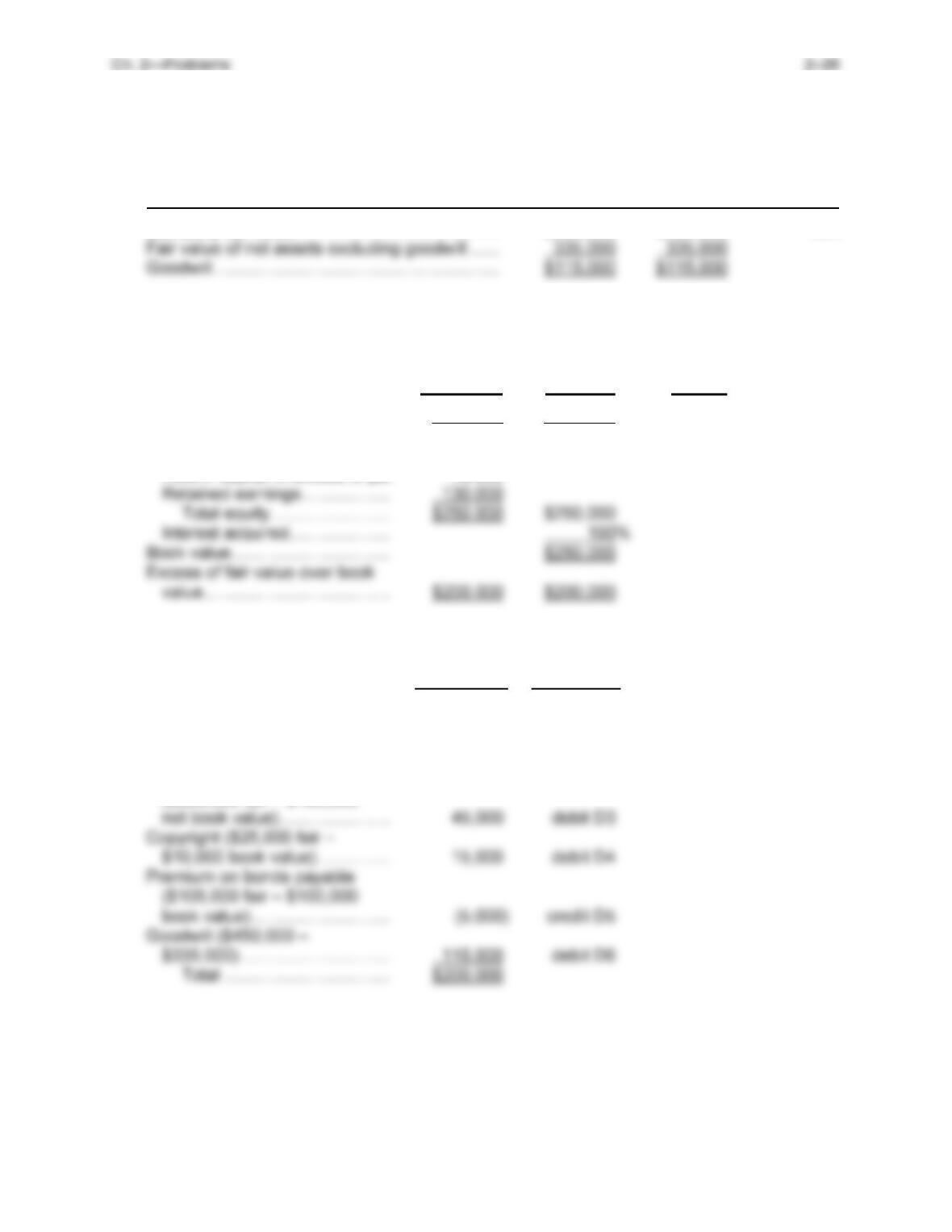

PROBLEM 2-5

(2) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ........................................... $480,000 $480,000 N/A

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary .............. $480,000 $480,000 N/A

Less book value of interest acquired:

Common stock ($5 par) .......... $ 50,000

Paid-in capital in excess of par 250,000

2–25 Ch. 2—Problems

Problem 2-5, Concluded

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($100,000 fair –

$80,000 book value) ............... $ 20,000 debit D1

Land ($55,000 fair – $40,000

(3) Inventory ................................................................................... 20,000

Land .......................................................................................... 15,000

Buildings ................................................................................... 20,000

© 2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

PROBLEM 2-6

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ........................................... $450,000 $450,000 N/A

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary .............. $450,000 $450,000 N/A

Less book value of interest acquired:

Common stock ($5 par) .......... $ 50,000

Paid-in capital in excess of par 70,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($140,000 fair –

$120,000 book value) ............. $ 20,000 debit D1

Land ($45,000 fair – $35,000

book value) ............................. 10,000 debit D2

Building and equipment

($225,000 fair – $180,000

2–27 Ch. 2—Problems

Problem 2-6, Concluded

(2) Aron Company and Subsidiary Shield Company

Worksheet for Consolidated Balance Sheet

December 31, 2015

Eliminations Consolidated

Balance Sheet and Adjustments Balance

Aron Shield Dr. Cr. Sheet

Cash ........................................... 185,000 40,000 ............. ............ 225,000

Accounts Receivable .................. 70,000 30,000 ............. ............ 100,000

Inventory..................................... 130,000 120,000 (D1) 20,000 ............ 270,000

Investment in Shield ................... 450,000 ............ ............. (EL) 250,000 ............

Eliminations and Adjustments:

(EL) Eliminate investment in subsidiary against subsidiary equity accounts.

(D) Distribute $200,000 excess of cost over book value to:

(D1) Inventory, $20,000.

(D3) Buildings and equipment, $45,000.

(D5) Premium on bonds payable, ($5,000).

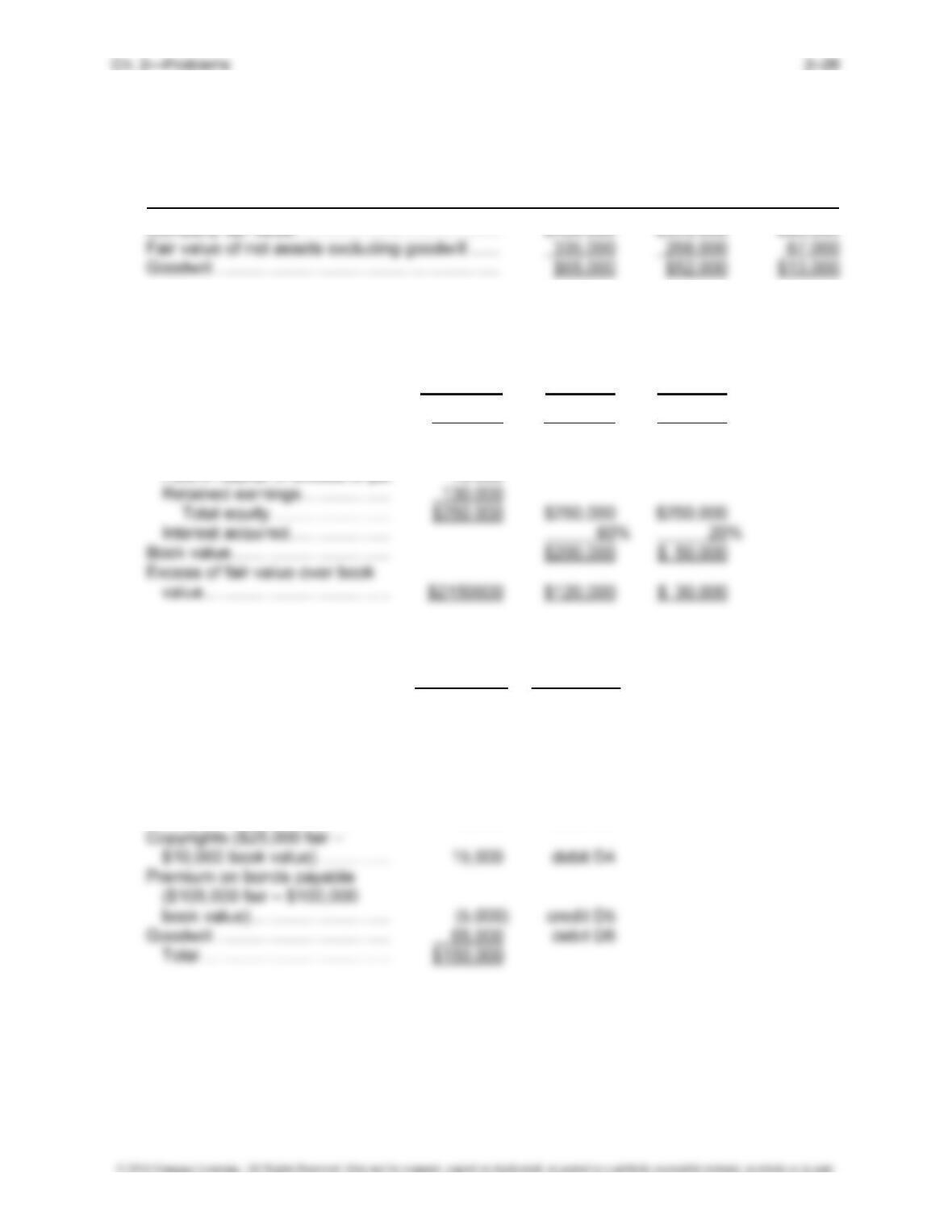

PROBLEM 2-7

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary .............. $400,000 $320,000 $ 80,000

Less book value of interest acquired:

Common stock ($5 par) .......... $ 50,000

Paid-in capital in excess of par 70,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($140,000 fair –

$120,000 book value) ............. $ 20,000 debit D1

Land ($45,000 fair – $35,000

book value) ............................. 10,000 debit D2

Buildings and equipment

($225,000 fair – $180,000

net book value) ....................... 45,000 debit D3

Problem 2-7, Concluded

(2) Aron Company and Subsidiary Shield Company

Worksheet for Consolidated Balance Sheet

December 31, 2015

Eliminations Consolidated

Balance Sheet

and Adjustments Balance

Aron Shield Dr. Cr. NCI Sheet

Cash ....................................... 315,000 40,000 ............. ............ ............ 355,000

Accounts Receivable .............. 70,000 30,000 ............. ............ ............ 100,000

Inventory ................................. 130,000 120,000 (D1) 20,000 ............ ............ 270,000

Investment in Shield ............... 320,000 ............ ............. (EL) 200,000 ............ ............

Eliminations and Adjustments:

(EL) Eliminate investment in subsidiary against 80% of the subsidiary equity accounts.

(D)/(NCI) Distribute $120,000 excess of cost over book value and $30,000 NCI adjustment to:

(D2) Land, $10,000.

(D4) Copyrights, $15,000.

(D6) Goodwill, $65,000.

Ch. 2—Problems 2–30

PROBLEM 2-8

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ........................................... $500,000 $500,000 N/A

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary .............. $500,000 $500,000 N/A

Less book value of interest acquired:

Common stock ($1 par) .......... $ 10,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($60,000 fair –

$50,000 book value) ............... $ 10,000 debit D1

Land ($80,000 fair – $40,000

book value) ............................. 40,000 debit D2

Buildings ($320,000 fair –

2–31 Ch. 2—Problems

Problem 2-8, Concluded

(2) Palto Company and Subsidiary Saleen Company

Worksheet for Consolidated Balance Sheet

January 1, 2015

Eliminations Consolidated

Balance Sheet

and Adjustments Balance

Palto Saleen Dr. Cr. Sheet

Cash ....................................... 61,000 ............ ............. ............ 61,000

Accounts Receivable .............. 65,000 20,000 ............. ............ 85,000

Current Liabilities .................... (80,000) (40,000) ............. ............ (120,000)

Bonds Payable ....................... (200,000) (100,000) ............. ............ (300,000)

Common Stock ($1 par)—

Saleen ................................. ............ (10,000) (EL) 10,000 ............ ............

Paid-In Capital in Excess of

Totals............................................................................................................................... 0

Eliminations and Adjustments:

(EL) Eliminate the investment in the subsidiary against the subsidiary equity accounts.

(D) Distribute $340,000 excess of cost over book value as follows:

(D1) Inventory, $10,000.

(D3) Buildings, $170,000.

(D5) Copyright, $50,000.

PROBLEM 2-9

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (100%) (0%)

Company fair value ........................................... $400,000 $400,000 N/A

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Price paid for investment ........... $400,000 $400,000 N/A

Less book value of interest acquired:

Common stock ($1 par) .......... $ 10,000

Paid-in capital in excess of par 90,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($60,000 fair –

$50,000 book value) ............... $ 10,000 debit D1

Land ($80,000 fair – $40,000

book value) ............................. 40,000 debit D2

Problem 2-9, Concluded

(2) Palto Company and Subsidiary Saleen Company

Worksheet for Consolidated Balance Sheet

January 1, 2015

Eliminations Consolidated

Balance Sheet

and Adjustments Balance

Palto Saleen Dr. Cr. Sheet

Cash ....................................... 161,000 ............ ............. ............ 161,000

Accounts Receivable .............. 65,000 20,000 ............. ............ 85,000

Inventory ................................. 80,000 50,000 (D1) 10,000 ............ 140,000

Investment in Saleen .............. 400,000 ............ ............. (EL) 160,000 ............

Common Stock ($1 par)—

Saleen ................................. ............ (10,000) (EL) 10,000 ............ ............

Paid-In Capital in Excess of

Par—Saleen ........................ ............ (90,000) (EL) 90,000 ............ ............

Retained Earnings—Saleen ... ............ (60,000) (EL) 60,000 ............ ............

Common Stock—Palto ........... (20,000) ............ ............. ............ (20,000)

Eliminations and Adjustments:

(EL) Eliminate the investment in the subsidiary against the subsidiary equity accounts.

(D) Distribute $240,000 excess of cost over book value as follows:

(D2) Land, $40,000.

(D4) Equipment, $20,000.

(D6) Gain on acquisition (close to Palto’s Retained Earnings), $50,000.

Ch. 2—Problems 2–34

PROBLEM 2-10

(1) Company Parent NCI

Implied Price Value

Value Analysis Schedule Fair Value (80%) (20%)

Company fair value ........................................... $492,000 $400,000 $92,000*

Fair value of net assets excluding goodwill ...... 450,000 360,000 90,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary .............. $492,000 $400,000 $ 92,000

Less book value of interest acquired:

Common stock ($1 par) .......... $ 10,000

Paid-in capital in excess of par 90,000

Adjustment of identifiable accounts:

Worksheet

Adjustment Key

Inventory ($60,000 fair –

$50,000 book value) ............... $ 10,000 debit D1

Land ($80,000 fair – $40,000

book value) ............................. 40,000 debit D2

Buildings ($320,000 fair –

$150,000 net book value) ....... 170,000 debit D3