Chapter 02 – The Accounting Cycle: During the Period

Chapter 2

The Accounting Cycle: During the Period

INSTRUCTOR’S MANUAL

Authors’ Perspectives

PART A: Measuring Business Activities

LO2-1 Identify the basic steps in measuring external transactions.

Begin with the Basics: A = L + SE – Start slowly with just the basic accounting equation. In

Part A, students are given 10 external transactions for Eagle Soccer Academy. The transactions

are listed in an intentional order. The first five transactions involve accounts affecting only the

Expand the Accounting Equation – The final five transactions are used to help students

understand the effects of revenues, expenses, and dividends on retained earnings in the expanded

accounting equation.

Understanding how and why transactions involving revenues, expenses, and dividends affect

retained earnings is a difficult concept at first for many students. To help make this concept

easier, instructors can begin by explaining the simpler concept that a company’s equity is

Chapter 02 – The Accounting Cycle: During the Period

PART B: Debits and Credits

LO2-3 Assess whether the impact of external transactions results in a debit or credit to an

account balance.

“The very day a debit is born, it has a twin credit” – These words were written by Luca

Pacioli in his original Summa de Arithmetica, Geometria, Proportioni et Proportionalita. We can

present debits and credits as the language of accounting (or the terminology used to indicate an

increase or decrease in accounts). A journal entry is the sentence form of the accounting

language. Just like an English sentence has proper format, so does an accounting sentence.

✓ An English sentence requires at least one noun and one verb, and there is noun-verb

Part B shows students how to record transactions in a journal using debits and credits with

the same 10 transactions that were covered in Part A. This helps students draw the connection

between the effects of transactions on account balances and recording debits and credits.

• Illustration 2-6 is the debit-credit version of Illustration 2-3 and shows students how

debits and credits are used in the expanded accounting equation.

Aggregation of Measurements – To demonstrate the process of aggregation of individual

Chapter 02 – The Accounting Cycle: During the Period

transactions to compute a single ending account balance, the chapter ends with a full summary of

Cash account are posted to the credit side of the general ledger account, reducing the balance.

Self-Study Materials

■ Let’s Review—Effects of transactions on the accounting equation (p. 70).

■ Let’s Review—Effects of debits and credit on account balances (p. 73).

Chapter 02 – The Accounting Cycle: During the Period

Key Points by Learning Objective

Throughout the chapter, Key Points provide quick synopses of the critical pieces of information

LO2-1 Identify the basic steps in measuring external transactions.

External transactions are transactions between the company and separate economic entities.

Internal transactions do not include an exchange with a separate economic entity.

LO2-2 Analyze the impact of external transactions on the accounting equation.

After each transaction, the accounting equation must always remain in balance. In other words,

LO2-3 Assess whether the impact of external transactions results in a debit or credit to an

account balance.

For the basic accounting equation (Assets = Liabilities + Stockholders’ Equity), assets (left side)

increase with debits. Liabilities and stockholders’ equity (right side) increase with credits. The

LO2-4 Record transactions in a journal using debits and credits.

For each transaction, total debits must equal total credits.

LO2-5 Post transactions to the general ledger.

LO2-6 Prepare a trial balance.

Chapter 02 – The Accounting Cycle: During the Period

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO2-1

Understand the difference between external and

internal transactions

5

2

LO2-1

List steps to measure external transactions

5

3

LO2-2

Explain the dual effect of transactions

5

4

LO2-2

Describe the impact of transactions on the

accounting equation

5

5

LO2-2

Explain the dual effect of transactions

5

6

LO2-3

Identify normal accounting balances

5

7

LO2-3

Understand the effects of debits and credits on

account balances

5

8

LO2-3

Determine whether a debit or credit increases an

account balance

5

9

LO2-3

Determine whether a debit or credit decreases an

account balance

5

LO2-3

Explain the relation between retained earnings and

its revenue and expense components

5

LO2-4

Describe a journal and a journal entry

5

LO2-4

Explain why debits equal credits

5

LO2-4

Record transactions

5

LO2-4

Describe recorded transactions

5

LO2-5

Explain a T-account

5

LO2-5

Post transactions

5

LO2-5

Describe a general ledger

5

LO2-6

Describe a trial balance

5

LO2-6

Understand total debits and total credits in a trial

balance

5

Chapter 02 – The Accounting Cycle: During the Period

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE2-1

LO2-1

List steps in the measurement process

5

BE2-2

LO2-2

Balance the accounting equation

5

BE2-3

LO2-2

Balance the accounting equation

LO2-2

Analyze the impact of transactions on the

accounting equation

10

LO2-3

Understand the effect of debits and credits on

10

LO2-3

Understand the effect of debits and credits on

accounts

10

BE2-7

LO2-4

Record transactions

BE2-8

LO2-4

Record transactions

BE2-9

LO2-5

Analyze T-accounts

Analyze the impact of transactions on the

accounting equation, record transactions, and post

10

LO2-6

Prepare a trial balance

LO2-6

Correct a trial balance

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E2-1

LO2-1

Identify terms associated with the measurement

process

5

E2-2

LO2-2

Analyze the impact of transactions on the

accounting equation

5

E2-3

LO2-2

Analyze the impact of transactions on the

accounting equation

10

E2-4

LO2-2

Analyze the impact of transactions on the

accounting equation

5

LO2-2

Understand the components of retained earnings

LO2-3

Indicate the debit or credit balance of accounts

E2-7

LO2-3

Associate debits and credits with external

transactions

5

LO2-4

Record transactions

LO2-4

Identify transactions

5

LO2-4

Record transactions

LO2-4

Record transactions

LO2-4

Correct recorded transactions

LO2-4

Correct recorded transactions

LO2-5

Post transactions to Cash T-account

LO2-5

Post transactions to T-accounts

LO2-5

Identify transactions

LO2-6

Prepare a trial balance

LO2-6

Prepare a trial balance

Chapter 02 – The Accounting Cycle: During the Period

a trial balance

LO2-4, 2-5, 2-6

Record transactions, post to T-accounts, and prepare

a trial balance

30

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P2-1A

LO2-2

Analyze the impact of transactions on the

accounting equation

10

P2-2A

LO2-2

Analyze the impact of transactions on the

accounting equation

15

P2-3A

LO2-3

Identify the type of account and its normal debit or

credit balance

15

Record transactions

P2-5A

Analyze the impact of transactions on the

accounting equation and record transactions

30

Prepare a trial balance

P2-7A

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

45

P2-8A

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

50

transactions

P2-1B

LO2-2

Analyze the impact of transactions on the

accounting equation

10

P2-2B

LO2-2

Analyze the impact of transactions on the

accounting equation

15

P2-3B

LO2-3

Identify the type of account and its normal debit or

credit balance

15

Record transactions

P2-5B

Analyze the impact of transactions on the

accounting equation and record transactions

30

Prepare a trial balance

P2-7B

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

45

P2-8B

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

50

P2-9B

LO2-4, 2-5, 2-6

Complete the steps in the measurement of external

transactions

60

Chapter 02 – The Accounting Cycle: During the Period

Additional

Perspectives

Topic

Time

(Min.)

AP2-1

Continuing Problem: Great Adventures

45

AP2-2

Financial Analysis: American Eagle Outfitters, Inc.

15

Buckle, Inc.

Chapter 02 – The Accounting Cycle: During the Period

Alternate Let’s Review

Problem #1

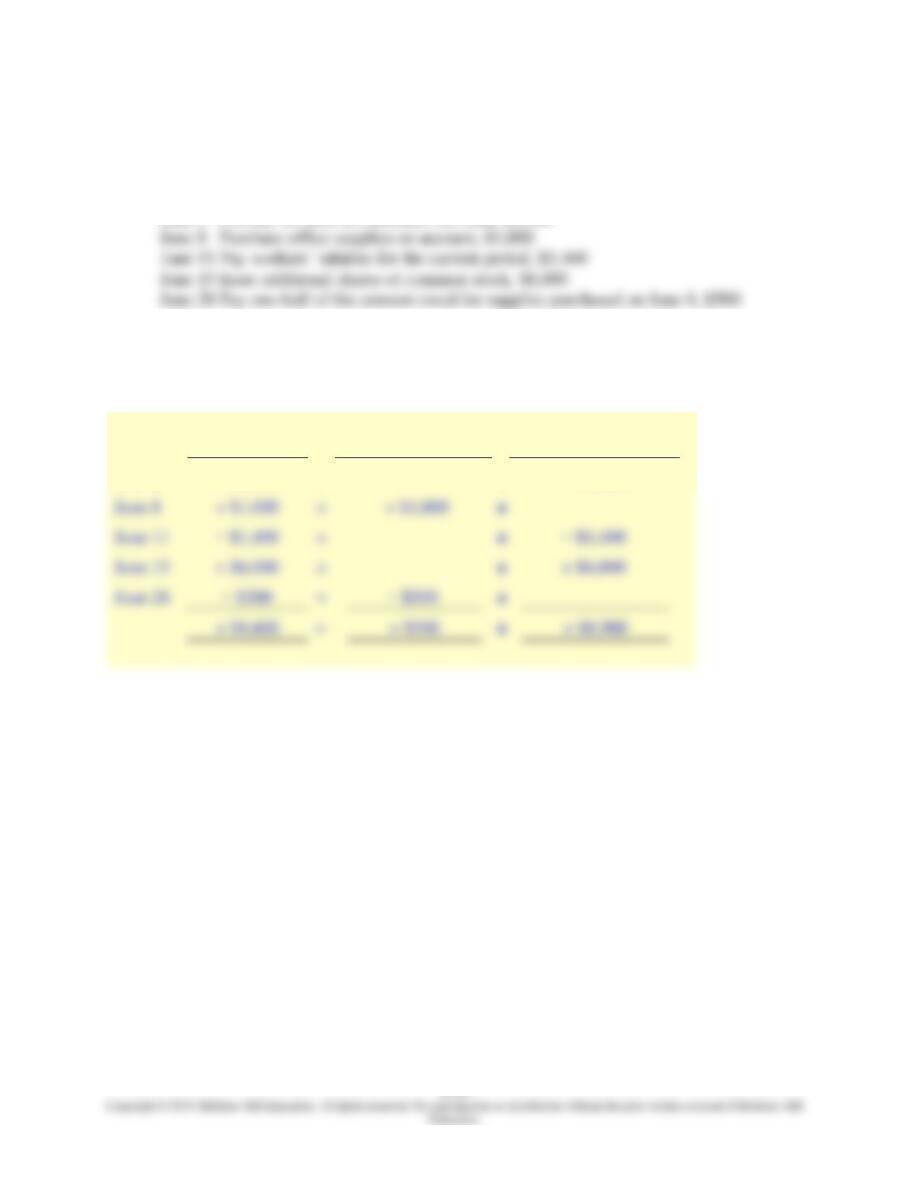

A company has the following transactions during June:

June 2 Provide services to customers for cash, $4,300

Required:

Indicate how each transaction affects the accounting equation.

Solution:

Assets

=

=

Liabilities

+

+

Stockholders’ Equity

June 2

+ $4,300

=

+

+ $4,300

June 8

+ $1,000

=

June 11

=

+

June 15

+ $6,000

=

+ $6,000

June 28

=

+

+ $9,400

=

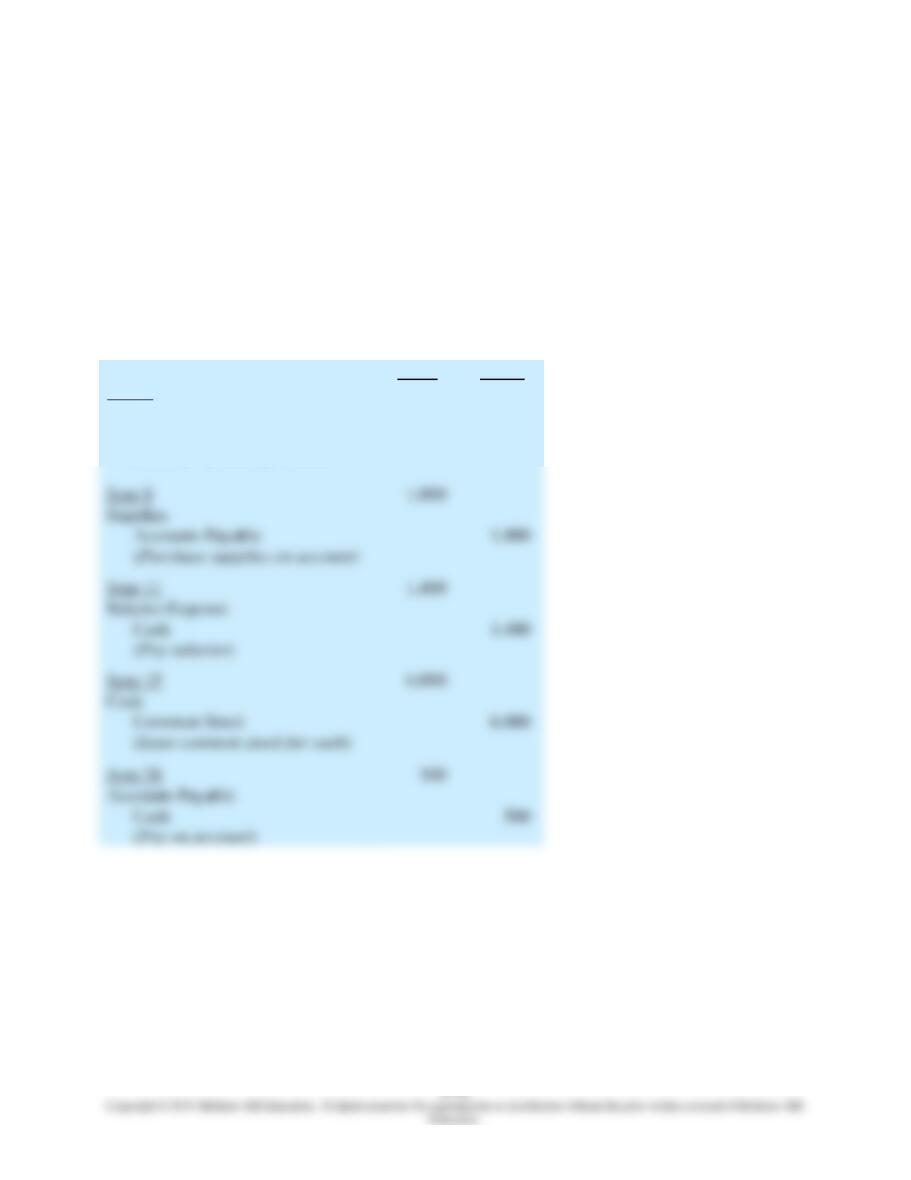

Problem #2

A company has the following transactions during June:

June 2 Provide services to customers for cash, $4,300

June 8 Purchase office supplies on account, $1,000

Solution:

Date

(1)

Accounts Involved

(2)

Account Type

(3)

Increase or

Decrease

(4)

Debit or Credit

June 2

Cash

Asset

Increase

Debit

Service Revenue

Revenue

Increase

Credit

June 8

Supplies

Asset

Increase

Debit

June 11

Salaries Expense

Expense

Increase

Debit

Cash

Asset

Decrease

Credit

June 15

Cash

Asset

Increase

Debit

June 28

Accounts Payable

Liability

Decrease

Debit

Cash

Asset

Decrease

Credit

Chapter 02 – The Accounting Cycle: During the Period

Problem #3

A company has the following transactions during June:

June 2 Provide services to customers for cash, $4,300

June 8 Purchase office supplies on account, $1,000

June 11 Pay workers’ salaries for the current period, $1,400

June 15 Issue additional shares of common stock, $6,000

June 28 Pay one-half of the amount owed for supplies purchased on June 8, $500

Required:

Record each transaction.

Solution:

Debit

Credit

June 2

Cash

4,300

Service Revenue

(Provide services for cash)

4,300

June 8

Supplies

June 11

Salaries Expense

June 15

Cash

June 28

Accounts Payable

Chapter 02 – The Accounting Cycle: During the Period

Common Mistakes

Common Mistakes made by students are highlighted in each of the chapters. With greater

awareness of the potential pitfalls, students can avoid making the same mistakes and gain a

deeper understanding of the chapter material.

Common Mistake

It’s sometimes tempting to decrease cash as a way of recording an investor’s initial investment.

However, we account for transactions from the company’s perspective, and the

company received cash from the stockholder—an increase in cash.

Common Mistake

Common Mistake

Students often believe a payment of dividends to owners increases stockholders’ equity.

Remember, you are accounting for the resources of the company. While stockholders have more

personal cash after dividends have been paid, the company in which they own stock has

fewer resources (less cash).

Common Mistake

Common Mistake

Common Mistake

Students sometimes hear the phrase “assets are the debit accounts” and believe it indicates that

assets can only be debited. This is incorrect! Assets, or any account, can be either debited or

Chapter 02 – The Accounting Cycle: During the Period

Common Mistake

Just because the debits and credits are equal in a trial balance does not necessarily mean that all

Chapter 02 – The Accounting Cycle: During the Period

Decision Points

Decision Points are provided in each chapter to give insight into how measurement and

communication of financial accounting information help decision makers.

Decision Points

Question

Accounting Information

Analysis

How much profit has

a company earned

business?

Retained earnings

The balance of retained earnings

provides a record of all revenues and

Question

Accounting Information

Analysis

transactions?

them in a trial balance.

How does the

Journal entries

The effects of external transactions

Chapter 02 – The Accounting Cycle: During the Period

Posting Transactions of Eagle Soccer Academy to the Cash General Ledger Account (Learning Objective 2-5)

Illustration 2-11

Cash account from Illustration 2-12

Account: Cash

Date

Description

Debit

Credit

Balance

Dec. 1

Beginning balance

0

Dec. 1

Issue common stock for cash

25,000

25,000

Dec. 1

Borrow by signing three-year note

10,000

35,000

Dec. 1

Purchase equipment for cash

11,000

Dec. 1

Prepay rent with cash

Dec. 12

Provide training to customers for cash

Dec. 23

Receive cash in advance from customers

Dec. 28

Pay salaries to employees

Dec. 30

Pay cash dividends

Post