33

CHAPTER 2

BASIC ACCOUNTING SYSTEMS: CASH BASIS

CLASS DISCUSSION QUESTIONS

1. The basic elements of a financial ac-

counting system include the following:

(1) a set of rules for determining what,

when, and how much should be recorded;

(2) a framework for preparing financial

statements; and (3) one or more controls

2. a. Purchase of land for cash affects

only assets.

b. Payment of a liability affects assets

and liabilities; receipt of cash for

fees earned affects assets and

stockholders’ equity.

c. Incurring an expense partially paid

in cash decreases assets increases

liabilities and decreases stockhold-

and decrease stockholders’ equity

(retained earnings) ($10,000). The

expense is an organizational ex-

pense. Likewise, a new business

might hire a new chief operating of-

ficer by agreeing to pay a nonre-

fundable, noncancellable signing

3. Out of balance. Assets are correct, but retained

earnings (utilities expense) should have been

decreased by $1,200 rather than $2,100. Thus,

retained earnings is understated by $900, and

total liabilities plus stockholders’ equity would be

less than total assets by $900.

liabilities are overstated by $7,000, and re-

tained earnings (fees earned) are understated

by $7,000; thus, the over- and understate-

ments offset each other, and the accounting

equation balances.

5. A primary control for determining the accuracy of

record keeping is the equality of the accounting

equation. The accounting equation must balance.

6. Total assets are increased by $175,000: an in-

crease in cash of $375,000 and a decrease in

come to stockholders and are not an ex-

pense.

8. a. The equality of the accounting equation

would not be affected. That is, the account-

ing equation would still balance.

b. On the income statement, total operating

expenses (salary expense) would be over-

34

9. a. The equality of the accounting equa-

tion would not be affected. That is,

the accounting equation would still

balance.

b. On the income statement, revenues

(fees earned) would be overstated

by $75,000, and net income would

activities, and thus, the net increase or

decrease in cash for the period is correct, as

is the ending cash balance.

10. a. $350,000 ($500,000 – $150,000)

b. Stockholders’ equity as of

December 31, 20Y8 …….. $400,000

Less stockholders’ equity as of

35

EXERCISES

E2–1

a. $950,000 ($357,500 + $592,500)

E2–2

Amounts in millions:

a. $47,323 ($92,033 – $44,710)

b. $6,075 increase ($3,756 + $2,319)

E2–3

Amounts in millions:

a. $1,533 ($7,837 – $6,304)

b. $112 increase ($223 – $111)

36

E2–4

(a) $193,437 ($241,272 – $47,835)

(b) $128,249 ($321,686 – $193,437)

(f) $221,656 [($214,047 + $7,609) or ($244,180 – $22,524)]

(g) $12,963 [($257,143 – $244,180) or ($20,572 – $7,609)]

E2–5

a. $825,000 ($1,200,000 – $375,000)

b. $895,000 ($825,000 + $150,000 – $80,000)

37

E2–6

a. (3) No effect

b. (3) No effect

f. (2) Decrease

g. (2) Decrease

E2–7

a. Increases assets and increases stockholders’ equity.

b. Decreases assets and decreases stockholders’ equity.

E2–8

1. Total assets decreased $140,000.

E2–9

1. (a) increase

4. (b) decrease

38

E2–10

1. (c)

2. (e)

6. (a)

7. (e)

E2–11

a. (1) Provided catering services for cash, $28,000.

(2) Purchased land for cash, $20,000.

b. $11,000 ($40,000 – $29,000)

c. $9,000 ($109,000 – $100,000)

d. $10,000 ($28,000 – $18,000)

E2–12

It would be incorrect to say the business incurred a net loss of $8,000. The excess

of the dividends over the net income for the period is a decrease in the amount of

retained earnings in the corporation.

39

E2–13

Company Sierra

Stockholders’ equity at end of year ($770,000 – $294,000) …..…………… $ 476,000

Deduct stockholders’ equity at beginning of year

($490,000 – $175,000) ………………………………………………………………… (315,000)

Net income (increase in stockholders’ equity) …………….……………… $ 161,000

Company Tango

Company Yankee

Increase in stockholders’ equity (as determined for Sierra) ……………… $ 161,000

Deduct issuance of additional common stock ………………..……………….. (75,000)

Net income ……………………………………………………………………………….. $ 86,000

Company Zulu

40

E2–14

In each case, solve for a single unknown, using the following equation:

Stockholders’ Equity (beginning) + Issuance of Common Stock – Dividends +

Revenues – Expenses = Stockholders’ Equity (ending)

Krypton: Stockholders’ equity at end of year ($350,000 – $110,000) … $ 240,000

Deduct stockholders’ equity at beginning of year

($250,000 – $130,000) ……………………………………………………………. (120,000)

Increase in stockholders’ equity ……………………………………… $ 120,000

Add dividends ………………………………………..………………………. 16,000

$ 136,000

Deduct additional issuance of common stock ………………….. (50,000)

Increase due to net income …………………………….……………….. $ 86,000

Add expenses ………………………………………………………………… 64,000

Revenue …………………………………………….……………………….. (b) $ 150,000

Radium: Stockholders’ equity at end of year ($248,000 – $136,000) … $ 112,000

Add decrease due to net loss ($112,000 – $128,000) ……….… 16,000

$ 128,000

Add dividends ………………………………………..………………………. 60,000

41

E2–15

Amounts in millions:

a. $(9,186) = $18,412 – $27,598

E2–16

a. ABBY’S INTERIORS

Balance Sheet

October 31, 20Y6

Assets

Cash ………………………………………………………………………. $ 50,000

Land ………………………………………………………………………. 500,000

Total assets ………………………………………….………………… $550,000

Liabilities

Notes payable ………………………………………………………… $200,000

42

E2–16, Concluded

ABBY’S INTERIORS

Balance Sheet

November 30, 20Y6

Assets

Cash ……………………………………………………………………… $ 175,000

Land ………………………………………………………………………. 575,000

Total assets ………………………………………….……………….. $ 750,000

Liabilities

Notes payable ………………………………………………………… $ 250,000

b. Retained earnings, November 30, 20Y6 …………………..…………………. $ 410,000

Less retained earnings, October 31, 20Y6 ………………………………….. (275,000)

Increase in retained earnings …………………………..………………………… $ 135,000

Add dividends ………………………………………………………………………….. 12,000

Net income ……………………………………………………………………………….. $ 147,000

c. Net cash flows from operating activities = $147,000 (The same as net income using

the cash basis.)

43

E2–17

WEST COAST DREAMS REALTY INC.

Income Statement

For the Month Ended June 30, 20Y9

Revenues:

Sales commissions ……………………………………..…………. $180,000

Expenses:

Salaries expense ……………………………………………………. $100,000

E2–18

WEST COAST DREAMS REALTY INC.

Statement of Stockholders’ Equity

For the Month Ended June 30, 20Y9

Common Stock Retained Earnings Total

Balances, June 1, 20Y9 ……………… $ 0 $ 0 $ 0

44

E2–19

WEST COAST DREAMS REALTY INC.

Balance Sheet

June 30, 20Y9

Assets

Cash ………………………………………………….……………………….. $ 86,000

Land ………………………………………………….……………………….. 200,000

Total assets ………………………………………………………………… $286,000

Liabilities

Notes payable ………………………………………….…………………. $100,000

E2–20

WEST COAST DREAMS REALTY INC.

Statement of Cash Flows

For the Month Ended June 30, 20Y9

Cash flows from (used for) operating activities:

Cash received from operating activities ………………….. $ 180,000

Cash paid for operating activities ……………………………. (140,000)

Net cash flows from operating activities ………………….. $ 40,000

45

E2–21

a. Decrease in assets and decrease in stockholders’ equity.

b. Increase in assets and decrease in assets.

f. Decrease in assets and decrease in stockholders’ equity.

g. Decrease in assets and decrease in stockholders’ equity.

h. Increase in assets, decrease in assets, and increase in stockholders’ equity.

l. Decrease in assets and decrease in stockholders’ equity.

E2–22

a. operating section

b. investing section

g. operating section

h. investing section

46

P2–1

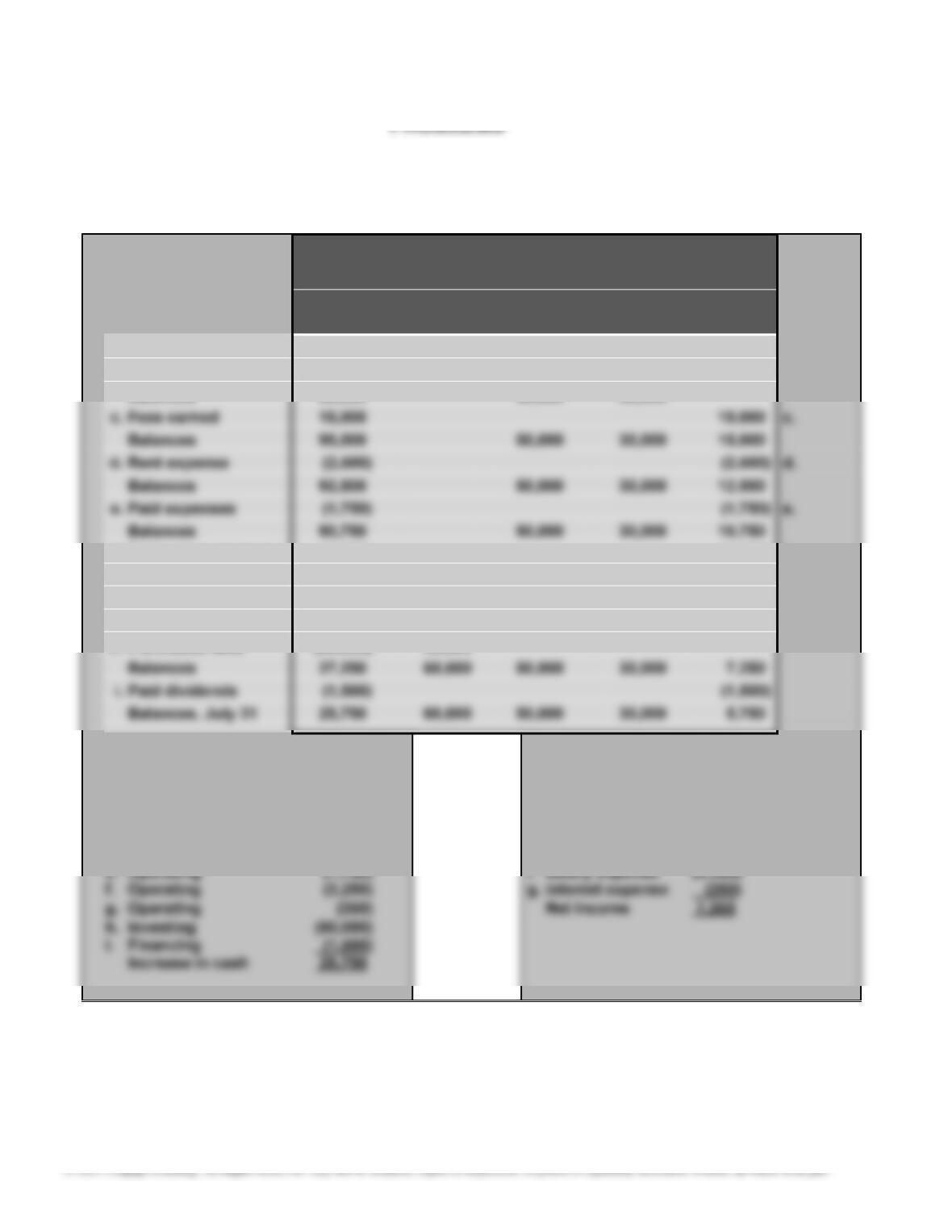

1.

Balance Sheet

Assets =Liabilities +Stockholders’ Equity

Notes Common Retained

Transaction Cash +Land =Payable +Stock + Earnings

a. Issued common stock 30,000 30,000

b. Issued note payable 50,000 50,000

f. Paid salary expense (3,250) (3,250) f.

Balances 87,500 50,000 30,000 7,500

g. Paid interest expense (250) (250) g.

Balances 87,250 50,000 30,000 7,250

Statement of Cash Flows Income Statement

a. Financin

g

30,000 c. Fees earned 15,000

b. Financing 50,000 d. Rent expense (2,500)

c. Operatin

g

15,000 e.

A

uto expense

(

1,250

)

d. Operatin

g

(

2,500

)

e. Misc. expense

(

500

)

g

(

)

(

)

(

)

g

(

)

2. Stockholders’ equity is the right of stockholders to the assets of the business.

These rights are increased by stockholders’ investments and revenues and

decreased by dividends and expenses.

47

P2–1, Continued

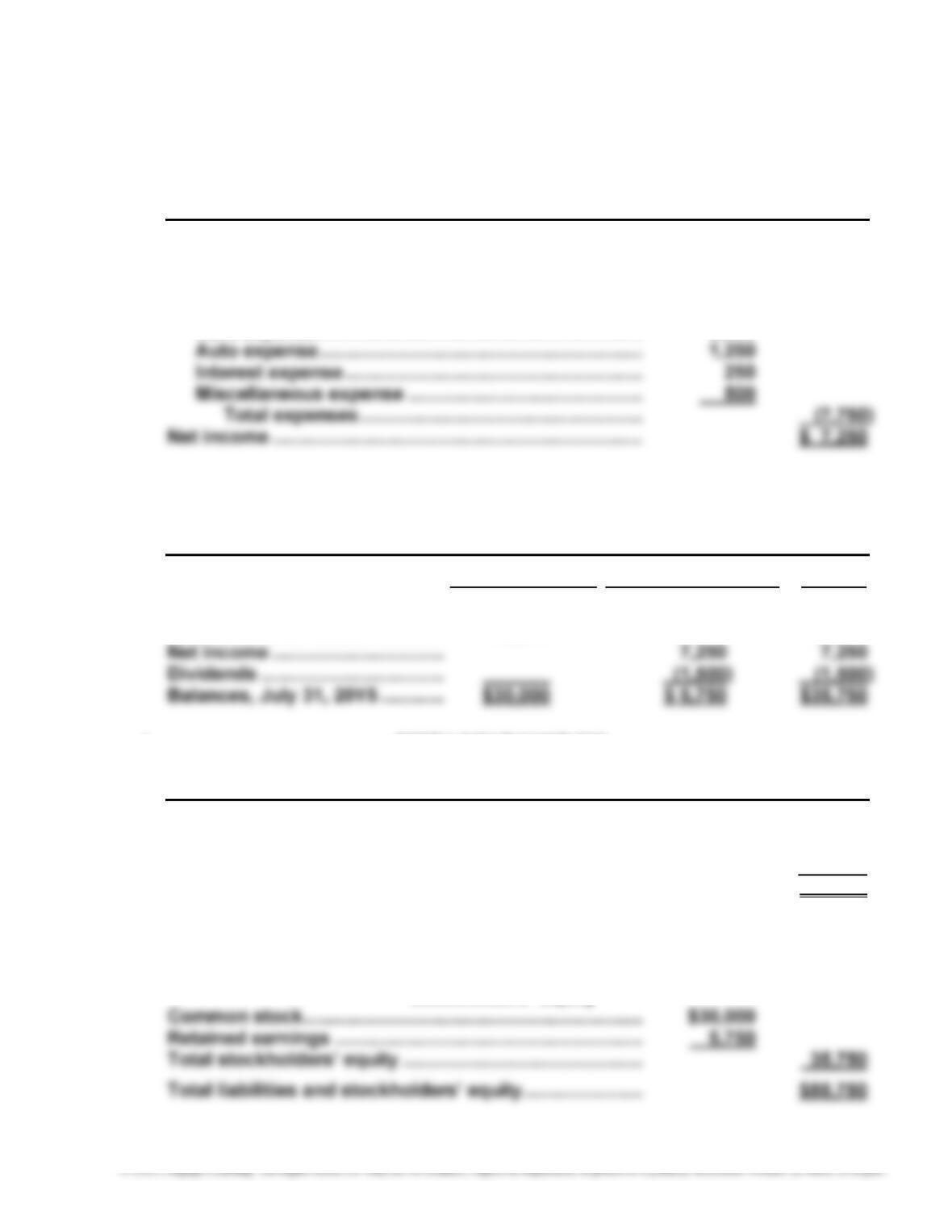

3. SMITH INSURANCE INC.

Income Statement

For the Month Ended July 31, 20Y5

Revenues:

Fees earned ………………………………………………………. $ 15,000

Expenses:

Salary expense ………………………………………………….. $3,250

SMITH INSURANCE INC.

Statement of Stockholders’ Equity

For the Month Ended July 31, 20Y5

Common Stock Retained Earnings Total

Balances, July 1, 20Y5 ………….. $ 0 $ 0 $ 0

Issued common stock …………… 30,000 30,000

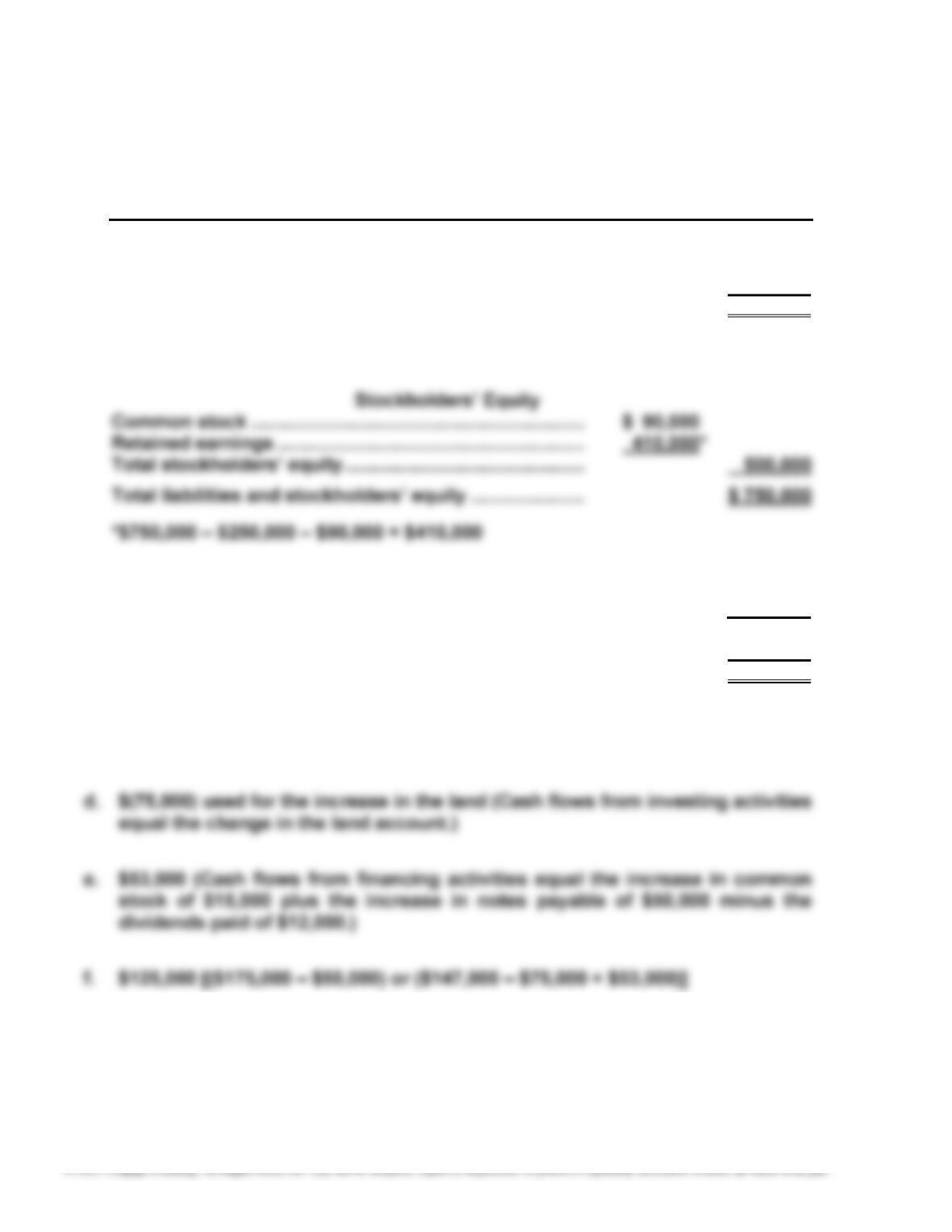

4. SMITH INSURANCE INC.

Balance Sheet

July 31, 20Y5

Assets

Cash ………………………………………………………………………. $25,750

Land ………………………………………………………………………. 60,000

Total assets ……………………………………………………………. $85,750

Liabilities

Notes payable ………………………………………………………… $50,000

48

P2–1, Concluded

5. SMITH INSURANCE INC.

Statement of Cash Flows

For the Month Ended July 31, 20Y5

Cash flows from (used for) operating activities:

Cash received from operating activities ……………… $15,000

Cash paid for operating activities …………………….... (7,750)

Net cash flows from operating activities …………….. $ 7,250

Cash flows from (used for) investing activities:

Cash paid for land ……………………………………………… (60,000)

49

1. RESTART TECHNOLOGY SERVICES

Income Statement

For the Month Ended August 31, 20Y4

Fees earned ……………………………………………………………. $54,000

Operating expenses:

Salaries expense ……………………………………………….. $9,200

2. RESTART TECHNOLOGY SERVICES

Statement of Stockholders’ Equity

For the Month Ended August 31, 20Y4

Common Stock Retained Earnings Total

Balances, Aug. 1, 20Y4 …………. $ 0 $ 0 $ 0

Issued common stock …………… 50,000 50,000

3. RESTART TECHNOLOGY SERVICES

Balance Sheet

August 31, 20Y4

Assets

Cash ………………………………………………………………………. $ 20,000

Land ………………………………………………………………………. 80,000

Total assets ………………………………………….………………… $ 100,000

Liabilities